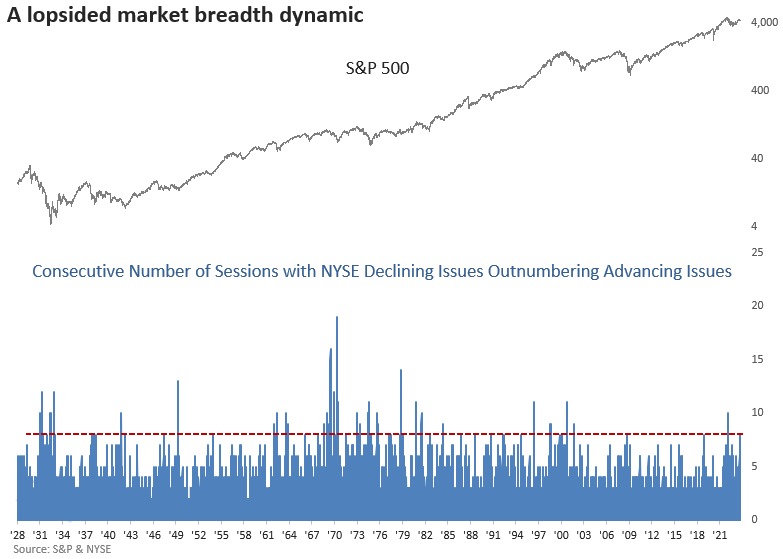

NYSE breadth skews to the negative side

Key points:

- Declining issues on the NYSE outnumbered advancing issues for seven consecutive sessions

- Similar advance-decline dynamics led to lackluster returns over the subsequent three months

- When the lopsided streak occurs in an uptrend, the outlook remains stagnant over the same horizon

What, if any, insights can we derive from the skewed NYSE breadth?

When considering breadth-based indicators for exchanges, I prefer the NYSE rather than the Nasdaq. The NYSE contains a more substantial collection of high-quality stocks and bond proxies, thus offering us two market insights.

With bond yields pressed near the upper end of multi-year highs, stocks and bond proxies on the NYSE have come under pressure. In each of the previous seven sessions, declining stocks on the NYSE have outpaced advancing issues. This dynamic has only occurred 1% of the time since 1928.

