Equal-weighted versus cap-weighted - Part II

Key points:

- In Part I, we highlighted a simple trend-following method for switching between the equal-weighted and capitalization-weighted S&P 500 indexes

- In Part II, we will add a seasonal component to the mix

- In Part III, we will put the two strategies together

Seasonal switching between cap-weighted and equal-weighted indexes

Many investors favor a buy-and-hold index strategy, and no index is more popular than the S&P 500. One weakness of this approach is that the largest companies in the index can assert an undue influence. In Part I, we highlighted a switching strategy that utilized a simple trend-following approach. Switching between the traditional capitalization-weighted index and its equal-weighted version can add to returns depending on the calendar. So, let's consider the effect of seasonality.

Testing a seasonal approach to switching between weighted and unweighted

The strategy below offers a potential edge to investors who have decided to devote some of their capital to an S&P 500 Index buy-and-hold approach. For testing purposes, we will use the SPDR S&P 500 ETF Trust (SPY) to track the S&P 500 Index and the Invesco S&P 500 Equal Weight ETF (RSP) to track the S&P 500 Equal Weighted Index.

There is not much to the strategy; there are only two steps:

- From November 1st through April 30th, hold RSP (SPX equal-weighted index fund)

- From May 1st through October 31st, hold SPY (SPX cap-weighted index fund)

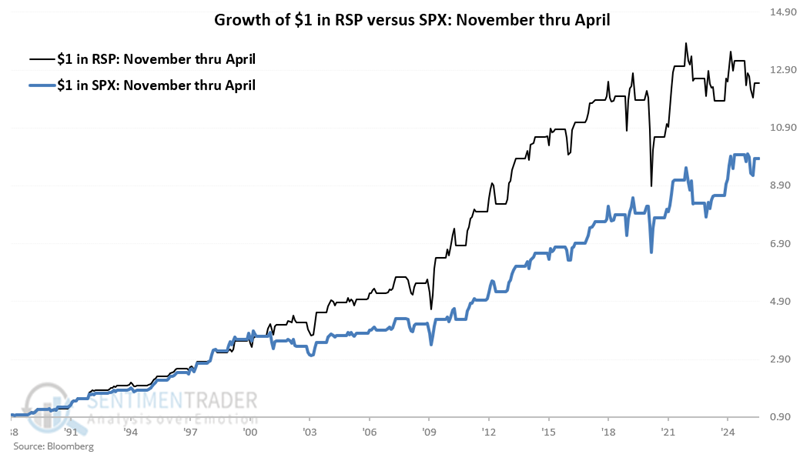

Results for November through April

The chart below displays the cumulative percentage return for RSP and SPY if both are held only from November through April from January 1988 through August 2025. The Equal-weighted index gained a cumulative 1,228% while the Cap-weighted index gained 931%.

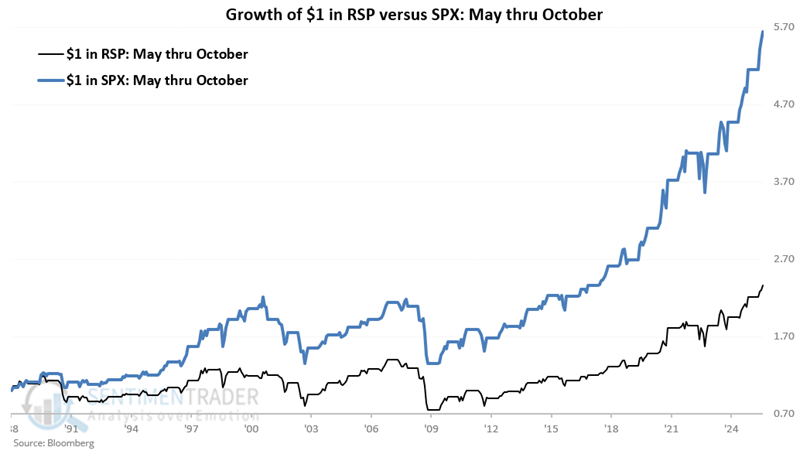

Results for May through October

The chart below displays the cumulative percentage return for equal-weighted and cap-weighted indexes if both are held only from May through October. The Equal-weighted index gained a cumulative 121%, while the Cap-weighted index gained 439%.

