Jobless claims trigger a bullish signal for stocks

Key points:

- Continuing jobless claims cycled from a 52-week high to a 16-week low

- Similar reversals in continuing claims resulted in excellent returns for the S&P 500

- Cyclical sectors outperformed defensive ones

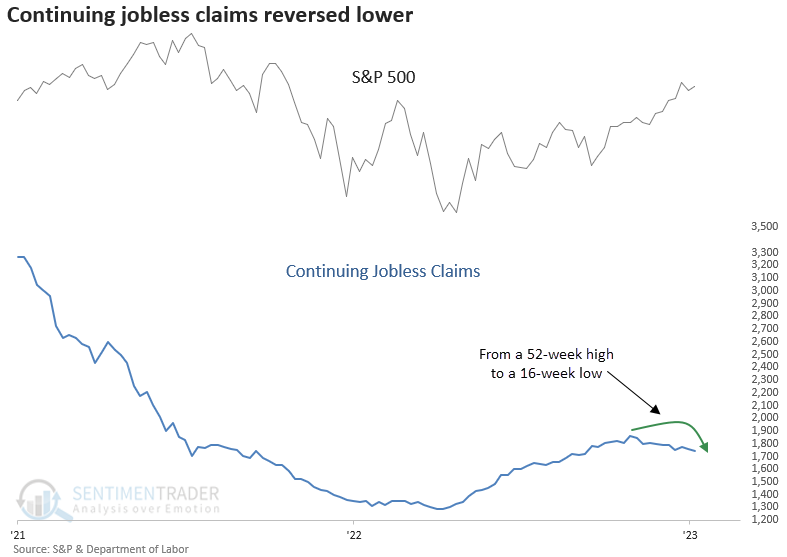

An interesting development from one employment data series

On Thursday, the Department of Labor released the latest weekly jobs data, and both initial and continuing jobless claims declined.

While the initial claims showed a significant week-over-week plunge, the continuing claims caught my attention. After steadily rising for seven months to a 52-week high in April, continuing claims have now fallen to a 16-week low. The presence of elevated continuing claims can be a sign of sluggish employment and economic growth. So, the reversal to a 16-week low is an interesting development in the debate over a soft or hard landing for the economy.

Let's assess the outlook for stocks and a manufacturing survey when the continuing jobless claims cycle from a 52-week high to a 16-week low.

