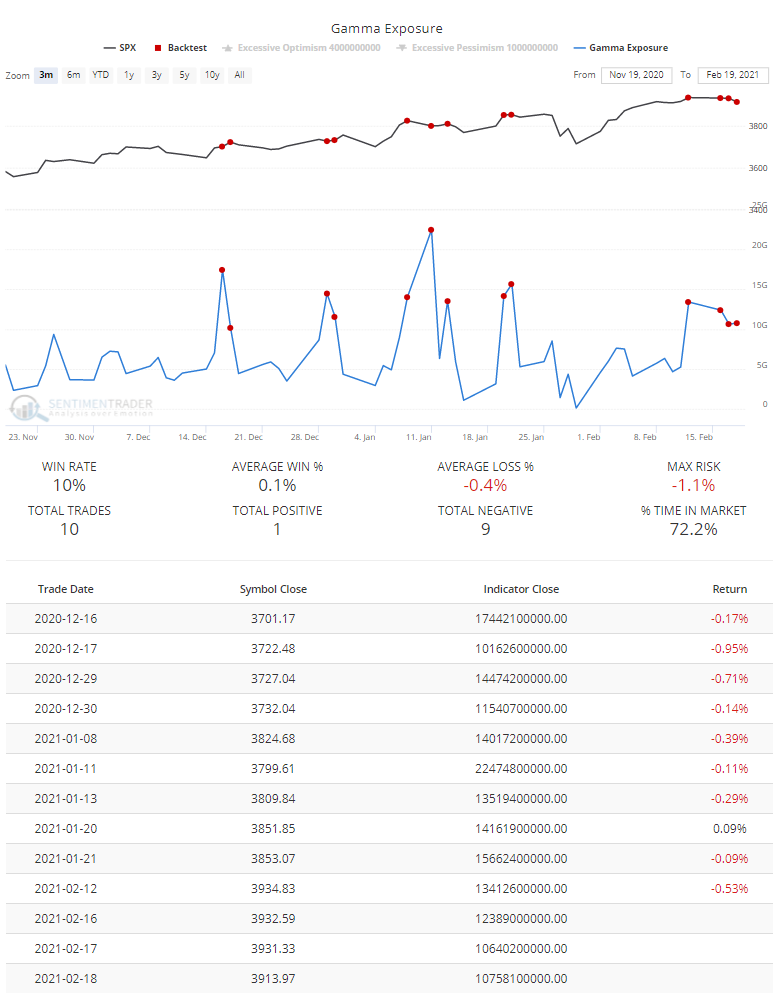

Opex games

As futures pop higher on option expiration day, it's worth keeping in mind that due to all the raging call buying from retail investors, dealers' exposure has been sky high. Gamma Exposure has averaged (median) more than $10 billion this week, the 2nd-highest in history, second only to January 13 of this year.

A daily Gamma Exposure above $10 bln has had a consistent tendency to precede short-term weakness, with the S&P 500 showing only 1 positive return over the next 3 days out of the past 10 attempts, according to the Backtest Engine.

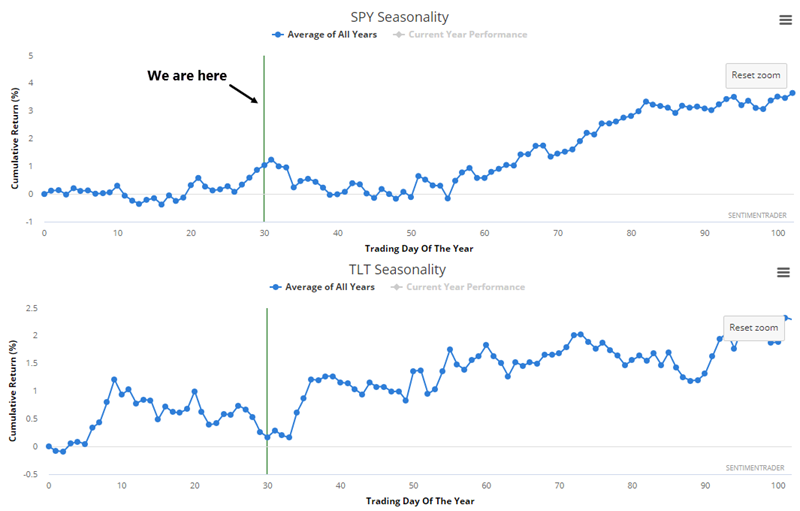

Another interesting wrinkle is that the Stock/Bond Ratio is once again bumping up against its ceiling, for all practical purposes.

This is happening right when SPY is forming its typical seasonal peak and bonds their seasonal low.