Divergences among indices have been brewing for weeks

Key points:

- When the S&P 500 made its last 52-week high, it was disguising significant deterioration

- Many stocks and indices, covering a broad cross-section of the market, were failing to keep up

- Similar divergences since 1928 have preceded mostly weak returns over medium time frames

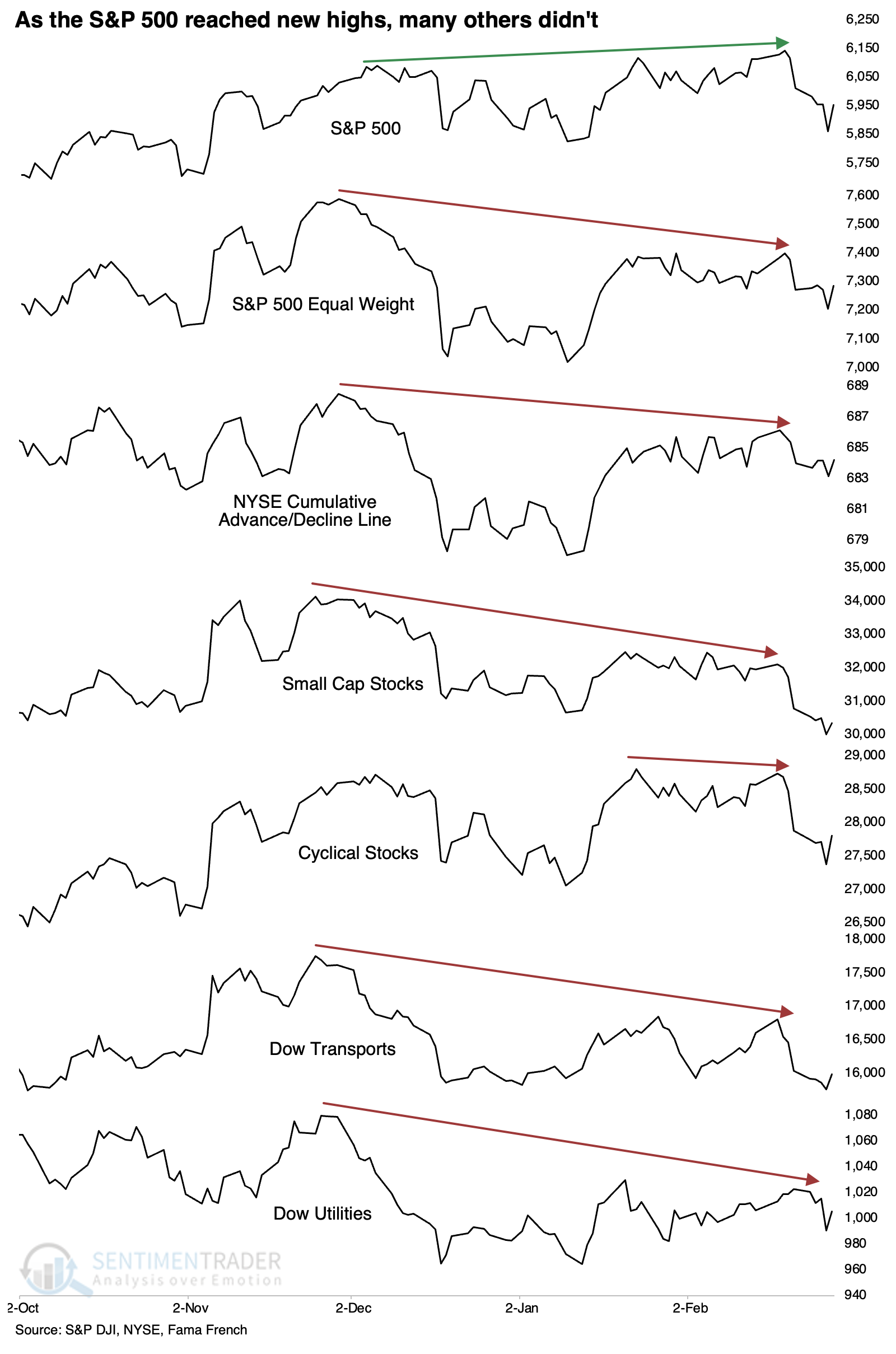

The S&P 500 has been hiding a lot

We've noted multiple times in recent weeks (and even months) that under the surface of the market - mostly meaning the S&P 500 - there have been some issues with participation among stocks or entire sectors.