Comparable stretches of skewed breadth led to uninspiring returns

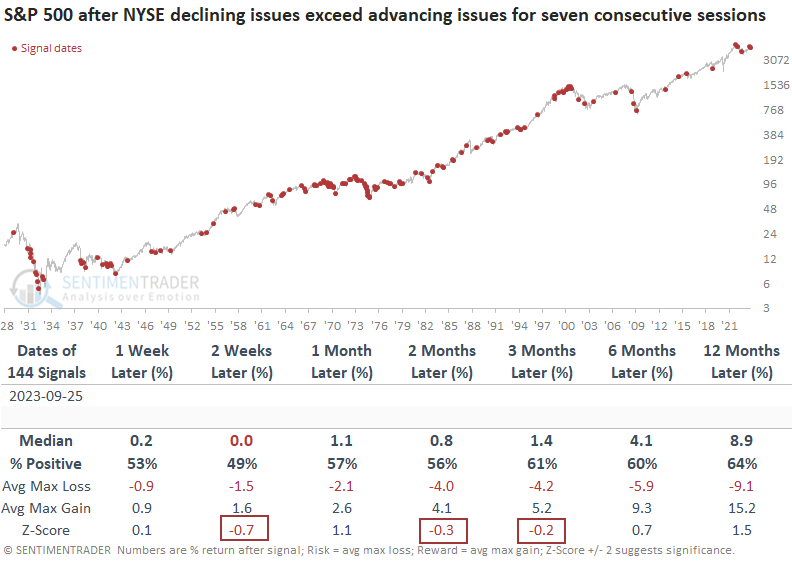

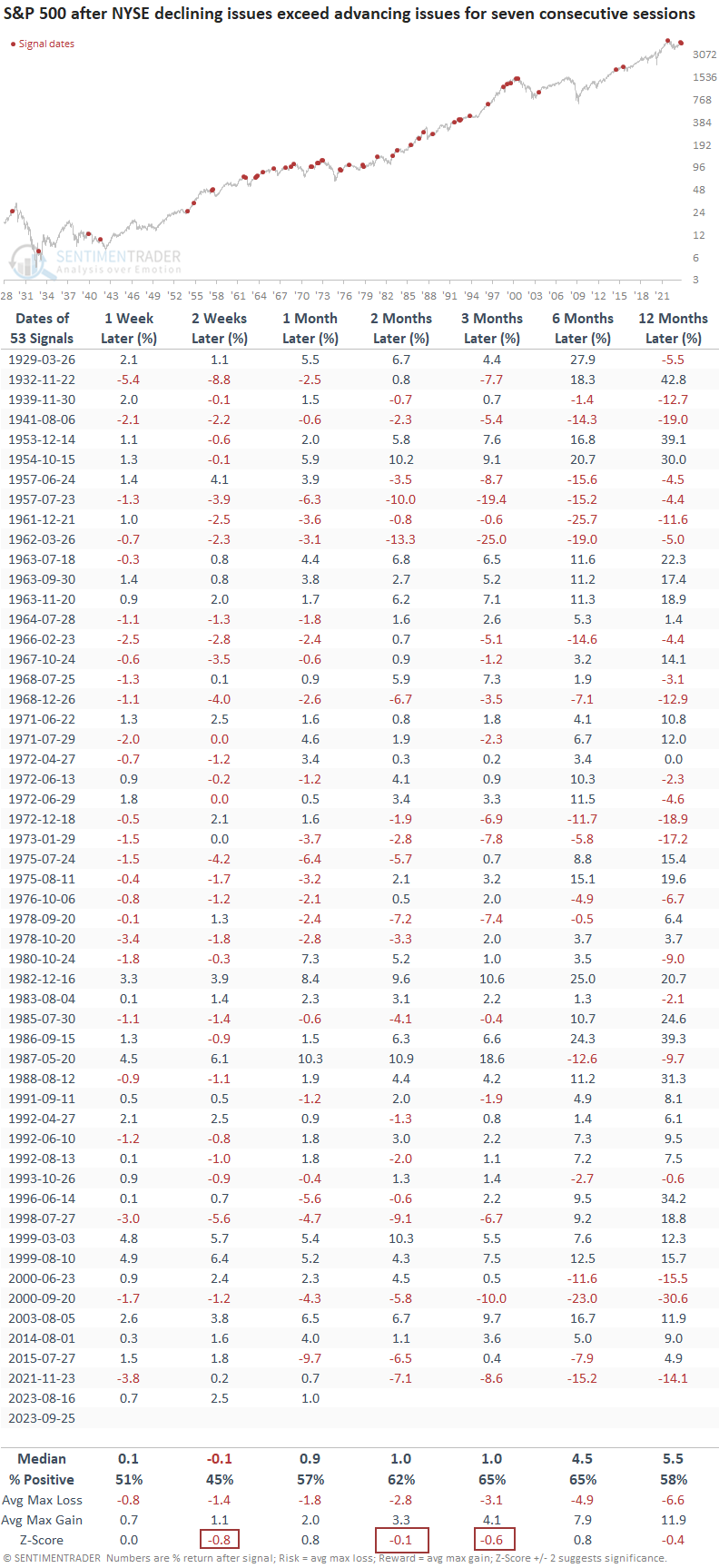

When the number of declining issues on the NYSE exceeds that of advancing issues like now, the S&P 500 shows uninspiring returns over the ensuing three months. During that timeframe, S&P 500 returns were worse than the overall study period returns in 3 out of 5 horizons.

Signals in an uptrend

Let's add some context. I will now require the S&P 500 to close above its 200-day average, signifying an uptrend similar to now. When NYSE breadth is negative for seven consecutive sessions, and the S&P 500 is above its long-term average, returns are still lackluster over the subsequent three months. Once again, 3 out of 5 time frames up to three months later underform the median return over the study period.

Interestingly, when I ran a test to identify the consecutive number of negative sessions that was ideal for buying the S&P 500, the optimization returned seven sessions. The optimal holding period was only 12 trading days.

What the research tells us...

NYSE advance-decline breadth has been skewed in favor of declining issues over the last seven sessions, reaching a point rarely seen in history. Typically, a mean reversion bounce back occurs when participation measures tilt one way for too long. While the S&P 500 tends to rally after seven consecutive sessions with declining issues outweighing advancing issues, forward returns are lackluster over the subsequent three months, and 3 out of 5 instances underperform relative to history. So, the market may need to fall further, creating a more meaningful oversold condition that entices buyers.