Investors baked in gains ahead of earnings season

Key points:

- The S&P 500 rallied more than 6% in the month before earnings season

- This is one of the best pre-earnings season rallies since 1950

- Big rallies before the season began did not consistently pull forward future returns though Q1 is a worry

A very good earnings season...before it begins

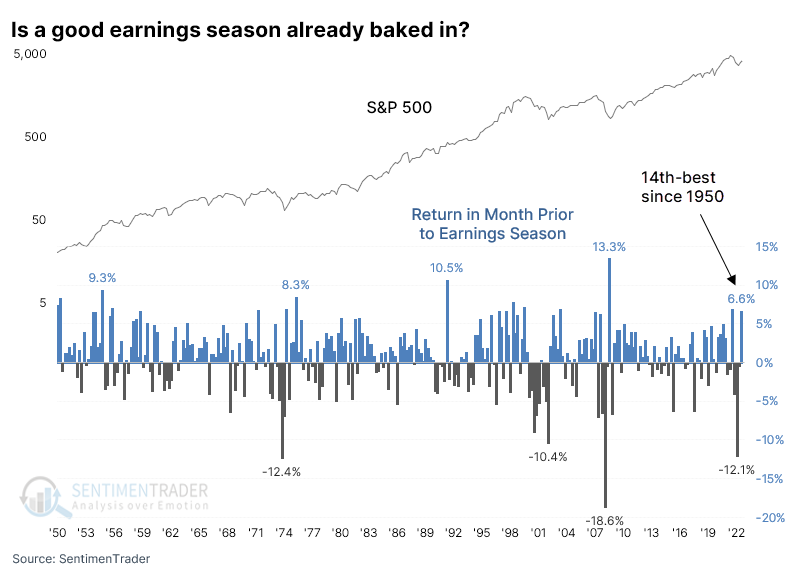

Is a good earnings season already baked in? Bloomberg notes that investors have been bidding up stocks in anticipation of good news:

Investors staring down what is forecast to be the biggest drop in corporate earnings since the Covid recession have had no trouble bidding up US stocks. By one measure, they've powered equities to the biggest pre-earnings rally since early 2009, as the S&P 500 jumped almost 6% in the month through Friday even as first-quarter profits are forecast to drop 8%.

There are many caveats with that assertion, primarily the assumption that investors buy stocks thinking only about the next quarter's earnings. Many investors think in years or decades, and many others don't consider earnings at all.

But let's just take the surface argument that over the past month, investors (traders, really) think that earnings season will bring good news and have already bought in advance. If that's the case, then this is one of the most-baked-in earnings seasons since 1950. With more than a 6% rally in the month prior to the start of earnings season, the S&P 500 locked in the 14th-best pre-earnings month.

When earnings are baked in (and not)

