Is Consumer Confidence the Ultimate Contrarian Indicator?

Key points:

- Consumer confidence measures tend to be useful contrarian indicators

- Plunges in consumer confidence are reported in the news as ominous warnings

- Few understand the implications of low confidence for stocks and bonds

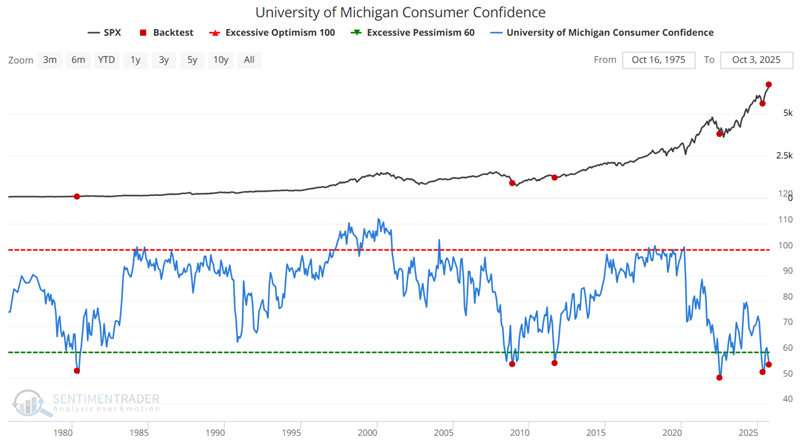

University of Michigan Consumer Confidence has plunged (Hooray for stock owners!)

If you listen to a financial news talk show host discuss low consumer confidence, you will hear it in hushed tones, couched in ominous warnings of impending fear and loathing and tough times ahead. Of course, this entirely ignores the contrarian nature of investor and consumer sentiment.

The chart below highlights those rare occasions when the University of Michigan Consumer Confidence survey crossed below 56%. The most recent signal occurred on September 30th.

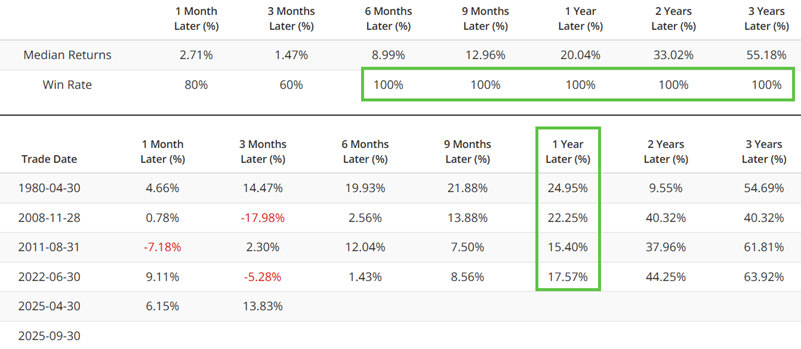

Does anything jump out at you just from eyeballing the chart above? The table below quantifies the performance of the S&P 500 index following the signal dates highlighted in the chart above.

While no signal is ever guaranteed to work "this time around," the results in the table above are "compelling."

