Headlines

|

|

Bond traders are pricing in more default risk:

The recent rise in volatility triggered bond traders to rush into protection against defaults. The rise in credit default swap prices was enough to push them to 6-month highs. Multi-month highs in CDS prices have augured in some tough markets, particularly for financials.

|

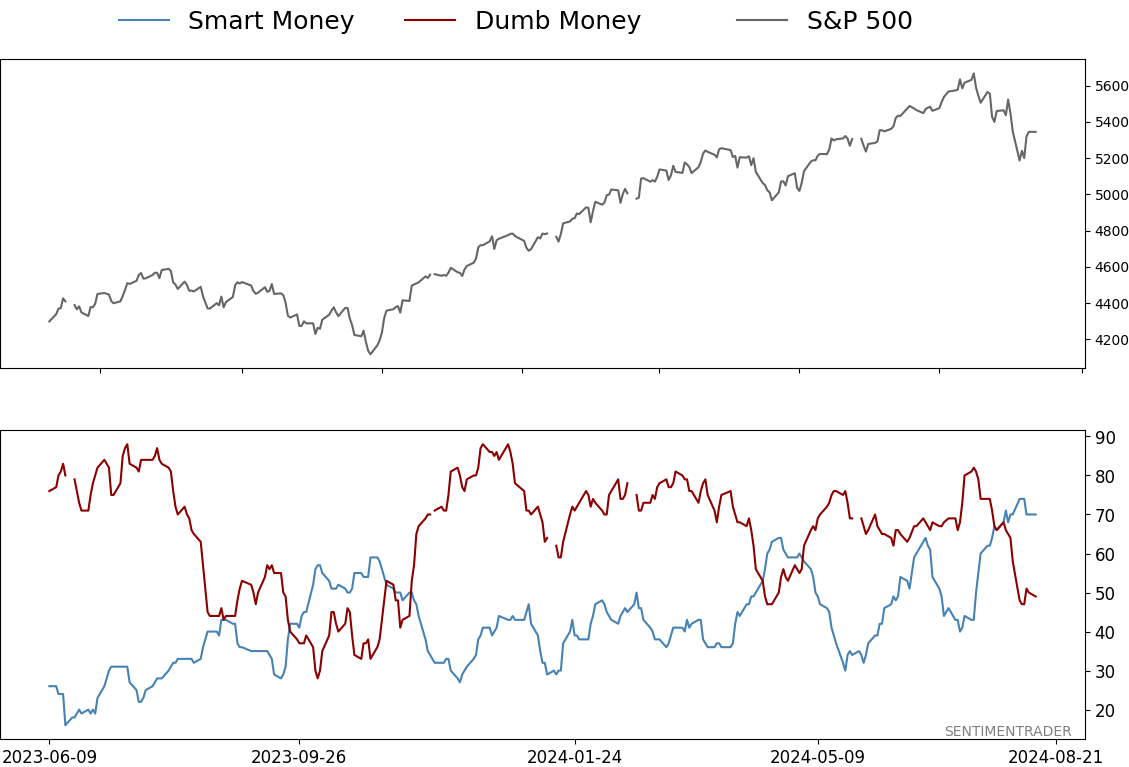

Smart / Dumb Money Confidence

|

Smart Money Confidence: 70%

Dumb Money Confidence: 49%

|

|

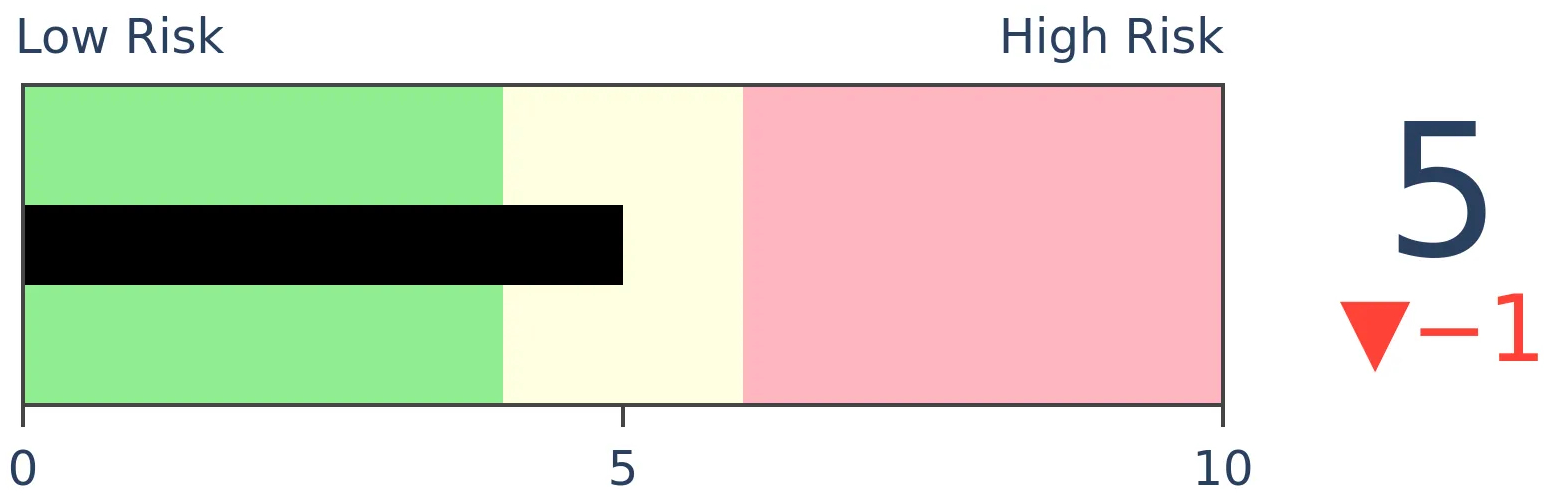

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

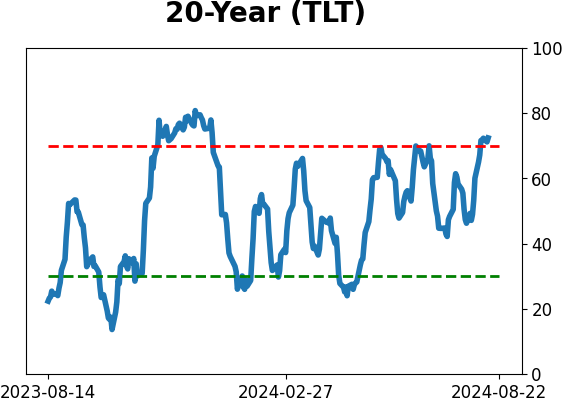

