Headlines

|

|

Options traders bet against sectors while insiders relax:

Options traders have been trading a record number of puts relative to calls in Technology and Financial stocks and even the broader S&P 500. At the same time, corporate insiders at those companies have been selling little stock. In the case of the S&P 500, insider selling was recently at a 12-year low.

|

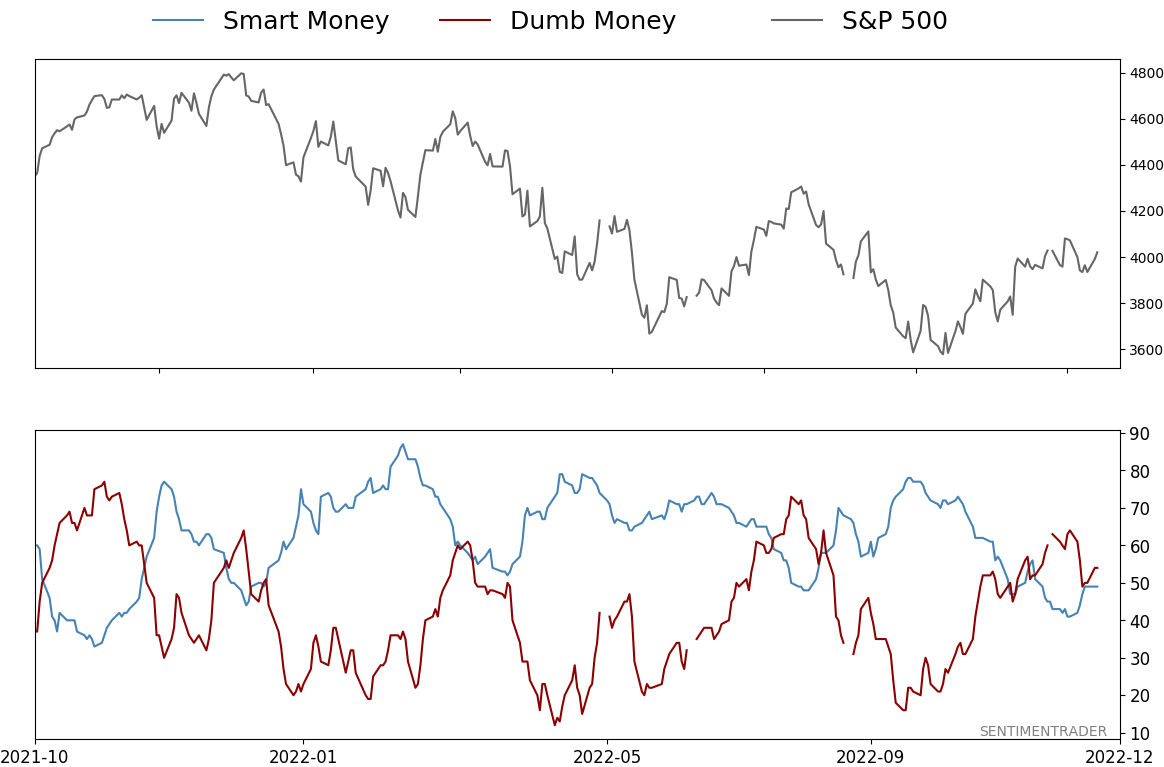

Smart / Dumb Money Confidence

|

Smart Money Confidence: 49%

Dumb Money Confidence: 54%

|

|

Risk Levels

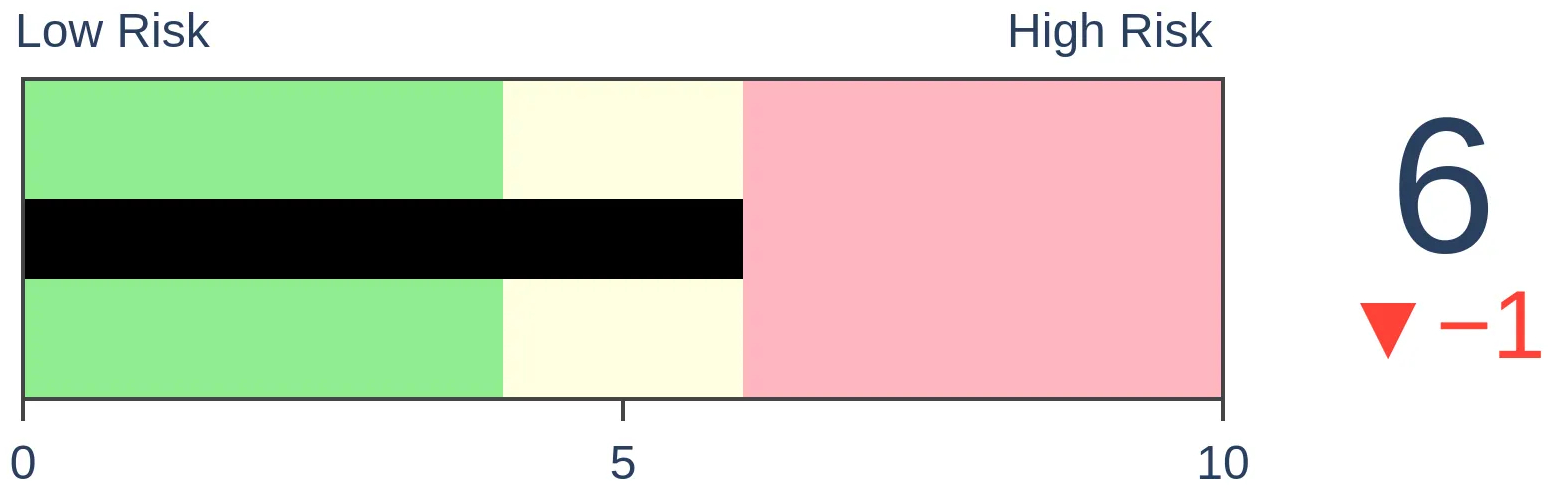

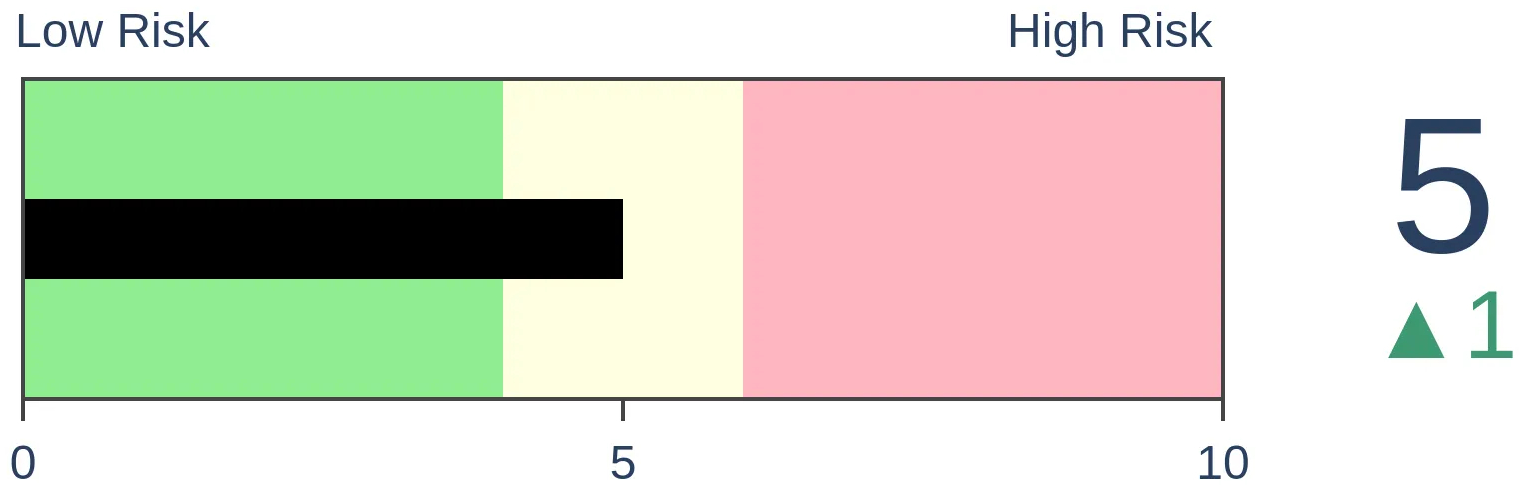

Stocks Short-Term

|

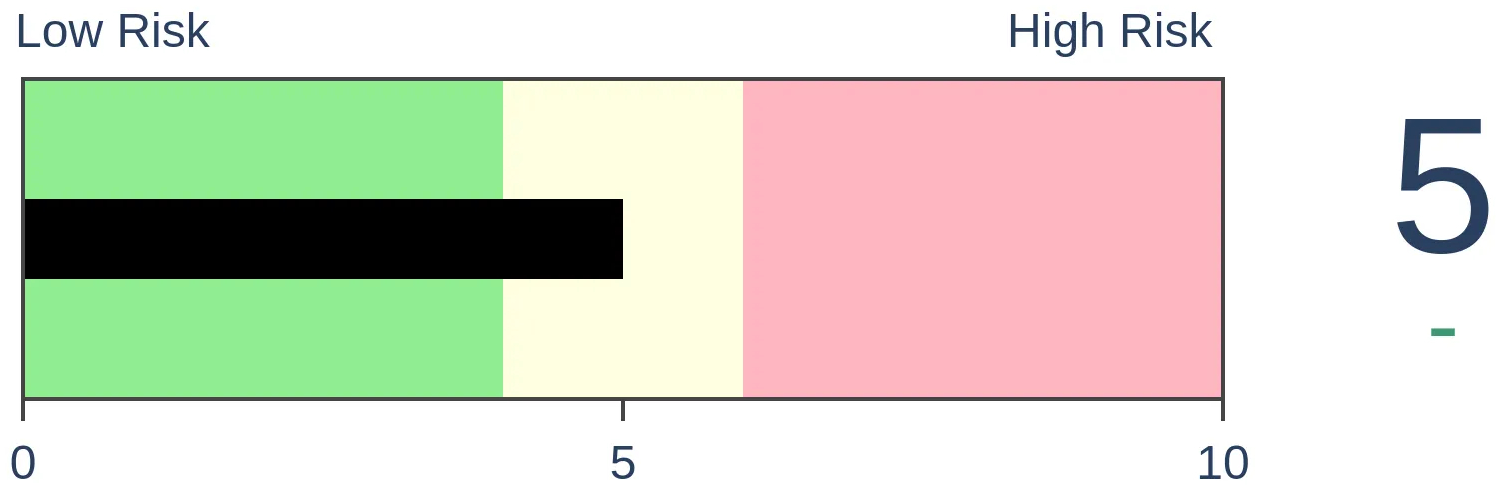

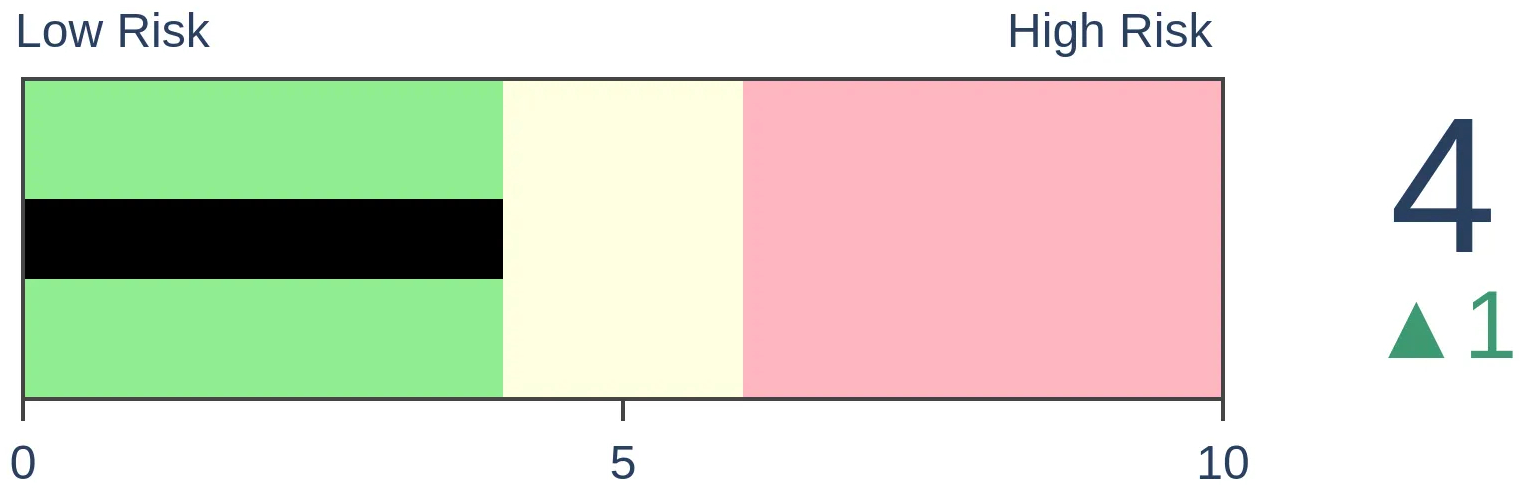

Stocks Medium-Term

|

|

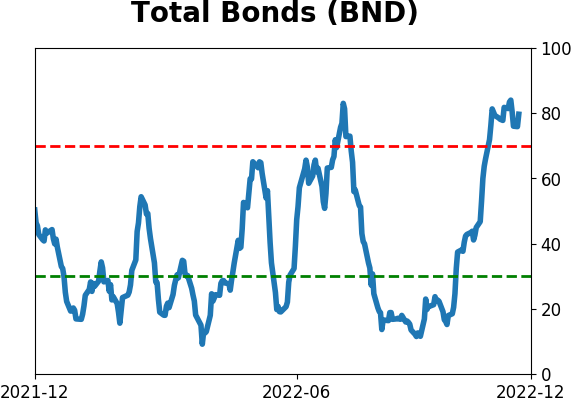

