One measure of inflation is collapsing at a historic rate

Key points:

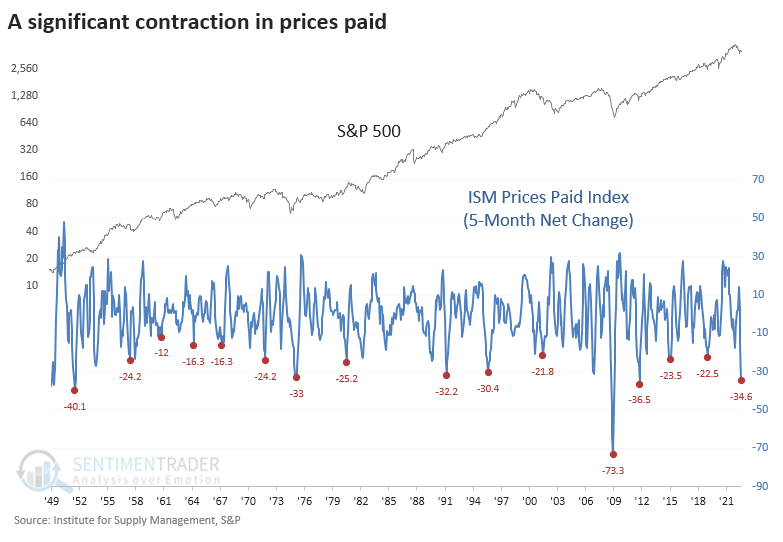

- The 5-month net change for the ISM prices paid index has declined by over 34%

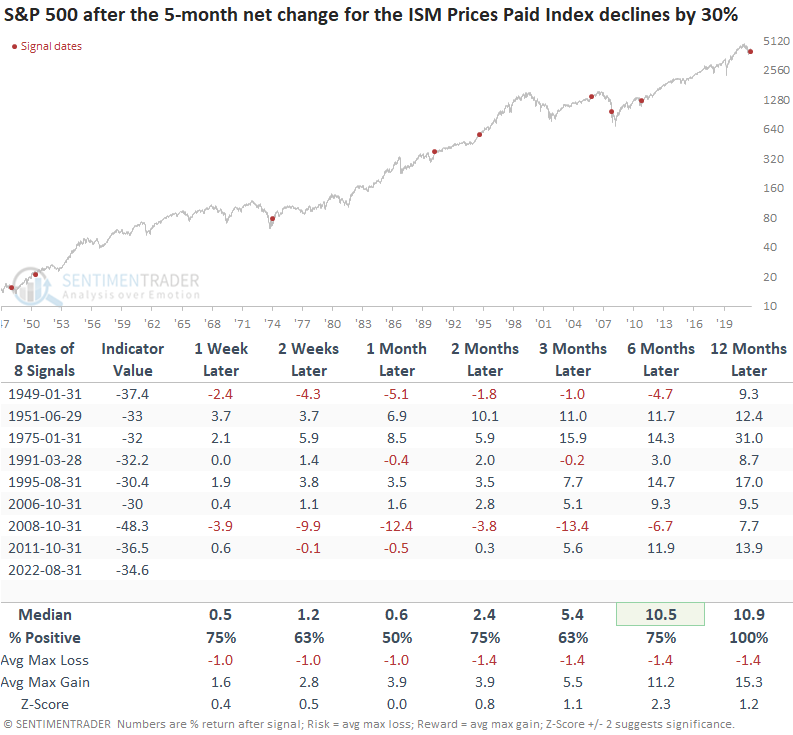

- After similar contractions, stocks were higher 100% of the time a year later

