Headlines

|

|

TradingEdge Weekly for Aug 16 - Volatility reversals, bond protection, tech thrust:

This week, we saw that volatility returned to markets. It was brief, however - historically so. The VIX reversed quickly from its spike and continued to decline. Other option indicators are giving bullish long-term implications, but the rising cost of protection against bond defaults should be watched. Some sectors are facing technical/seasonal issues, though tech has enjoyed a breadth thrust and volatility reversal.

|

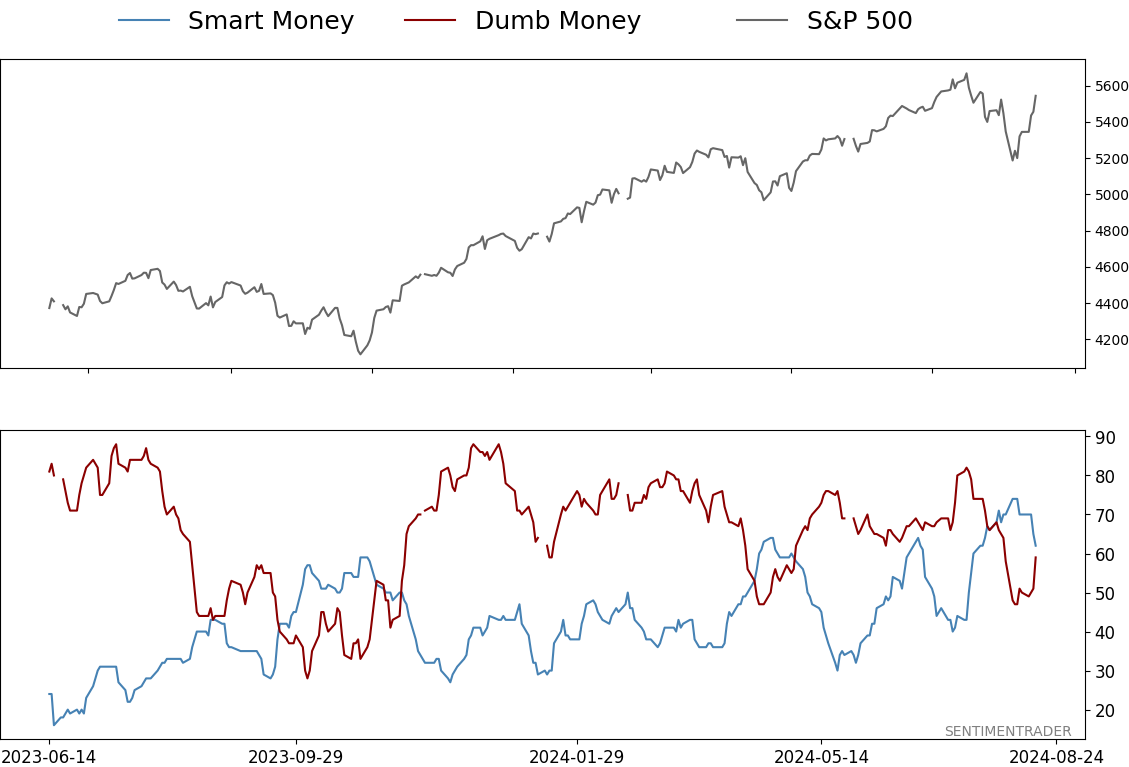

Smart / Dumb Money Confidence

|

Smart Money Confidence: 62%

Dumb Money Confidence: 59%

|

|

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

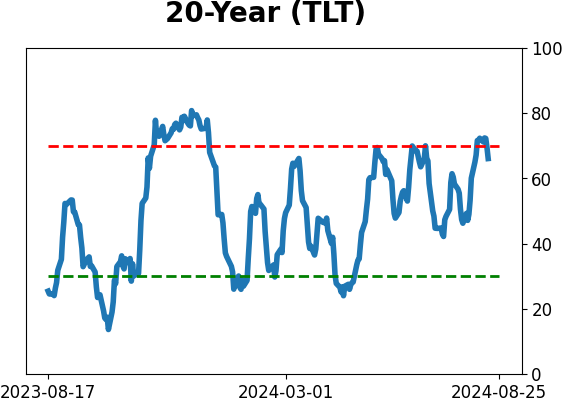

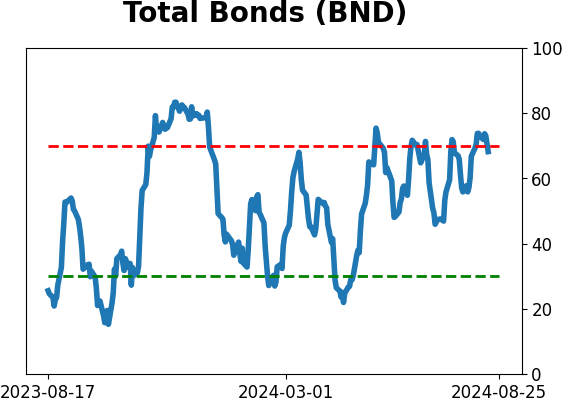

Bonds

|

Crude Oil

|

|

Gold

|

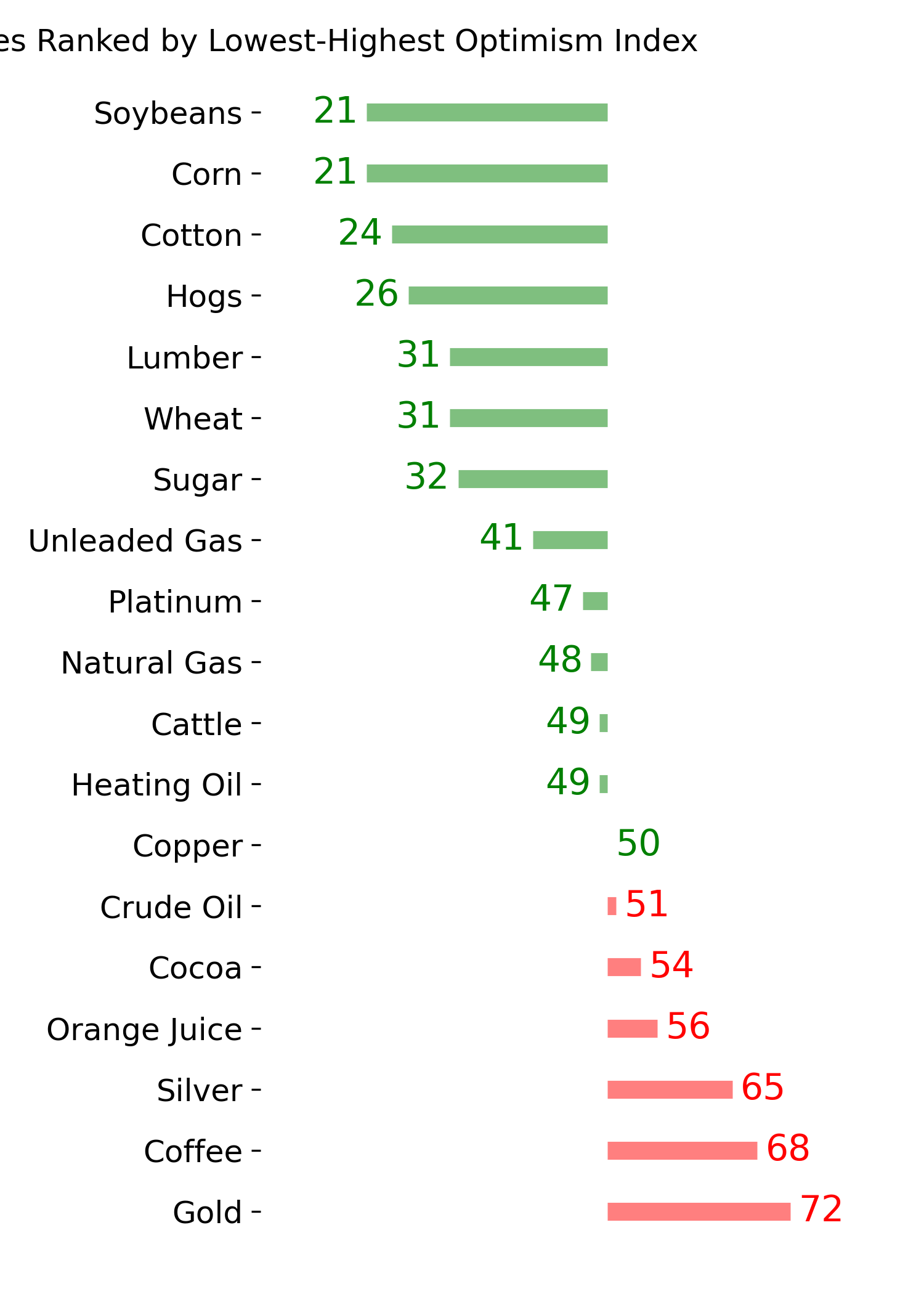

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

This week, we saw that volatility returned to markets. It was brief, however - historically so. The VIX reversed quickly from its spike and continued to decline. Other option indicators are giving bullish long-term implications, but the rising cost of protection against bond defaults should be watched. Some sectors are facing technical/seasonal issues, though tech has enjoyed a breadth thrust and volatility reversal.