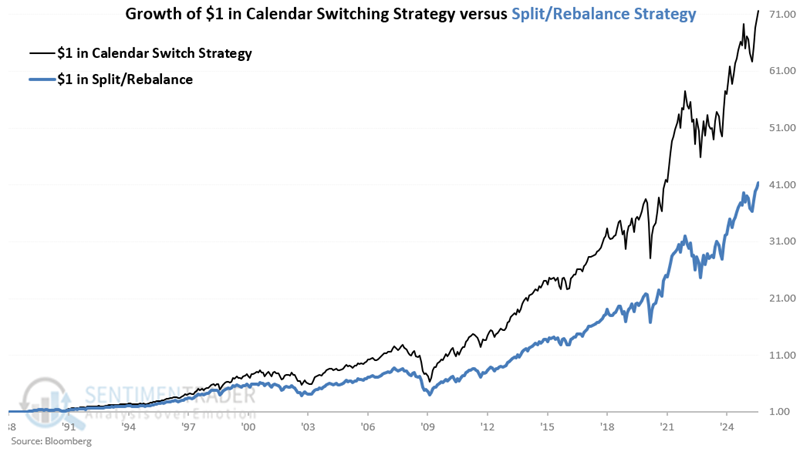

Combining the two periods into one strategy

The switching strategy involves two trades per year, switching to SPY on April 30th and switching to RSP on October 31st. Let's take a look at the complete strategy results. For comparison, we will also track a strategy that splits capital 50/50 between equal-weighted and cap-weighted indexes and rebalances to 50/50 on January 1st of each year.

The chart below shows that the Switching Strategy gained +7,059% versus +4,038% for the Split/Rebalance Strategy.

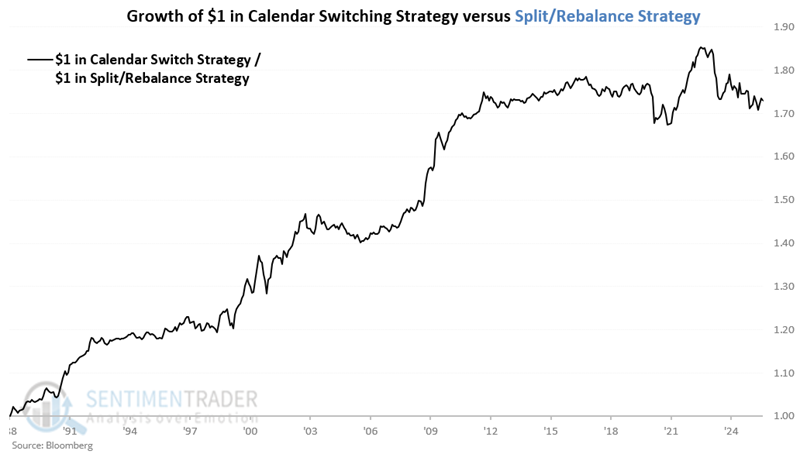

The value in the chart below divides the cumulative growth of $1 invested using the Switching Strategy by the cumulative growth of $1 invested using the Split/Rebalance Strategy. When the line rises, it means that the Switching Strategy is outperforming. While long-term results have favored this seasonal approach, recent years have seen less robust results in terms of outperforming the Split/Rebalance Strategy.

We will combine the trend-following and seasonal strategies from Parts I and II in Part III.

What the research tells us…

Since ticker RSP started trading, the unweighted S&P 500 Index has tended to outperform during November through May. While this consistency is not guaranteed to continue, the consistency of returns makes the above switching strategy a viable alternative for investors who have decided to invest in index funds.