Small traders press their bearish bets

Key points:

- The smallest options traders have moved back to a normal range of call buying

- They remain heavy buyers of put options, betting on swift and severe selling pressure

- Over the past ten weeks, this behavior is on par with the (near) end of the last two major bear markets

Pervasive bets on a crash rival the worst markets in 22 years

Small options traders have been slowly giving up the ship. Now, they're actively betting it's going to sink.

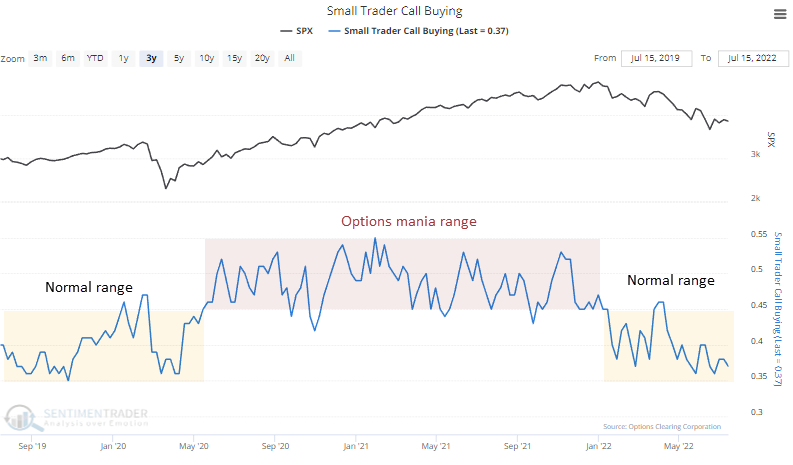

In recent weeks, the smallest options traders have moved back to a normal level of speculative activity on the bullish side of the ledger. Their extended foray into the meme-driven pandemic options mania has ended. Instead of spending 45% - 55% of their options volume on buying calls to open, they're back to spending about 35% - 45%.

The more remarkable thing has been - and continues to be - their interest in hedging against a crash. It's probably less accurate to call this hedging than inverse speculation. The way these traders use the options market, there is little portfolio hedging involved. Most of it is purely short-term speculation on a rally (buying calls to open) or a crash (buying puts to open).

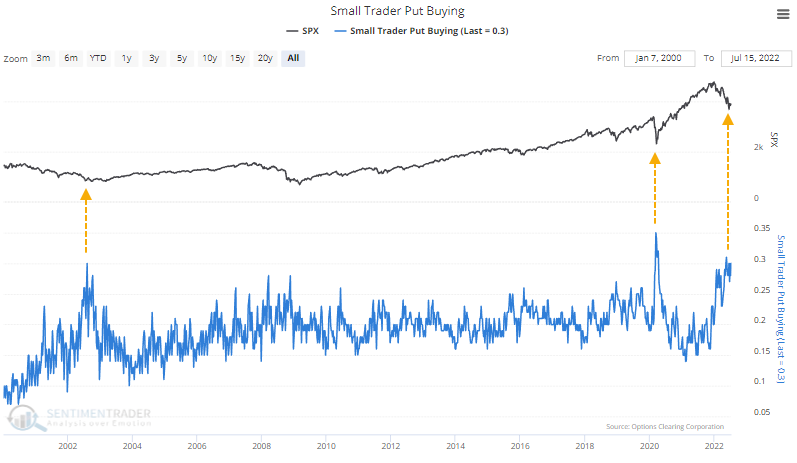

They're still focusing heavily on these put options, spending about 30% of their volume on these bets that stocks will drop quickly. This is remarkable because there have been only two times in 22 years when they've spent so much of their volume on put options - during the fraud scare meltdown in July/August/September 2002 and during the pandemic.

Even though implied volatility has come down, small traders are still paying up for these puts. Over the past ten weeks, they've spent $39.7 billion on put options and $39.6 billion on call options.

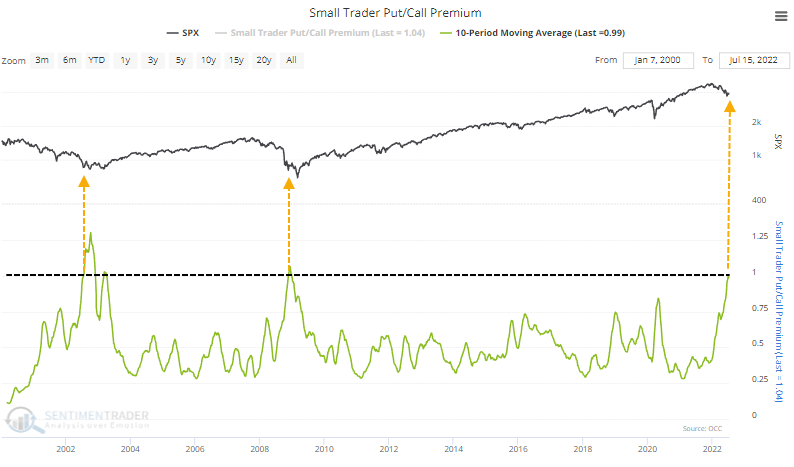

It's extremely rare for them to spend more on leveraged, expiring bets that stocks will fall than they spend on bets that stocks will rise. It takes a devastating decline to change mass psychology this much, so the only two precedents were the two worst bear markets in recent memory. This flip in psychology also coincided with the bear markets' end games. After a relief rally each time, there was another leg lower, but the bulk of the losses was already past.

