Metal muddle

Key points

- Except for gold bullion, the metals and mining markets and sectors have been very weak of late

- Also, except for gold bullion, seasonality is an unfavorable factor across much of the metals arena in the months ahead

- The combination of weak prices and weak seasonality suggests that investors tread lightly on the long side and that traders look for opportunities to play the short side

Gold is the solitary leader

Much of the talk surrounding metals focuses on gold and its breaking out to new highs this year. Often, the implication is that "gold is strong; therefore, metals are a great place to be." And if you focus solely on gold, there appears to be something to it. The chart below displays a market in an apparent powerful uptrend.

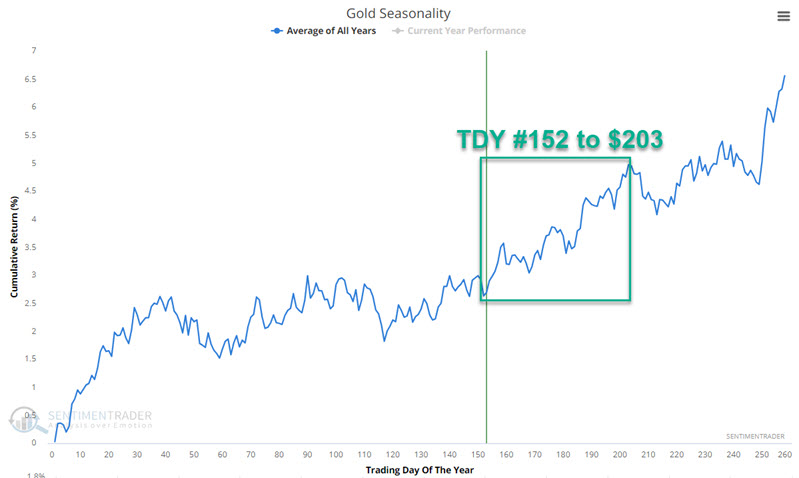

In addition, the annual seasonal trend chart below for Gold shows a favorable period that extends from the close of Trading Day of the Year (TDY) #152 through TDY #203.

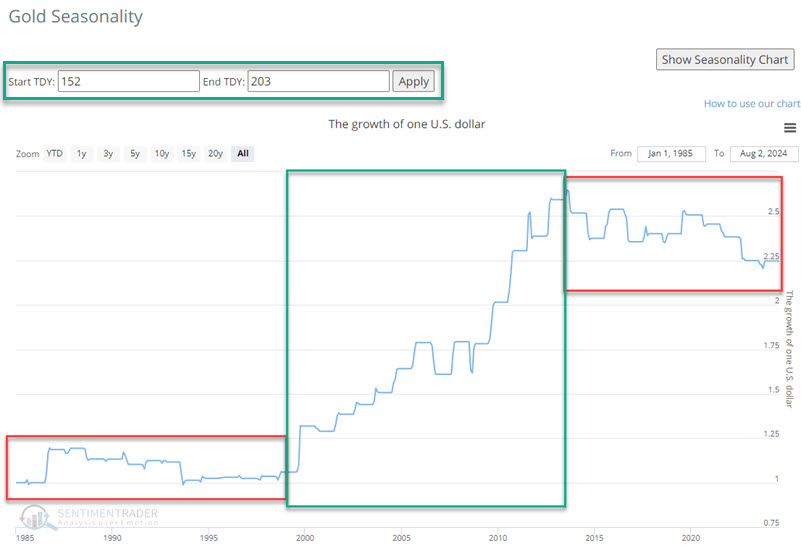

The chart below displays the hypothetical growth of $1 invested in Gold only during the TDY #152 through #203 period since 1985. Overall, it's positive, but not exactly a "sure thing."

So, should we buy the assertion that "gold is strong, so metals are strong"? Let's take a closer look.

Gold stocks are a different story

In this article dated 2024-07-16, I warned about some worrisome developments for gold stocks. Through 2024-08-02, the VanEck Gold Miners ETF (ticker GDX) has lost over -7%.

