More signs of bullish optimism

Key points:

- The net % of consumers expecting stocks to increase minus decrease cycled from < -19% to 8%

- Similar reversals in consumer expectations for stock prices preceded excellent returns for the S&P 500

- The National Association of Active Manager's exposure index rose above 100% for the first time in a year

Consumers and active managers are feeling better about the outlook for stocks

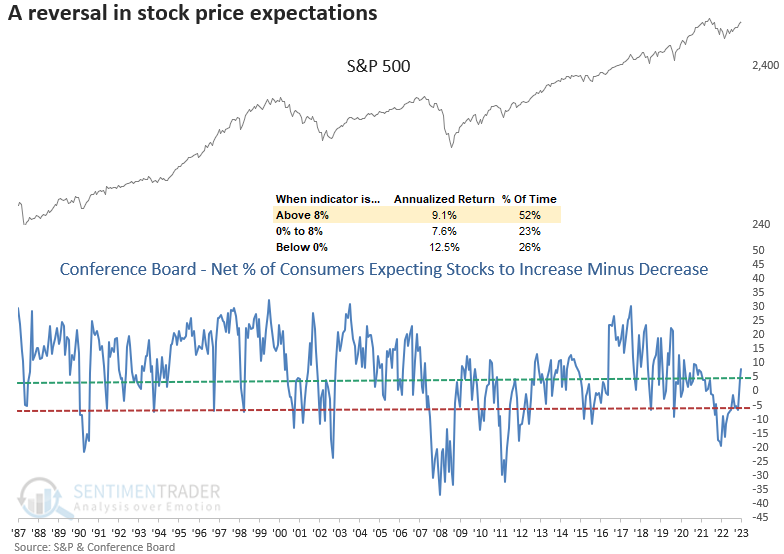

After falling to the 5th lowest reading in history, the Conference Board's net percentage of consumers expecting stocks to increase minus decrease rose to 8% with the July update last week. The survey, which measures 3000 households, confirms what we have seen from several other sentiment indicators: a reversal from pessimism to optimism.

When the net % of consumers expecting stocks to increase minus decrease reaches 8%, like now, the S&P 500 annualizes at 9.1%. It's crucial to note that annual returns only turn negative when the spread exceeds 28%. So, there is a substantial margin between the current reading and the danger zone.