FORECAST / TIMEFRAME

None

|

Key points:

- Investors finally had to deal with a spike in volatility (briefly)

- Expectations of future volatility ebbed quickly

- The 6-day drop in the VIX was the largest ever

- Other option-related indicators are giving bullish long-term implications

- Bond traders have started to pay up for default protection

- The tech sector has enjoyed a breadth thrust and volatility reversal

- A few sectors are giving some concerns

- Biotech, anyway, is entering a potential bright spot

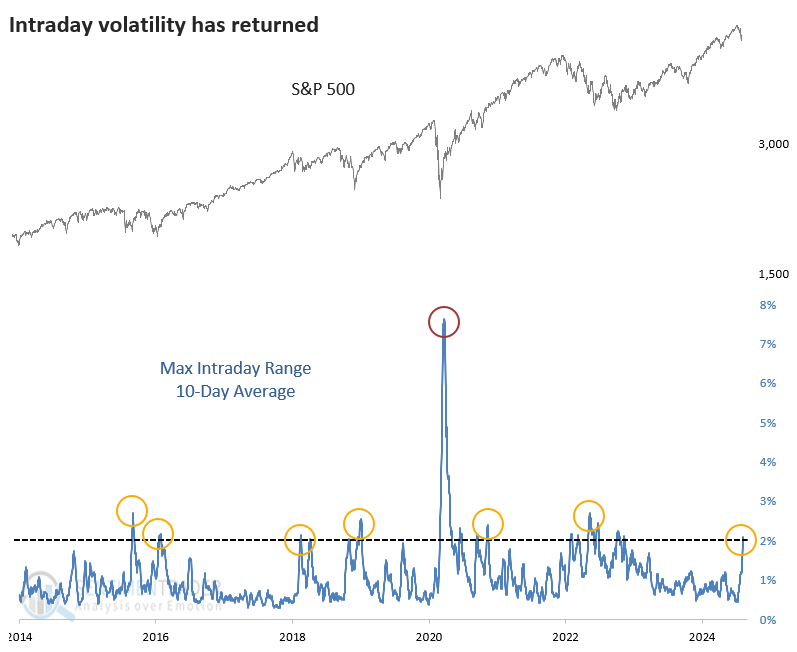

A return to volatility (for a little while)

After a historic stretch of calm conditions, investors have been reminded of what volatility looks like.

Over the past ten sessions, the S&P has averaged a maximum intraday range of at least 2%. During the last decade, that's been about the most the index has swung before calming down. The pandemic exceeded that by about 4x, but that was essentially the only exception.

The 2% threshold has contained most of the "normal" moves. The 10-day range went beyond 3% a handful of times, and all-out blow-out moves only occurred three times.

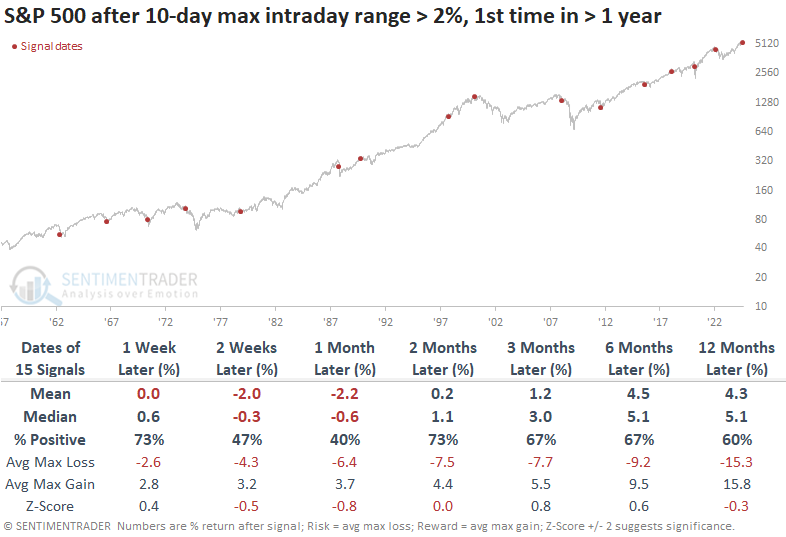

The table below shows S&P 500 returns after it ended a streak of at least a year with a maximum intraday range under 2%. A month later, the S&P was positive only 40% of the time, with a negative average return and poor risk/reward ratio. But from two to twelve months later, its returns were about in line with any random time, even though the risk/reward skew remained ugly.

The past 25 years have been especially troublesome. The spike in intraday volatility served as a good entry point for long-term investors in 2011 and 2015, but other than that, not so much. The other signals witnessed more risk than reward up to a year later.

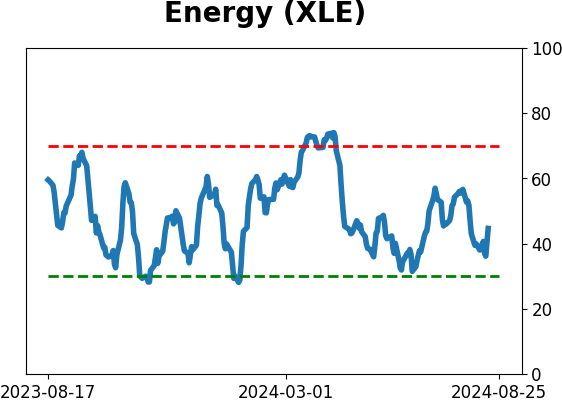

A return of volatility in the S&P 500 often prompted investors to shift their allocations to more defensive sectors. Energy stocks were the biggest beneficiary (not that that's considered a defensive sector), along with staples, utilities, and health care. Over the past 25 years, defensive stocks have stood out even more. Three to twelve months later, that factor rallied every time.

Volatility expectations dropped quickly

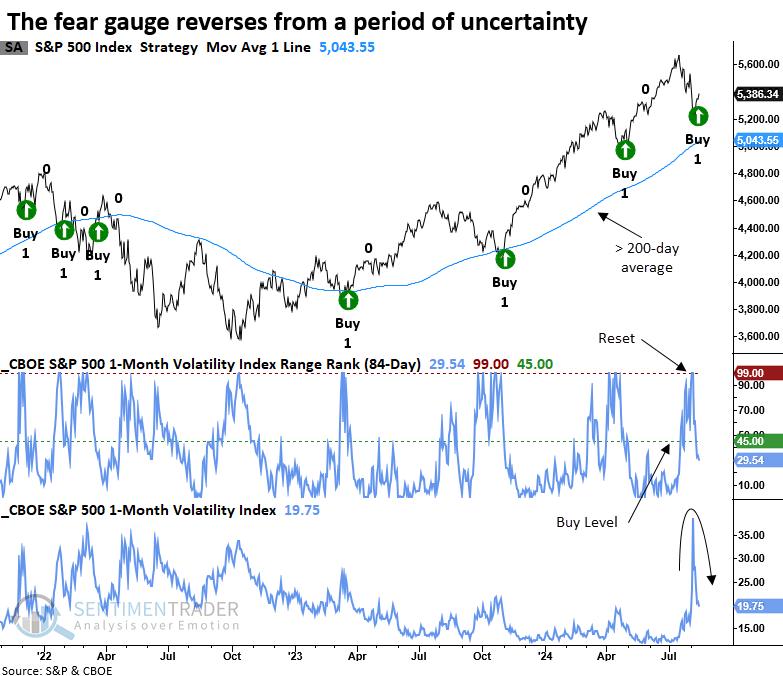

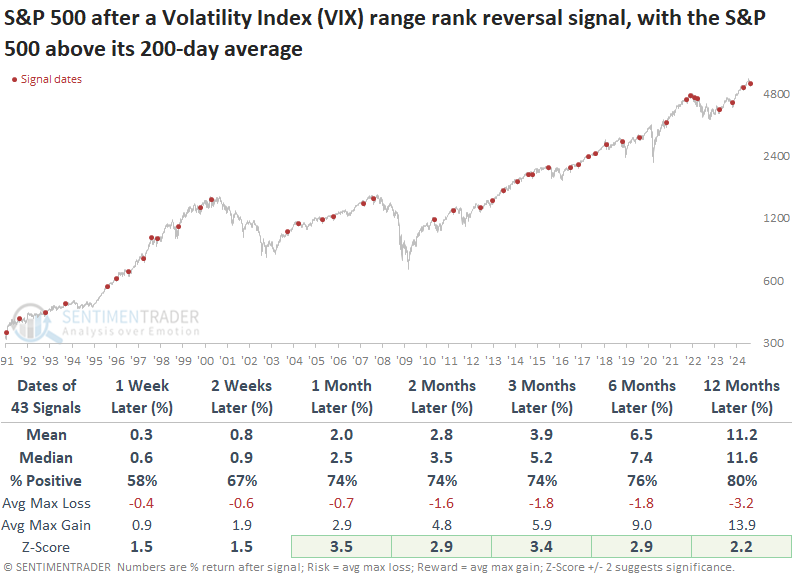

The biggest caveat about putting too much weight on rising volatility is that it has already decreased substantially. A swing trading system based on the CBOE Volatility Index (VIX) triggered a new buy signal. Dean showed that comparable reversals in volatility produced excellent returns and consistency for the S&P 500.

Following a significant surge in the VIX, a swing trading system triggered a new alert when the volatility index's 84-day range rank reversed lower after rising to the top end of its range.

Whenever the S&P 500 Volatility Index's 84-day range rank cycled from above 99% to less than 45%, with the S&P 500 above its 200-day average and exhibiting positive price momentum, the world's most benchmarked index displayed excellent returns and consistency over medium and long-term horizons. Over the next two months, only eight precedents saw a maximum loss exceeding -5%.