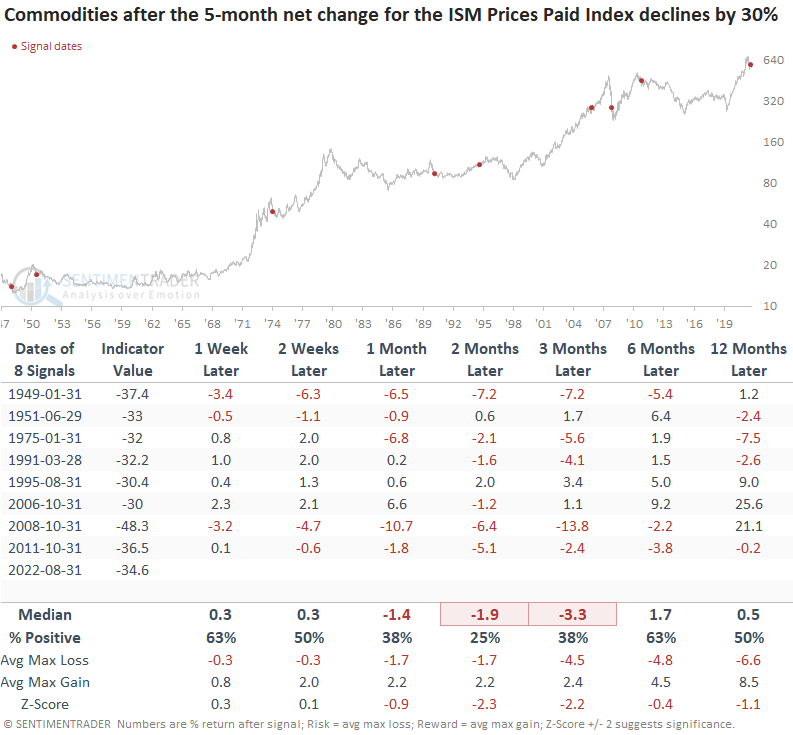

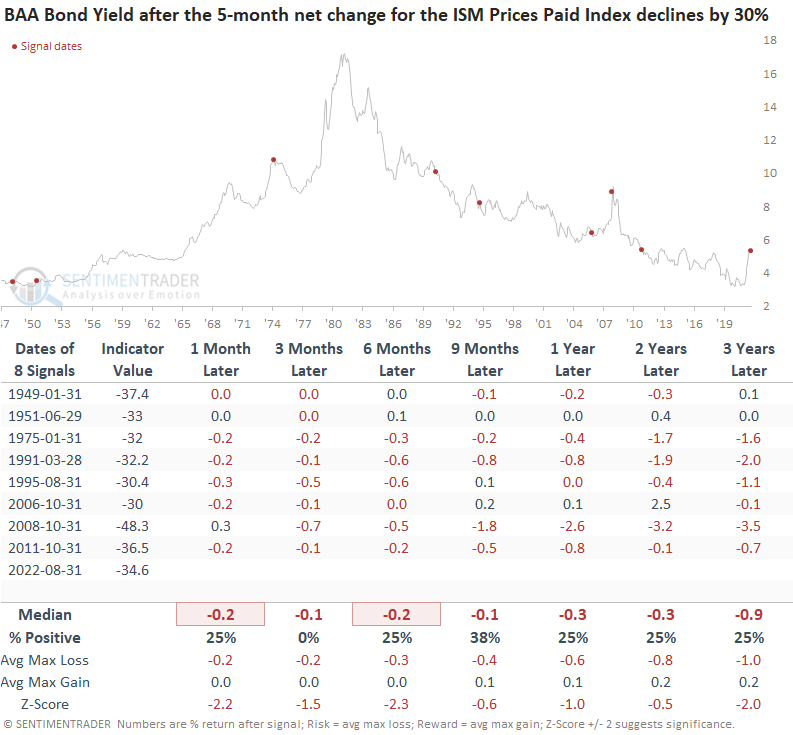

- Commodities struggled, which should help with elevated consumer prices and bond yields

The manufacturing sector is seeing some relief in prices paid

Purchasing executives are reporting sharply lower prices for goods, and that bodes well for markets.