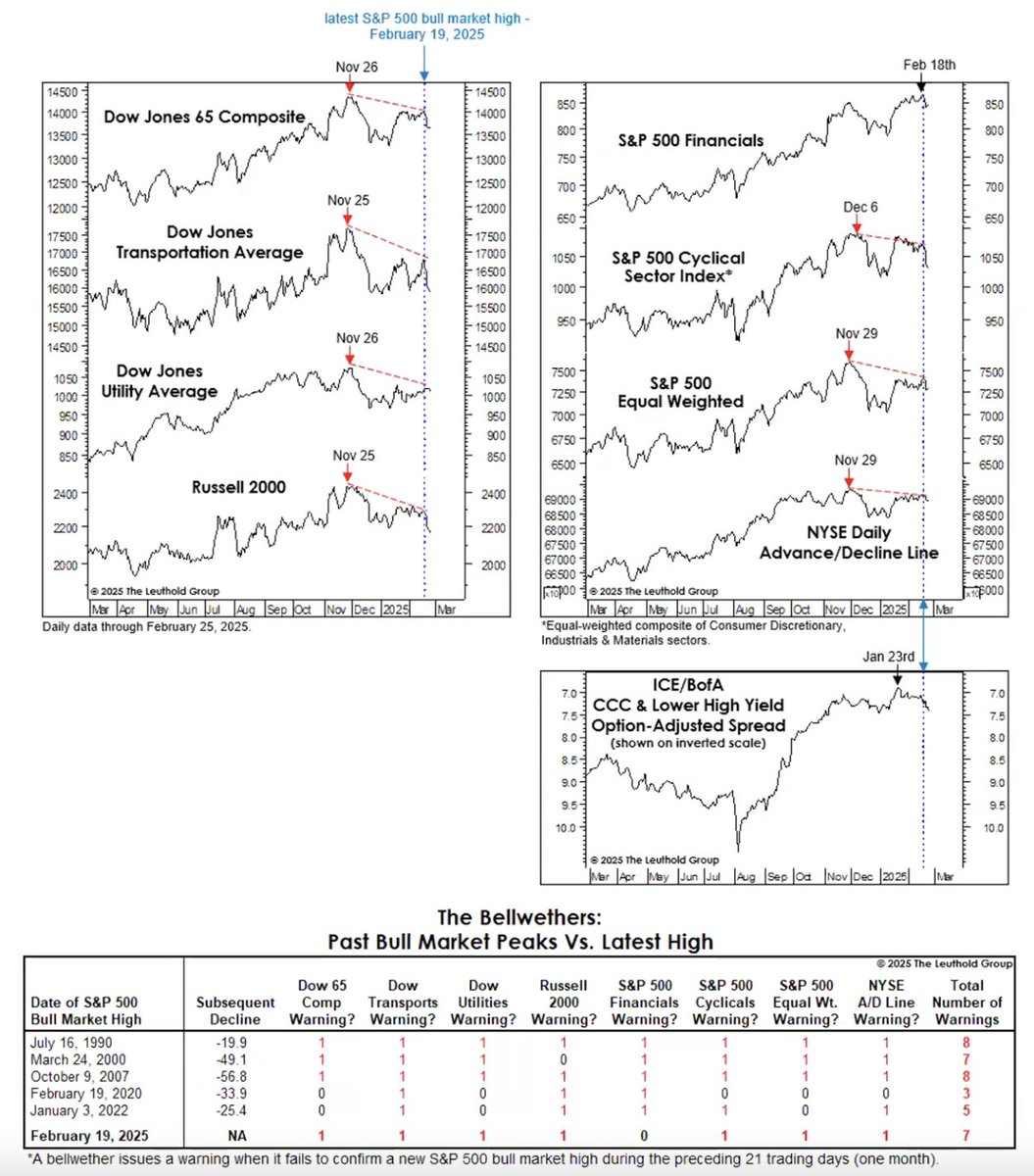

The fine folks at Leuthold Group noted something related when the S&P 500 made its last push to new highs in February.