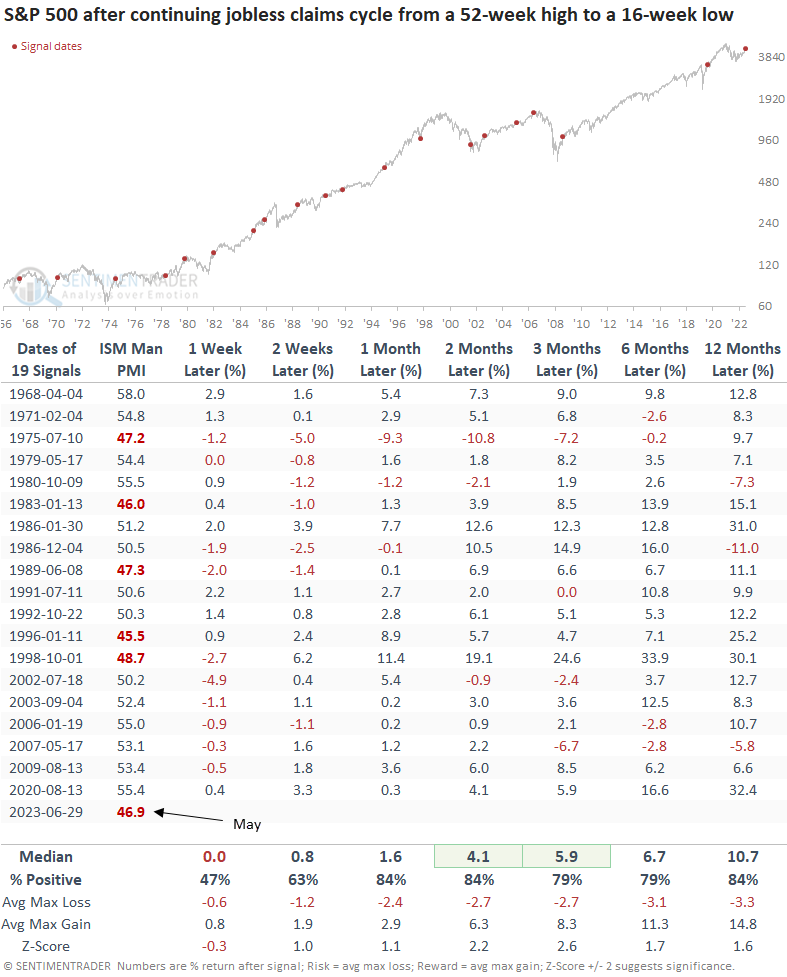

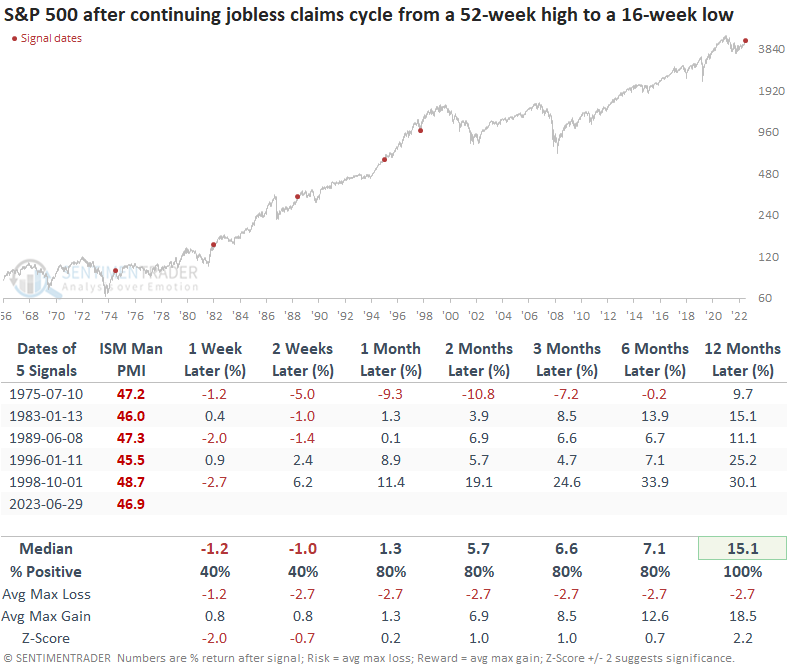

Similar reversals in continuing claims preceded positive returns

The S&P 500 demonstrates excellent returns and win rates when the continuing claims cycle from a 52-week high to a 16-week low, particularly over medium and long-term horizons. The only notable drawdown occurred in 1975, representing a correction following a substantial rally from the 1974 bottom.

I used the as-of-release date.

When I isolate the signals associated with a contraction in the ISM Manufacturing PMI, like now, the S&P 500 was higher a year later every time.

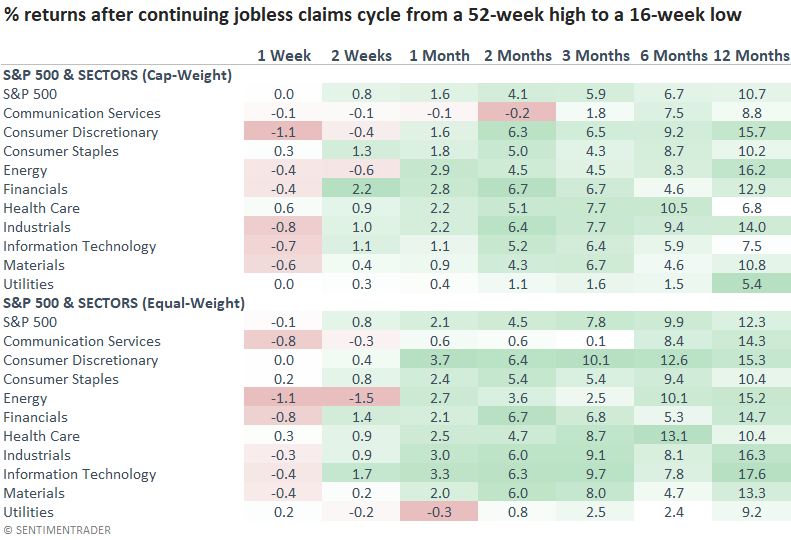

How should one position a portfolio when continuing claims reverse lower?

An improvement in the continuing claims suggests one should favor cyclical groups over defensive ones. Remember, historical returns serve as a general guide. It's crucial to utilize relative strength indicators to ensure that current-day trends align with past performance.

Can an improvement in continuing claims impact the manufacturing sector?

