Outperformance by global indexes bodes well for a new cyclical upswing in stocks

Key points:

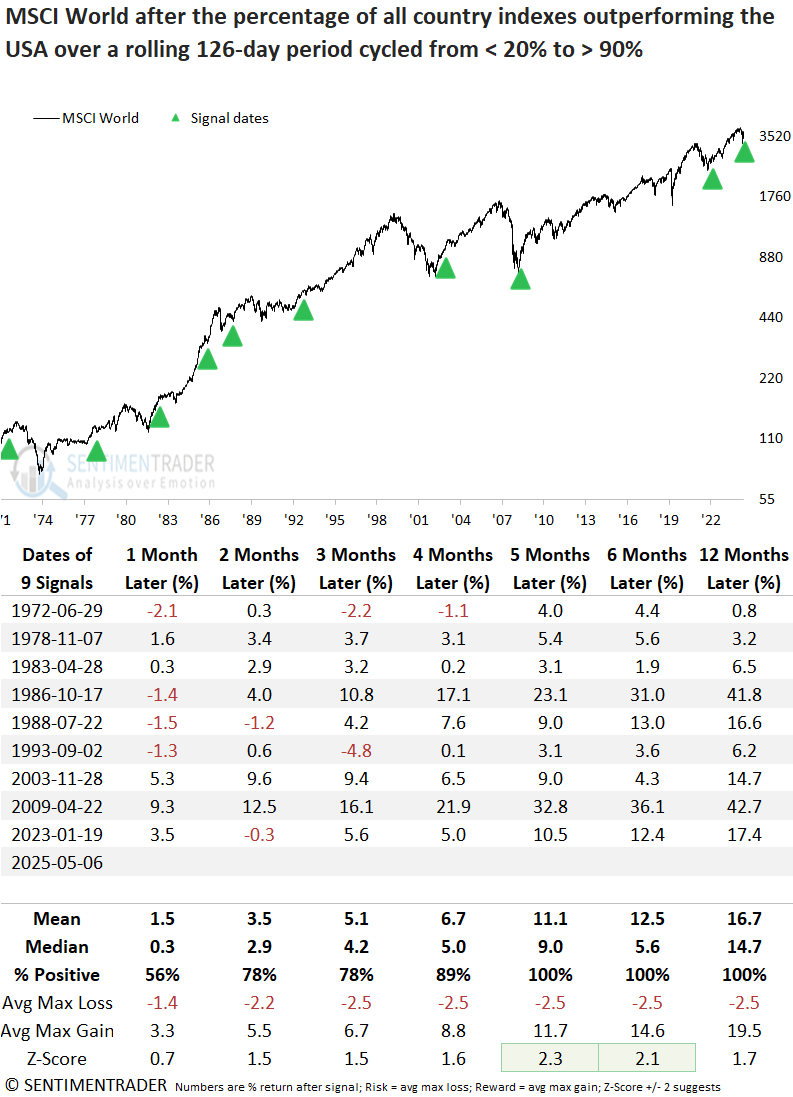

- Over the last six months, more than 90% of MSCI country indexes have outperformed the USA

- Similar relative trends led to gains in a global index 100% of the time over the next five, six, and twelve months

- The S&P 500 rose 100% of the time over the following six months and outperformed a world index

The beginning of sustained global equity leadership, or a classic head fake?

