One useful credit spread indicator turns unfavorable

Key Points

- We will look at a credit spread that measures the calculated spreads between a computed index of all bonds in a given rating category and a spot Treasury curve

- Credit spreads can offer warnings when they behave abnormally

- Typically, relatively smooth sideways action indicates a favorable environment for stocks and the overall economy

- In addition, credit spreads typically move inversely to stock prices

- However, over time there can be wide swings in the level of correlation between credit spreads and stocks

- Recognizing extremes in these correlation swings can alert investors to favorable and unfavorable environments for stocks

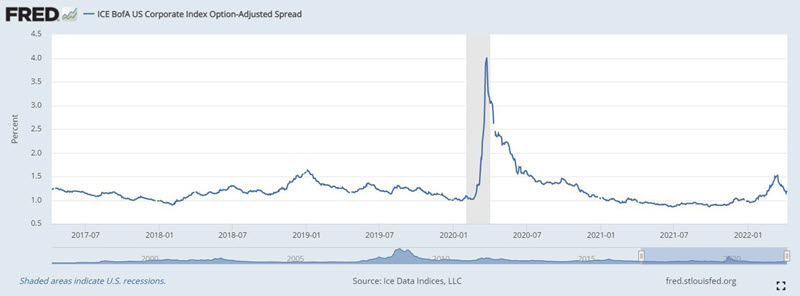

ICE BofA US Corporate Index Option-Adjusted Spread

The indicator we start with is the ICE BofA US Corporate Index Option-Adjusted Spread which can be accessed here. This spread represents the Option-Adjusted Spread (OAS) of the ICE BofA AA US Corporate Index, a subset of the ICE BofA US Corporate Master Index tracking the performance of US dollar-denominated investment grade rated corporate debt publicly issued in the US domestic market. For simplicity, we will use only month-end values in our analysis and will heretofore refer to this as "Credit Spread*."

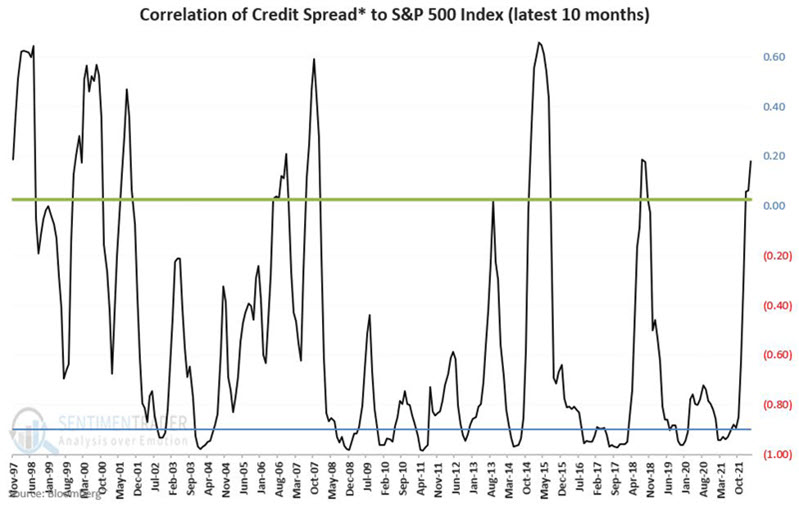

The second piece of data is the S&P 500 Index month-end closing price. The chart below puts both data series on the same chart, with the credit spread axis on the left and the S&P 500 Index axis on the right.

Building an Indicator

In our analysis, the indicator we will use is the correlation between the Credit Spread* and the S&P 500 Index over the latest ten months. As you can see in the chart above, there is a strong tendency for these two series to be non-correlated. However - as we will see - the level of correlation can swing widely over time. We will use these swings to designate the indicator as "favorable" or "unfavorable" for stocks.

The variables appear below:

A = Month-end Credit Spread*

B = Month-end S&P 500 price

C = Correlation of A and B over the past ten months

D = 0.027

E = -0.900

The chart below displays variables C, D, and E.

Rules

- If C crosses above D (0.027), the indicator is "Unfavorable" for stocks

- If C crosses above E (-0.90), the indicator is "Favorable" for stocks

A little clarification:

- As soon a Variable C registers a monthly close of 0.27 or higher, the indicator flips to "Unfavorable."

- In other to turn "Favorable," Variable C must a) first register a monthly close BELOW -0.90, and then b) subsequently register a monthly close back ABOVE -0.90

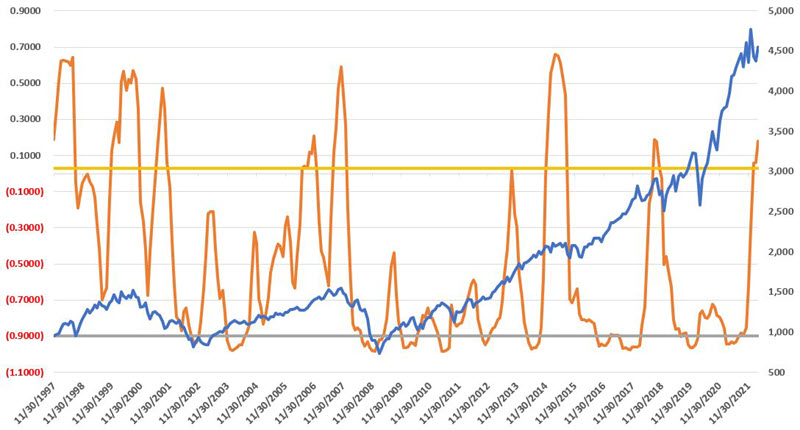

To highlight the relationship between the indicator and the S&P 500 Index, both are plotted below, with the correlation value axis on the left and the S&P 500 Index axis on the right.

