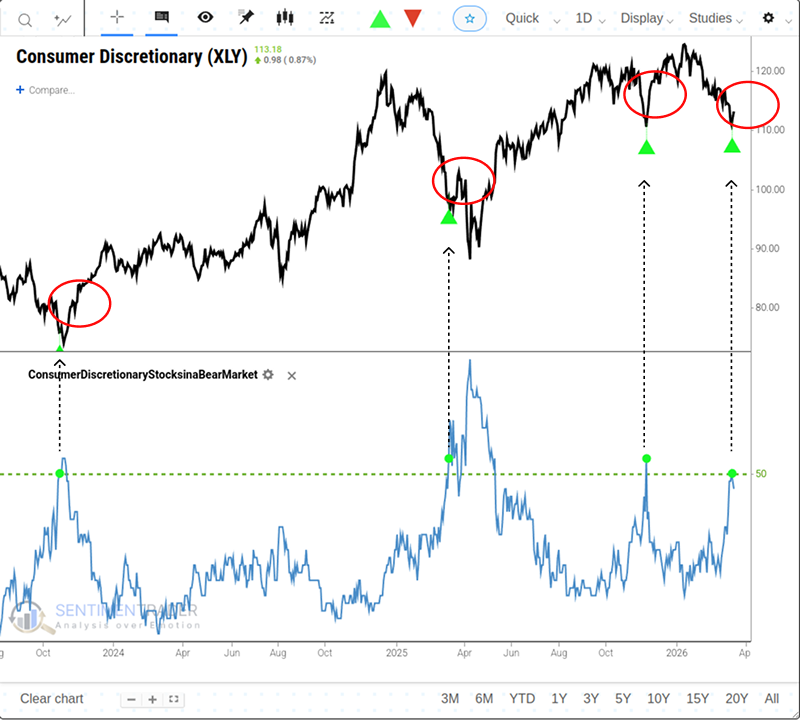

Half of Consumer Discretionary stocks are in a bear market

Key points

- The percentage of S&P 500 Consumer Discretionary stocks in a bear market (down 20% from a 252-day high) has reached 50%.