A very fast volatility reset

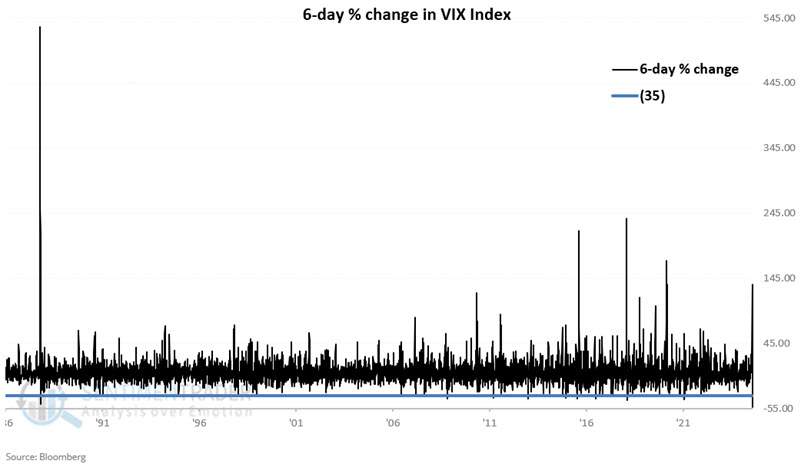

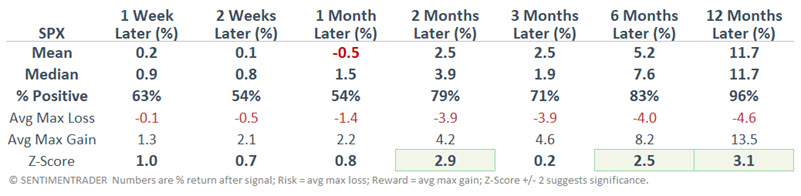

Jay also noted that a sharp plunge in the index has often preceded higher stock prices, and the recent one in the VIX Index was the largest on record.

For this test, we will consider the VIX Index's six-day percentage rate of change. Specifically, we will look for rare occasions when the index declined by -35% or more over six trading days. In other words, we want to see a peak in VIX and a sharp decline over the next six trading days.

The chart below displays all six-day rate-of-change readings with the -35% level (horizontal blue line) noted below.

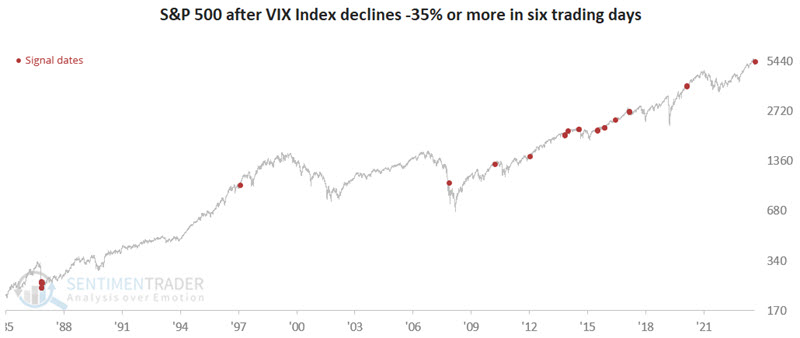

The chart below highlights all dates when the VIX declined -35% or more in six days.

When we look only at signals that are the first in three months, the S&P 500 was higher a year later 100% of the time by an average of +14%.

It is helpful to understand the potential usefulness of the indicator if we apply specific trading rules. So, if the VIX Index declines -35% over six trading days, we will buy and hold the S&P 500 for 252 trading days (roughly one year). If a new signal occurs within that year, we will extend the holding period for another 252 trading days.

The chart below displays the hypothetical growth of $1 invested in the S&P 500 only, as described above, from 1986-01-02 through 2024-08-13.

Note that this "strategy" (such as it is) was long the S&P 500 continuously from 2014-10-23 through 2019-02-20 due to the overlapping nature of the signals. Even though drawdowns could be large, every signal was a winner, averaging +20%.

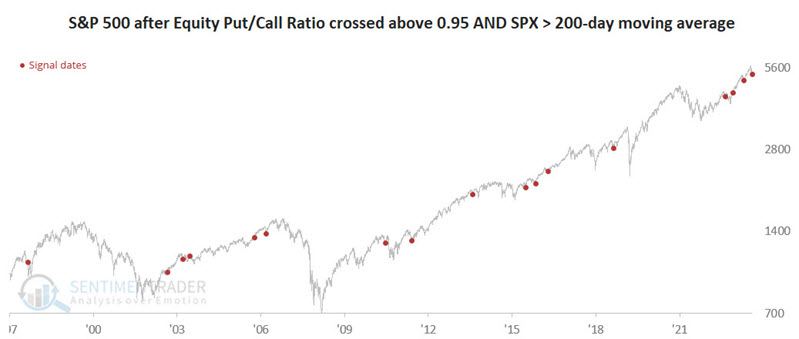

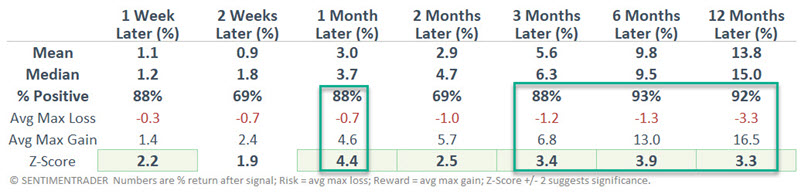

More positive indications

Jay further noted that the Equity Put/Call Ratio, the ROBO Put/Call Ratio, and the VIX Index have all flashed typically useful signals recently

Some indicators have typically proven helpful in identifying buyable pullbacks in an ongoing uptrend. The Equity Put/Call Ratio indicator fits this description. The chart below highlights all dates when the indicator crossed above 0.95 while the S&P 500 Index was above its 200-day moving average.

The most recent signal generated on 2024-08-08 suggests a favorable outlook for stocks in the year ahead.

Jay also outlined bullish implications from a more specific put/call ratio as well as elevated levels of implied volatility.

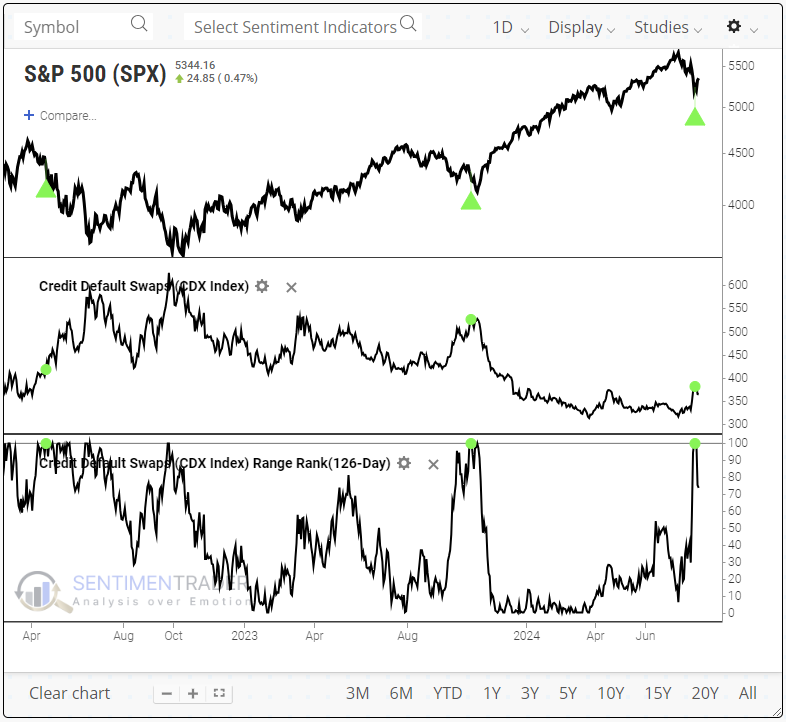

One worry - bond traders are paying up for protection

As investors' concerns rose during the volatility spike, traders bought protection against bond defaults.

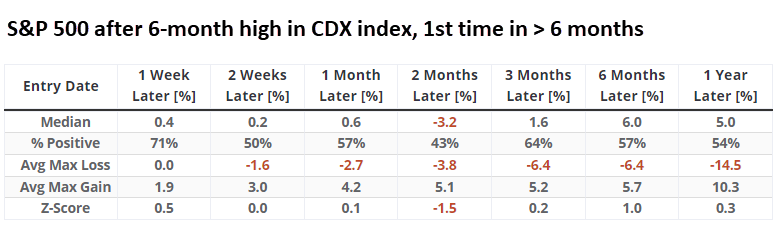

Prices rise when traders scramble for protection, which we can see in the spike in credit default swaps. The chart below shows that the price of CDS protection notched a six-month high last week (100% of its 126-day range) for the 3rd time since the 2021 peak. The first augured the 2022 bear market; the second triggered near the low for stocks in the fall of 2023.

When we zoom out, we can see that these signals have been triggered multiple times over the past couple of decades.

Over the following two months, the S&P 500 was relatively weak, with only a 43% win rate and a negative median return. Even a year later, the average risk outweighed the average reward.

