Earnings are recovering and investors don't care

Key points:

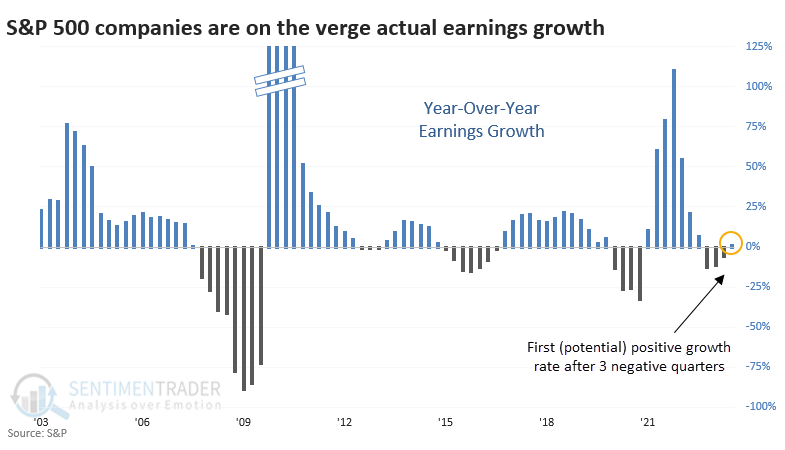

- S&P 500 companies are on track to show year-over-year earnings growth for the 1st time in 3 quarters

- Earnings recoveries mostly preceded higher prices, especially during the past 50 years

- When stocks declined in the first month after a recovery, returns nine months later were good

After three negative quarters, earnings are on track to recover

It might not seem like it, given how the average stock has performed over the past few months, but their underlying fundamentals are improving. For the first time in several quarters, earnings among S&P 500 companies are on track to show growth.

The corporate earnings downturn is poised to end, but you wouldn't know it looking at the stock market carnage.

With the third-quarter earnings season nearly halfway over, companies in the S&P 500 are on track to post a 2.7% year-over-year increase in profits, according to a FactSet blend of reported results and consensus analyst estimates. That would mark the first earnings growth in four quarters.

According to S&P Global Data, as-reported 12-month earnings per share for S&P 500 companies are estimated to total $189.20 for the quarter ending September 30. That's a little more than 1% higher than Q3 2022 - not much, but hey, it's something. And it would mark the first actual earnings growth after three consecutive declines.

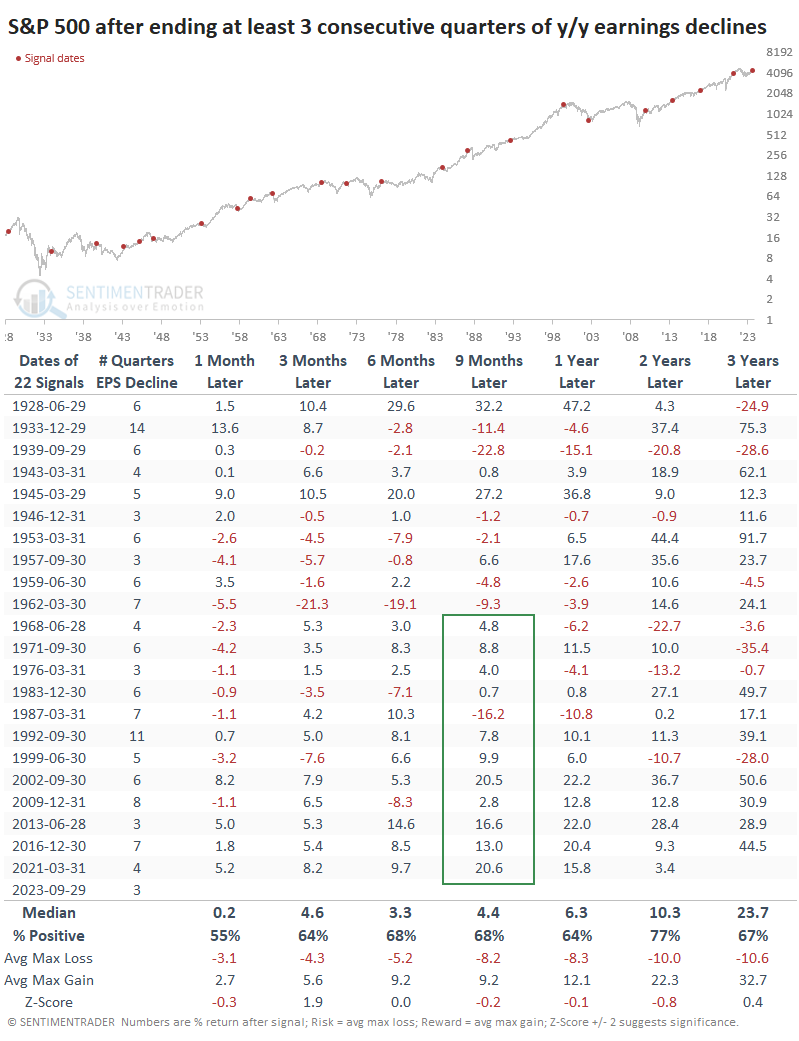

Earnings recoveries preceded mostly rising prices

There is a dubious relationship between stock prices and fundamentals, or the economy. The table below shows that while investors might reasonably expect an earnings recovery to precede a rising stock market, it did not consistently do so. Investors anticipate rather than react (mostly).