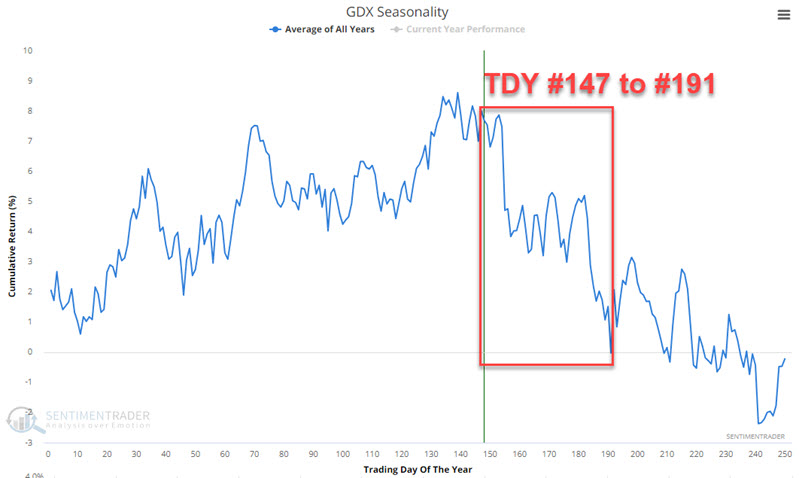

The annual seasonal chart for GDX shows an unfavorable seasonal period that extends from TDY #147 to TDY #191.

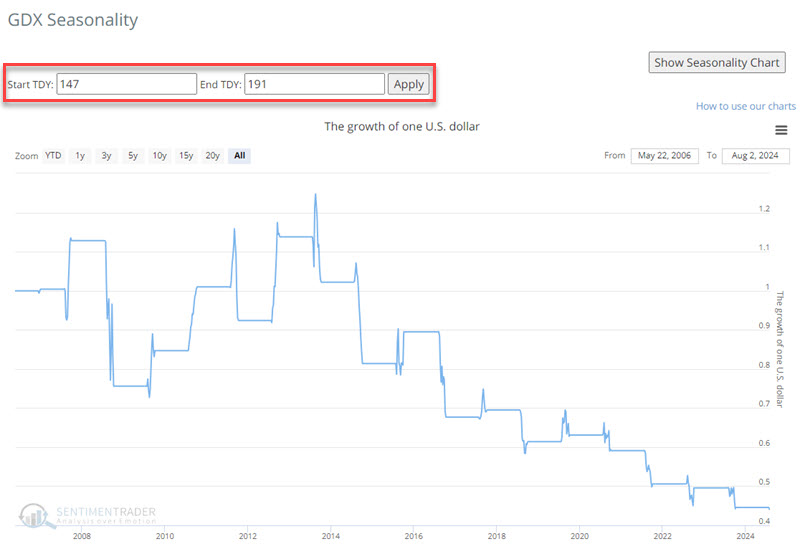

The chart below displays the hypothetical growth of $1 invested in GDX only during the TDY #147 through #191 period, during which GDX started trading in 2006. Is GDX sure to decline during this period every year? Not at all. But importantly, betting on a rally during this period sure looks like "swimming upstream."

Other metals also diverge from gold

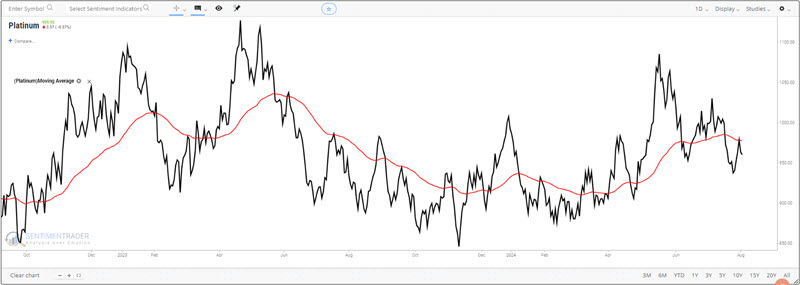

Gold mining stocks have a history of spotty performance. But "what's good for gold is good for other metals" is a common line of thinking. Common, but often incorrect. Let's first consider another "precious metal," platinum. While gold threatens new all-time highs, platinum is languishing and lagging badly.