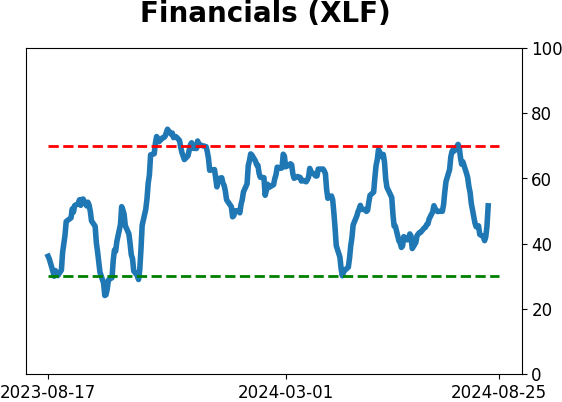

Among major sectors, the next couple of months showed weak returns across the board, except for the defensive utilities sector. Worst of all were the financials, with negative average returns and poor win rates over the medium- to long-term.

If we go back to the test and see how the XLF fund performed after these signals, we see that over the next year, XLF sported a negative return either six or twelve months later after nine signals. It rose over both of those time frames only four times.

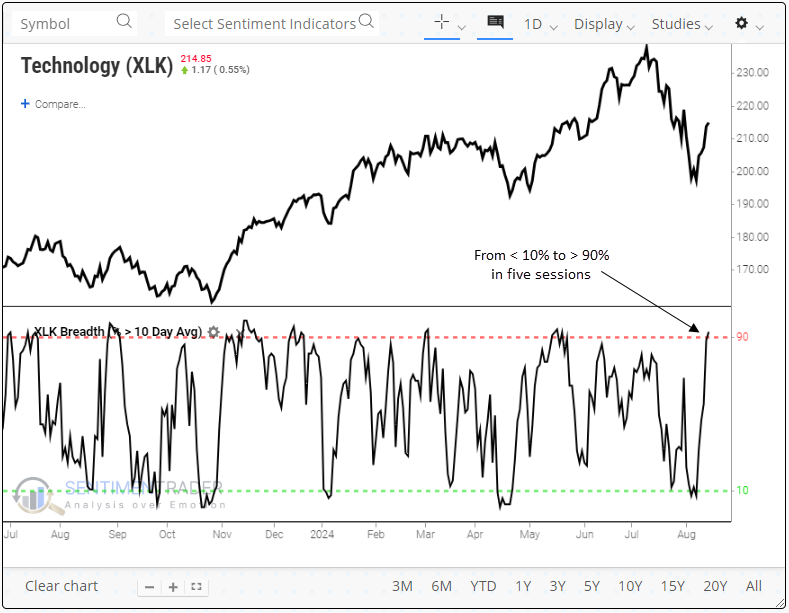

Tech thrust and volatility reversal

Dean showed that the percentage of Technology stocks above their 10-day average cycled from oversold to overbought. In addition, the implied volatility index for the sector cycled from a high to low relative level.

Over the last five sessions, the percentage of S&P 500 Technology sector stocks above their 10-day average cycled from below 10% to above 90%, triggering a breadth thrust signal.

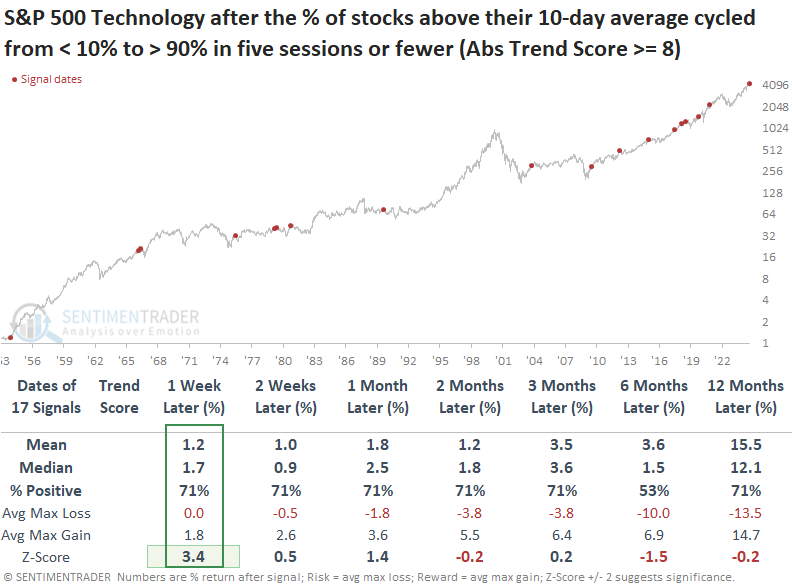

Whenever the percentage of S&P 500 Technology sector stocks above their 10-day average cycled from below 10% to above 90% in five sessions or fewer, and the sector maintained an absolute trend score of eight or higher, the industry typically rallied over the following month. During this period, gains were observed at some point in 15 of the 17 historical instances.

Suppose we include a condition requiring both the absolute and relative trend composites for the S&P Technology sector to maintain a score of eight or higher at the time of a signal. In that case, when Technology displayed positive trends, like now, returns and consistency were outstanding, with several time frames exhibiting significance.

Similar to the VIX range reversal noted above, the gauge tied to the Nasdaq 100 reversed as well.

The Nasdaq 100 Volatility Index (VXN) 's historical data (since 2005) is not as extensive as the VIX's (since 1990), and most signals occurred during a growth-driven bull market led by Technology. Still, results are spectacular across all time frames.

Additionally, drawdowns were limited. Over the following three months, the signal experienced only three maximum losses exceeding -5%.

Potential trouble among sectors

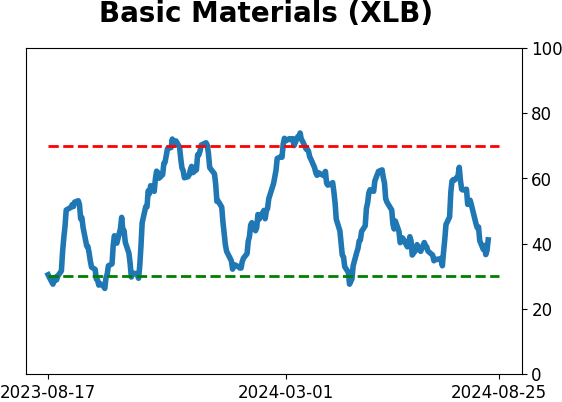

Jay suggested that when price trends and seasonal trends align, there is often a great opportunity or at least a warning to stand aside. Four sectors set up for potential trouble in the months ahead are materials, Argentinian stocks, gold stocks, and regional banks.

The SPDR S&P 500 Materials ETF (ticker XLB) has been moving sideways since March. In the chart below, we see price action currently below the 50-day moving average and a recent negative crossover in the Price Momentum Oscillator.

In the annual seasonal chart for XLB, we see a sector about to enter an unfavorable seasonal period from Trading Day of the Year #154 through #190. For 2024, this period extends from 2024-08-12 through 2024-10-02. The chart below displays the hypothetical growth of $1 invested in ticker XLB only during this period every year since 1999. XLB has lost ground 64% of the time, with a cumulative decline of -60%.

He then outlined similar concerns for Argentina, gold miners, and regional banks.

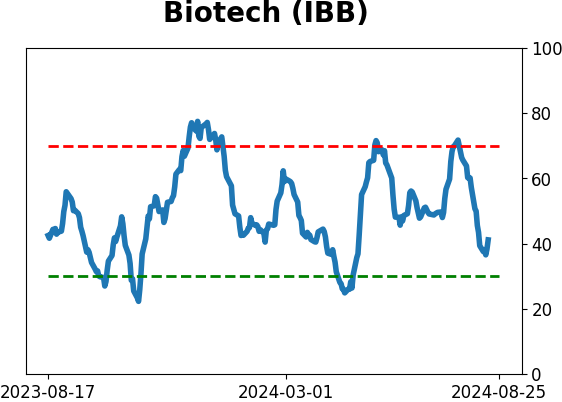

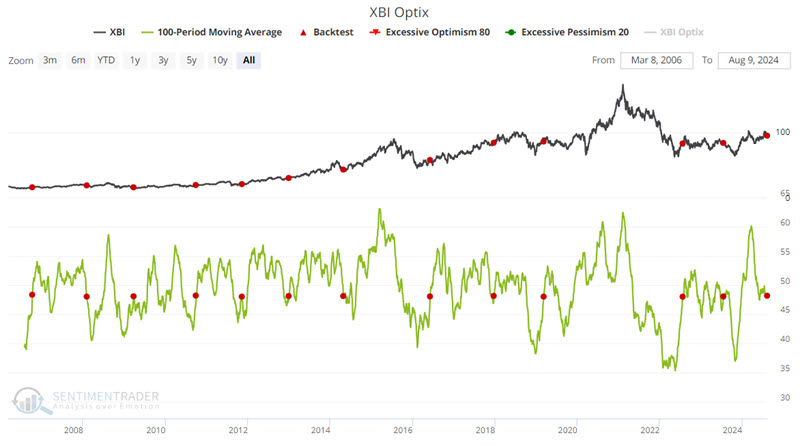

Bright spot for biotech

The biotech sector has been working higher, and our XBI Optix indicator just flashed a favorable sign for biotech stocks. Jay noted that XBI is also soon entering a brief favorable seasonal period.

After bouncing off a long-term support level in October 2023, XBI rallied over 60% in March 2024 before pulling back in recent months. The chart below highlights those dates when the 100-day average of our XBI Optix indicator crossed above 48% for the first time in a year.