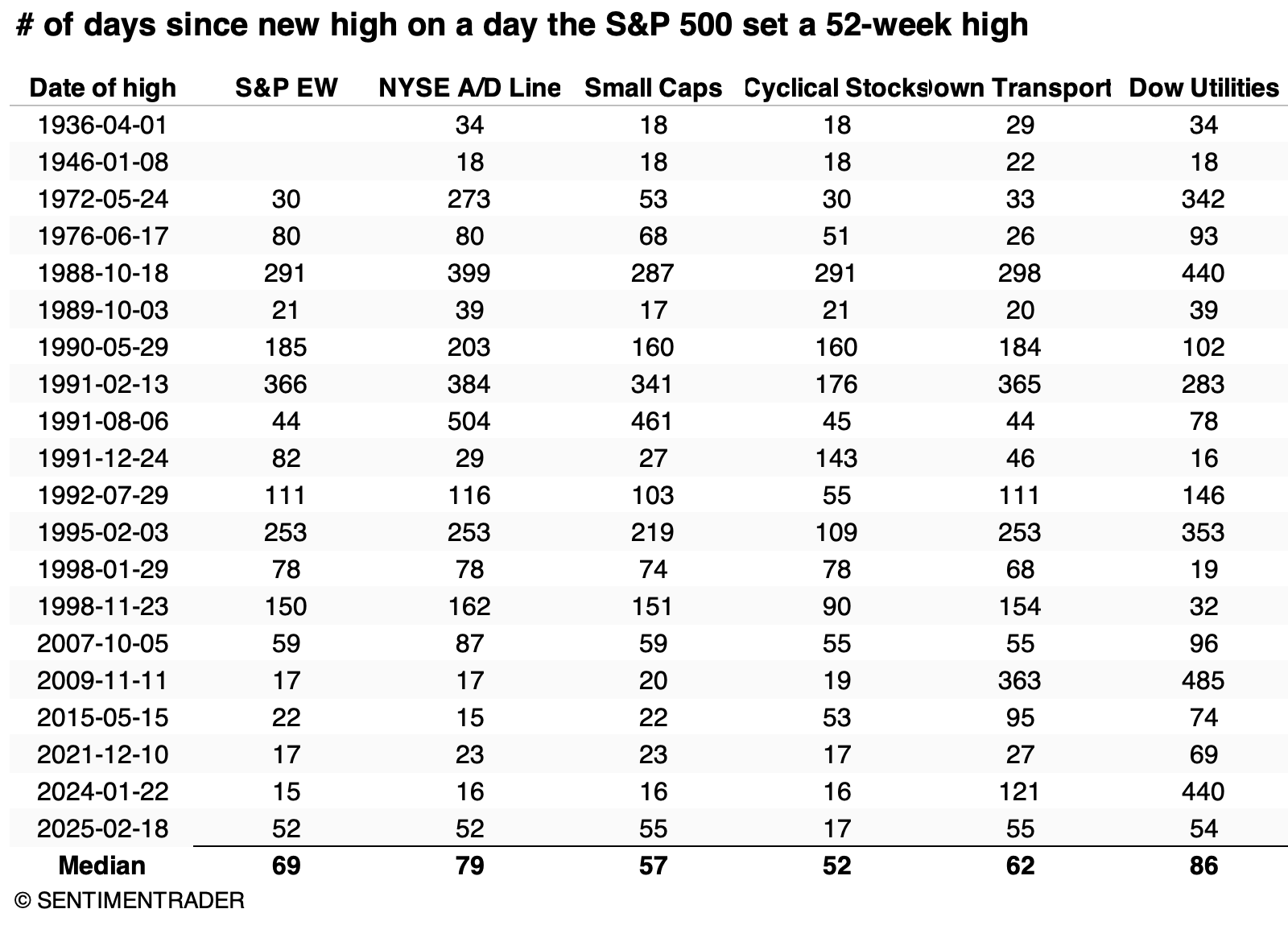

We've been asked how reliable a signal this has been. We don't have the same or as extensive a data set as Leuthold. However, we can approximate some of the indices with the most history and look for times there were extended divergences from them on any day the S&P 500 made a 52-week high.