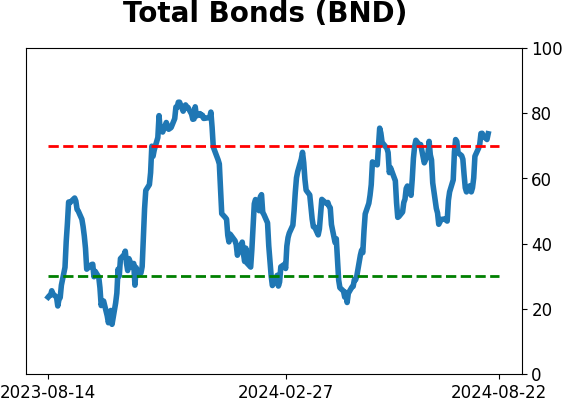

Bonds

|

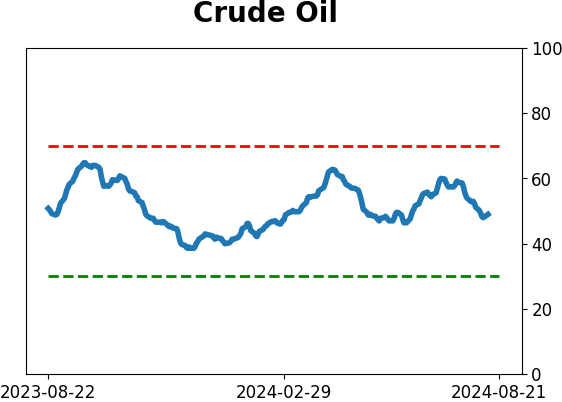

Crude Oil

|

|

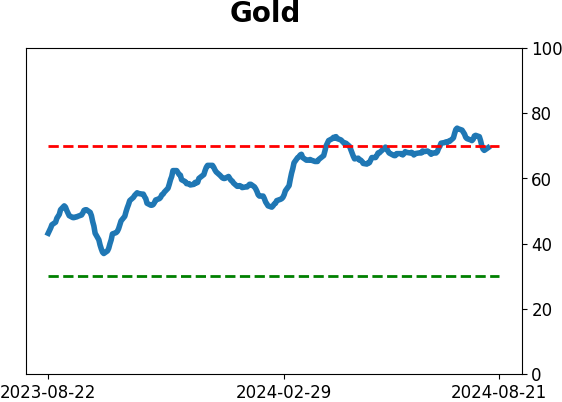

Gold

|

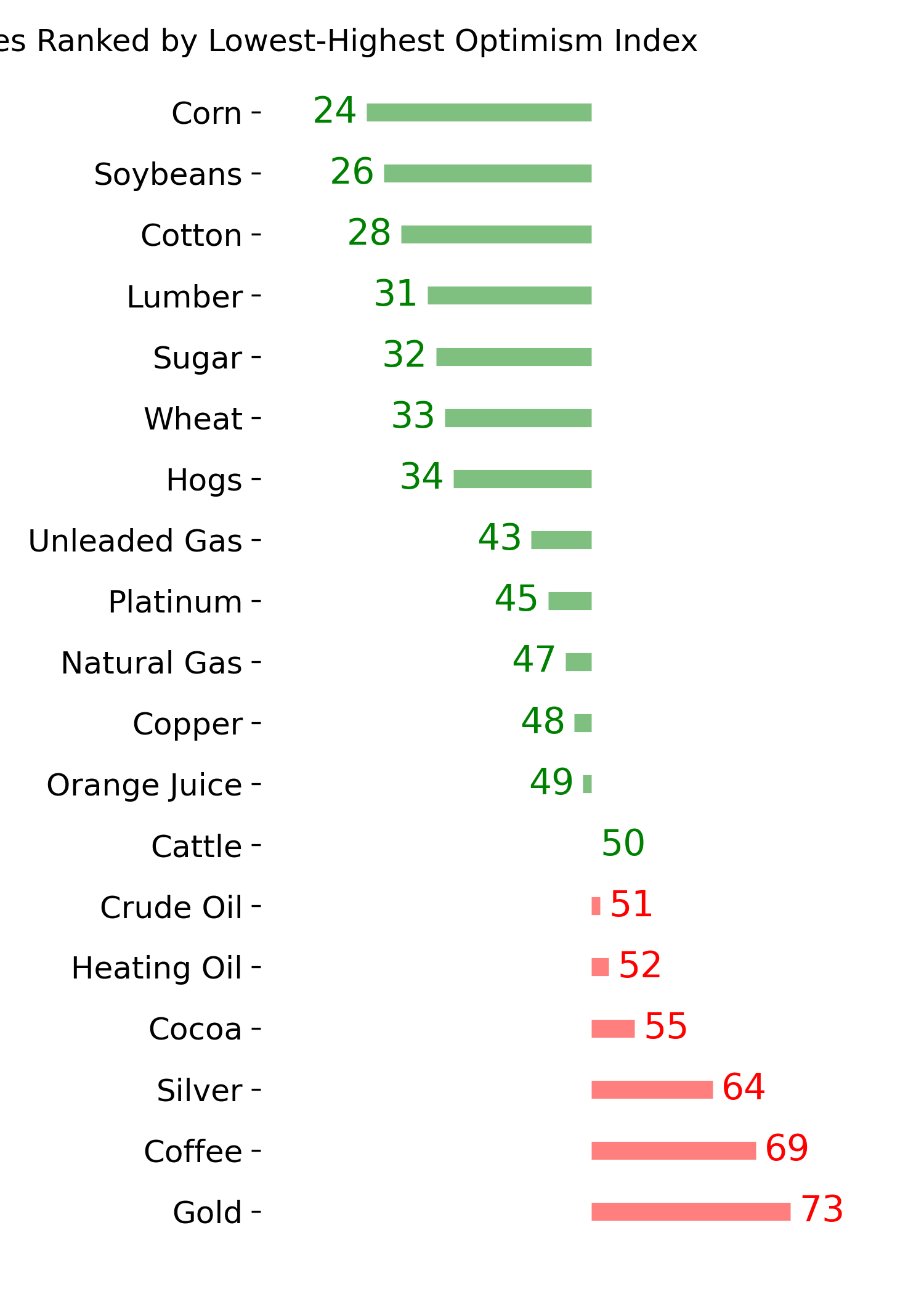

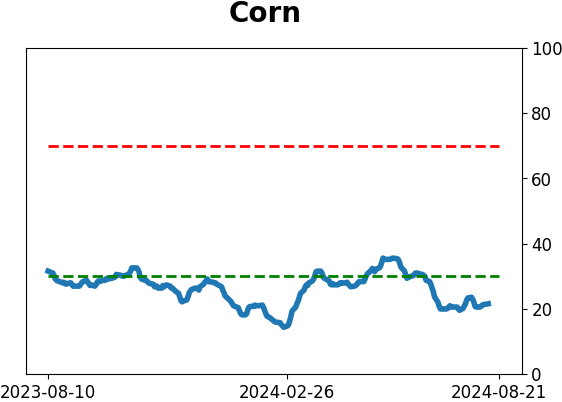

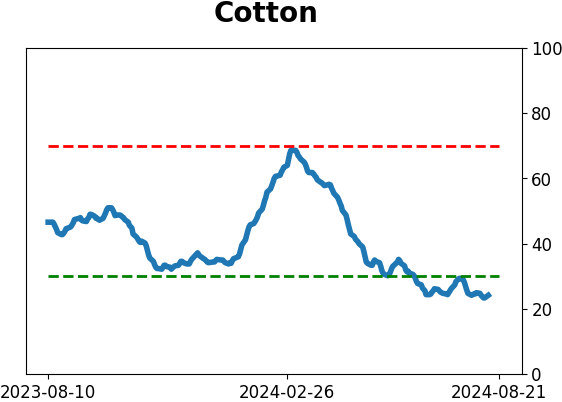

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

The recent rise in volatility triggered bond traders to rush into protection against defaults. The rise in credit default swap prices was enough to push them to 6-month highs. Multi-month highs in CDS prices have augured in some tough markets, particularly for financials.

FORECAST / TIMEFRAME

None

|