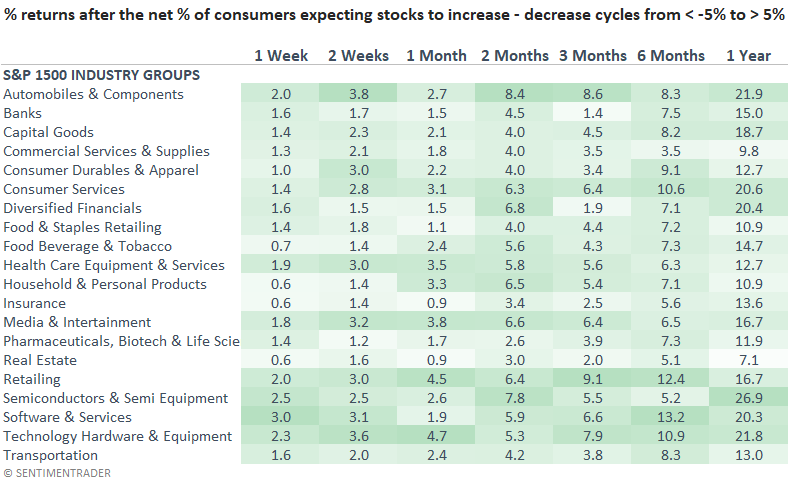

Similar reversals in consumer expectations for stocks preceded excellent returns

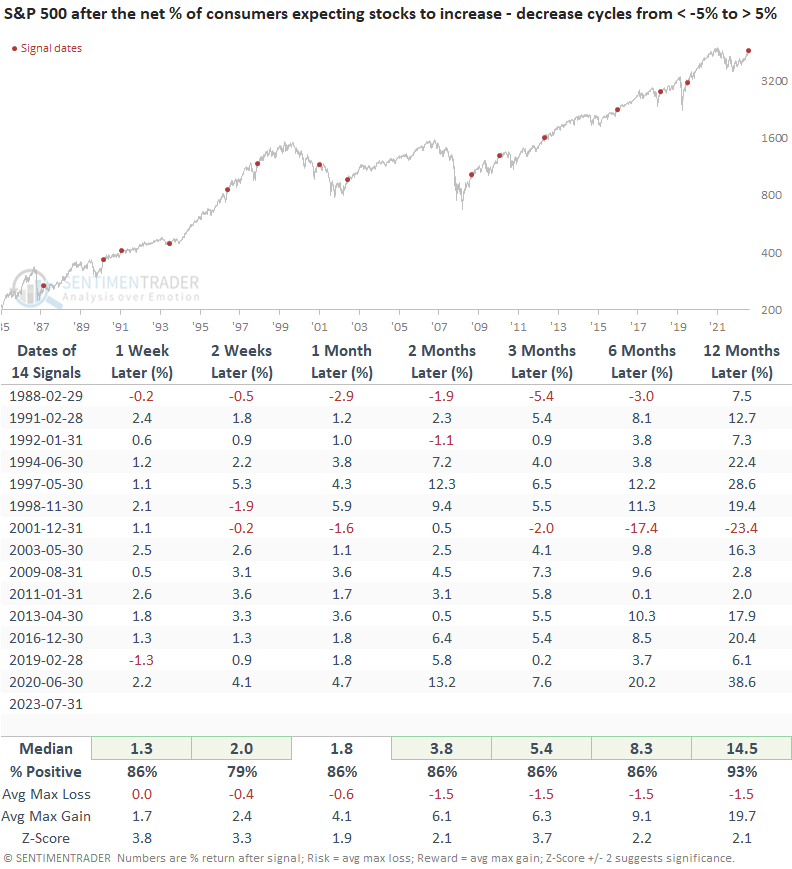

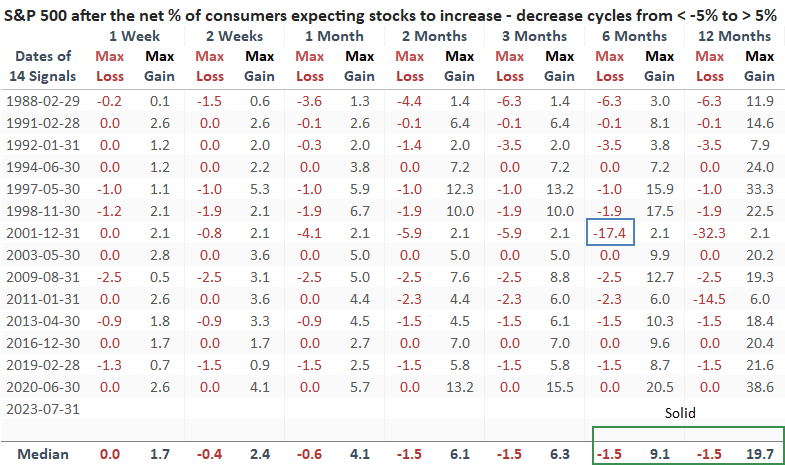

When the spread for consumer expectations on stocks cycles from less than -5% to greater than 5%, returns, win rates, and z-scores for the S&P 500 are excellent. A year later, the world's most benchmarked index was higher in all but one precedent. The only whipsaw signal occurred in 2001 when the S&P 500 was entrenched in a significant downtrend, which is not the case now.

I adjusted the threshold levels to increase the sample size.

Over the next six months, the S&P 500 suffered only one max loss of greater than -6.3%. A year later, the risk/reward skew was astonishing as the median gain far surpassed the median loss.

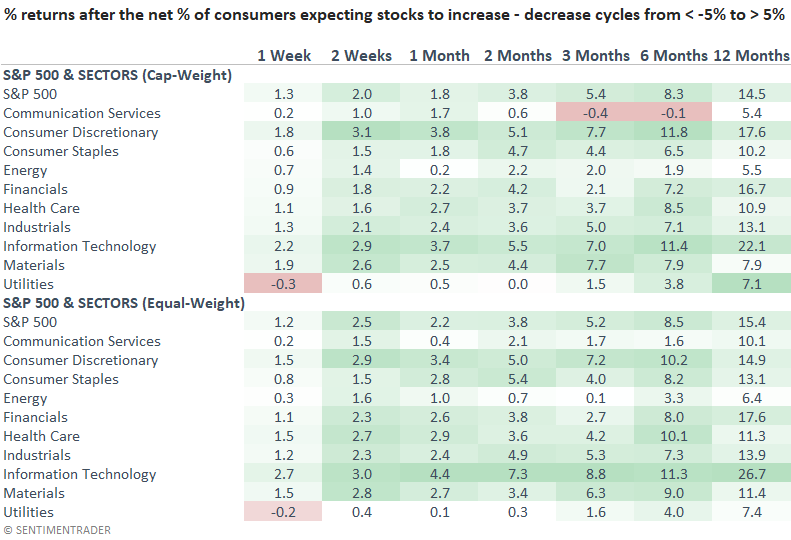

History suggests sentiment shifts like the one occurring now are favorable for the Consumer Discretionary and Technology sectors, aligning with bullish relative trends for those groups. While Financials do well, the industry is struggling on a comparable basis.