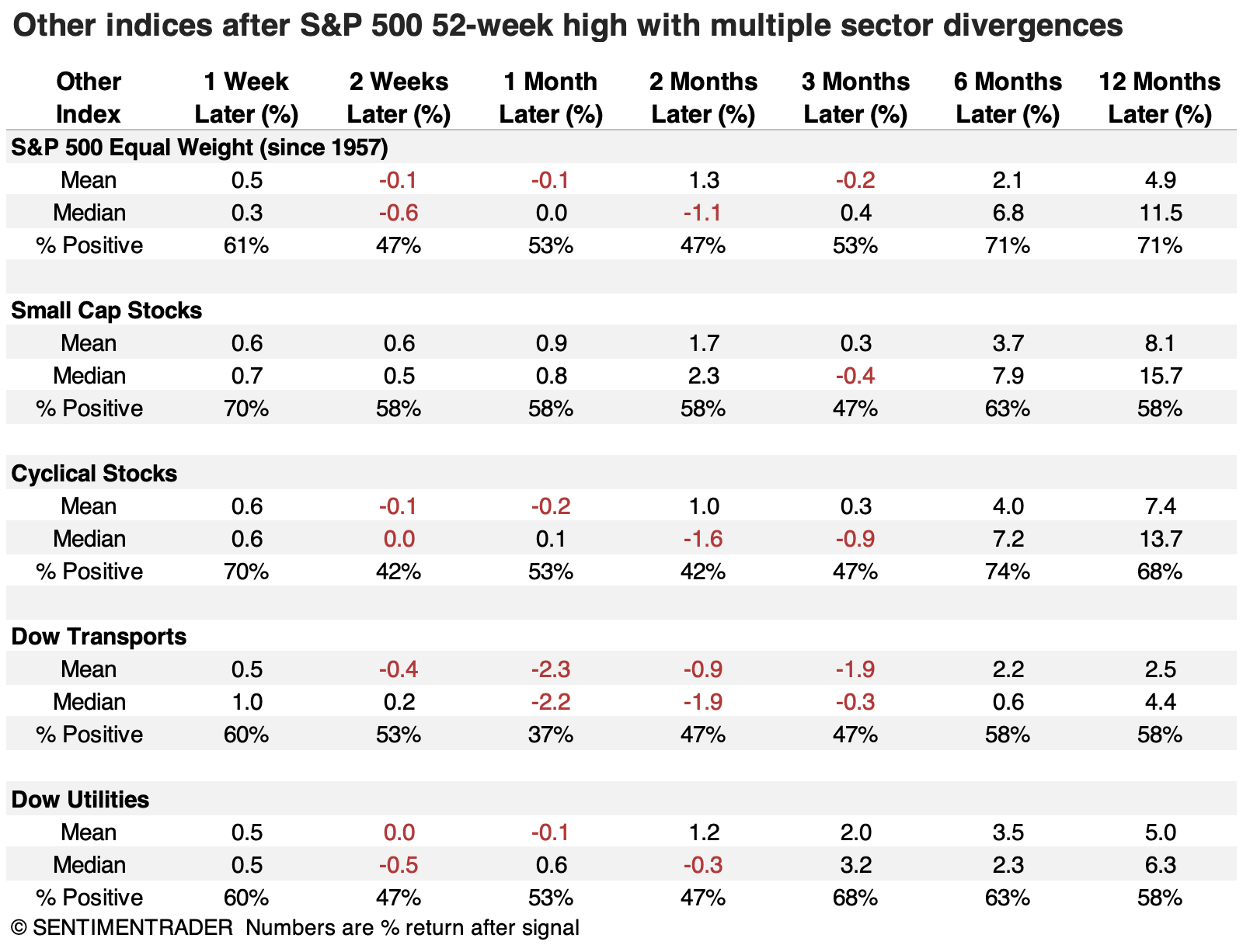

The indices we will use below clearly show their deterioration even as the S&P pushed higher into late February.

