Expensive stocks crushed volatility Again

Key points

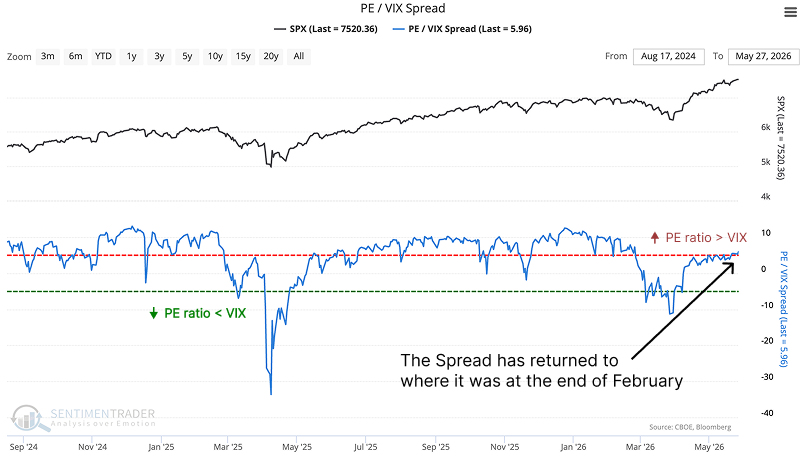

- The forward P/E ratio on the S&P 500 is nearly six points above the VIX, crossing back above 5.5 for the first time in more than three months

- Across 21 prior signals of the spread crossing above 5.5 with at least a 63-day gap, SPX was higher a year later 81% of the time, averaging an 8.2% gain

- The VIX was higher three months later 86% of the time, with a median surge of 47%, stocks rallied, but the ride got bumpier

- The risk was contained but not absent

Back to February levels

Over the past few weeks, stocks have pushed higher and volatility has been crushed. The result is the widest gap between what investors are paying for earnings and what they are pricing in for future volatility since late February. The spread between the S&P 500 forward P/E ratio and the VIX has crossed back above 5.5, landing at 5.96 on Wednesday, the first time in more than three months.

The spread sat above 5.5 for most of 2024 and early 2025 before pulling back. Now it is back, and it took more than 63 trading days to get here. That gap matters. When the spread lingers above this threshold for weeks or months, the signal gets noisy, the market has already priced in the complacency. The first surge after an absence is different.