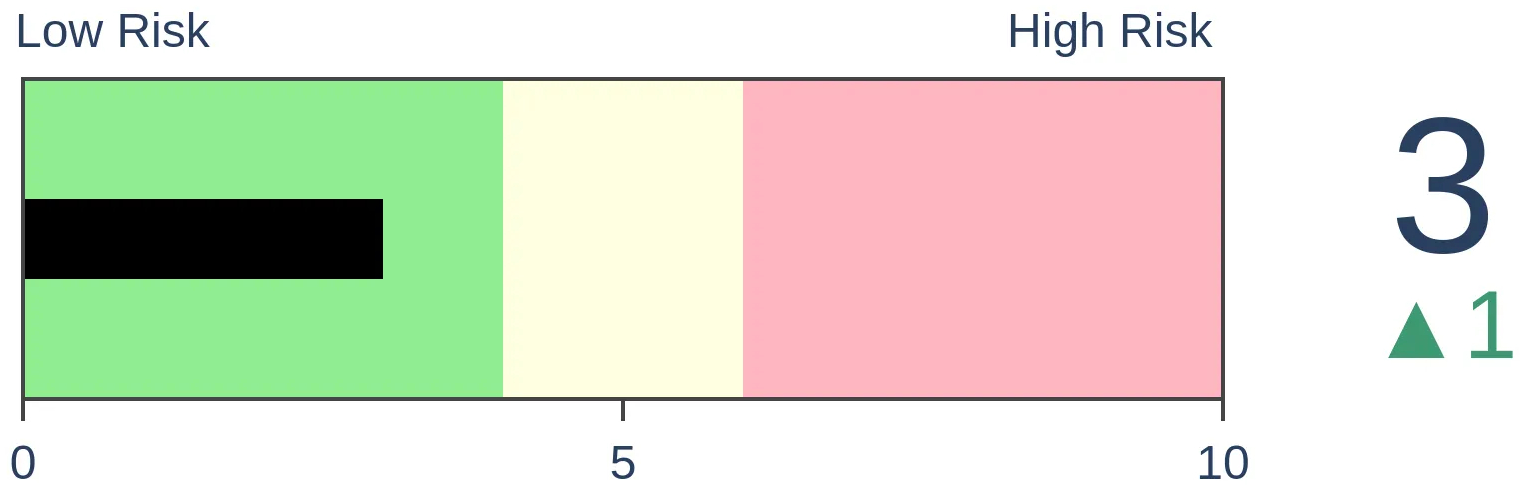

Bonds

|

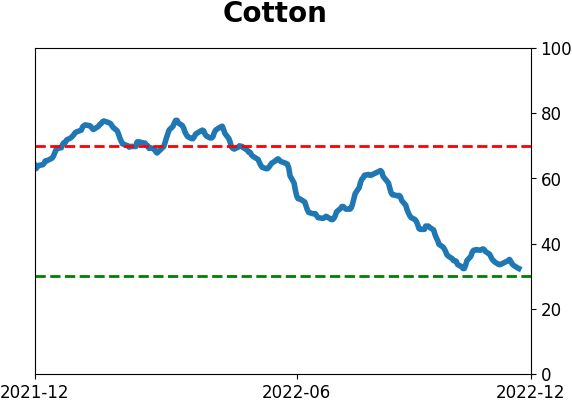

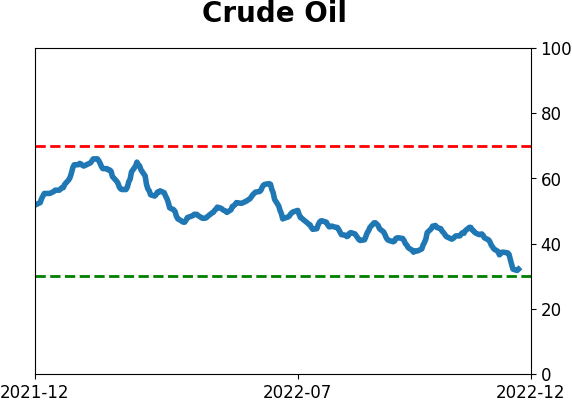

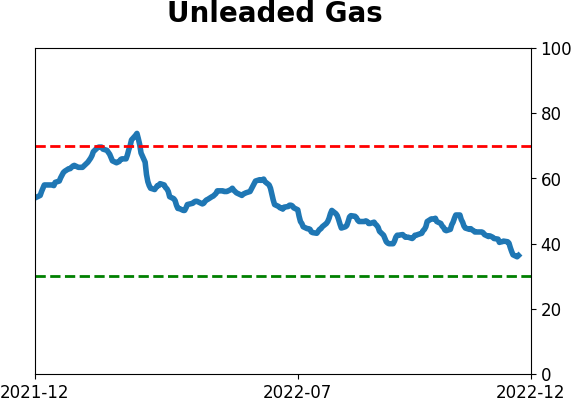

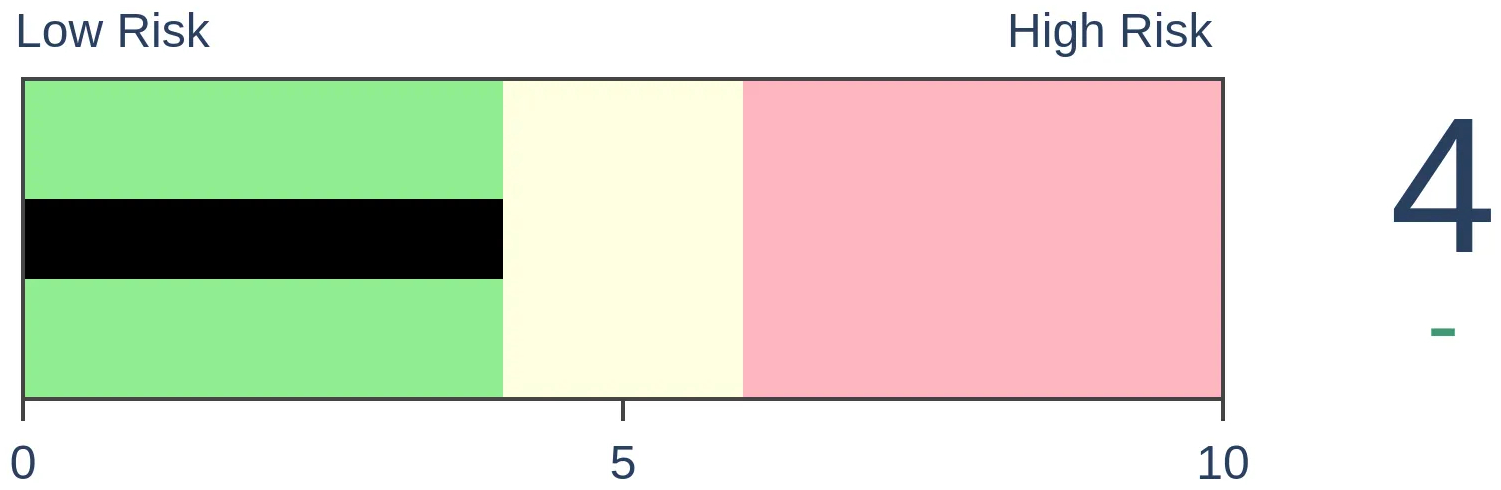

Crude Oil

|

|

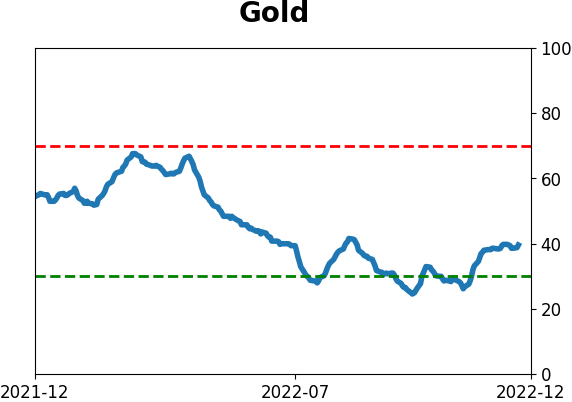

Gold

|

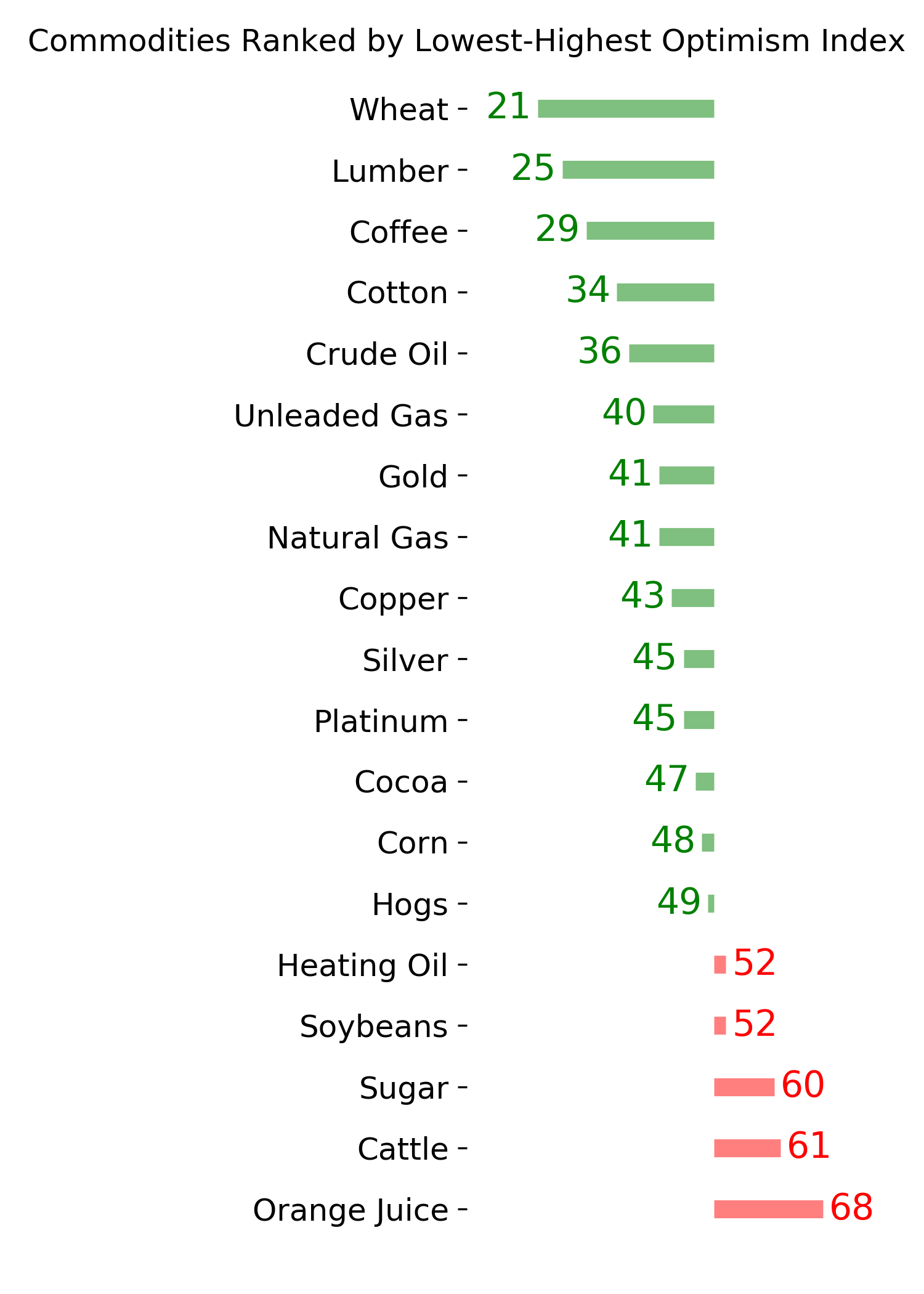

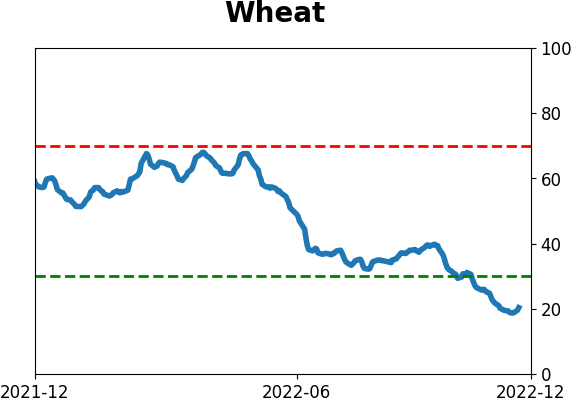

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

Options traders have been trading a record number of puts relative to calls in Technology and Financial stocks and even the broader S&P 500. At the same time, corporate insiders at those companies have been selling little stock. In the case of the S&P 500, insider selling was recently at a 12-year low.

FORECAST / TIMEFRAME

None

|

Key points:

- Options traders have turned over record numbers of puts relative to calls in Technology and Financial stocks

- At the same time, smart money corporate insiders have sold multi-year low amounts of stocks in those companies

- The same holds for the broader S&P 500, which should support stock prices

Options traders bet against stocks, while insiders don't

On Monday, we saw that large options traders have been busy paying up for put protection against stocks and ETFs. Their pessimism seems broad-based, but insiders at those companies apparently don't share their concerns.

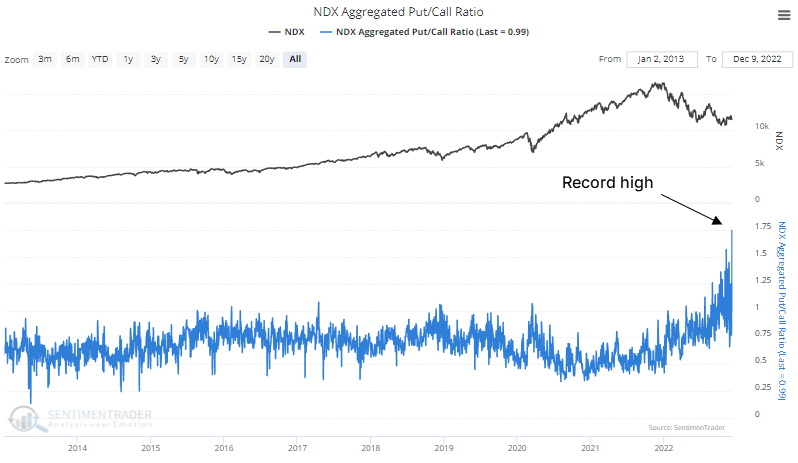

Among the Technology sector companies included in the Nasdaq 100 index, there has been a marked increase in put option volume relative to call options. Last week, the NDX Aggregated Put/Call Ratio reached a record going back almost a decade.