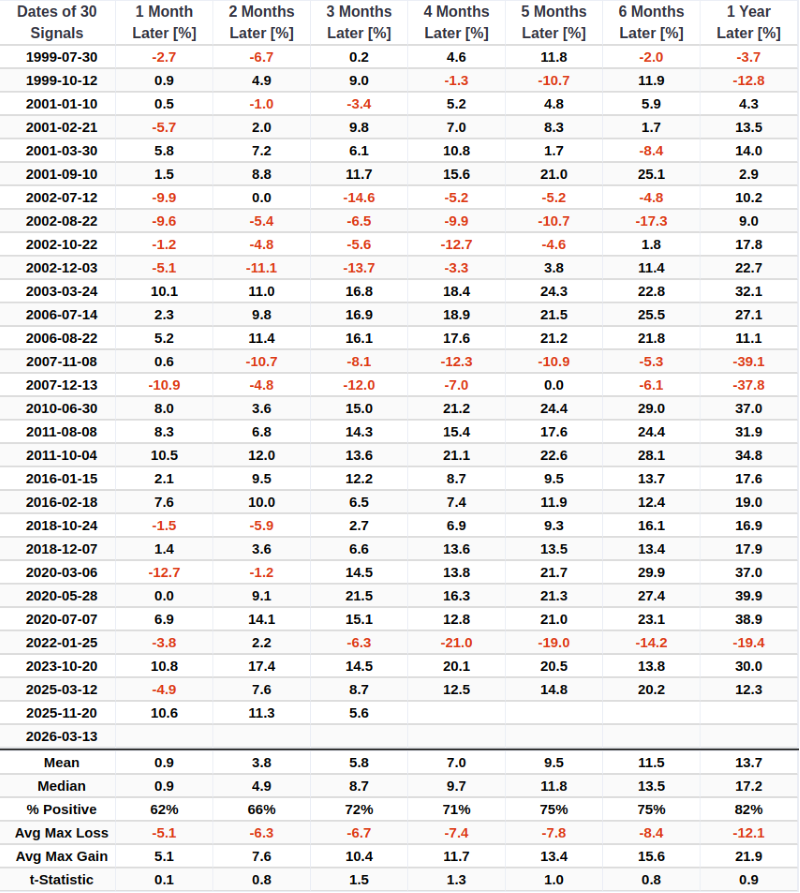

- When this extreme washout occurs, the Consumer Discretionary sector (XLY) has historically achieved an 82% win rate over the subsequent year.

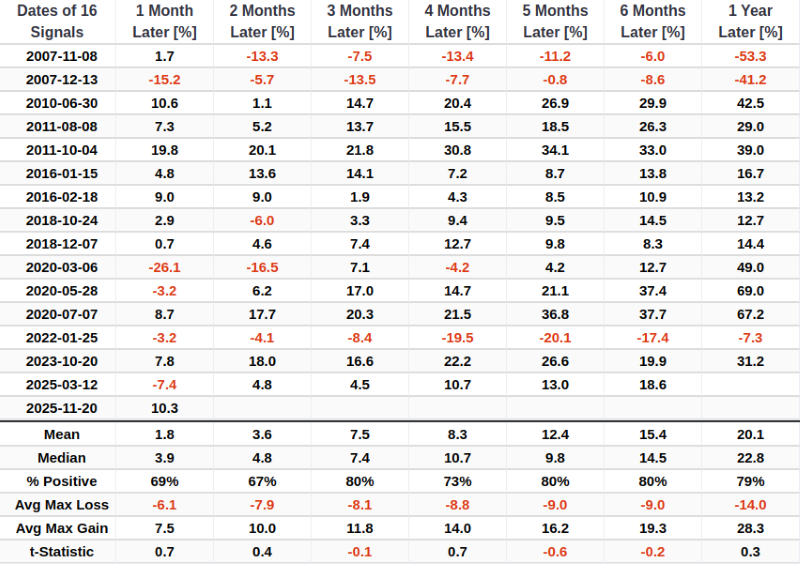

- The Equal-Weight Consumer Discretionary ETF (RSPD) has historically outperformed the cap-weighted ETF (XLY) following these capitulation events.

- A separate breadth indicator-the percentage of XLY stocks above their 50-day moving average plummeting from >80% to <20%-corroborates this extreme oversold condition, supporting a bullish medium-to-long-term outlook for both the sector and the broader market.

When Fear Peaks, Opportunity Follows

The percentage of Consumer Discretionary stocks within the S&P 500 that have entered a bear market (defined as a 20% decline from a 252-day high) has crossed above 50% for the 30th time in over 20 years. The last time this signal triggered was on Nov 20, 2025, and XLY rallied by more than 10% over the following month.

This swelling proportion of battered stocks within a highly pro-cyclical sector highlights peak pessimism. In our view, at this juncture, the bearish macroeconomic narrative has been discounted by the market. This sets up a textbook asymmetric risk/reward scenario for investors willing to step in while sentiment is washed out.