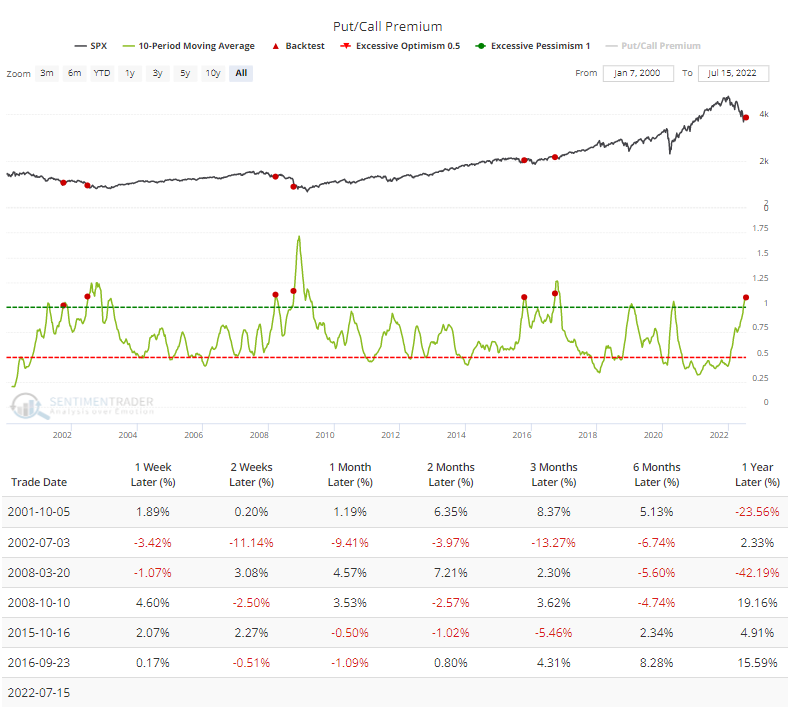

While the behavior of small options traders is one of the most consistently useful contrary indicators, and while small traders are a more significant influence in the options (and overall) market than they've been in decades, they're not the end-all, be-all. If we look at the premiums that all options traders in the U.S. have been paying over the past ten weeks, they're not quite at extreme a level as the smallest traders are.

The table shows forward returns in the S&P 500 after all traders spent 10% more on put options than call options during an average week over the prior ten weeks. The returns were not consistent, but either three or six months later, the S&P did show a positive return after all but one date, which was right before the worst of the meltdown in July 2002. That preceded a hefty loss, though it was entirely reversed in the months afterward.

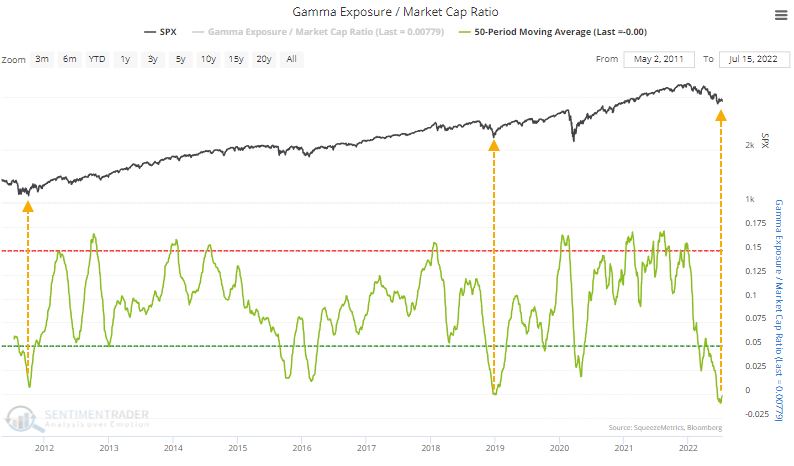

On the flip side of these trades are often dealers, who often have to hedge their book by buying or selling the underlying securities. That's the essence of Gamma Exposure. As a percentage of S&P 500 market capitalization, gamma exposure has been negative, suggesting that dealers would have to buy stocks to hedge their options positions on further declines. In fact, the 50-week average just turned negative for the first time; the only times it even got close were in October 2011 and December 2018.

What the research tells us...

Ground zero of the pandemic speculative orgy was evident in the options market, and it's safe to say that sentiment has been thoroughly wrung out. Not only are those traders no longer aggressively betting on flyers (in aggregate, anyway), they're certainly betting that many of these stocks will tank. The mentality has become so pervasive that long-term moving averages of their behavior rival the worst markets in 22 years.

This kind of behavior, from this group of traders, is nearly a sure-bet contrary signal, but the trouble is that the time frame isn't all that clear. Usually, it's most effective over several months, but if it fails, it fails hard. The silver lining is that the only time it failed was almost precisely 20 years ago, which was an excellent entry for long-term investors.