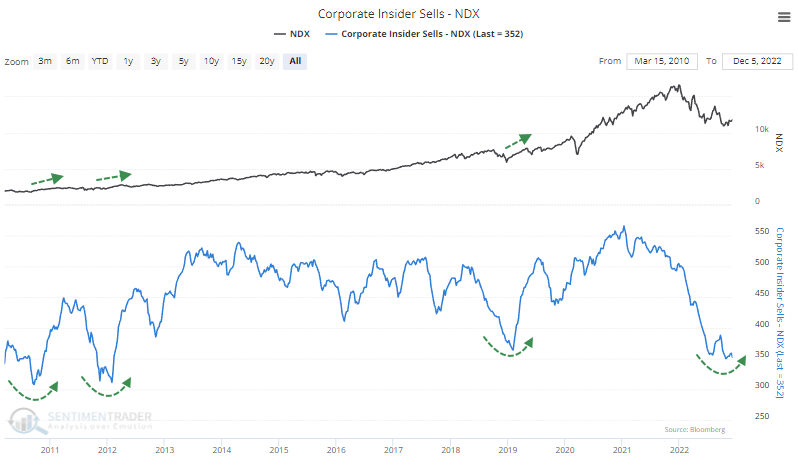

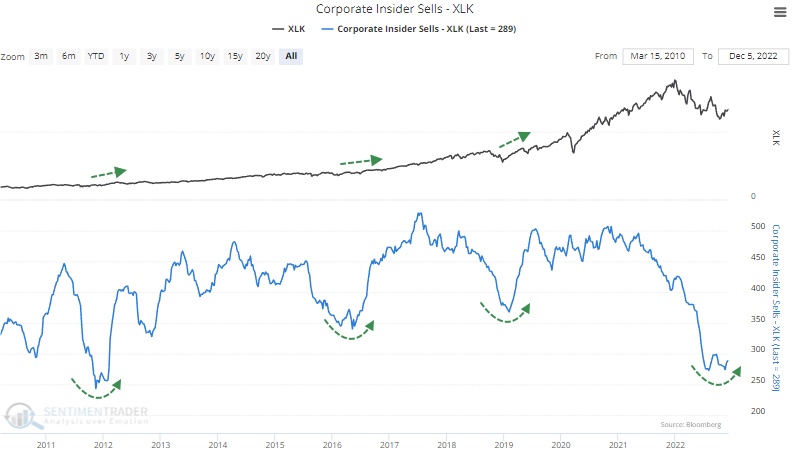

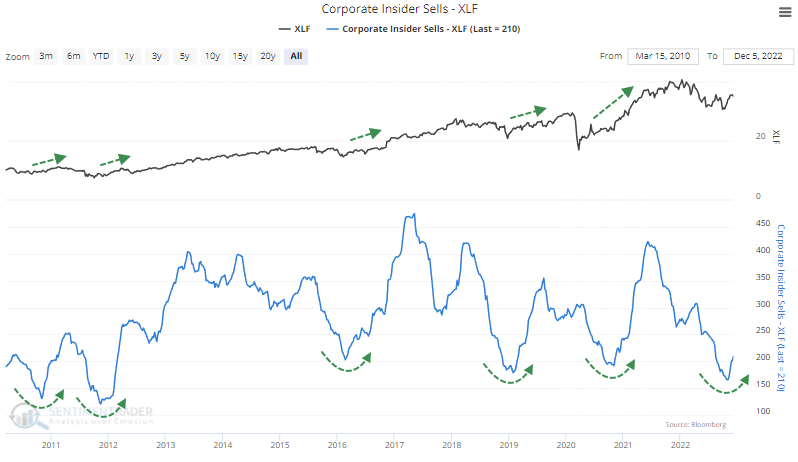

At the same time, corporate insiders working for these companies have pulled back on selling.

That's also the case for the broader technology sector, where the Aggregated Put/Call Ratio hit a record last week.

The selling pressure among corporate insiders in these companies has been even less enthusiastic for the big tech companies in the NDX.

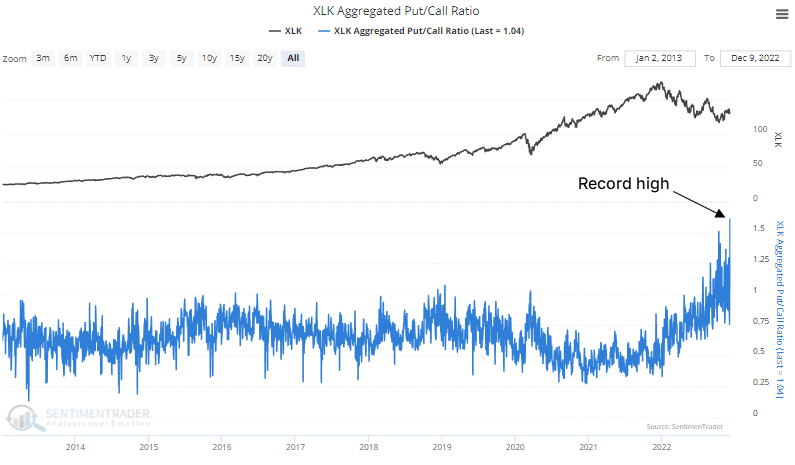

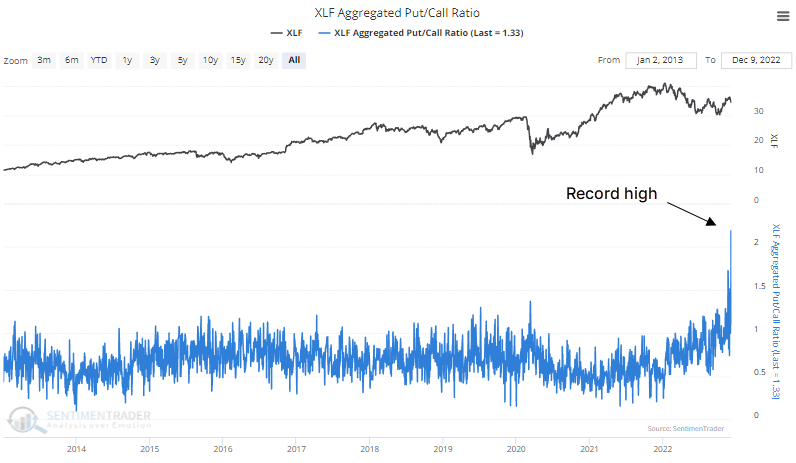

Outside of tech, the sector with the largest spread between what options traders seem to be betting on versus corporate insiders is Financials. That sector Aggregated Put/Call Ratio hit a level last week nearly twice any other extreme.

While corporate insider selling has picked up a bit recently, it's still historically low.

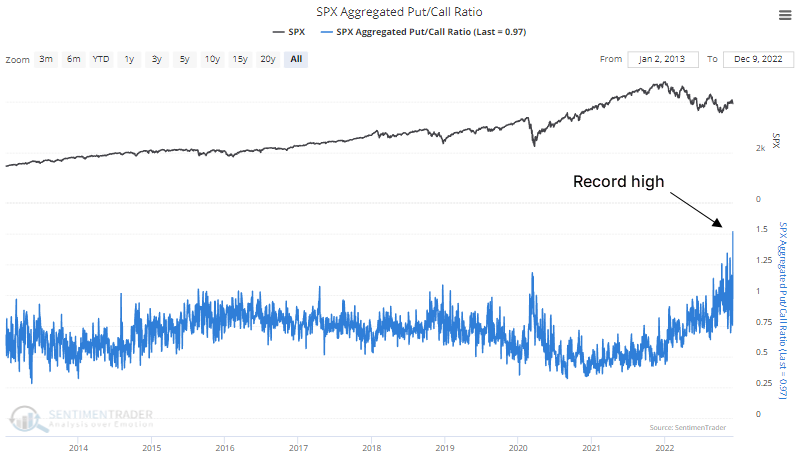

If we roll all the sectors together and look at the total S&P 500 Aggregated Put/Call Ratio, it should be no surprise that it also skyrocketed to a record high last week.

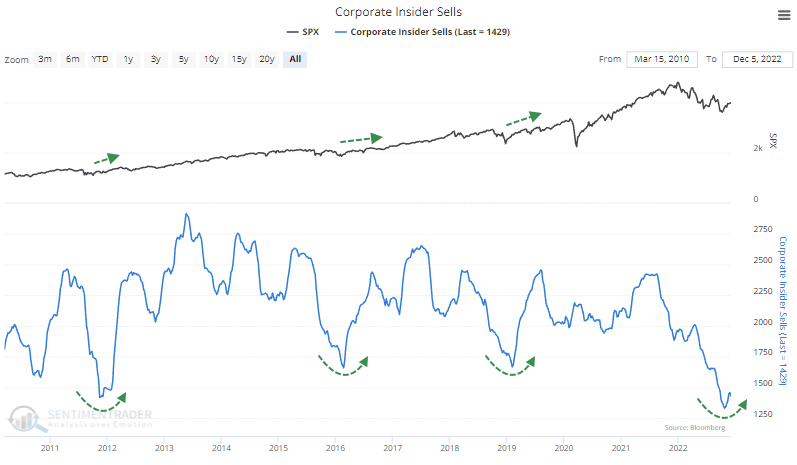

Among all companies in the index, corporate insider selling has just increased from a record low (at least over the past 12 years).