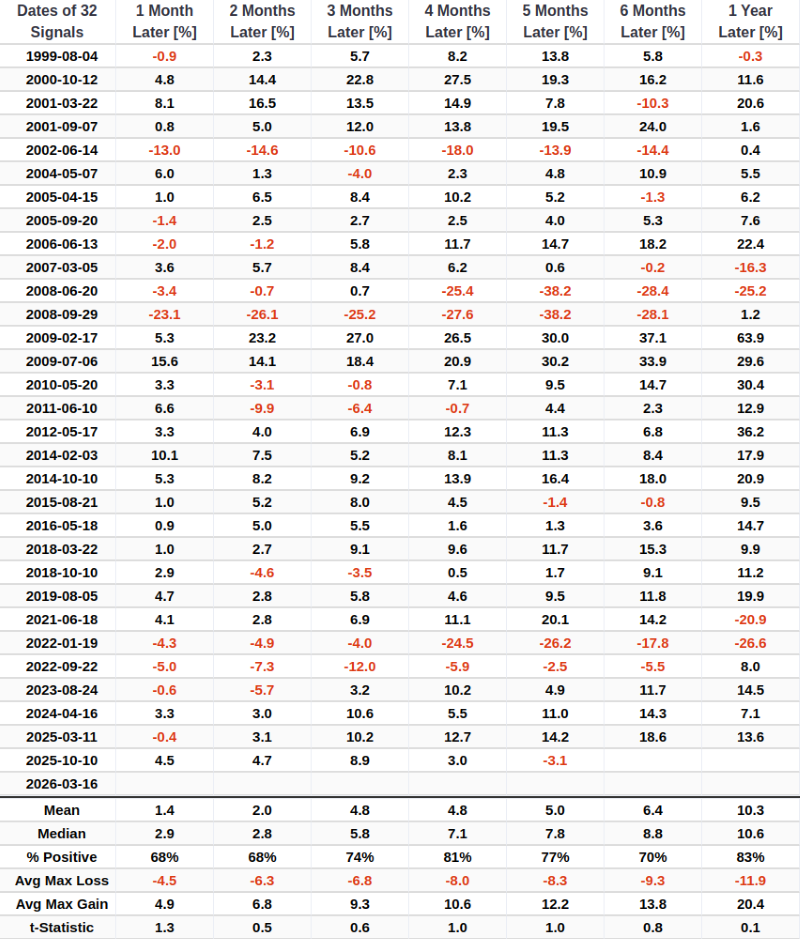

Similar breakouts yielded an 82% win rate over the following year

When the proportion of Consumer Discretionary stocks in a bear market cycle rises to 50% or higher, the Consumer Discretionary sector has performed exceptionally well over the next 12 months. For related backtest, click here.

