Nervous about your GLD position?

Key points

- Gold has witnessed an explosive rally

- Traders who have been holding a long position in SPDR Gold Trust ETF (GLD) are now faced with a decision - "Take profits" or "Let it ride?"

- Options may offer traders a way to do both - but not without specific tradeoffs

What if Gold does NOT go to the moon?

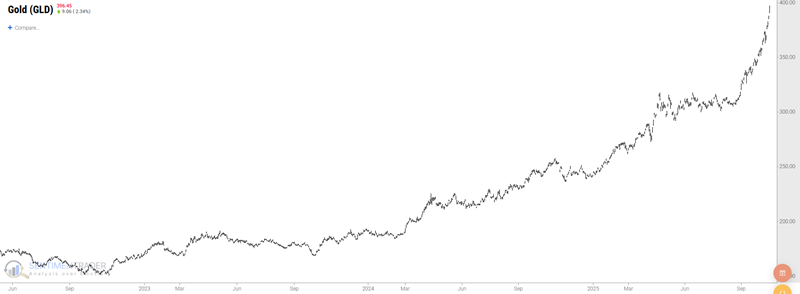

Gold has witnessed a historic rally in recent months, which has only accelerated in recent weeks. Below we see the action for the SPDR Gold Trust ETF (GLD).

At this point, many traders who bought GLD are now grappling with the "Should I take profits or let it ride" conundrum. Two thoughts:

First, remember that it is not written in stone that you must be 100% fully in or 100% fully out. One option is to sell some portion of your position. Thus, you "take profits" on some and "let it ride" with the rest. This can make great sense, but you must prepare for the potential psychological trap. If gold continues to rally, you may be tempted to beat yourself up with "I should have stayed in." Conversely, if gold were to fall apart, the lament may be "I should have sold it all." So be prepared to combat those psychological pitfalls.

The other alternative is to hedge with options on GLD. Buying a put option can make sense if your primary goal is to limit downside risk. However, we see in the chart below (all subsequent screenshots courtesy of www.Optionsanalysis.com) that implied volatility on GLD options is high. This means that GLD options are relatively "expensive", i.e., there is an above-average amount of time premium built into the price of GLD options. This can result in paying out a lot of premium, with upside potential reduced by the cost of the premium paid.

Another alternative is a long collar, which involves selling an out-of-the-money call and buying an out-of-the-money put option. However, this strategy will completely limit upside potential beyond the strike price of the call option sold.

So, for the current situation, let's consider a strategy best referred to as a ratio collar. While holding at least 200 shares of GLD, this position involves selling an out-of-the-money call option and using the proceeds to help offset the cost of buying two put options.

A closer look at hedging GLD

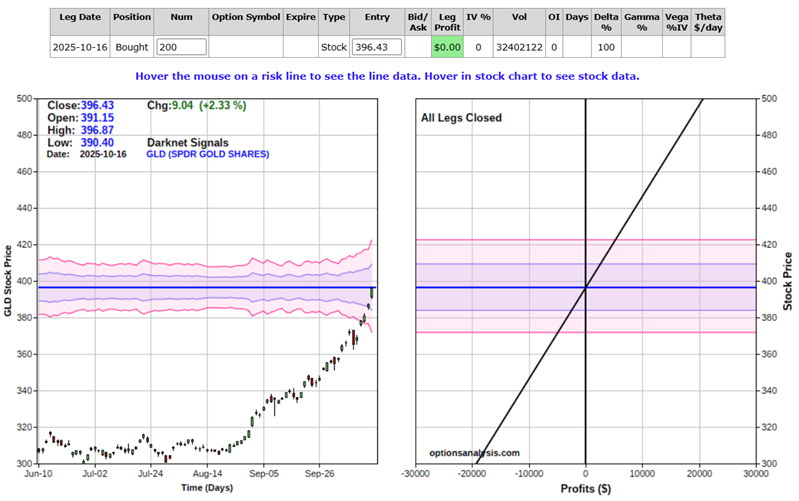

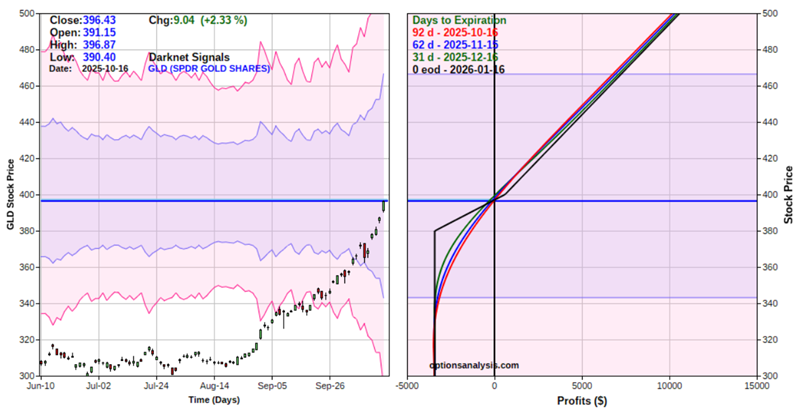

A trader holding 200 shares of GLD for any length of time is presently sitting on a nice open profit. And while they hope/expect even more upside in the months ahead, the potential for a sharp pullback - and a giveback of a significant amount of open profit - is high. So, let's consider the following example position:

- While holding long 200 shares of GLD (currently @ $396.43 a share)