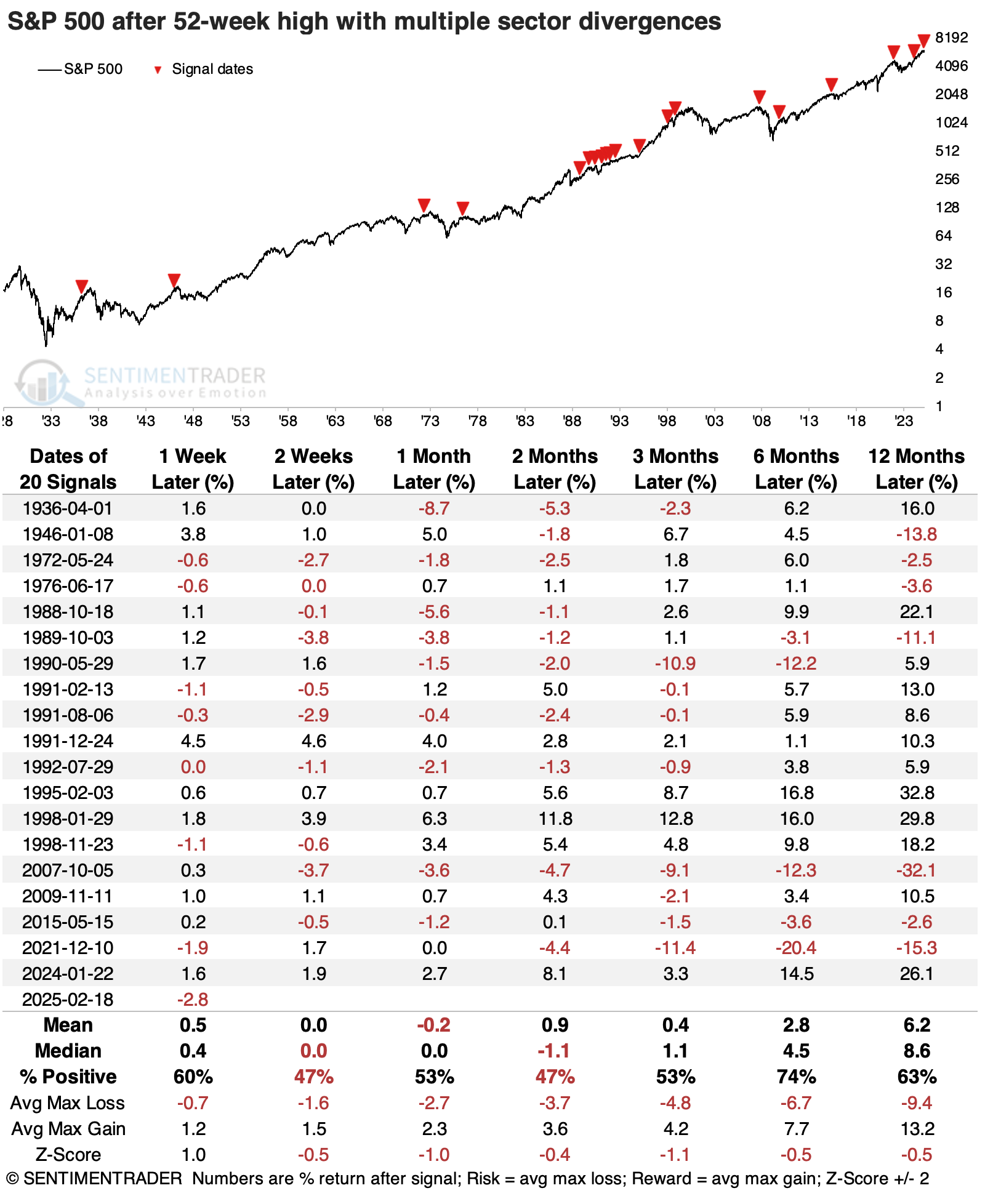

The table below shows all dates when the S&P was at a 52-week high, but each of the indices above hadn't set a 52-week high for at least the prior three weeks.

This was a rare and bad omen before the 1990s, with each signal preceding little upside in the S&P 500 in the months ahead. It was triggered multiple times in the early 1990s, again mostly preceding weak returns for months afterward. The late 1990s signals preceded the last gasp of the internet bubble. Since then, returns have been weak again, with the only real exception being one from about a year ago. It should be noted that that exception from 2024 met the criteria of this test, but the current divergence is significantly more extended than that one was.

The peak in 2020 did exhibit divergences in all of the indices we used. However, those divergences hadn't been as extended (lasting at least three weeks) as the one last month. The peak in 2000 came close, but cyclical stocks were an exception, briefly making a new high along with the S&P 500, so that instance didn't count in our study, either.