The option for exposure to the Discretionary sector if the bear market is over

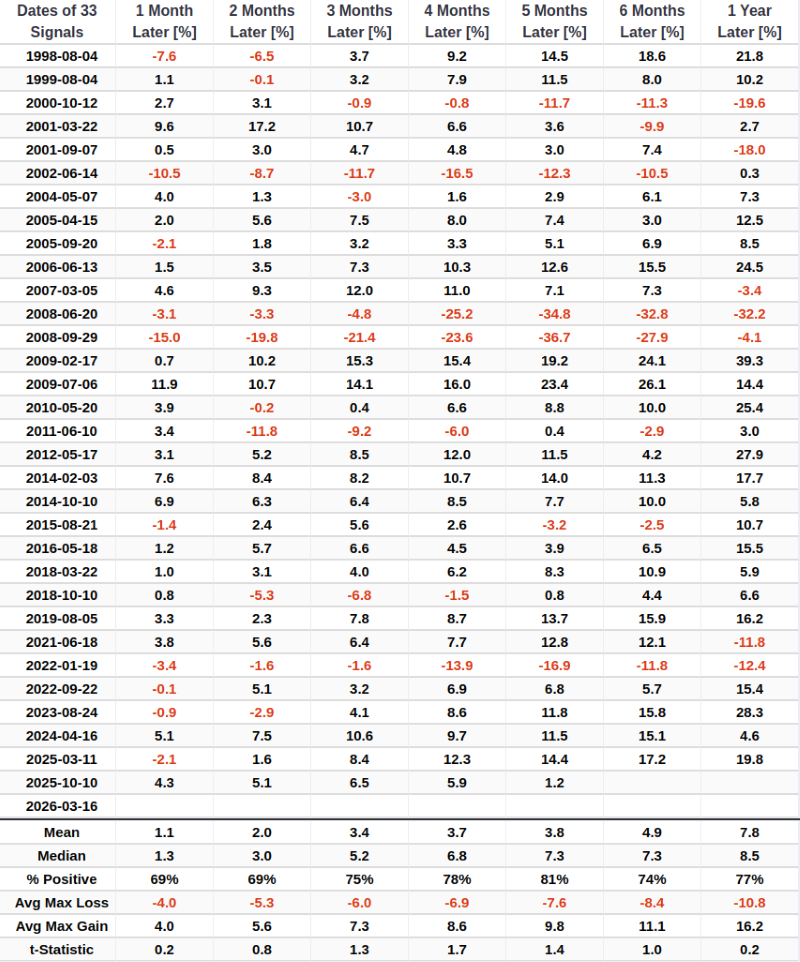

With the advent of ETFs, investing in a basket of stocks to capitalize on historical trends is more convenient and cost-effective than ever. Assuming the pessimism in consumer discretionary stocks signals that the bear market is over, investors might consider investing in the Invesco S&P 500 Equal Weight Consumer Discretionary ETF (RSPD) rather than the cap-weighted discretionary ETF (XLY).

As the table illustrates, the equal-weight consumer discretionary sector tends to outperform and generate higher returns than its market-cap-weighted counterpart following these events.

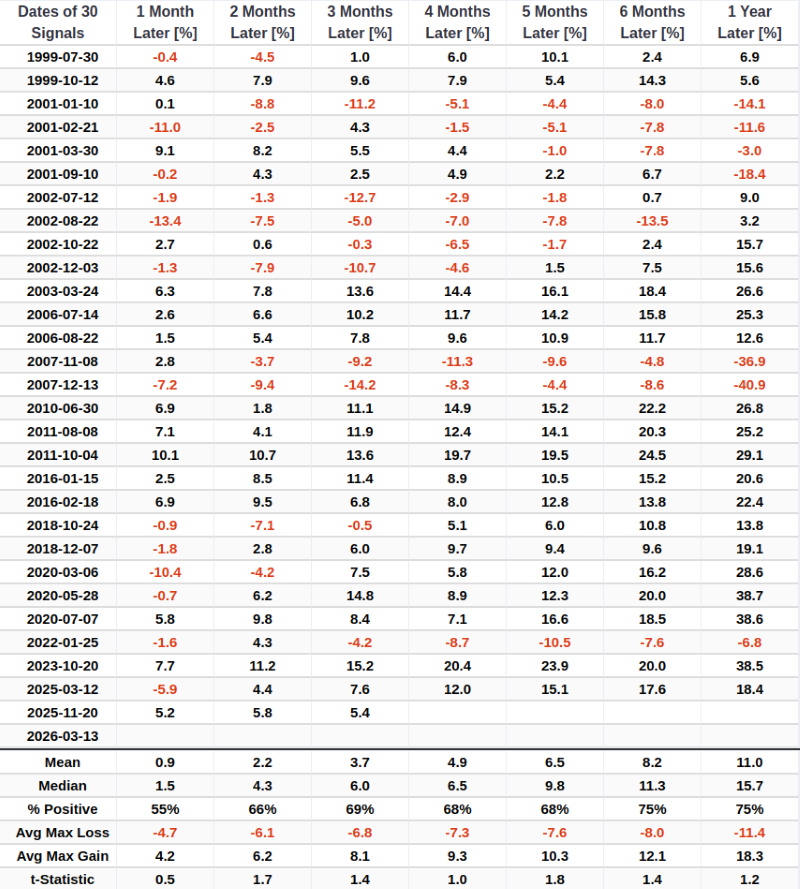

Furthermore, when the percentage of consumer discretionary stocks in a bear market reaches 50% or higher, the S&P 500-the world's most representative benchmark index-also exhibits a positive win rate over the six to twelve-month window.