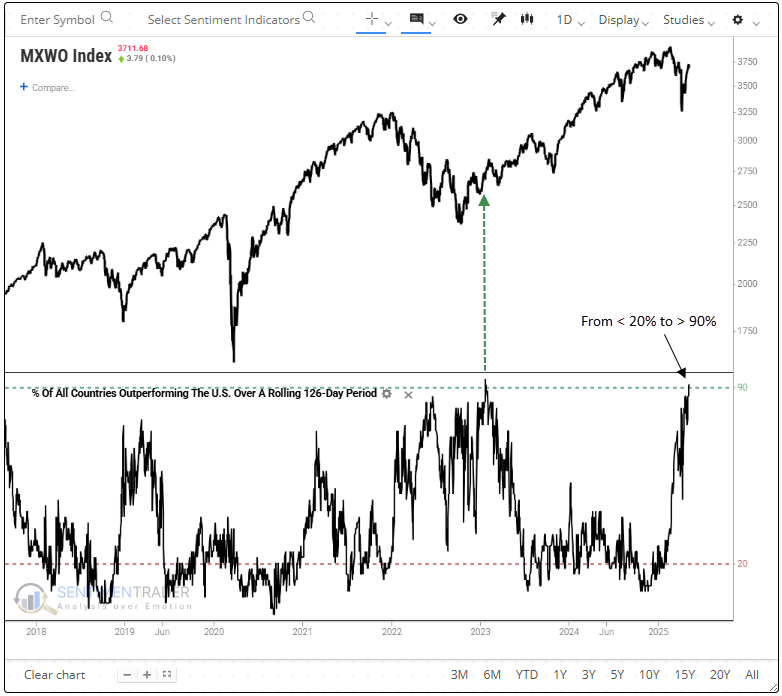

International equities have outperformed, with over 90% of MSCI Country indexes surpassing the MSCI United States Index during the past six months.

Although some suggest the era of U.S. exceptionalism is fading and a global equity rotation is gaining traction, the central question remains: Can this outperformance persist as trade tensions subside? While definitive answers lie in hindsight, history may offer some perspective.

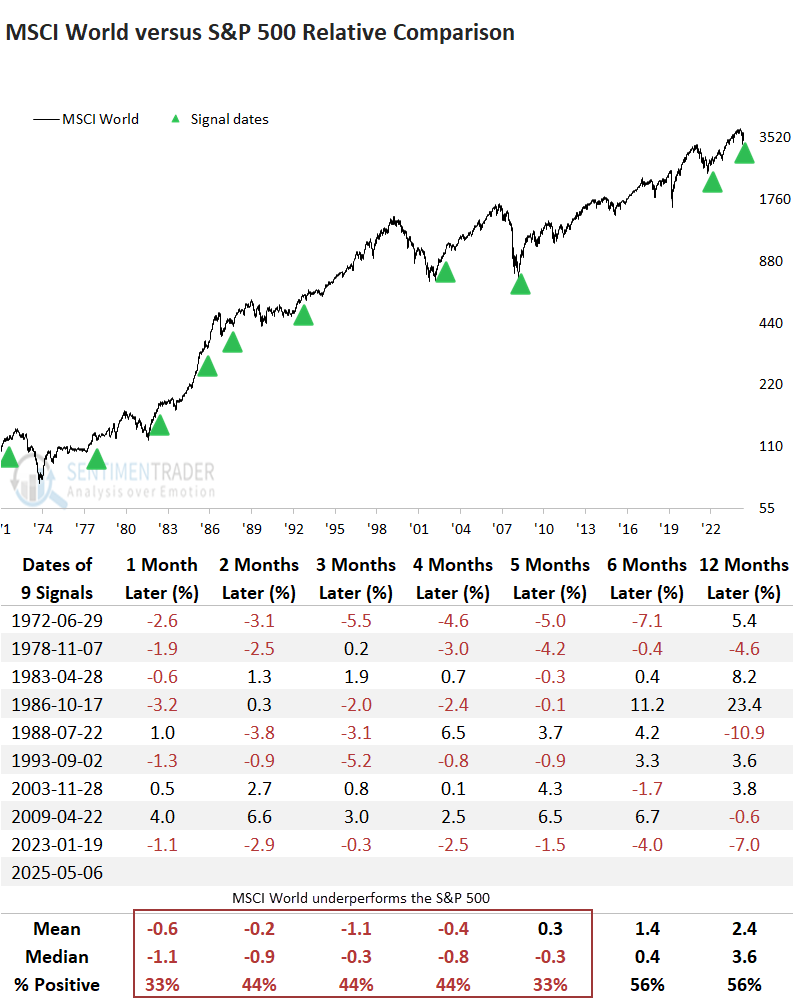

As illustrated in the chart below, the last time the percentage of country indexes outperforming the U.S. over a rolling six-month period cycled from below 20% to above 90%, equities were in the initial stages of emerging from the 2022 bear market. Will history repeat?