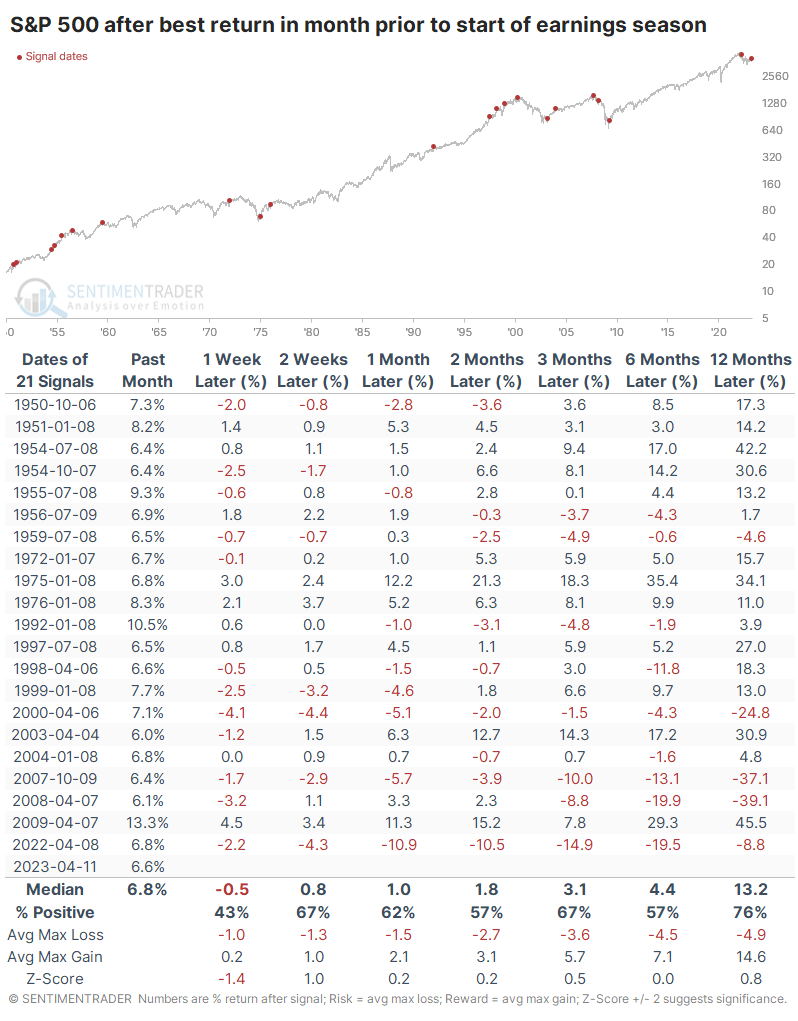

The table below shows the earnings seasons that saw the largest rallies in the S&P in the month prior to the start of the season. On average, the index gained nearly 7% during those four-week stretches, so the current one is right around average.

The baked-in argument has a bit of merit in the very short term. Over the first week of earnings, the S&P rallied 43% of the time, with a negative median return. But after that, the case becomes much harder to make. Earnings season runs roughly 30 trading days, between one and two months. And in the month following these signals, the index rallied 62% of the time, with its average max gain exceeding the average max loss.

Across all future time frames, the S&P's return was better than random. Granted, there was nothing special in the returns, but that's kind of the point - the "baked-in good news" didn't radically impact forward returns, though anyone buying last year would disagree.