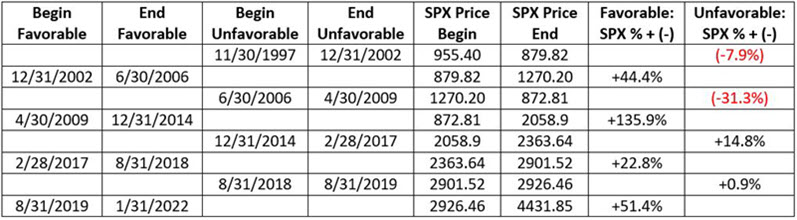

Performance results

The table below displays the "Favorable" and "Unfavorable" period start and end dates as the performance of the S&P 500 Index during each period.

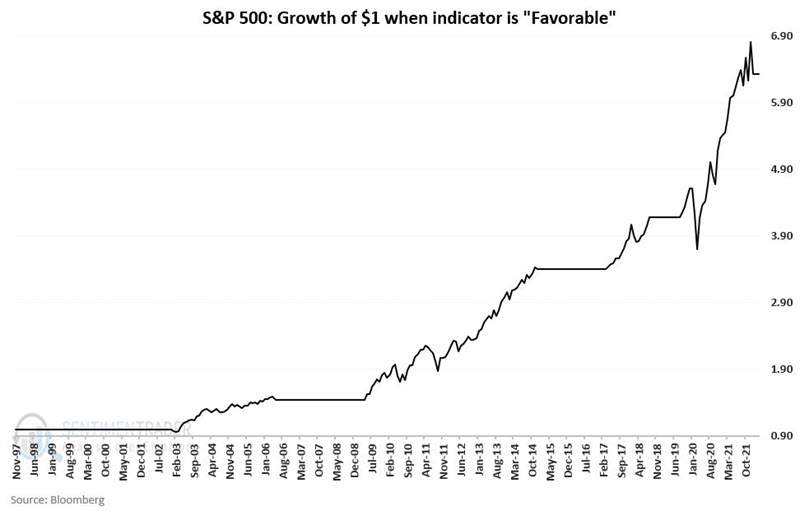

The chart below displays the growth of $1 in the S&P 500 Index held only during "Unfavorable" periods.

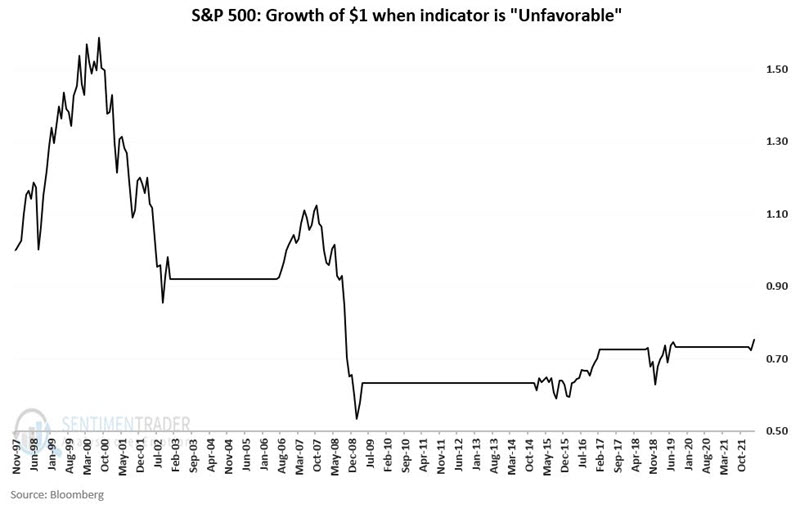

The chart below displays the growth of $1 in the S&P 500 Index held only during "Unfavorable" periods.

Since 1997:

- During Favorable periods the S&P 500 gained +533%

- During Unfavorable periods the S&P 500 lost -24.8%

What the research tells us…

Stable credit spreads indicate "normal" economic circumstances (i.e., steady growth). When credit spreads begin to act abnormally and become volatile, it offers a potential warning sign that something is amiss. The recent high correlation between credit spreads and stocks is not an "automatic" sell signal. Sometimes the stock market chops a bit before regaining its footing. Other times a significant bear market ensues.

The indicator detailed in this piece is not intended to serve as a standalone buy and sell signal generating system. But as a "weight of the evidence" tool, it can offer valuable clues regarding the current relative state of the stock market and the overall economy.