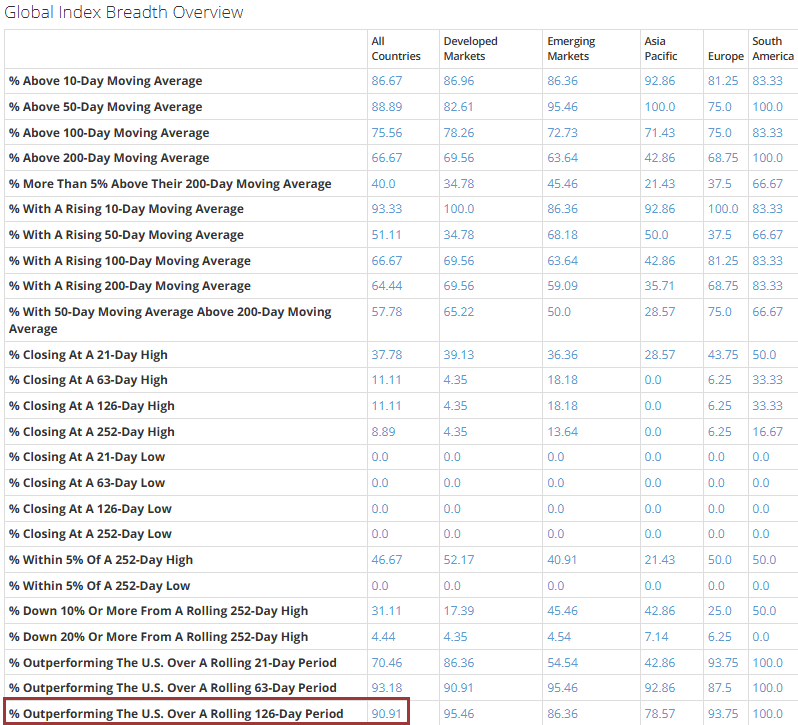

Our Global Index Breadth Overview page features 35 indicators, including the rolling six-month percentage of country indexes outperforming the U.S., segmented by region, developed and emerging markets, and all countries. Our backtest engine fully supports these indicators. Access today's signal here.

Similar global index relative trends preceded a bullish outcome

Whenever the proportion of MSCI country indexes outperforming the U.S. index over a rolling six-month period cycled from below 20% to above 90%, the MSCI World Index rose over the subsequent five, six, and twelve months without exception. Furthermore, the five and six-month windows exhibited significance relative to random returns.