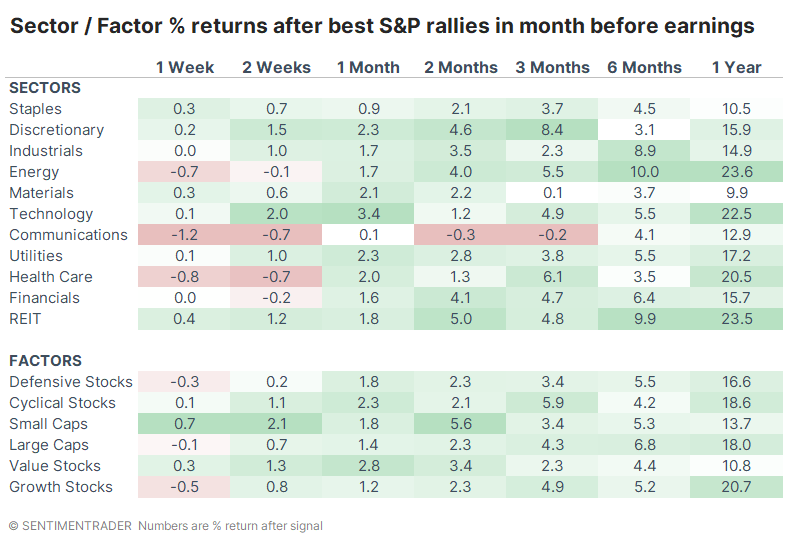

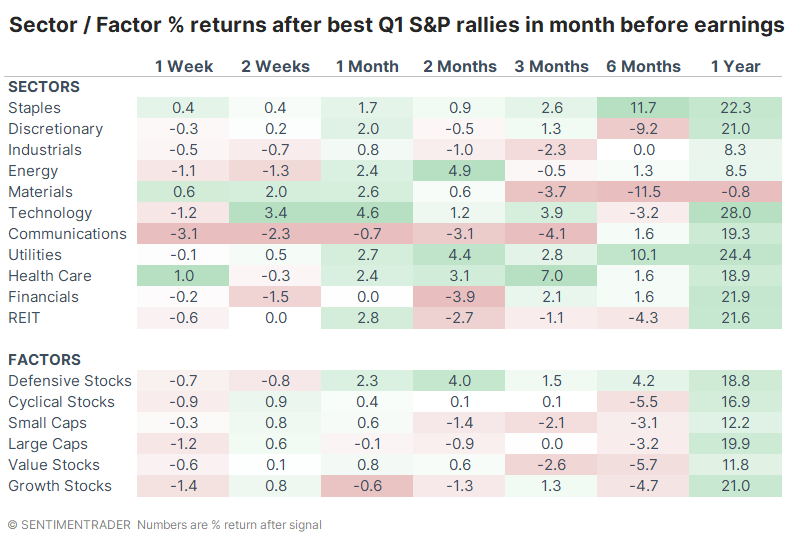

Among sectors, Technology and Discretionary stocks tended to react the best in the month following these signals.

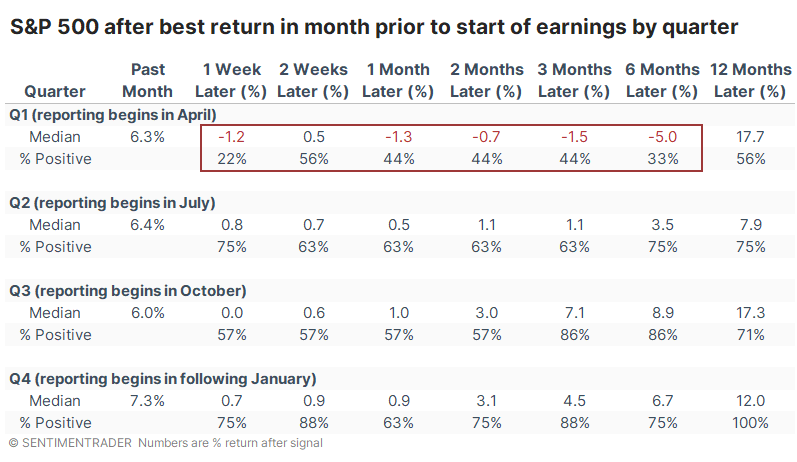

There is some bad news for bulls, however. If we break down the prior-month rallies before earnings season by quarter, then the current one comes out the worst, by far. When the S&P 500 rallied hard into Q1 earnings season - when companies start to report their results in April - then forward returns were quite poor.

Across all time frames, forward returns were the least consistently positive, and usually had the worst median returns during Q1 earnings season. Three months later, the S&P averaged a return of -1.5% and was positive only 45% of the time. Compare that to times when stocks rallied into Q4 reporting season, when the S&P rallied 88% of the time, averaging +4.5%, over the next few months.

Even though overall Q1 forward returns were weak, Technology and Discretionary still tended to do well. In fact, Tech returns actually increased compared to other quarters.

What the research tells us...

Even though stocks rallied hard in the month prior to the latest earnings releases, it doesn't necessarily mean that investors have already priced in good earnings. It's always dicey assigning meaning to moves in stock prices anyway. And even when the S&P 500 rallied 6% or more in the month before earnings season began, it didn't consistently lead to poor returns going forward, other than perhaps in the first week. The biggest caveat is seasonality because when these gains occurred before Q1 reporting season, then forward returns were significantly worse than other quarters. The sample size drops by a lot, which makes it harder to rely on the data. Overall, it looks like perhaps a mild worry for bulls at worst.