That's not to say forward S&P returns were poor; they were just...fine. Cycles over the past 50 years have led to excellent returns, except for that little interruption called Black Monday in October 1987.

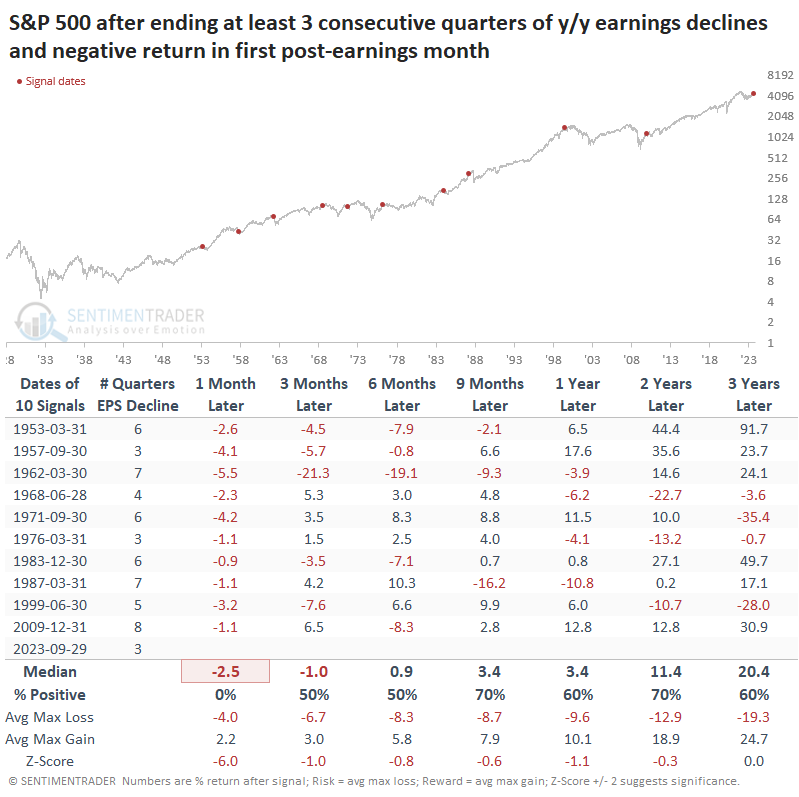

One interesting wrinkle is that since the quarter ended, the S&P has continued to decline, and we're almost guaranteed to have an adverse reaction in the first month after quarter-end. There were ten other times when earnings returned to growth, but stocks declined in the first month after that quarter ended. That dampened returns across most time frames going forward.

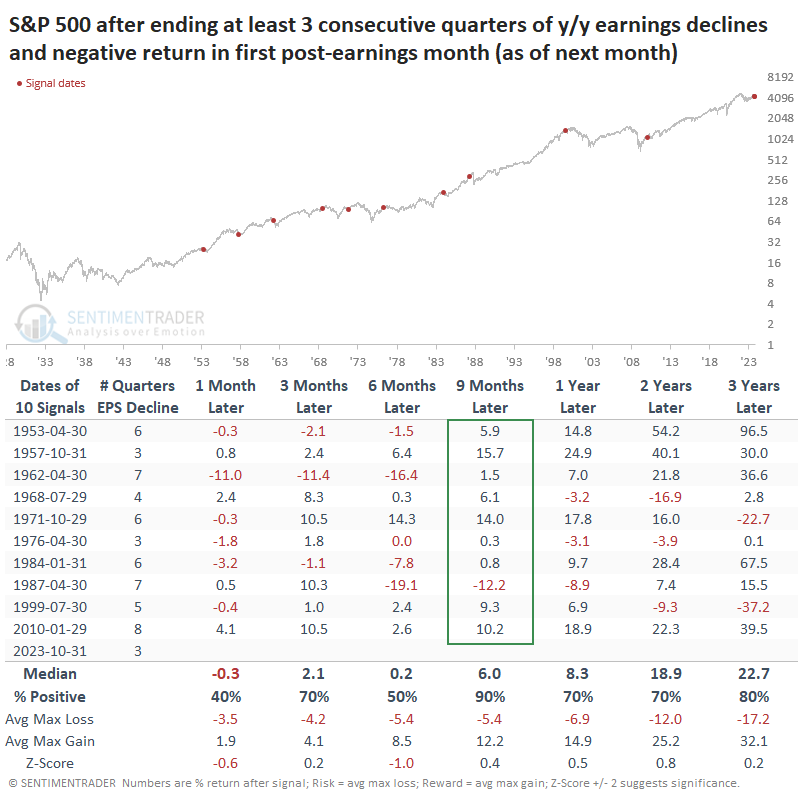

The returns in the table above, however, are influenced negatively by that first month, through which we have already suffered. The table below corrects that and represents what investors would experience going forward in real-time. That helped quite a bit for expectations during the next 9-12 months. Nine months later, there was only one negative return (that pesky '87 crash).

What the research tells us...

According to Standard & Poors, there is a high likelihood that stocks in the S&P 500 will show an aggregate increase in earnings from the same quarter a year ago, ending a several-quarter streak of declines. A return to growth has always translated into rising stock prices since sometimes investors had already anticipated that earnings would recover and bid up prices ahead of time.

When there has been a negative reaction in the month after earnings recover, as has happened this time, future returns were above average, especially during the next nine months. This appears to be a modest positive for the current recovery.