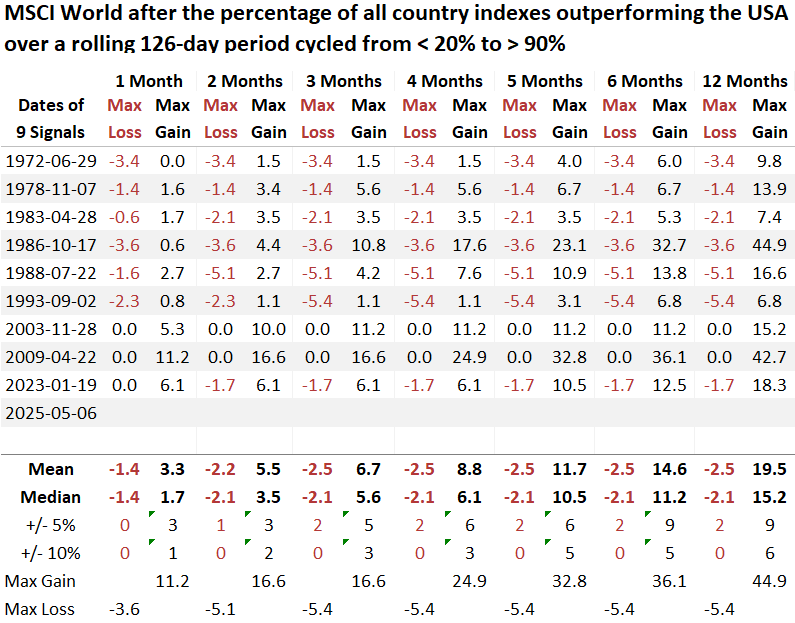

Over the following twelve months, the MSCI World Index experienced just two maximum losses greater than 5%, with none exceeding 10%, indicating a favorable risk/reward environment.

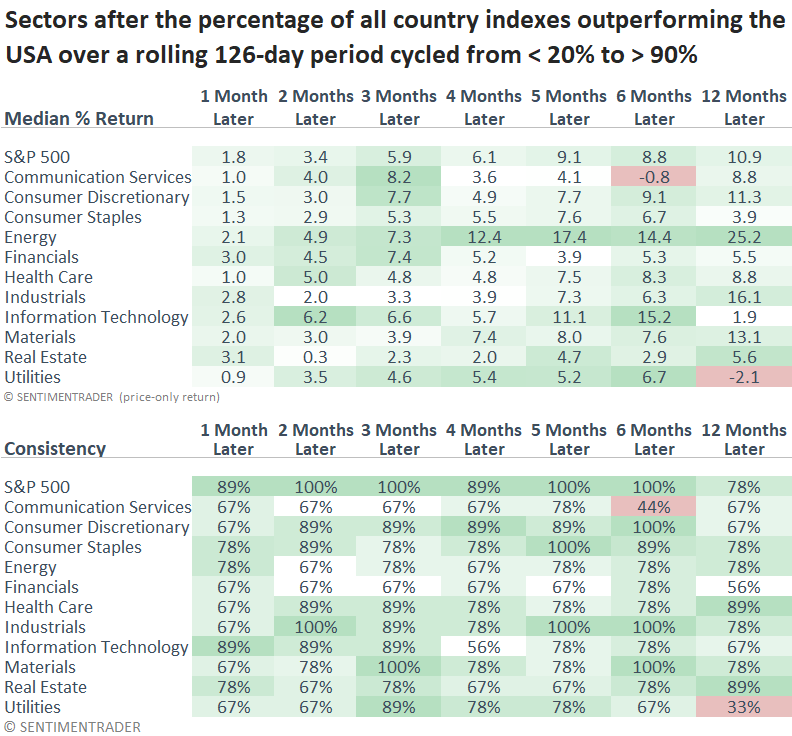

If I apply the signals to the S&P 500 and its sectors, offensive-oriented groups outpaced defensive-minded ones. That was especially the case for technology in the initial six months, reinforcing findings from other recent reports pointing to where opportunities may lie.

Historically, when a significant proportion of countries outperform the U.S. over six months, it hasn't led to sustained global leadership. The MSCI World Index generally underperformed the S&P 500 over the next one to five months, and even the mild advantage from six to twelve months wasn't particularly compelling.

What the research tells us...

Despite recent outperformance and attractive valuations, the narrative of a "great rotation" into global equities appears more like a head fake than a durable shift. While I have my views, I defer to the data, and the market's message takes precedence. Historically, when global equities have outperformed the U.S. as sharply as they have over the past six months, it has generally been a positive signal for stocks across the globe. However, this hasn't translated into sustained international leadership compared to the S&P 500. For now, a home country (U.S.) bias is advisable with a tilt toward cyclicals, especially technology.