The Win Rates for six and twelve months are above average, and the 12-month Median Return is a robust 21.62%. However, before six months, returns are often quite volatile and inconsistent.

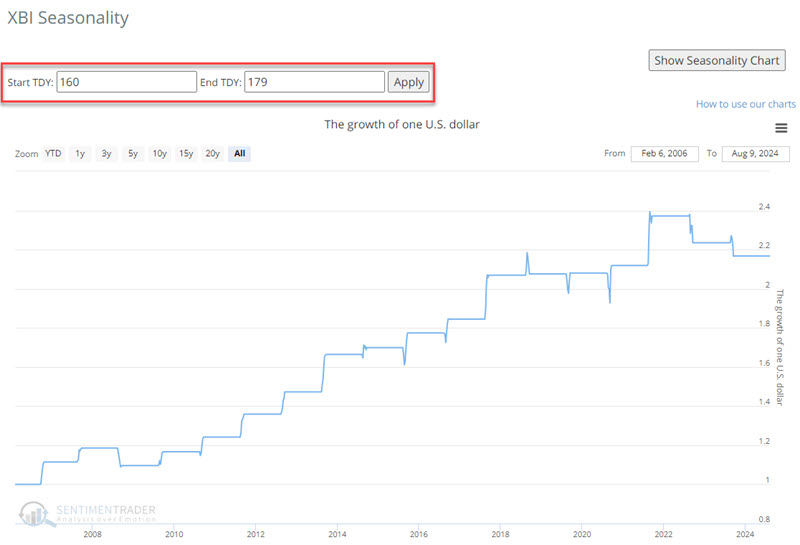

A favorable period for XBI extends from Trading Day of Year (TDY) # 160 through TDY #179. For 2024, that period extends from the close on 2024-08-20 through 2024-09-17. The chart below displays the hypothetical growth of $1 invested in XBI only during this period since 2006.

The good news is that this period has seen XBI risk 83% of the time (15 out of 18 years). Tempering this, however, is that the most recent two years were losers.

About TradingEdge Weekly...

The goal of TradingEdge Weekly is to summarize some of the research published to SentimenTrader over the past week. Sometimes there is a lot to digest, and this summary highlights the highest conviction or most compelling ideas we discussed. This is NOT the published research; rather, it pulls out some of the most relevant parts. It includes links to the published research for convenience, and if you don't subscribe to those products, it will present the options for access.

