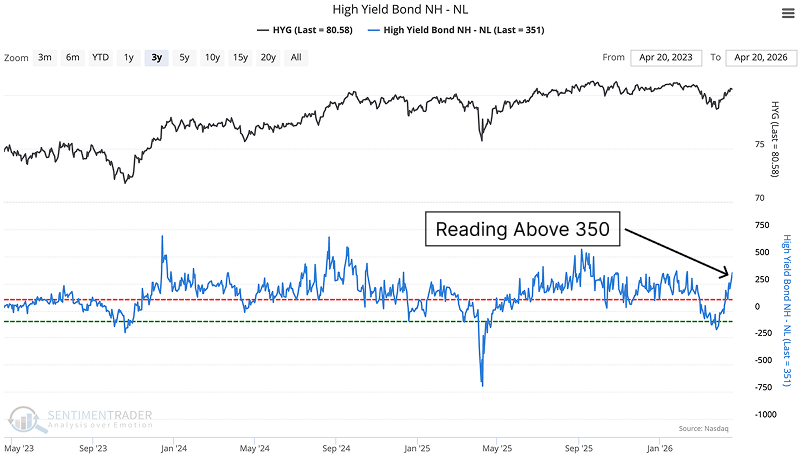

High-yield bonds are showing signs of weakness

Key points:

- New highs for high-yield bonds outpace new lows by a wide margin

- Longer-term breadth measures for the high-yield bond market are diverging from stocks

- There are few precedents for similar behavior, but the ones that exist suggest limited upside

The junk bond rally is running on fumes

When things get so good that it's hard to imagine anything going wrong, it's often (not always) a good time to be nervous. Reasons tend to come out of nowhere, markets rarely reward overconfidence.

One of our favorite early-warning markets is the high-yield (junk) bond market. When investors begin to worry about credit quality, it has often given a heads-up as equity investors were more focused on the upside instead of possible downside.

When high-yield bond new highs significantly outpace new lows-especially when breaching the 350-point threshold-it looks like a structural green light. The reality in the credit market is quite different. This extreme breadth reading is an exhaustion event for junk bonds.

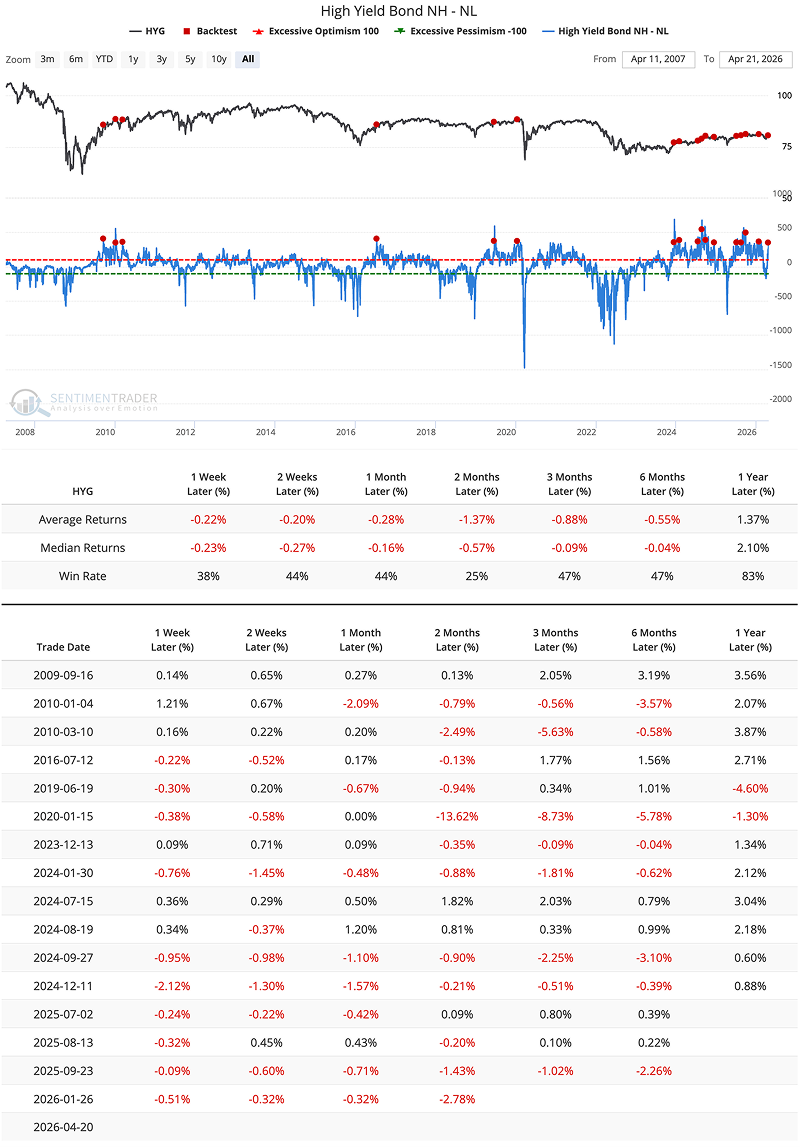

Two months after the signal, HYG