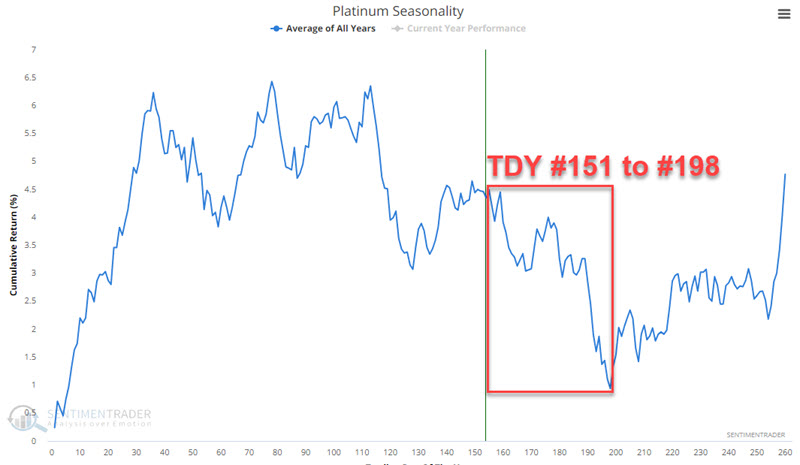

The annual seasonal chart for platinum futures shows an unfavorable seasonal period that extends from TDY #151 to TDY #198.

The chart below displays the hypothetical growth of $1 invested in platinum only during the TDY #151 through #198 period since 1987. During these periods, the price of platinum has declined by almost 80%.

Now, let's look at the leading industrial metal, copper. From February into May, copper's price soared almost 40%. In just over two months since it has plummeted 20%.

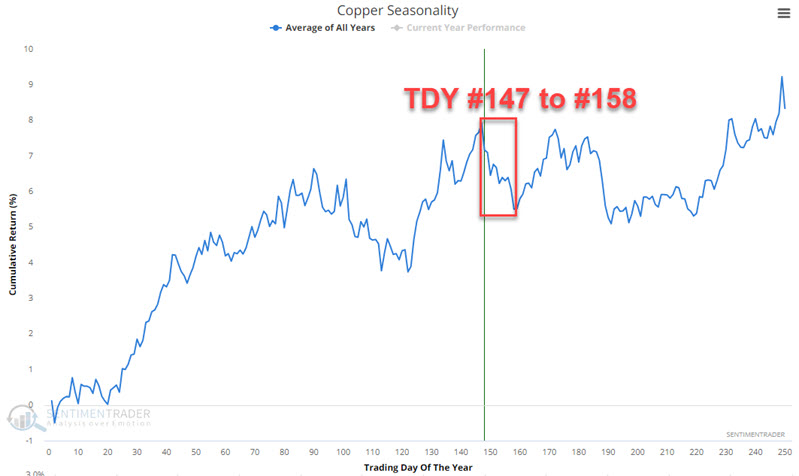

Could copper bounce in the near term? Of course. However, seasonal and price trends suggest this could be a very high-risk play. The annual seasonal chart for copper futures shows an unfavorable seasonal period that extends from TDY #147 to TDY #158.

The chart below displays the hypothetical growth of $1 invested in copper only during the TDY #147 through #158 period since 1985. After considerable up periods in 1989 and 1990, this period has been challenging for copper bulls. Since 1991, the price of copper has lost -55% of its value if held only during this period.