Indicators at Extremes

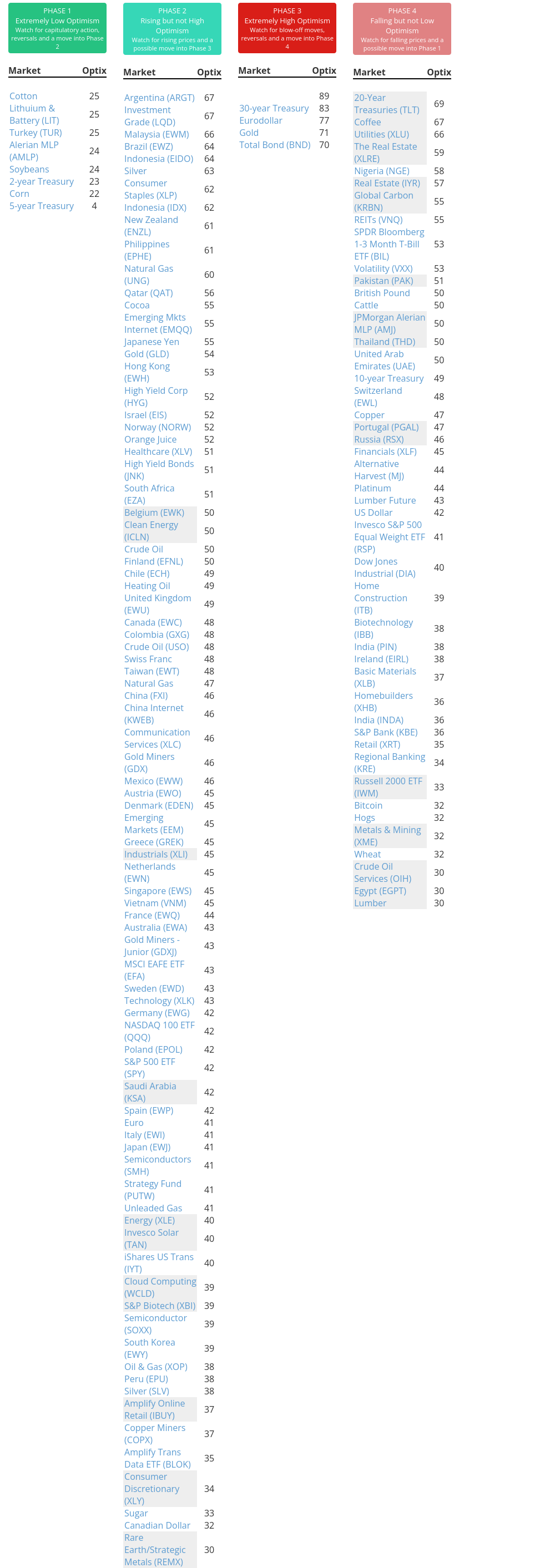

Phase Table

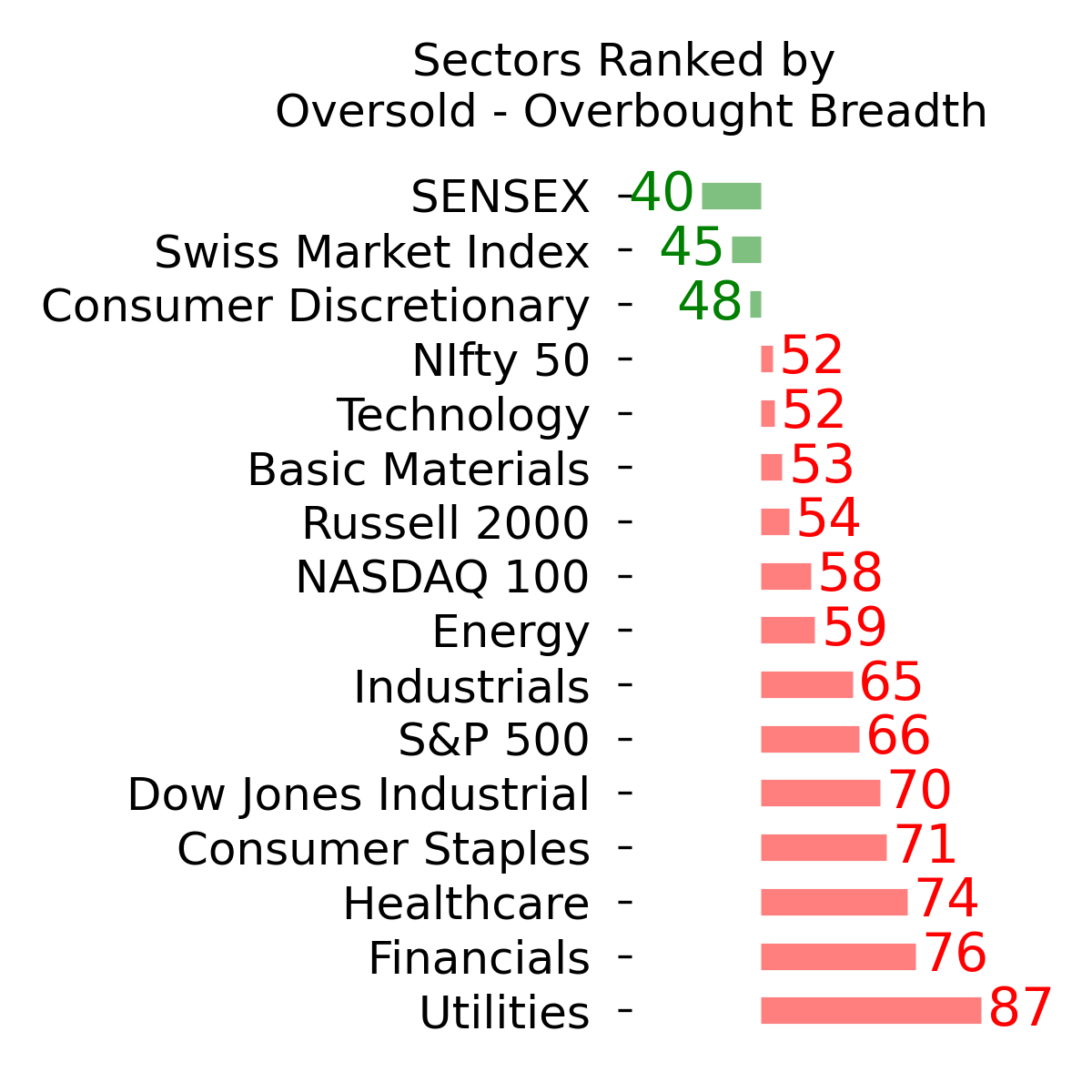

Ranks

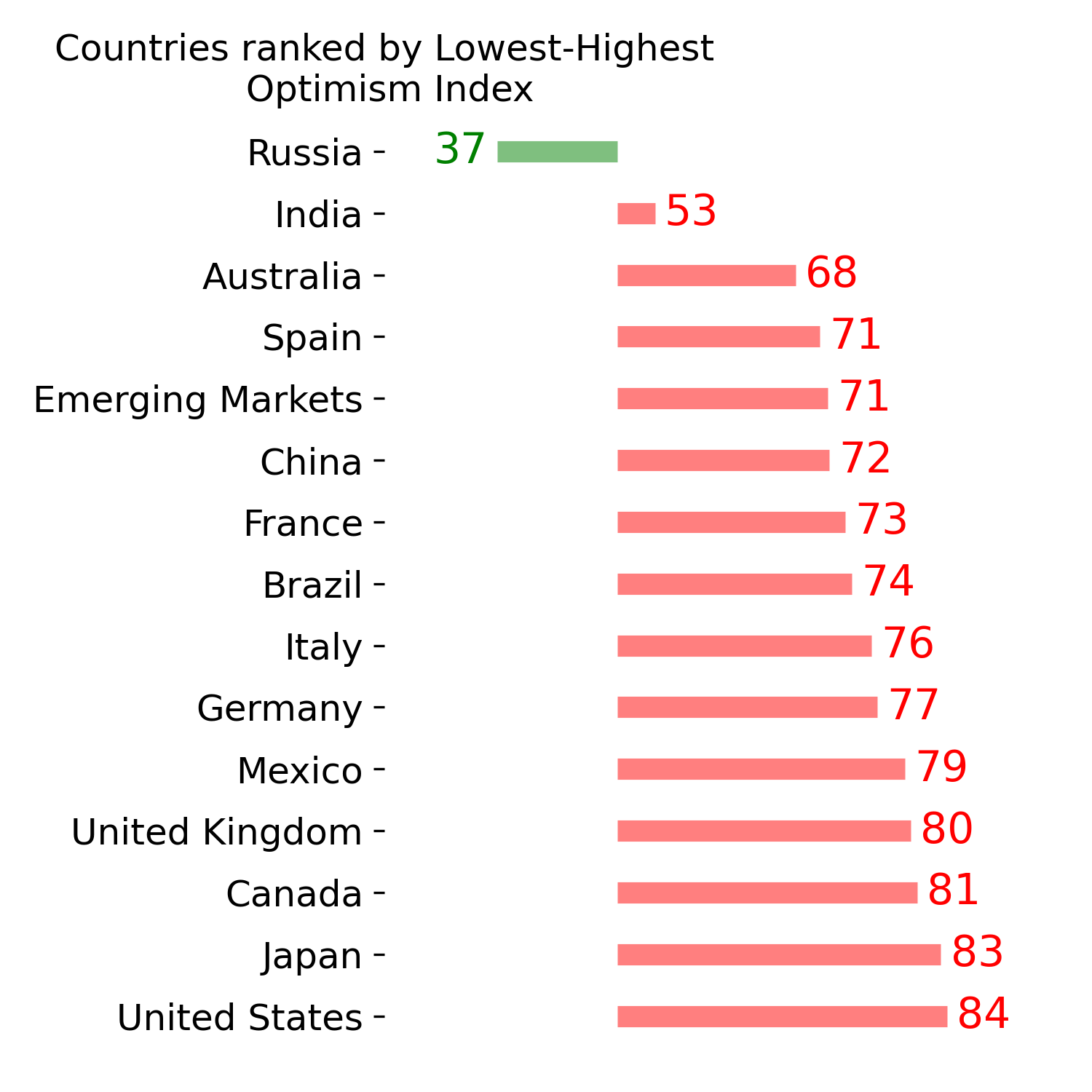

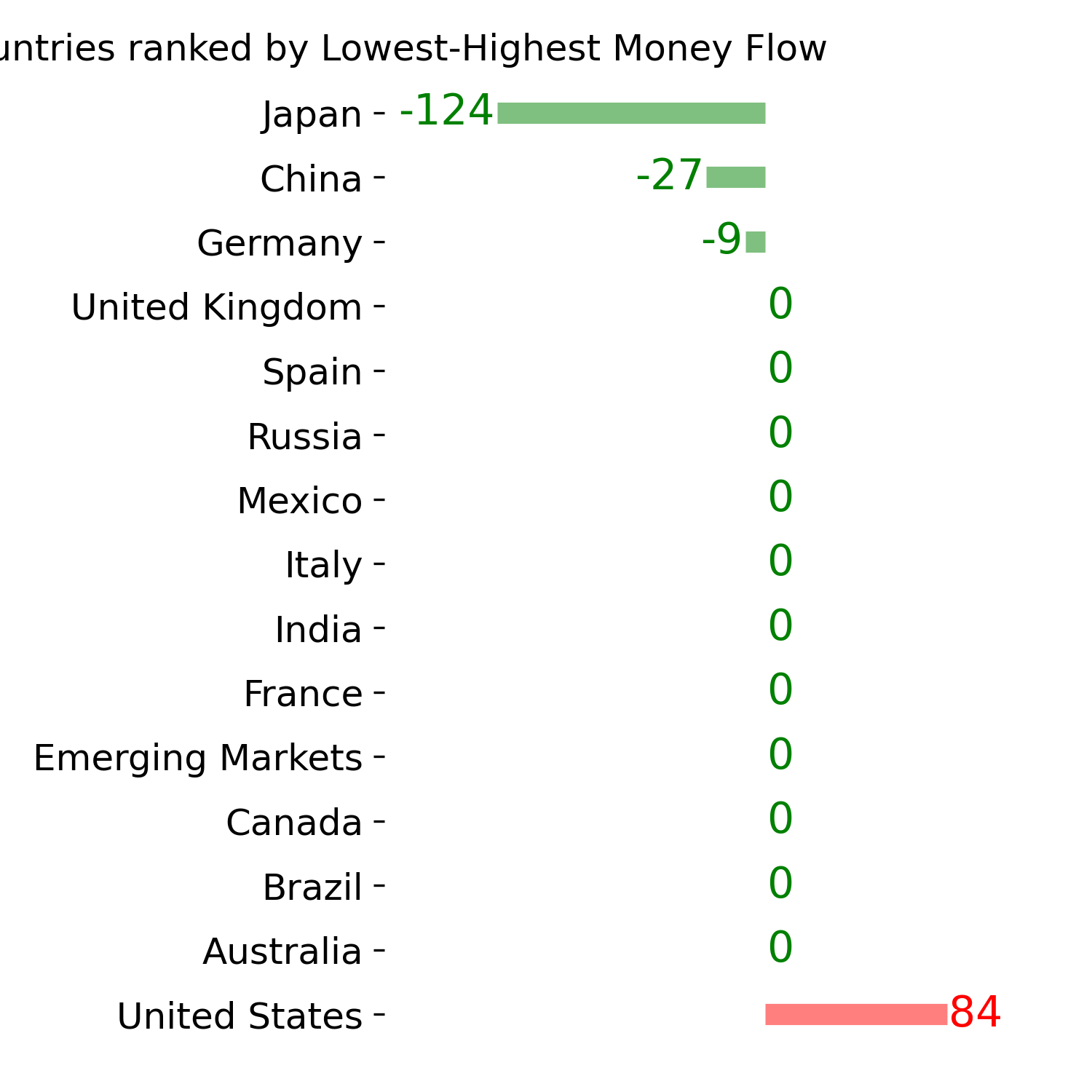

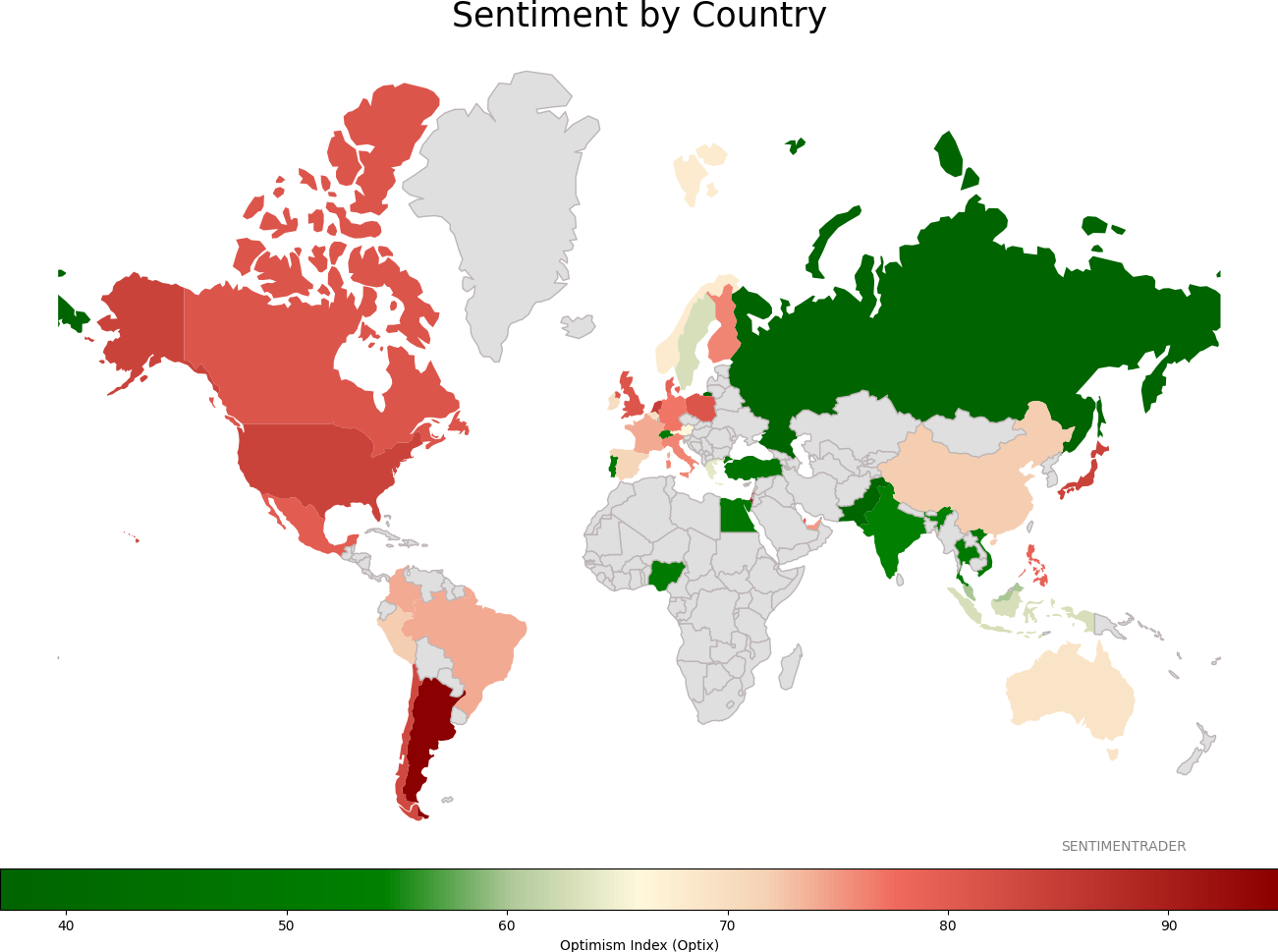