There are all sorts of explanations for the jump in put/call ratios. Most common excuses:

- A large institution is trading a reverse conversion strategy on a handful of major stocks

- Hedge funds are using an interest rate arbitrage strategy via puts

- A massive spike in same-day-expiration options is making everything irrelevant

- It doesn't mean anything because the VIX hasn't jumped, and SKEW is low

- Overall volumes are low, especially for calls

- Open interest is declining, so pessimism isn't actually increasing

Look, there are always reasons to ignore extremes in indicators. We've done it in the past and usually regretted it. Sometimes, markets change, and indicators lose effectiveness. Maybe that's the case here; I don't know. But it takes many successive failures in an indicator to cast doubt on their future effectiveness, and we don't have nearly enough evidence for that here.

What the research tells us...

If the jumps in put/call ratios last week were a one-day affair, there would be understandable reasons to be skeptical of it. But readings have been elevated for a while, and they are broad-based. While options traders are consistently contrary indicators at extremes, smart money corporate insiders are precisely the opposite. And it's notable that while options traders are betting against stocks, insiders are demonstrably not. This should be a bullish factor for the sectors and broader S&P 500 in the months ahead.

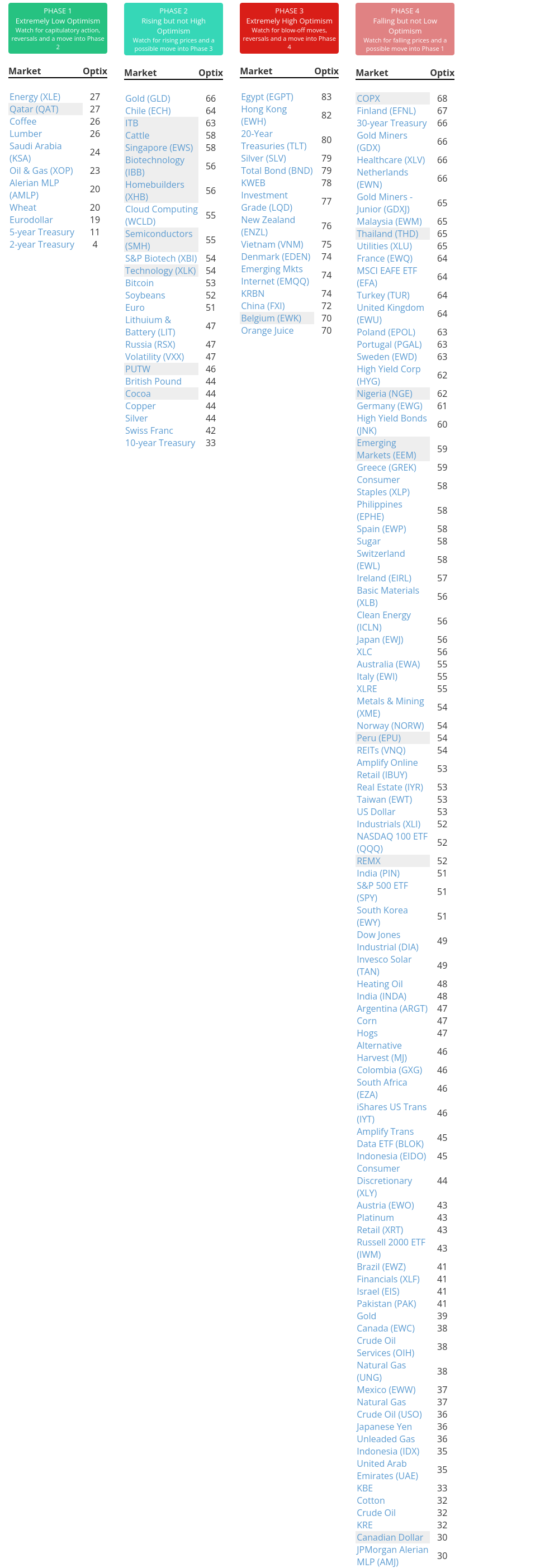

Indicators at Extremes

Phase Table

Ranks

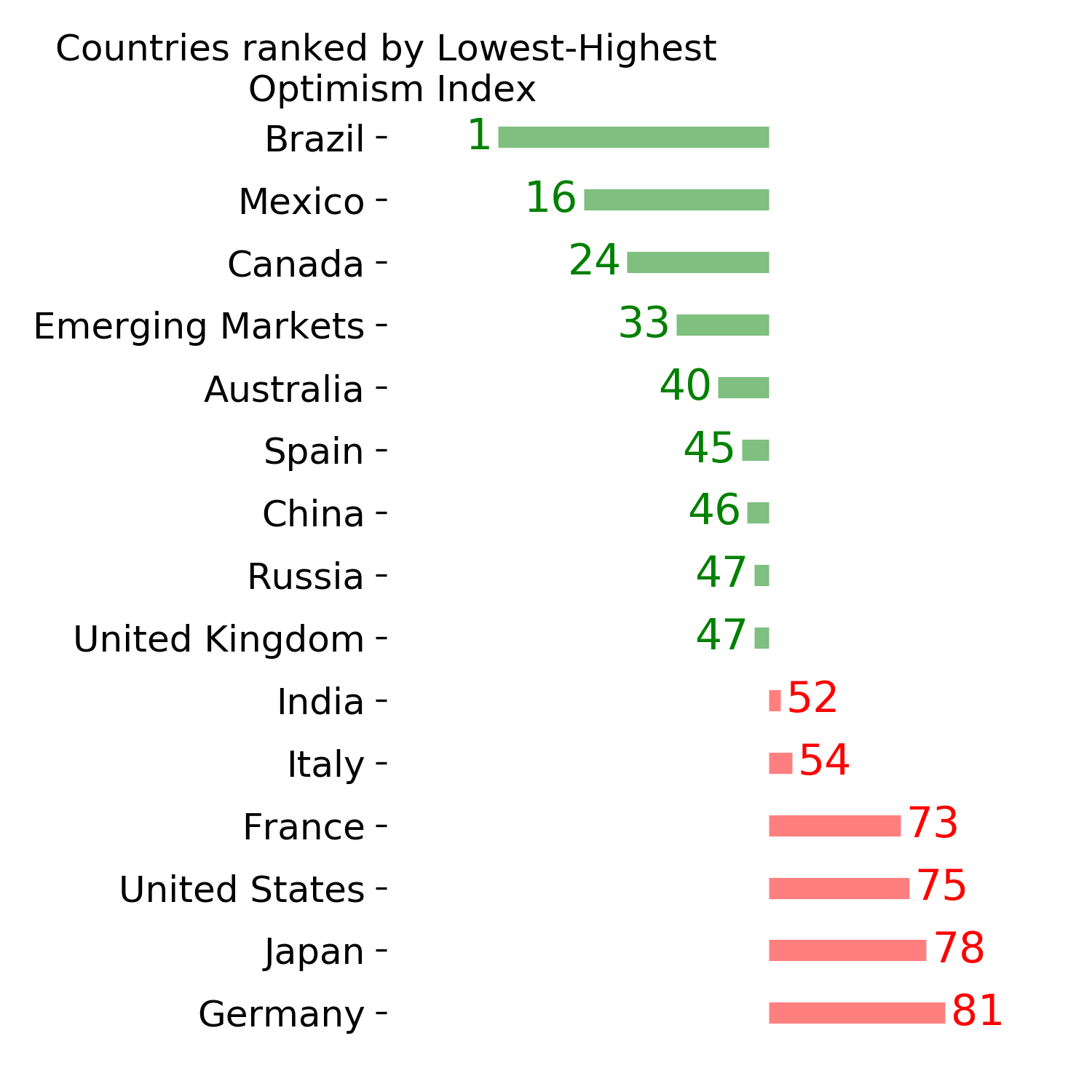

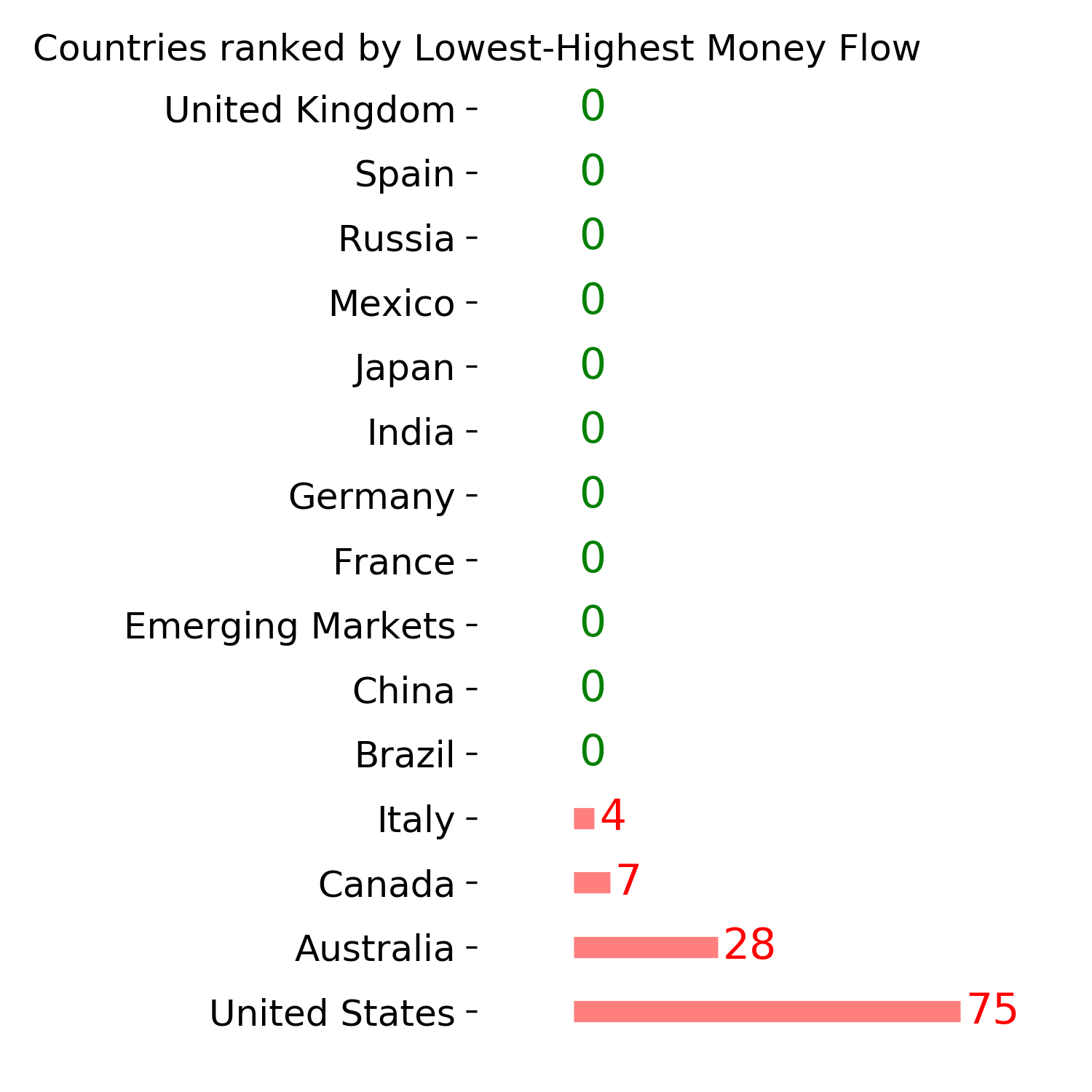

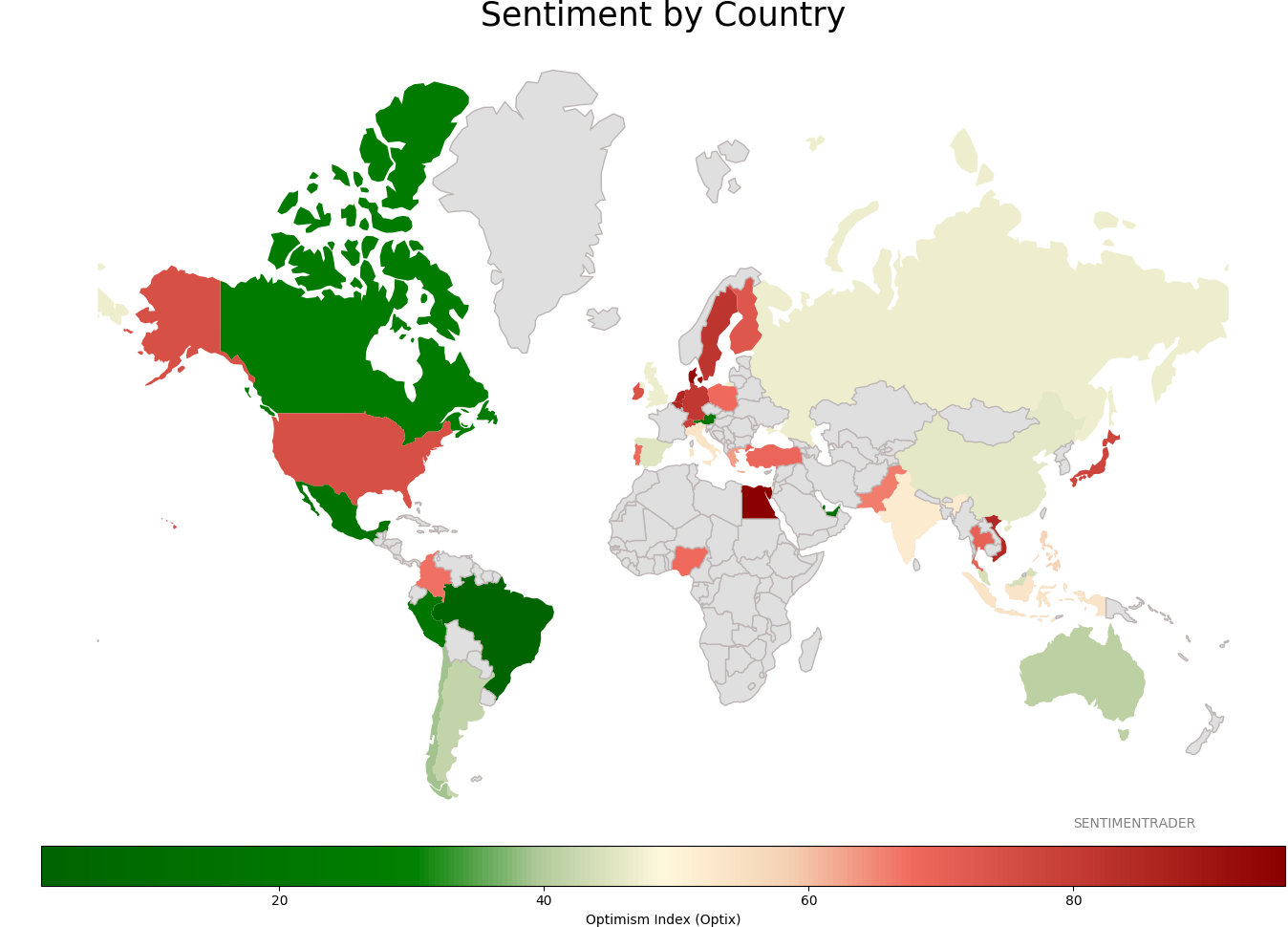

Sentiment Around The World

Optimism Index Thumbnails