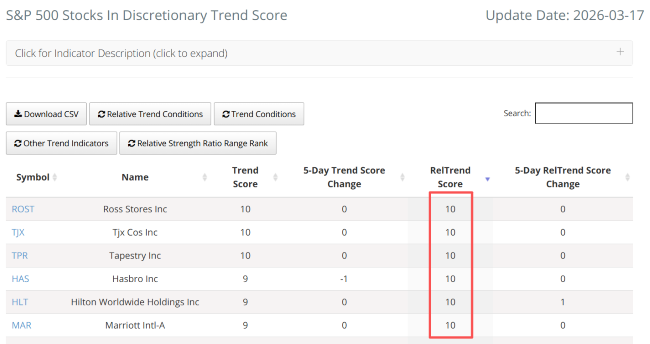

From the perspective of Relative Trend Scores, six stocks currently hold a perfect score relative to the S&P 500 Index.

Additional context from market breadth

The SentimenTrader team emphasizes two indispensable market analysis concepts in our research reports, among many others: the strategic use of composite models and the identification of reversal signals.

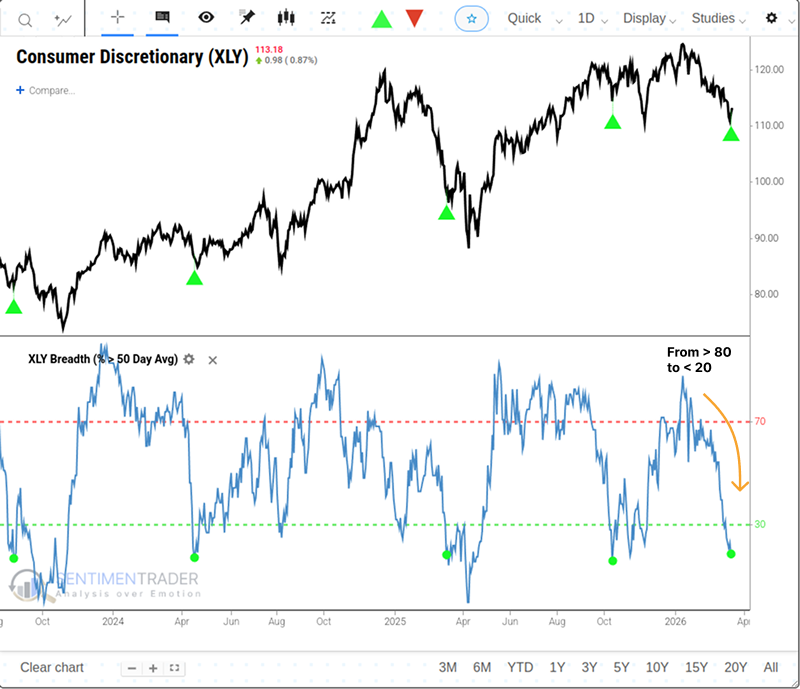

Last Friday, the percentage of S&P 500 Consumer Discretionary stocks trading above their 50-day moving average-XLY Breadth (% > 50 Day Avg)-plummeted from > 80% to < 20%. The latest reading stands at 20.83%.

Following similar sharp reversals from overbought to oversold, the Consumer Discretionary sector has trended higher 83% of the time exactly one year later. For related backtest, click here.

Similarly, this signal also augurs strong upward momentum for the broader market over the medium to long term.

What the research tells us...

The Consumer Discretionary sector has experienced a severe internal washout, with half of its constituents falling into bear market territory (down 20%+ from highs) and XLY Breadth (% > 50 Day Avg) plummeting below 20%. Rather than a warning sign, history shows that this level of capitulation in a highly cyclical sector usually marks peak pessimism. When selling pressure reaches this magnitude, the "weak hands" have been flushed out, setting the stage for a durable recovery. Both the sector and the S&P 500 have consistently delivered strong returns in the 6-to-12 months following these extremes, with the Equal-Weight version of the sector (RSPD) offering the better historical leverage to the subsequent rebound.