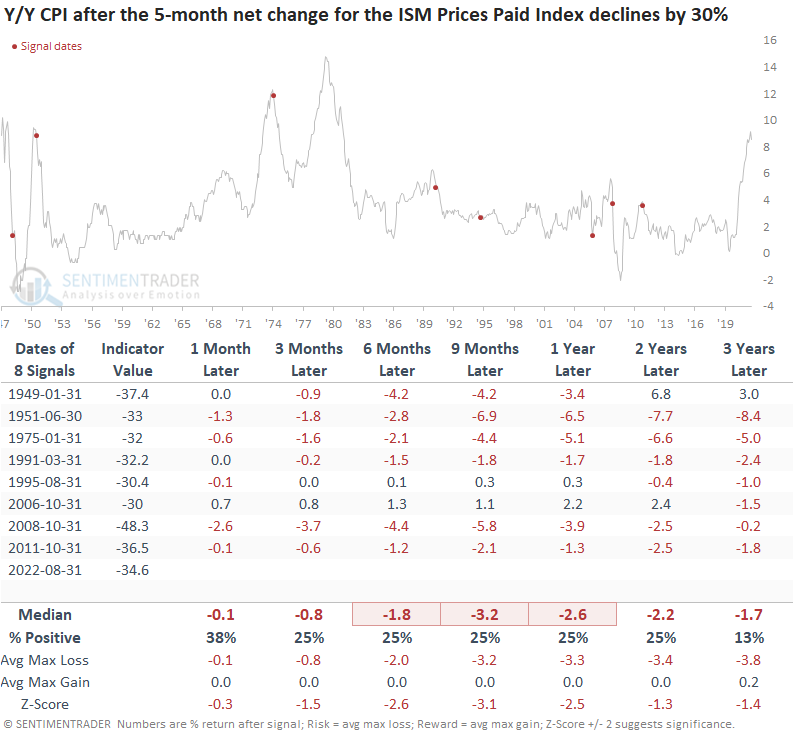

The Institute for Supply Management released the latest manufacturing data last week. While the overall survey has fallen in the previous few months, the prices paid index has fallen off a cliff. The index has declined by over 34% in five months, the fifth largest contraction in history.

Sharp contractions in the survey preceded positive returns for stocks

A sharp drop in the ISM prices paid index was bullish for stocks, especially on a medium to long-term basis. A year later, the S&P 500 was higher 100% of the time. The one untimely signal in 2008 occurred after the collapse of Lehman, a period when just about every risk asset was in freefall.

On average, the S&P suffered minimal drawdowns within the next year while averaging a gain of more than 15% at some point.

Commodities tended to struggle after these signals

Commodities tend to suffer after a significant contraction in the ISM prices paid index, especially over the next one to three months. A year later, the median return was flat, with a win rate no better than a coin toss. The only times when the previous uptrends in commodities managed to sustain themselves were in 1995 and 2006.

Corporate bond yields tended to fall

The contraction in the ISM prices paid index should help to bring down the cost of capital for corporations. Bond yields were lower in every instance three months later, even in 1975, which occurred in a high-inflation environment.

Expect some relief in traditional inflation measures

The significant contraction in the ISM prices paid index bodes well for some relief from elevated consumer prices.

Suppose we compare current-day Y/Y CPI to the other two extreme levels where we got a signal in 1951 and 1975. In that case, the collapse in the ISM prices paid index provided a timely alert for an impending contraction in CPI.

We must acknowledge that CPI components/weights have changed throughout history.

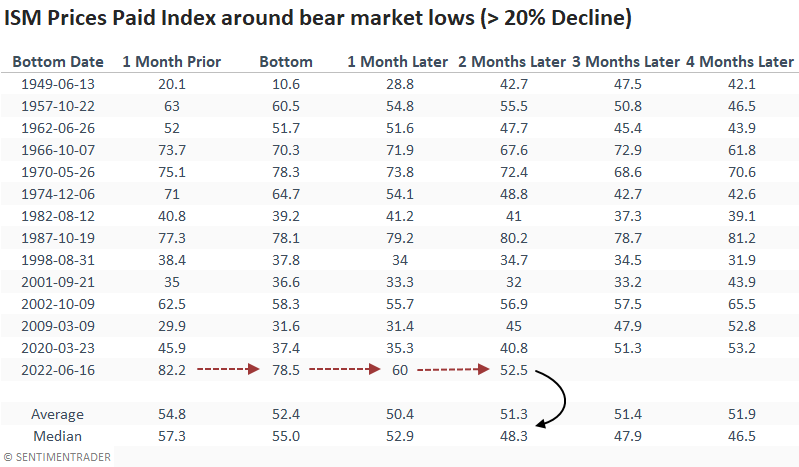

An assessment of ISM prices paid index around bear market lows

The ISM prices paid index has now fallen to a level more in line with other historical periods around bear market lows. So, if June was the market low, stocks should have less of a headwind on a go-forward basis.

What the research tells us...

Inflation has been the catalyst for one of the most aggressive tightening cycles by global central banks in history, and stocks have responded accordingly. The significant contraction in the ISM prices paid index is a positive development for stocks as it removes one significant macroeconomic headwind. While the decline is positive for stocks, it doesn't bode well for commodities, which should help alleviate the high Y/Y CPI numbers. With lower inflation, the environment for bonds looks more encouraging.