Semiconductors, another relative winner this year, outperform all other industries when consumer expectations on stocks shift like now.

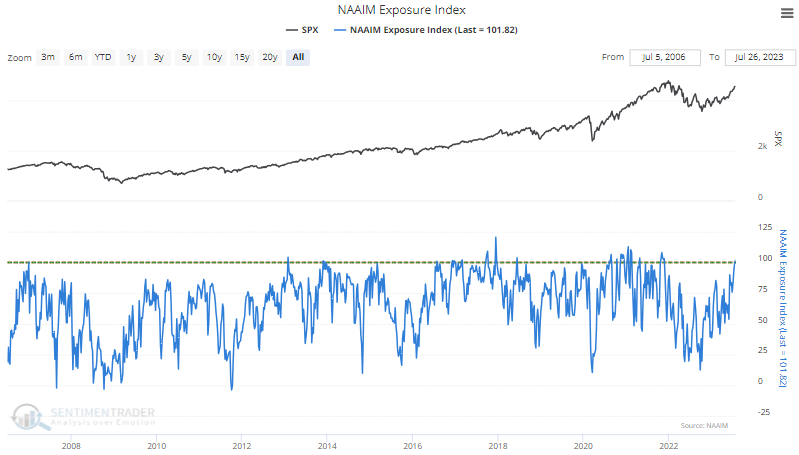

Active managers are fully invested, according to a survey

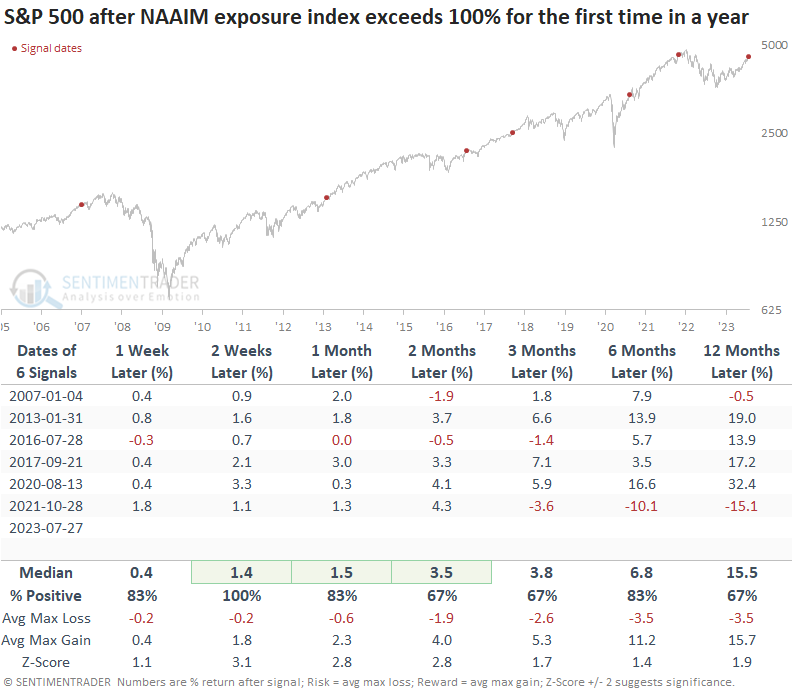

The National Association of Active Investment Managers (NAAIM) exposure index crossed above 100% for the first time in a year. The index measures the average exposure to US Equity markets reported by members and can range from 200% long to -200% short. A level of 100% implies investors are fully invested.

While the sample size is small, when the exposure index crosses above 100% for the first time in a year, the S&P 500 consistently rises over the next year. Moreover, despite being fully invested, stocks tend to follow through in the near term, with a 100% win rate two weeks later.

What the research tells us...

As we've seen with other sentiment surveys and real money indicators, shifts from pessimism to optimism are bullish for equity markets. Remember, sentiment, like valuations, is a pre-condition. Other factors, such as market breadth, must deteriorate before we should be concerned about a significant drawdown. Consolidations and 3-5% corrections can occur out of nowhere and are extremely difficult to market time. That's why my TCTM Composite Risk Warning Model contains big-picture algorithms.