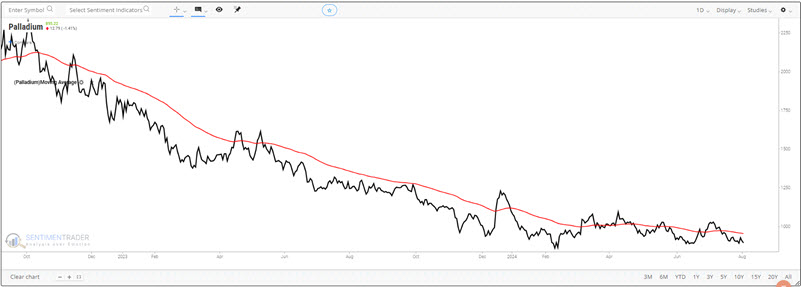

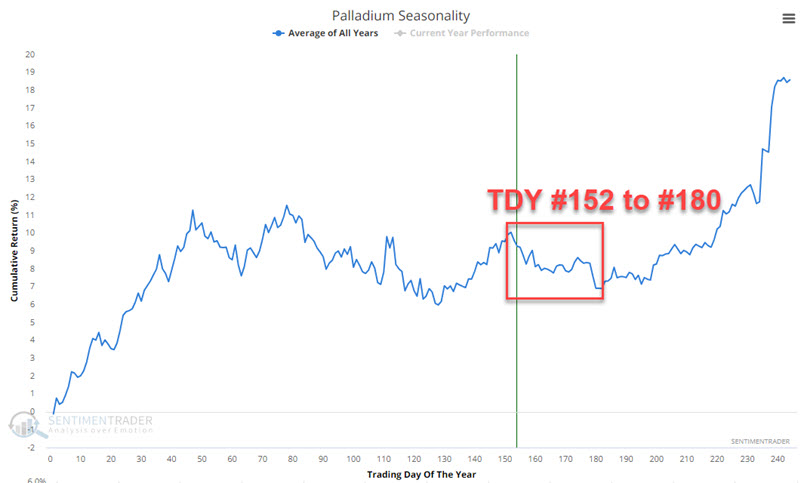

Palladium is another industrial metal that does not follow gold's lead. Between March 2022 and February 2024, palladium lost over 70% of its value. Since then, it has been trading sideways in a range.

A significant breakout often follows an extended sideways base and moves higher. Is it time to bet on that with palladium? Seasonality suggests "not yet." The annual seasonal chart for palladium futures shows an unfavorable seasonal period that extends from TDY #152 to TDY #180.

The chart below displays the hypothetical growth of $1 invested in palladium only during the TDY #152 through #180 period since 1994.

Metals-related stocks are entering the "danger zone"

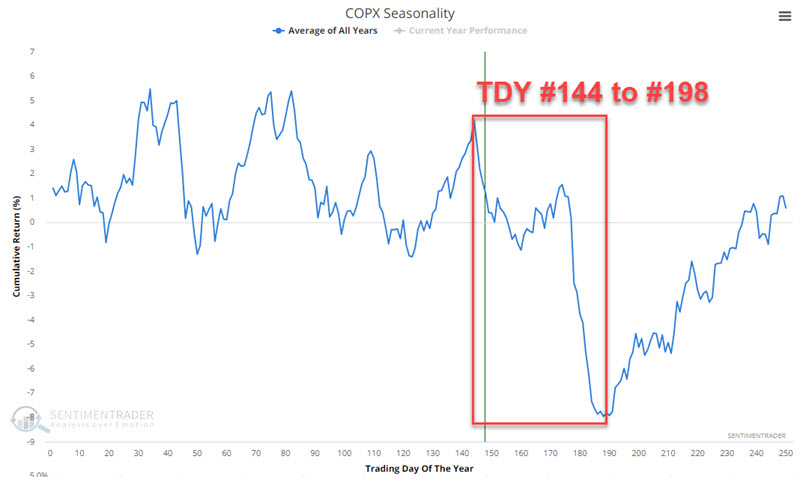

We looked at gold mining stocks earlier. Let's spread our horizon just a little wider. The Global X Copper Miners ETF (ticker COPX) tracks an index of copper mining stocks. Like copper, the metal (highlighted above), copper mining stocks have fallen hard in recent months.

Is this a buying opportunity? Again, anything is possible. However, seasonality suggests that now is not the time. The annual seasonal chart for COPX shows an unfavorable seasonal period that extends from TDY #144 to TDY #198.

The chart below displays the hypothetical growth of $1 invested in COPX only during the TDY #144 through #198 period since 2010. The results speak for themselves.