Key points:

- The cost to insure against bond defaults spiked to a 6-month high

- Jumps in the prices for credit default swaps have occurred before some major declines

- The most consistently bothersome sector was financials, which showed weak returns after these signals

Paying up for protection

One of the main drivers of the rise in stock prices this year has been loose financial conditions. That's something of a tautology because stock prices are a portion of most financial condition models, but other inputs carry just as much, if not more, weight.

One of those factors is bond spreads. As spreads widen, showing distress, it feeds into tighter financial conditions. Many of those models show tightening conditions, which have preceded more challenging environments for stocks.

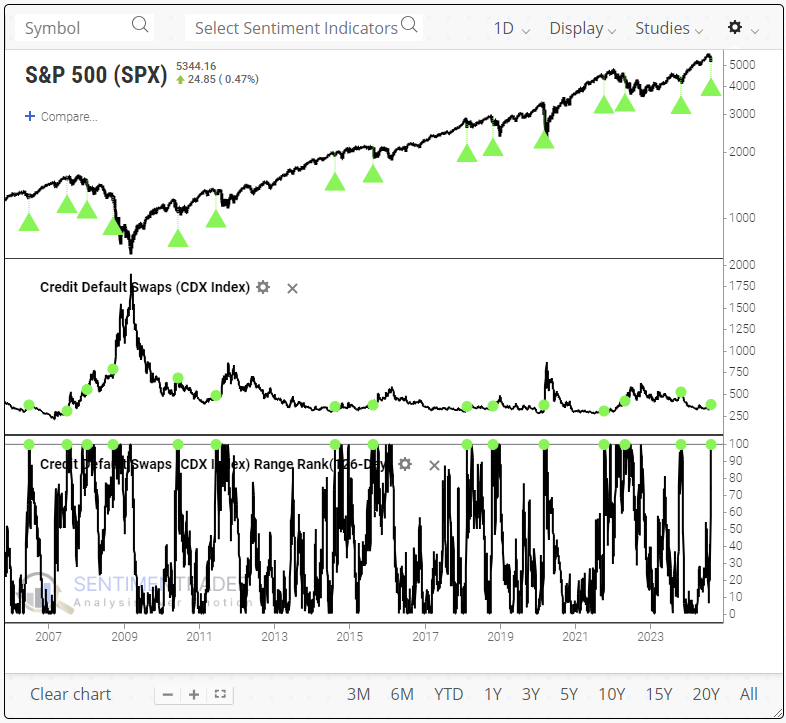

As those concerns rose, traders bought protection against bond defaults. Prices rise when traders scramble for protection, which we can see in the spike in credit default swaps. The chart below shows that the price of CDS protection notched a six-month high last week (100% of its 126-day range) for the 3rd time since the 2021 peak. The first augured the 2022 bear market; the second triggered near the low for stocks in the fall of 2023.