|

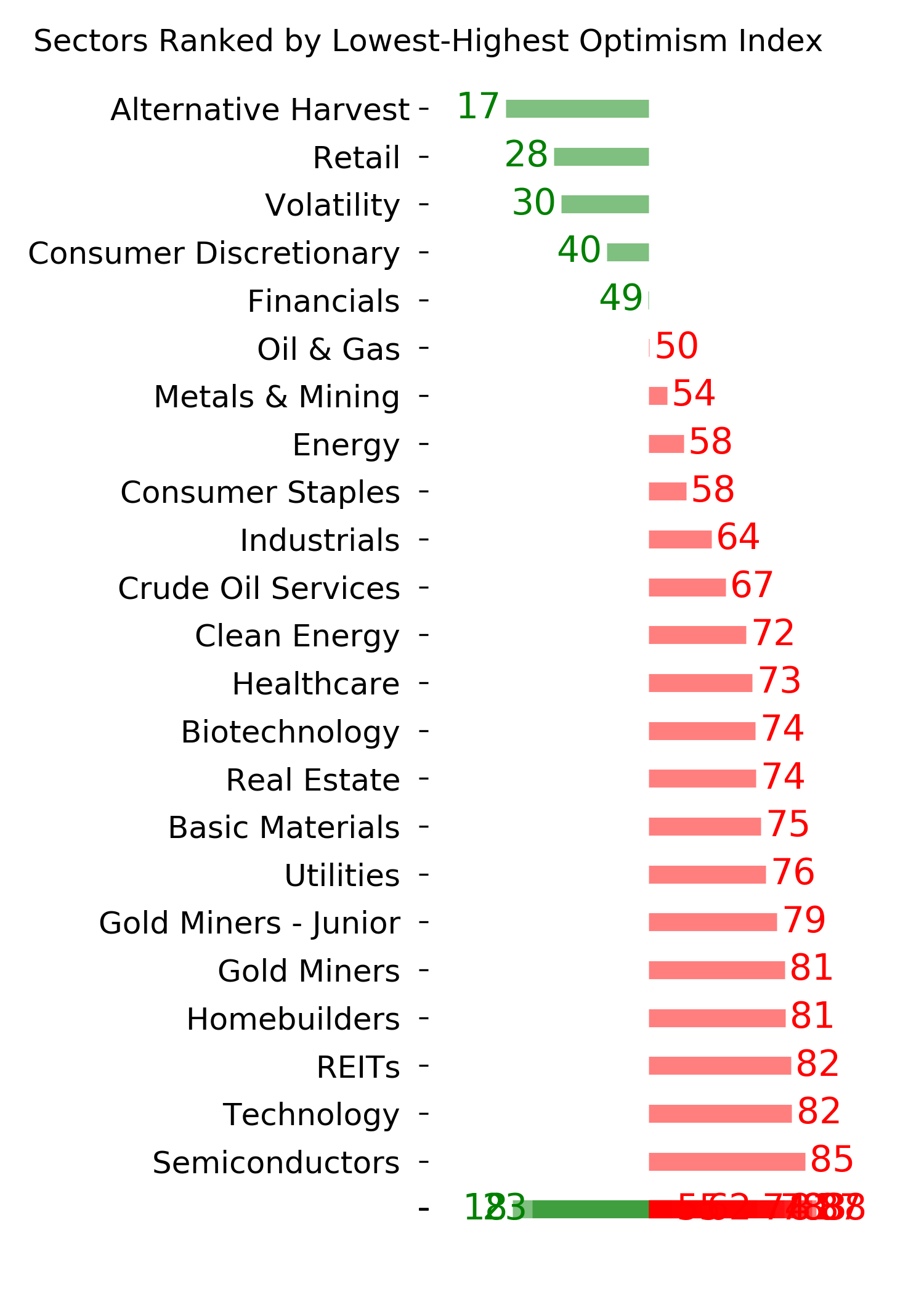

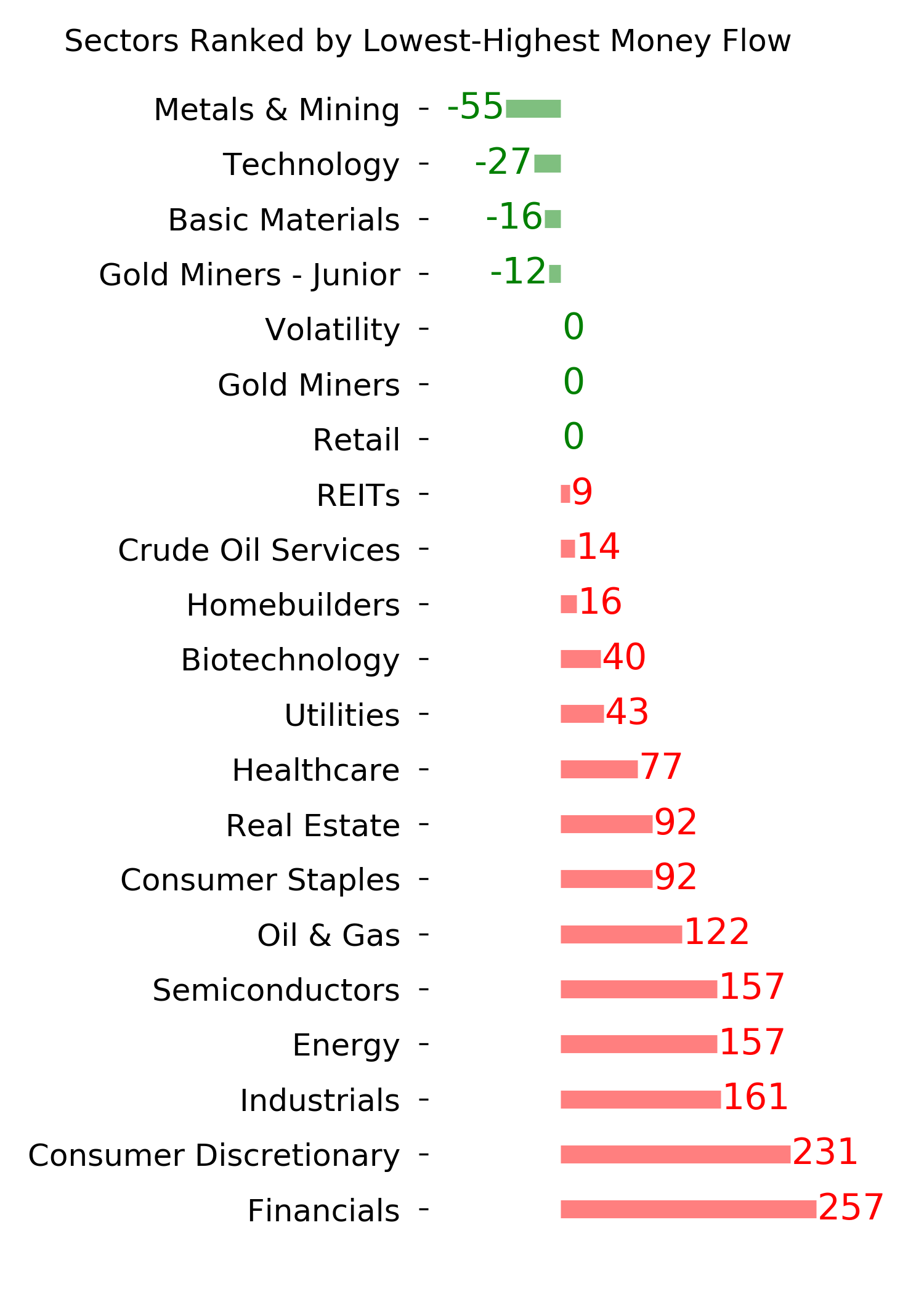

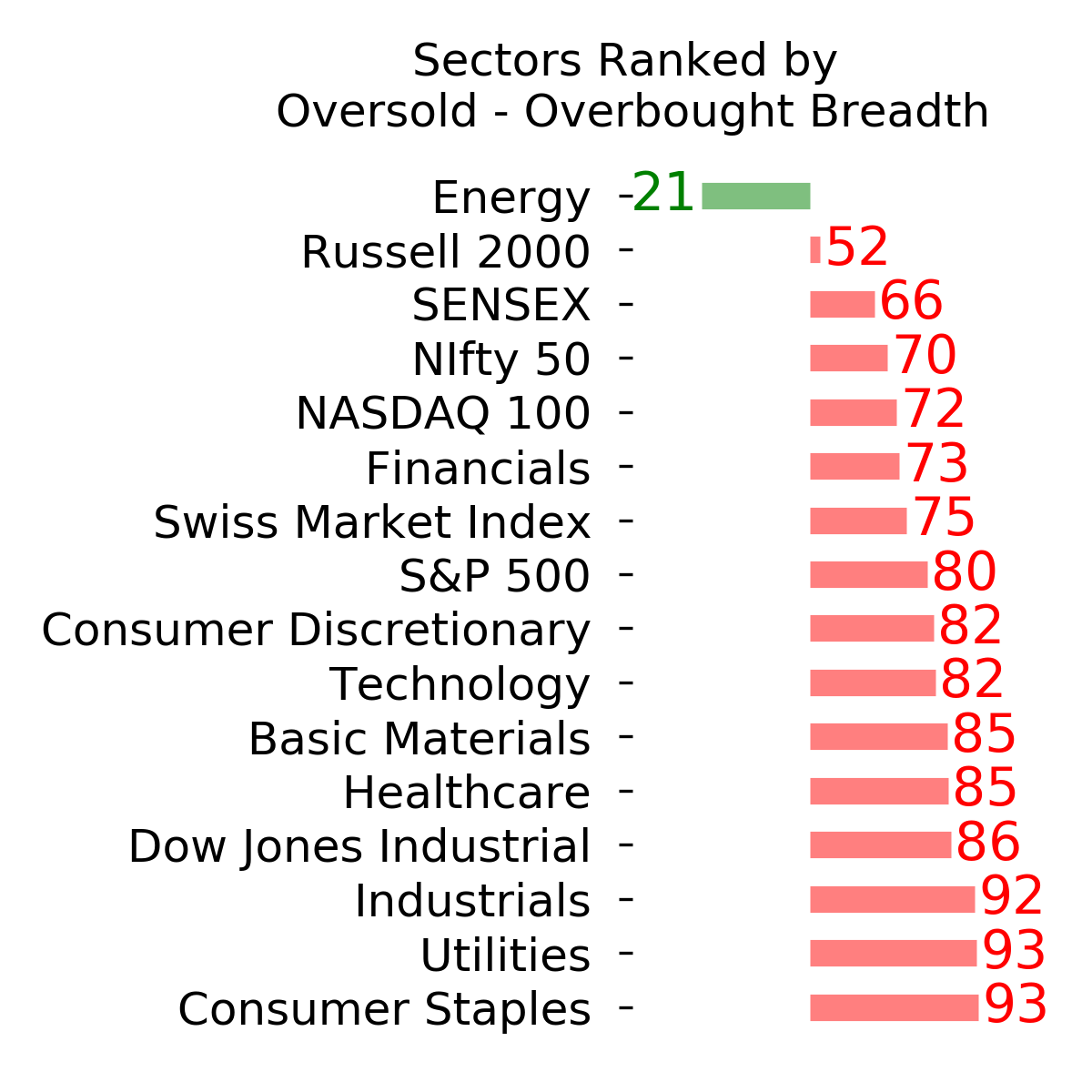

Sector ETF's - 10-Day Moving Average

|

|

|

Country ETF's - 10-Day Moving Average

|

|

|

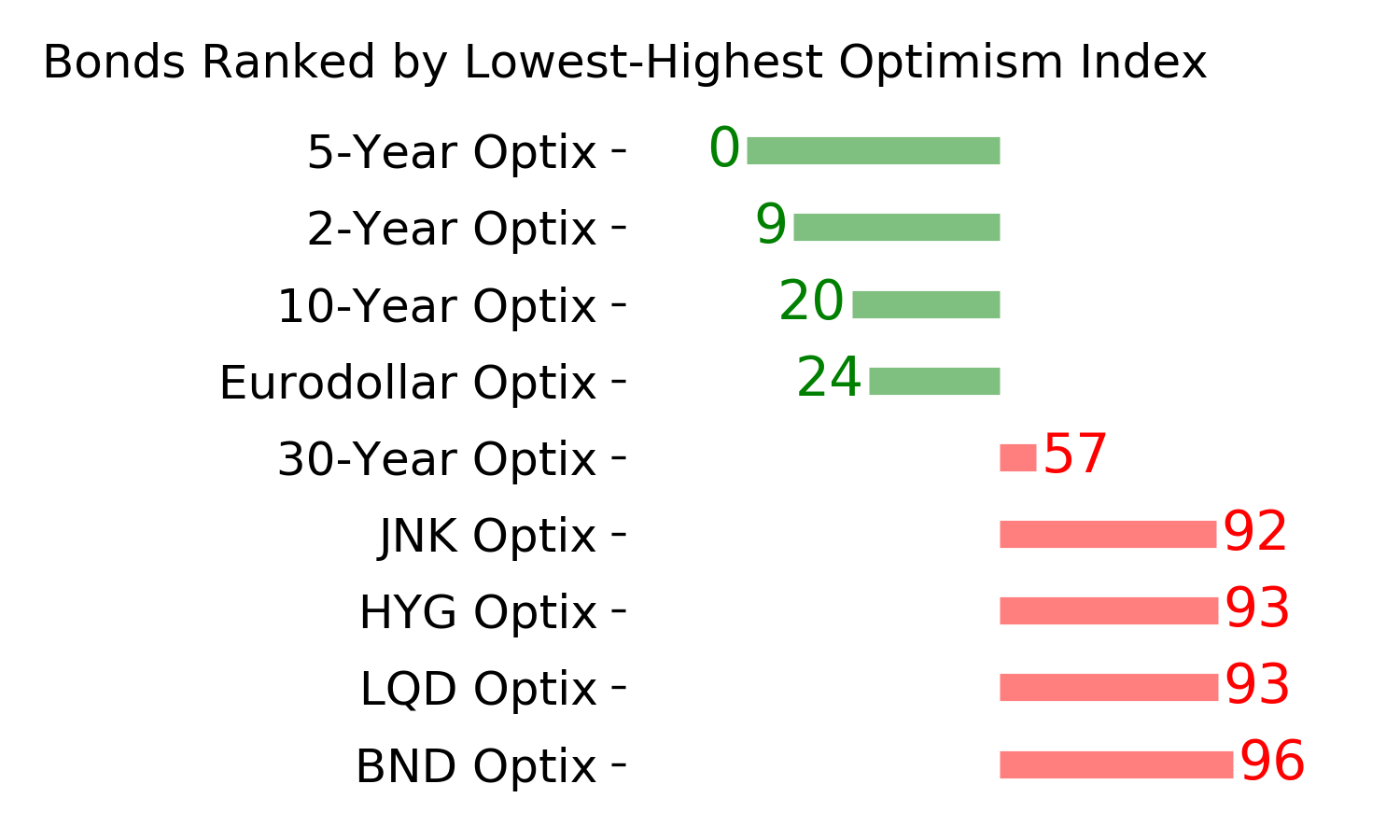

Bond ETF's - 10-Day Moving Average

|

|

|

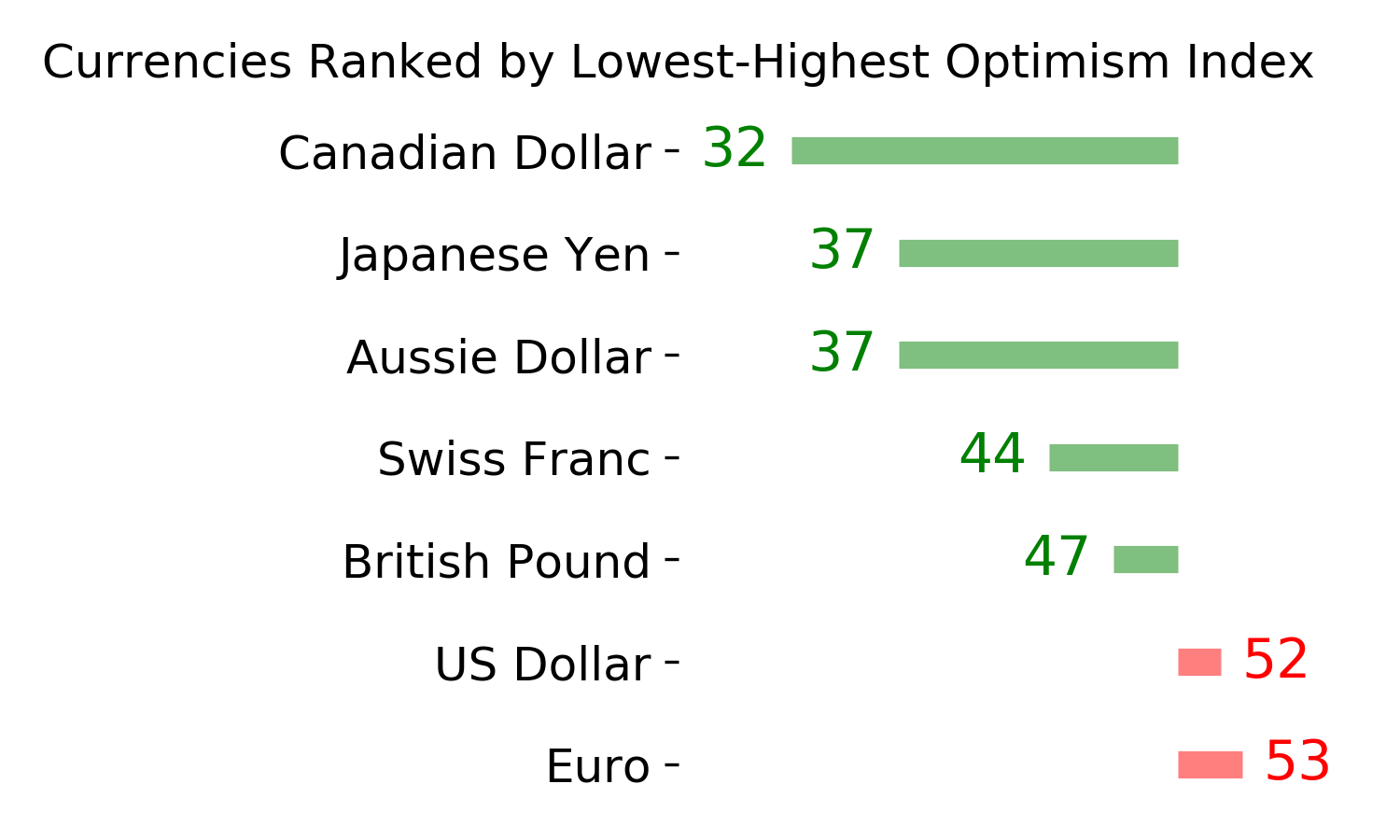

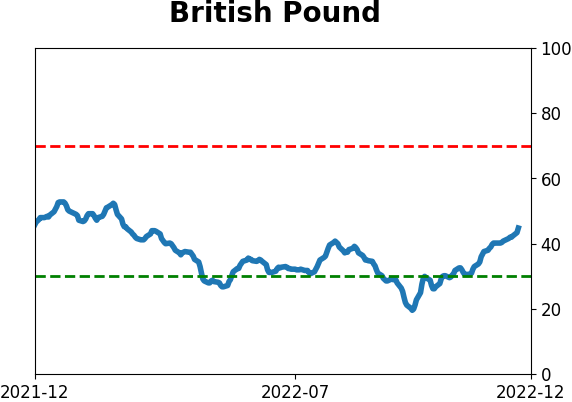

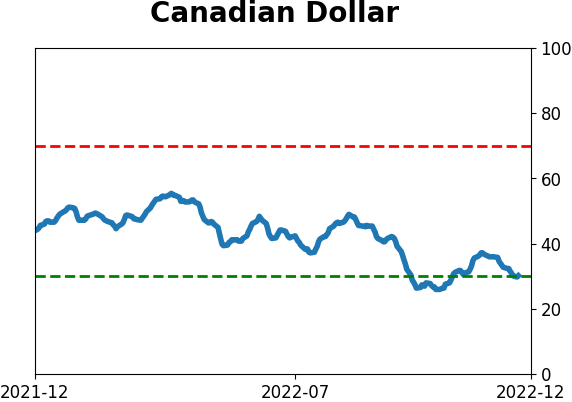

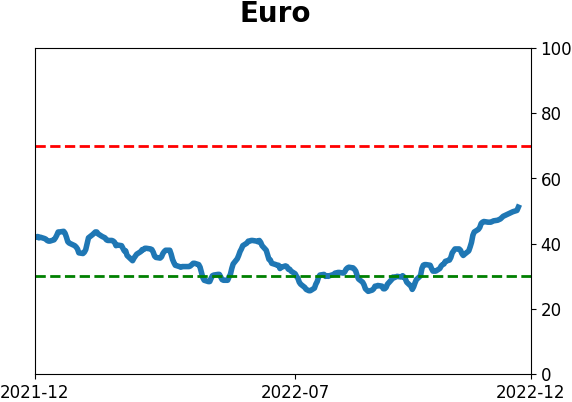

Currency ETF's - 5-Day Moving Average

|

|

|

Commodity ETF's - 5-Day Moving Average

|

|