Sentiment Around The World

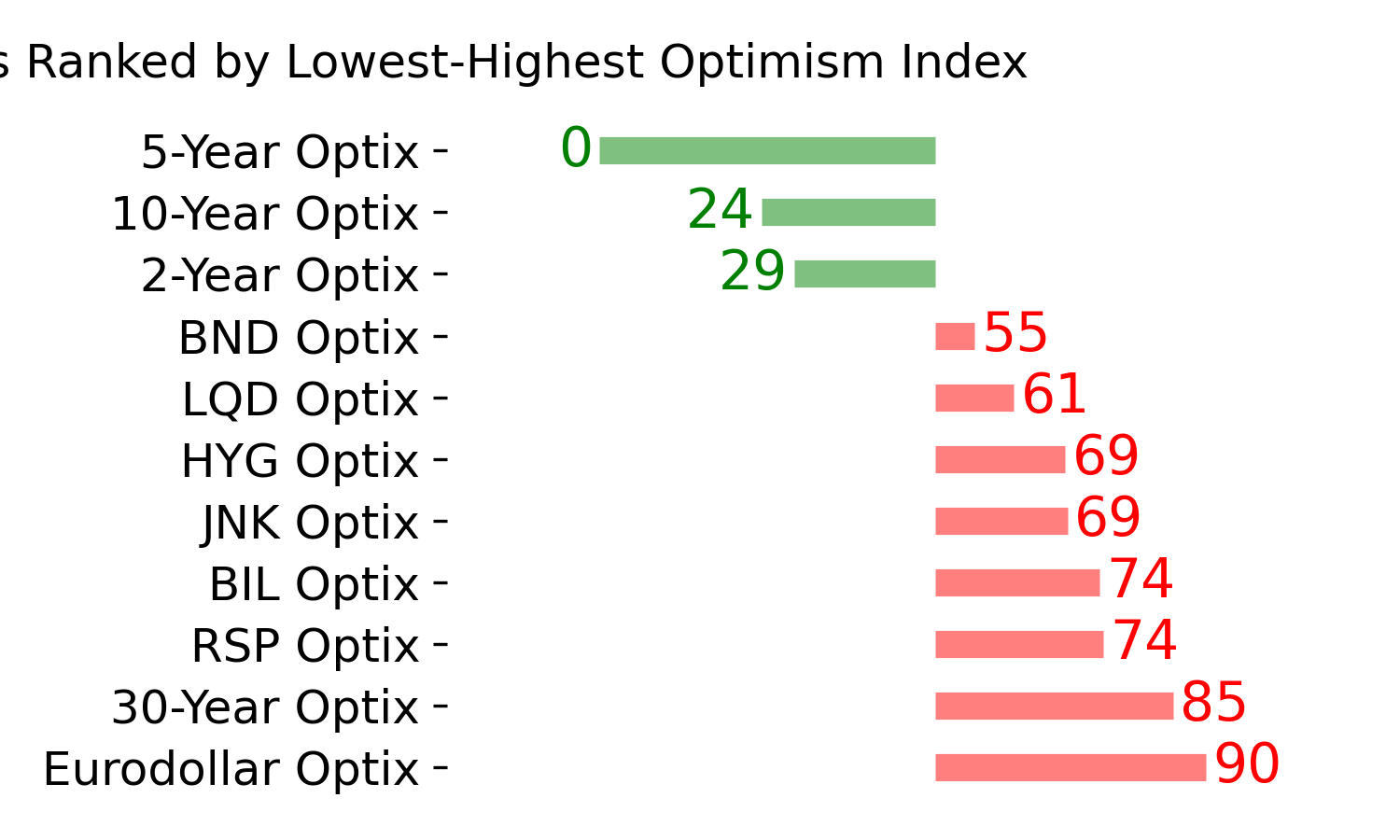

Optimism Index Thumbnails

|

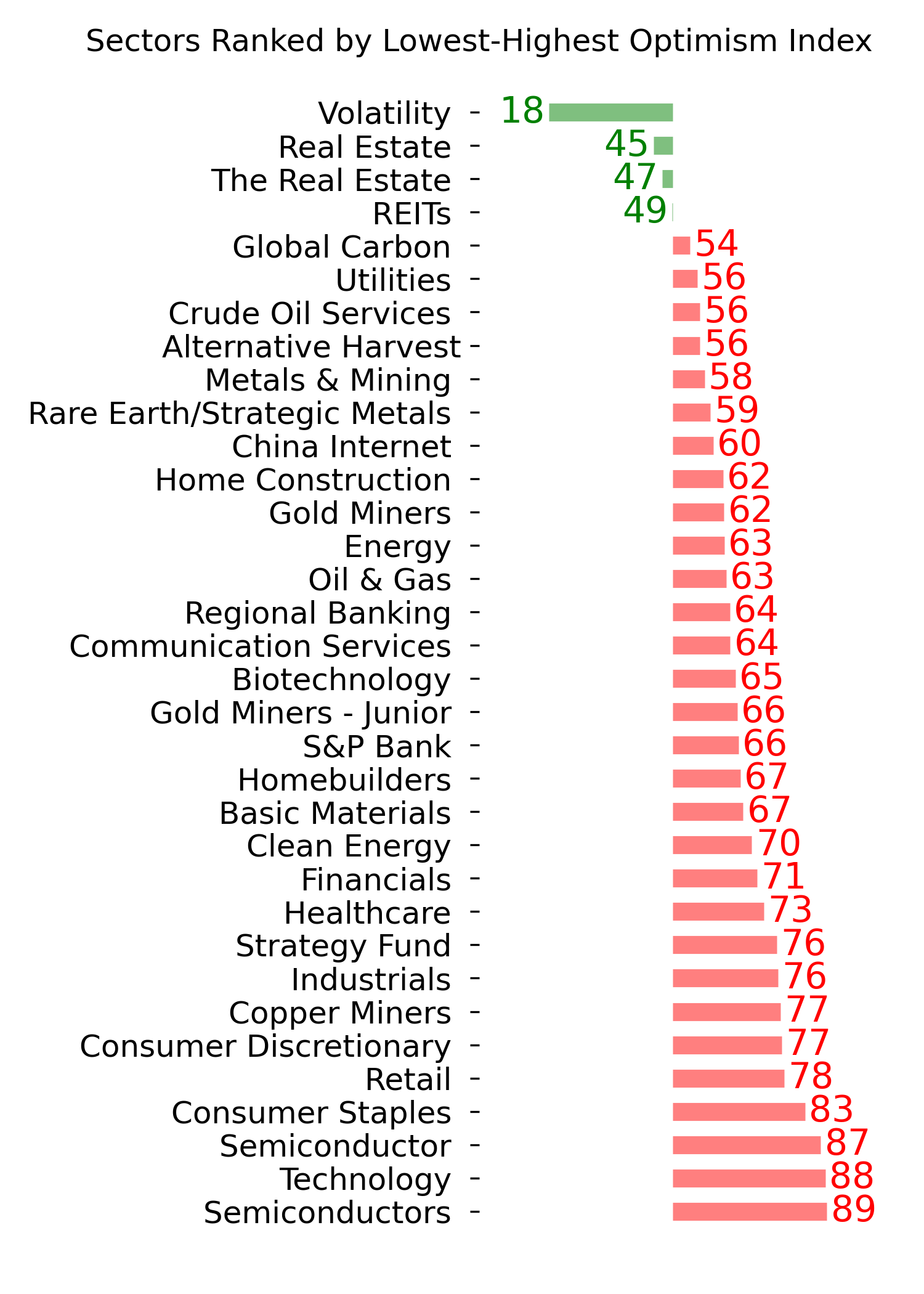

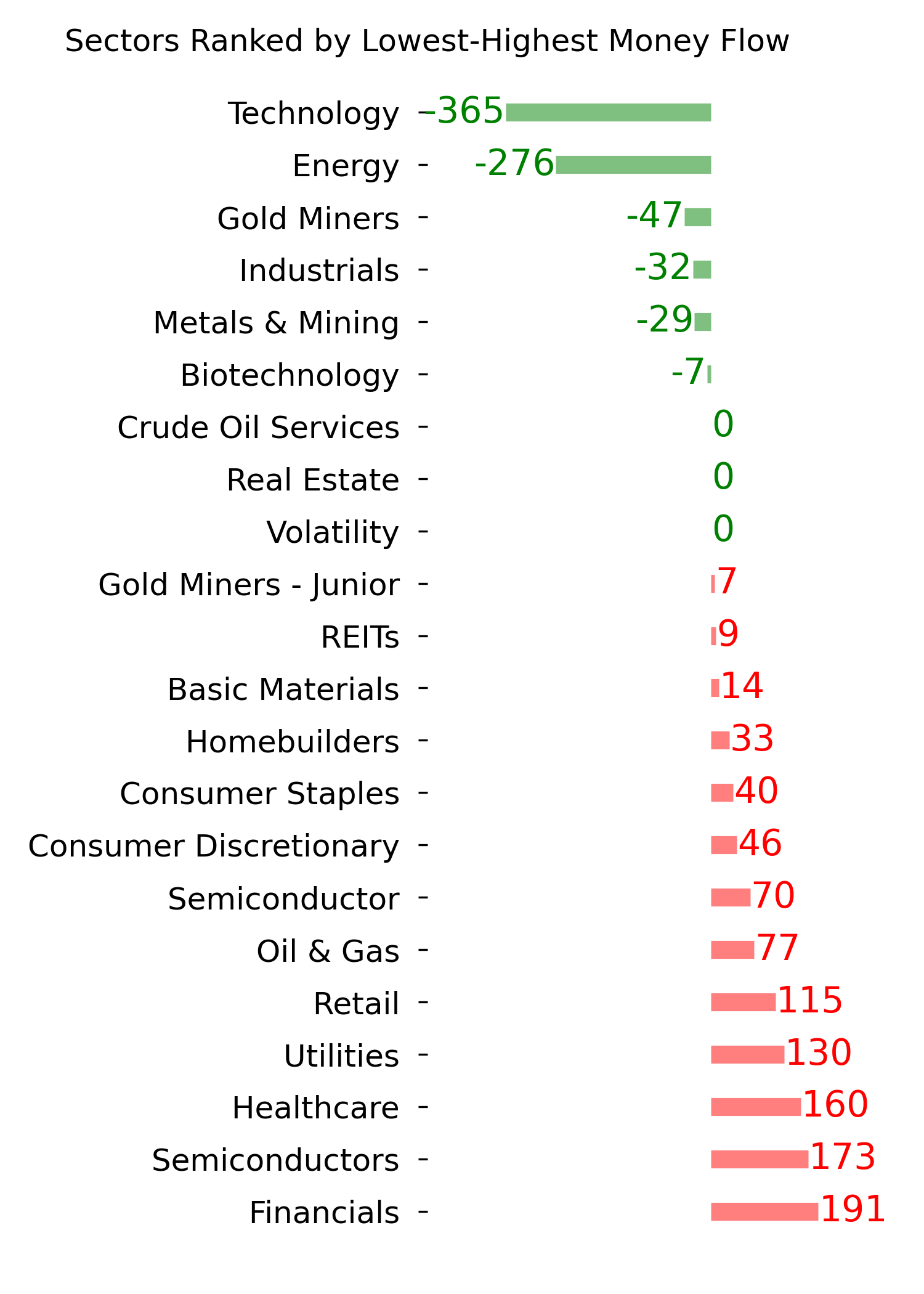

Sector ETF's - 10-Day Moving Average

|

|

|

Country ETF's - 10-Day Moving Average

|

|