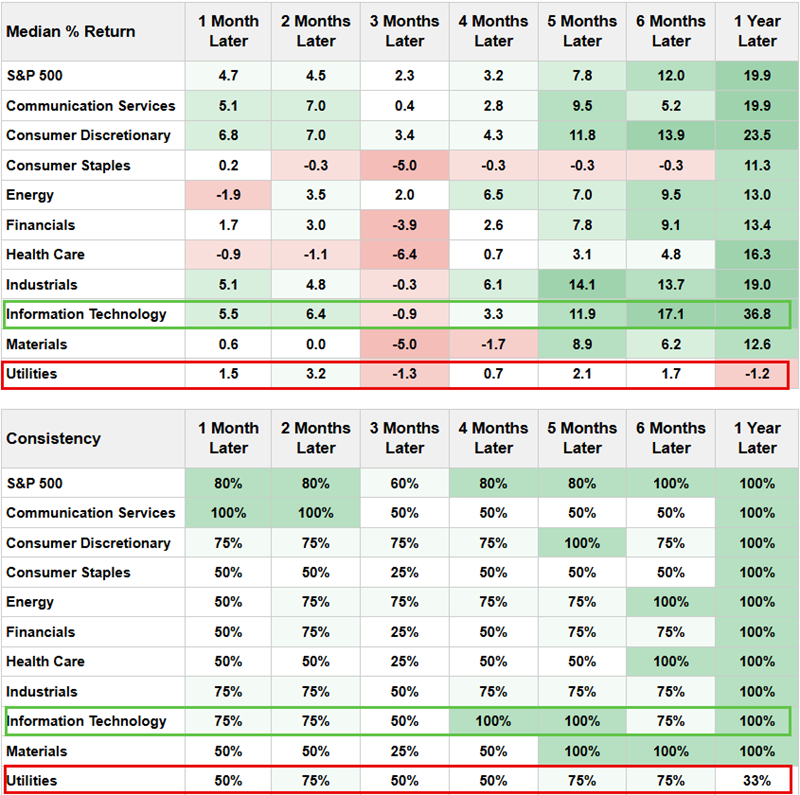

The table below displays performance for the various S&P 500 sectors following the signal dates. While much is to be gleaned, the most compelling item is the stark difference in performance between Technology (100% twelve-month Win Rate and 36.8% Median Return) and Utilities (33% twelve-month Win Rate and -1.2% Median Return).

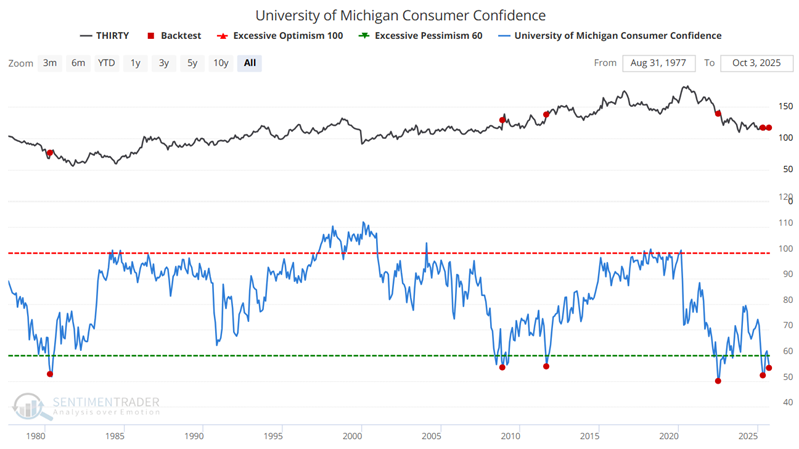

University of Michigan Consumer Confidence has plunged (Bond buyers beware!)

Low consumer confidence readings raise the specter of a poor economy. Many expect an impending decline in economic growth to be accompanied by declining interest rates. Ergo, the conventional wisdom surrounding low consumer confidence is that bonds will perform well. How has this theory held up in reality?

The chart below highlights those rare occasions when the University of Michigan Consumer Confidence survey crossed below 56% with the thirty-year treasury bond futures contract as the relevant index. The most recent signal occurred on September 30th.

The table below quantifies the performance of thirty-year treasury bond futures following the signal dates highlighted in the chart above.

Once again, there is no guarantee that t-bonds will decline in the months and years ahead. That said, this indicator suggests avoiding a significant commitment to long-term treasury bonds at this time.

What the research tells us…

The most compelling argument for using sentiment to analyze the financial markets is that human nature is the one constant. Fear and greed are universal human emotions. When they reach an extreme, the attendant groupthink gets turned on its head, and the market (typically) looks the other way. The reactions of the stock and bond markets to the extreme in consumer confidence detailed above are a classic case in point. While the end-of-September reading in the U of M Consumer Confidence survey does not guarantee higher stock prices and/or lower bond prices in the year ahead, the results highlighted strongly suggest giving stocks the benefit of the doubt, much more so than the bond market.