When we zoom out, we can see that these signals have been triggered multiple times over the past couple of decades.

A worry for stocks (especially financials)

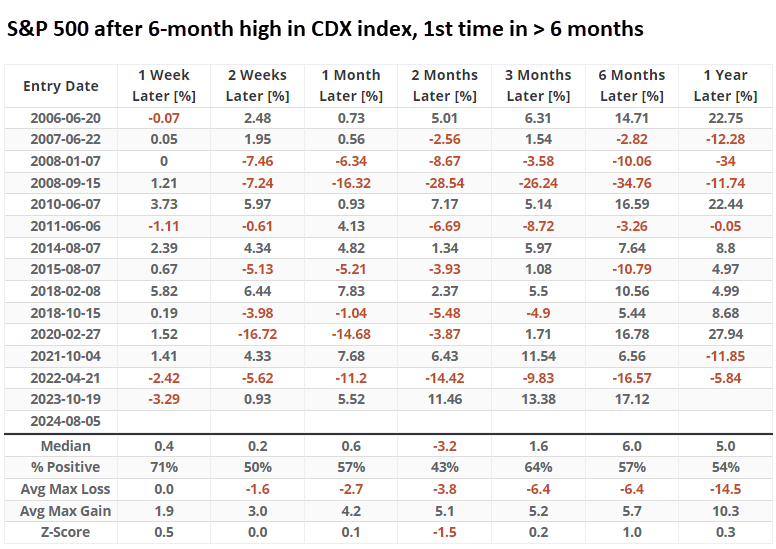

It's hard to tell what these 6-month highs in the cost of CDS protection meant for stocks, so the table below breaks it down. Over the following two months, the S&P 500 was relatively weak, with only a 43% win rate and a negative median return. Even a year later, the average risk outweighed the average reward.

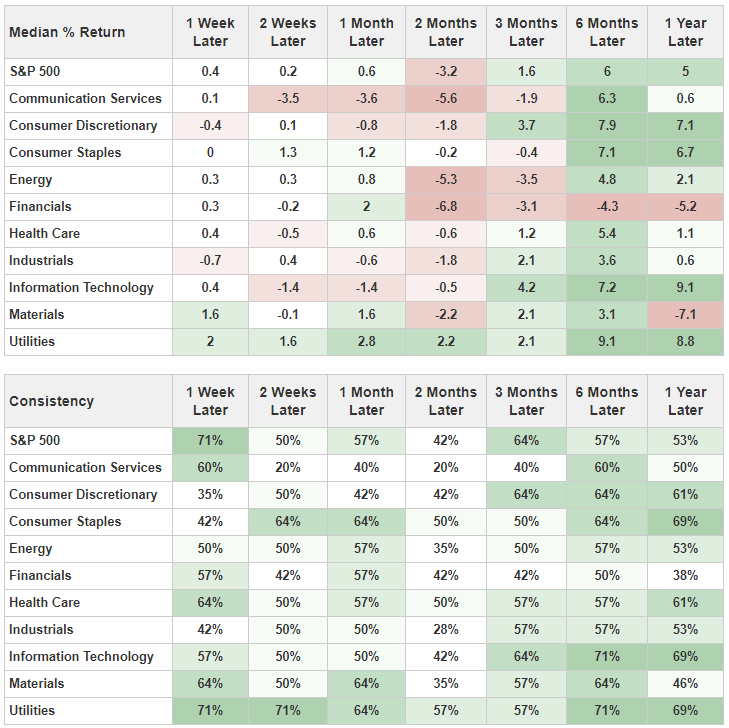

If you use Backtest Engine 2.0 to run this test (click here to load it and then click the Run Backtest button), you can use the Major Sectors tab to see how specific sectors reacted to these jumps in default protection. The next couple of months showed weak returns across the board, except for the defensive utilities sector. Worst of all were the financials, with negative average returns and poor win rates over the medium- to long-term.