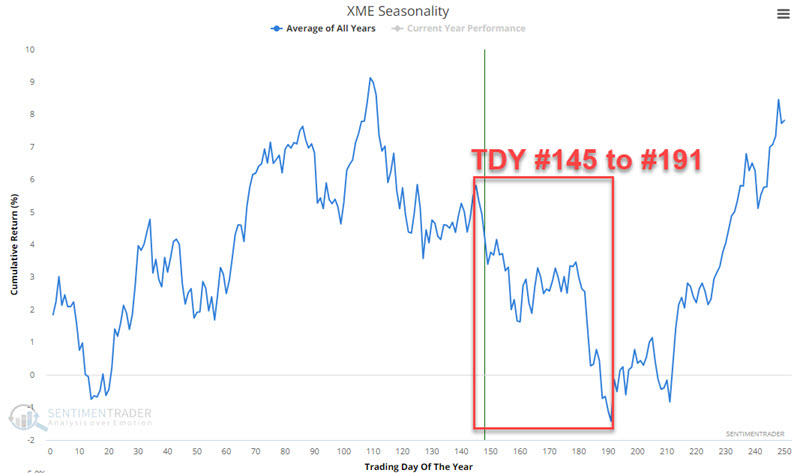

The SPDR S&P Metals & Mining ETF (ticker XME) tracks the broad S&P 500 Metals & Mining index. XME has plunged over -9% in the last two weeks.

The annual seasonal chart for XME shows an unfavorable seasonal period that extends from TDY #145 to TDY #191.

The chart below displays the hypothetical growth of $1 invested in XME only during the TDY #145 through #191 period since 2006.

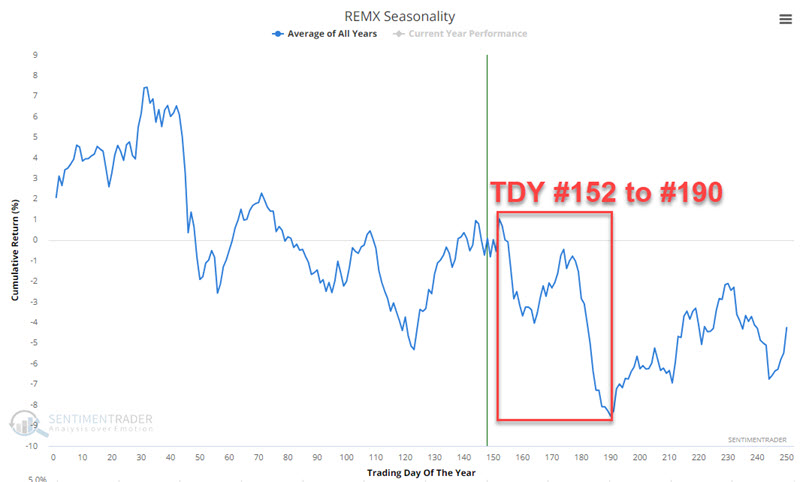

Finally, let's look at the performance of rare metals via the VanEck Rare Earth and Strategic Metals ETF (ticker REMX). REMX has lost -70% since peaking in April 2022.

Are you feeling compelled to "pick a bottom" in REMX? The annual seasonal chart for REMX shows an unfavorable seasonal period that extends from TDY #152 to TDY #190.

The chart below displays the hypothetical growth of $1 invested in REMX only during the TDY #152 through #190 period since 2010

What the research tells us…

Gold looks good. Price action is strong, and seasonality is entering a favorable period. Beyond that, price action and seasonality for virtually all other metals and metal sectors are unfavorable. Could the other markets highlighted above surprise in 2024 and bounce sharply higher in the months ahead? That absolutely could happen. However, as investors and traders, one of our primary responsibilities is to allocate capital into investments and trades with the highest likelihood of success. There is little in the information above to suggest that that involves a significant allocation to long positions in the metals arena in the months ahead. On the contrary, aggressive traders might consider any short-term bounce in some of the beaten-down metal vehicles highlighted above as an opportunity to press the short side in the months directly ahead.