|

Bond ETF's - 10-Day Moving Average

|

|

|

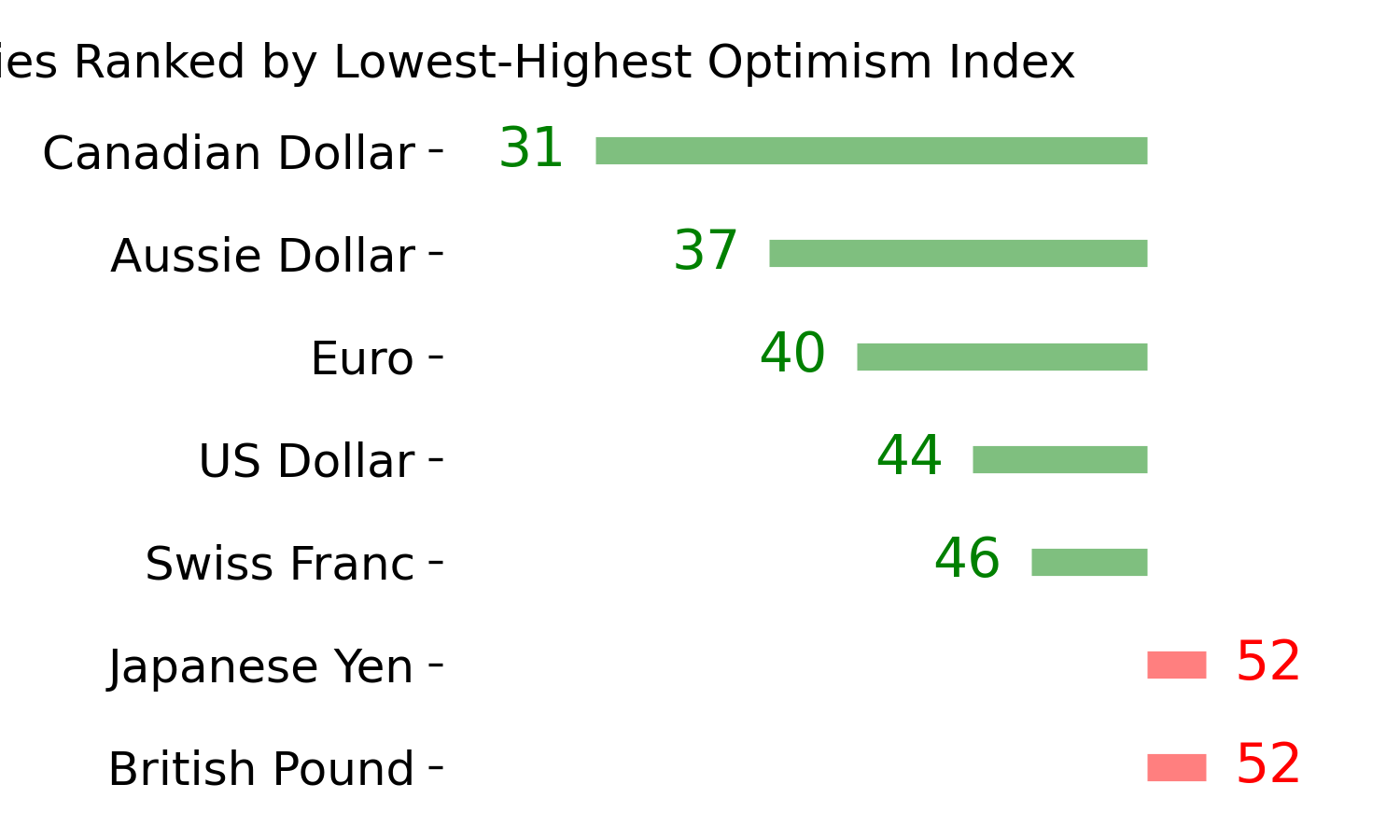

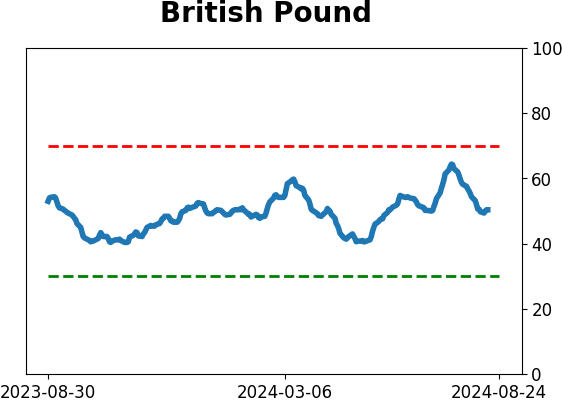

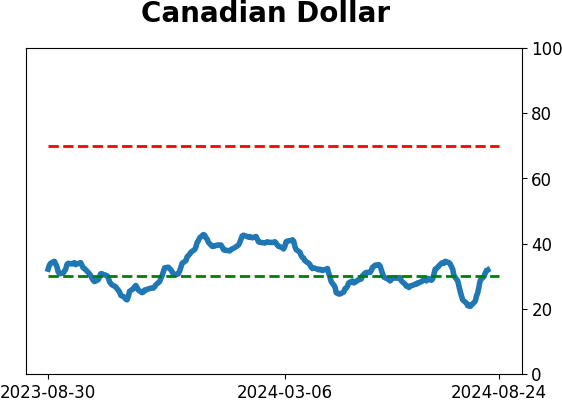

Currency ETF's - 5-Day Moving Average

|

|

|

Commodity ETF's - 5-Day Moving Average

|

|