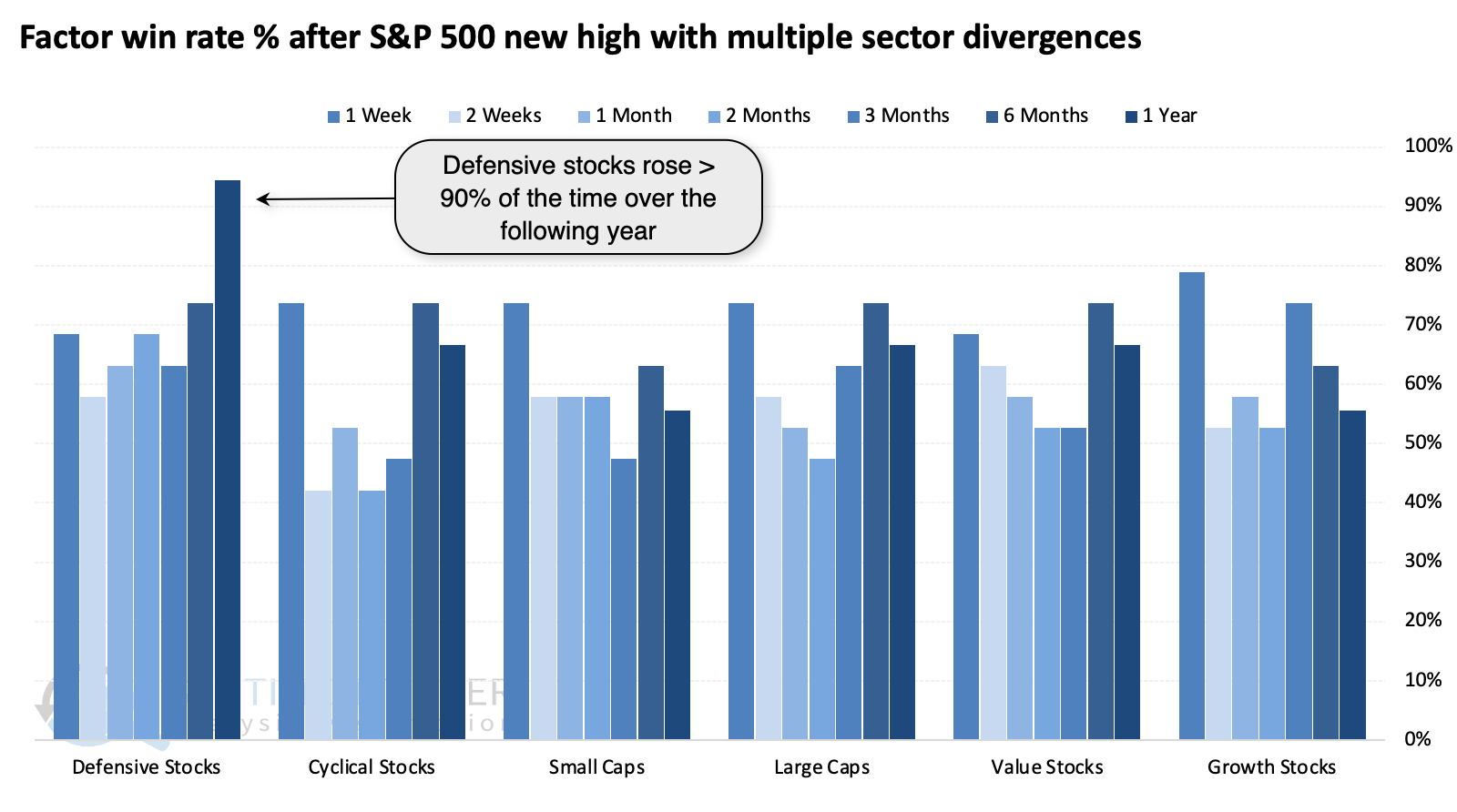

Another nod toward defensive stocks

Among the other indices, the Dow Transports suffered the worst returns in the months ahead, with cyclical stocks also struggling. None of them sported very good returns, really.

Looking at win rates across factors, defensive stocks were the most consistent winners, rising more than 90% of the time over the following year. Growth stocks were the least consistent, with barely a 55% win rate a year later.