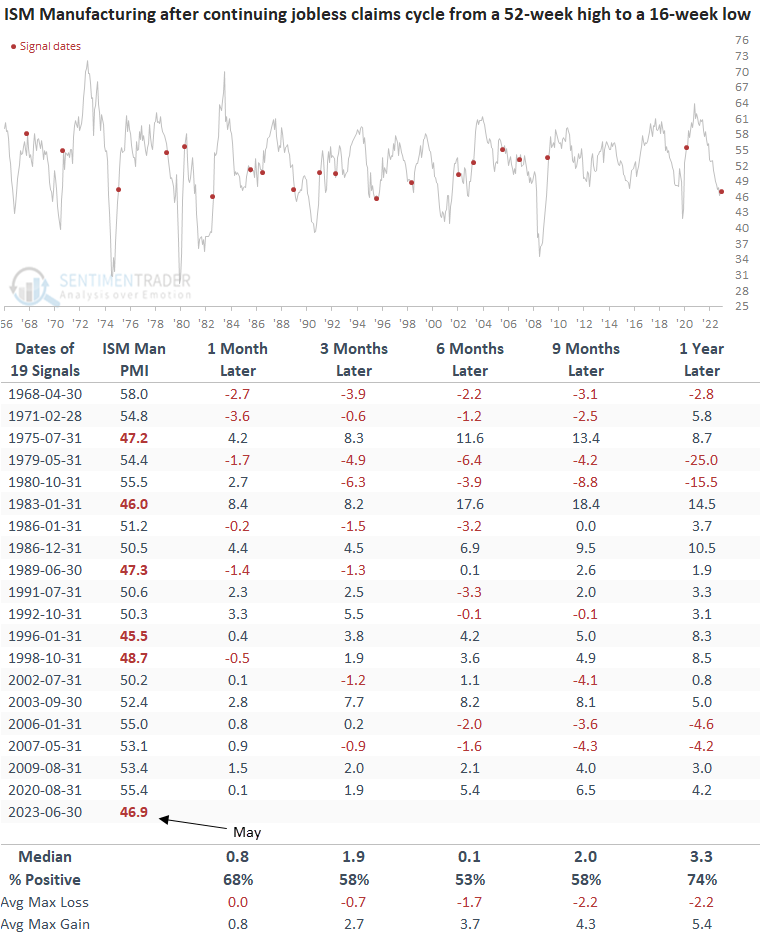

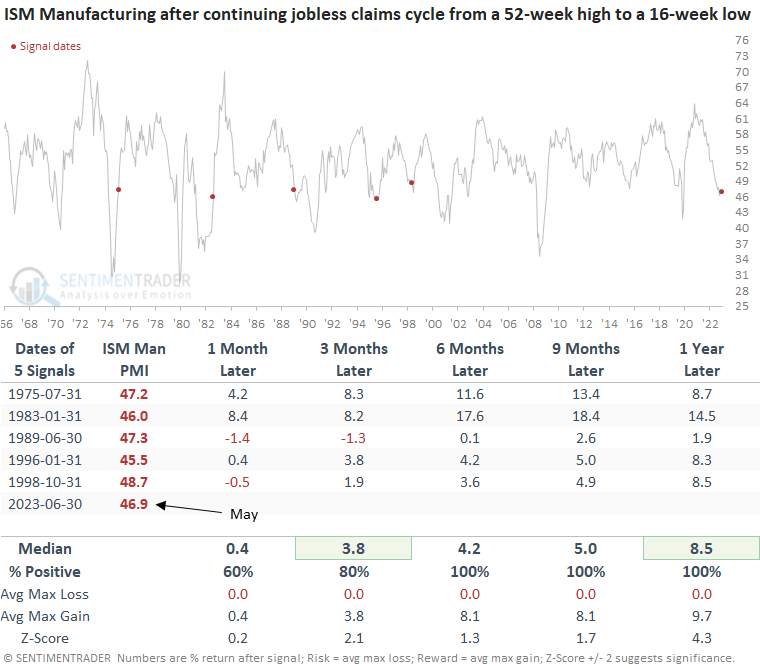

Applying the continuing claims signals to the ISM Manufacturing PMI data reveals a positive correlation, indicating that an improvement in employment data tends to lift the manufacturing survey. The last occurrence of a continuing claims reversal coinciding with an ISM manufacturing PMI survey reading this low dates back to 1996.

Could the manufacturing sector be close to a turning point?

In cases where the continuing claims reverse with the ISM Manufacturing PMI in contraction territory, the manufacturing survey has increased every time in the subsequent six, nine, and twelve-month periods.

What the research tells us...

Whether housing or now continuing claims, the economy remains resilient in the face of a sharp increase in interest rates. The latest data to show improvement, continuing claims, cycled from a 52-week high to a 16-week low, triggering a bullish signal for stocks, especially cyclically-oriented groups. The improvement in employment tends to lift manufacturing, especially when the ISM survey was in contraction territory.