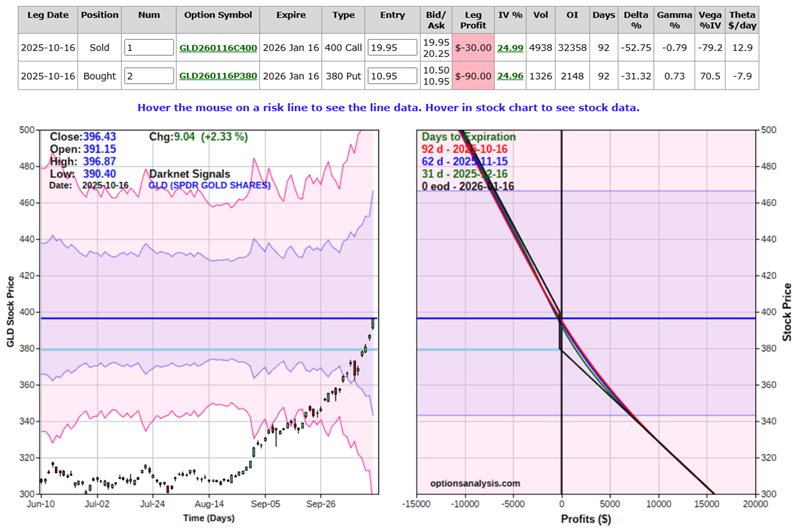

- Sell 1 GLD Jan16 2026 400 call @ $20.10

- Buy 2 GLD Jan16 2026 380 puts @ $10.70

Let's first break this down into two parts. The following chart shows the equity curve (i.e., the expected P/L at a given price for GLD as of a given date) for holding 200 shares of GLD. As you can see, it is a straight line, because for every $1 GLD rise in price, the position will gain $200 and vice versa. A $200 gain or loss for GLD share would result in a gain or loss of $20,000 in position value.

The next chart shows the equity curve for only the option hedge portion - i.e., short one 400 call and long two 380 puts. Note that:

- Above $400 a share, the option portion will lose $100 for each $1 GLD rises in price

- Below $380 a share, the option portion will gain $200 for each $1 GLD declines in price

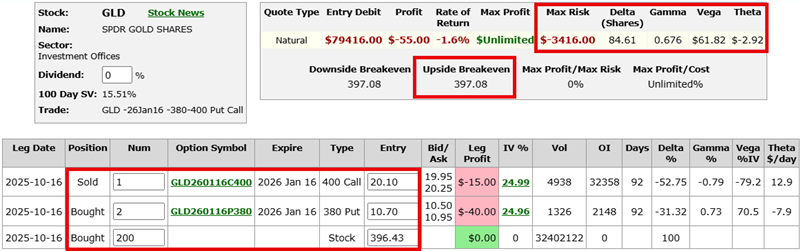

If we put the long 200 shares together with the short one call and long two puts, we see the particulars for the adjusted position and the risk curves for the adjusted position, which combines the two equity curve charts above.

About the adjusted, hedged position

There are some key things to note about the adjusted position:

- To enter this position, we pay $2,140 to buy the two 380 puts at $10.70 and take in $2,010 to sell the 400 call. This results in a net outlay of $130.

- Because we hold 200 shares of stock but only sold one call, we retain unlimited profit potential on the second 100 shares if GLD rallies above the 400 strike price.

- We are giving up some upside potential to limit downside risk. Our Delta for holding 200 shares of GLD is 200. Once we enter the new position involving the call and put options, our Delta declines to 84.61. So, for each $1 GLD rises or falls in price, we will gain or lose roughly $85 (instead of $200 if we only held the shares).

- A Gamma of 0.676 means we will gain that many Deltas if GLD rises $1 or lose that many Deltas if GLD declines $1.

- A Vega of $61.82 means that the position will gain roughly that dollar amount if implied option volatility rises by one percentage point, and vice versa. This means an increase in implied volatility is good for this position, and a decline in implied volatility is bad

- A Theta of -$2.91 means that the position will lose that much value due to time decay from the passage of one day of time

- Because we are paying out cash to enter the adjusted position, our breakeven price at option expiration rises to $397.06 a share.

Comparing the adjusted position to the initial position

The chart below shows the risk curves for the initial position (long 200 shares of GLD) and the adjusted position (long 200 shares of GLD, short one 400 call, and long two 380 puts).

Here we can also visualize the tradeoffs involved:

- Above the breakeven price of $397.06 to the call strike price of $400, the adjusted position will rise dollar for dollar with the long 200 shares position

- Above the call strike price of $400, the long 200 shares position will continue to gain $200 for each point GLD rises in price. The adjusted position will make only $100 for each point GLD rises in price

- If GLD rallied to $450 a share, the long 200 shares position would gain $10,714 from its current value. The adjusted position would earn roughly $5,584

- On the downside, the adjusted position holds an advantage. If GLD declines to $350, the long 200 shares position would fall $9,286 in value. The net adjusted position can lose up to $3,416 from its current level. However, that is the maximum amount it can lose, as the two long put options offset any losses from the 200 long shares below the 380 strike price

- If GLD fell all the way to $300 a share, the long 200-share position would lose $19,286 from its current value, while the adjusted position would lose only $3,416

What the research tells us…

For a trader holding a significant open profit who wants to maintain unlimited profit potential while limiting downside risk, selling a call option to help pay for enough put options to limit downside risk to a specific amount can make sense. Please note that the position detailed above is intended to serve as an example of one way to hedge a long position using options and is not a specific trade recommendation.