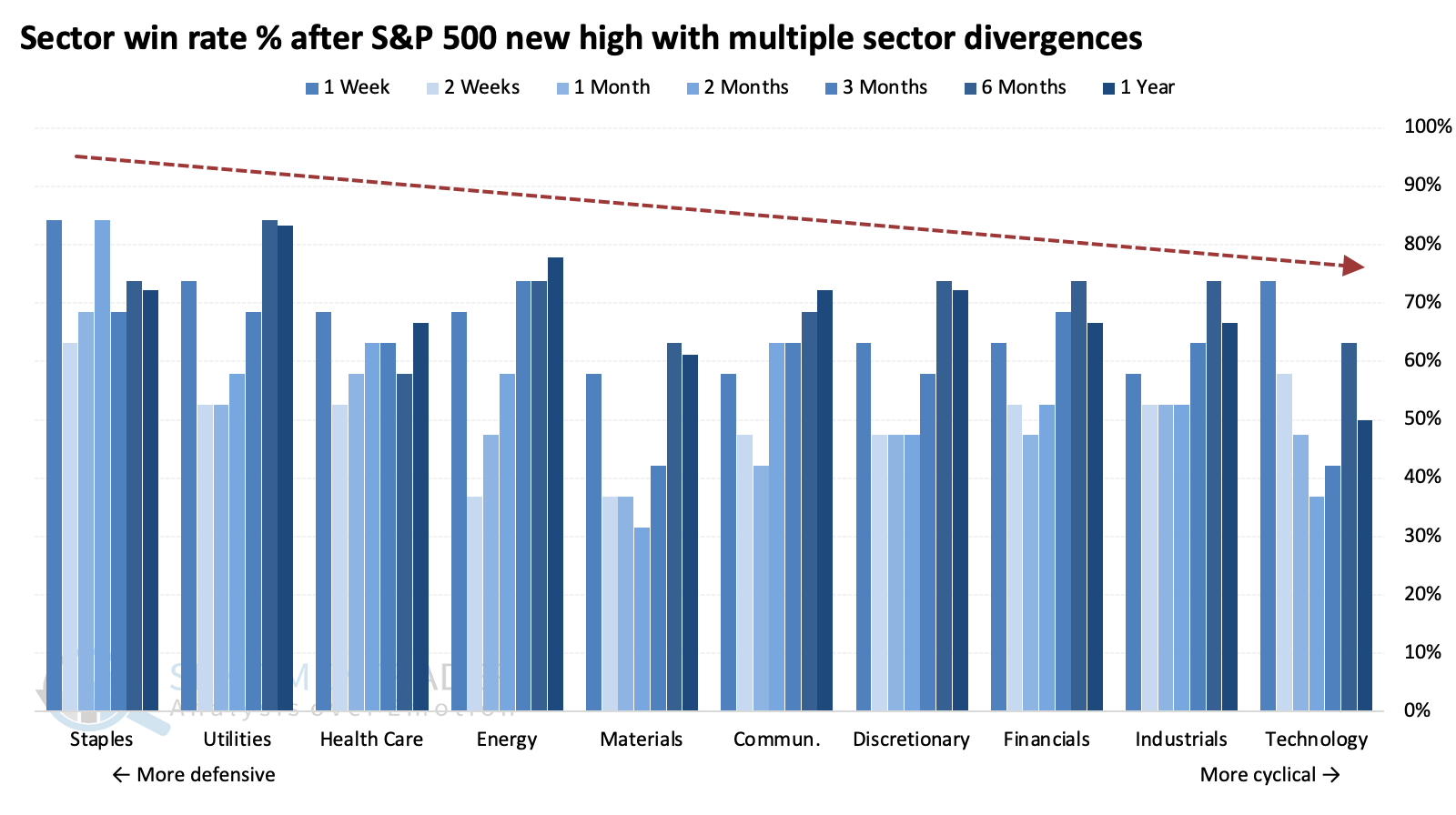

We can see this among sectors, as well. The most defensive sectors enjoyed the highest win rates; the most cyclical, the lowest.

What the research tells us...

Stocks have already pulled back a modest degree since the S&P 500's last high a couple of weeks ago. However, the divergences taking place at the time across a wide swath of the market are a sign of perhaps deeper issues than just a small hiccup in the uptrend.

There isn't enough evidence in the prior divergences noted above to suggest it's a raging sell signal for stocks. It is enough to suggest caution, especially over short to medium time frames, no longer than six months or so. This is another development that has shown an investor had better odds with defensive stocks as opposed to cyclical or growth.