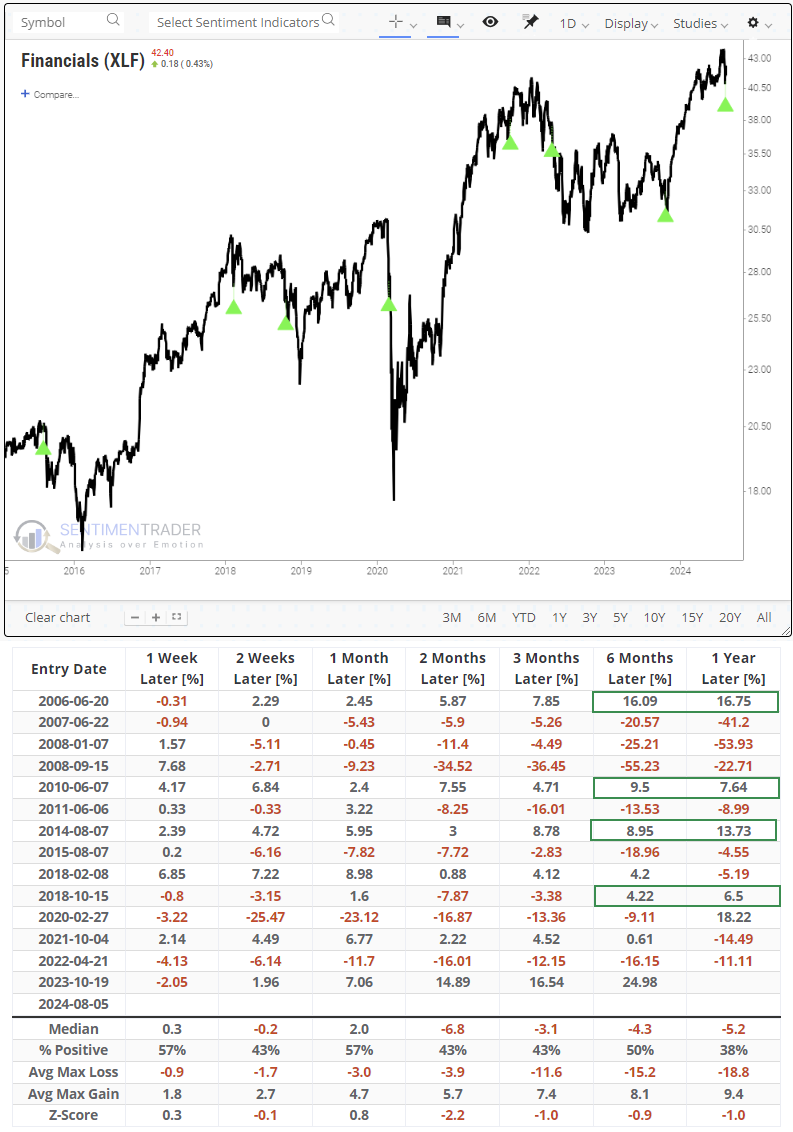

If we go back to the test and see how the XLF fund performed after these signals, we can get a clearer picture of how investors treated these stocks after they grew concerned about rising defaults. The chart below shows that those reactions were not good.

Over the next year, XLF sported a negative return either six or twelve months later after nine signals. It rose over both of those time frames only four times, though that's likely to be five when the last signal from October 2023 is included. Over the next year, the average risk was double the average reward, which is not something we often see.

What the research tells us...

Bull markets need bulls. Investors have to believe that prospects are bright to keep putting money into stocks, and when that sentiment shifts, rallies become much more difficult to sustain. So far, indications are good that investors are still in a buy-the-dip mentality, but it's starting to face its first real test since the panic last week.

The spike in credit default protection prices is a worry, especially if it doesn't recede quickly and substantially. That worry is valid for the broader market but is particularly acute for financials. After other signals, how investors reacted over the first couple of weeks was a decent guide to longer-term returns, so it may pay to watch if buyers are willing to step in right away and use the recent mini-panic as an opportunity to buy rather than an excuse to sell.

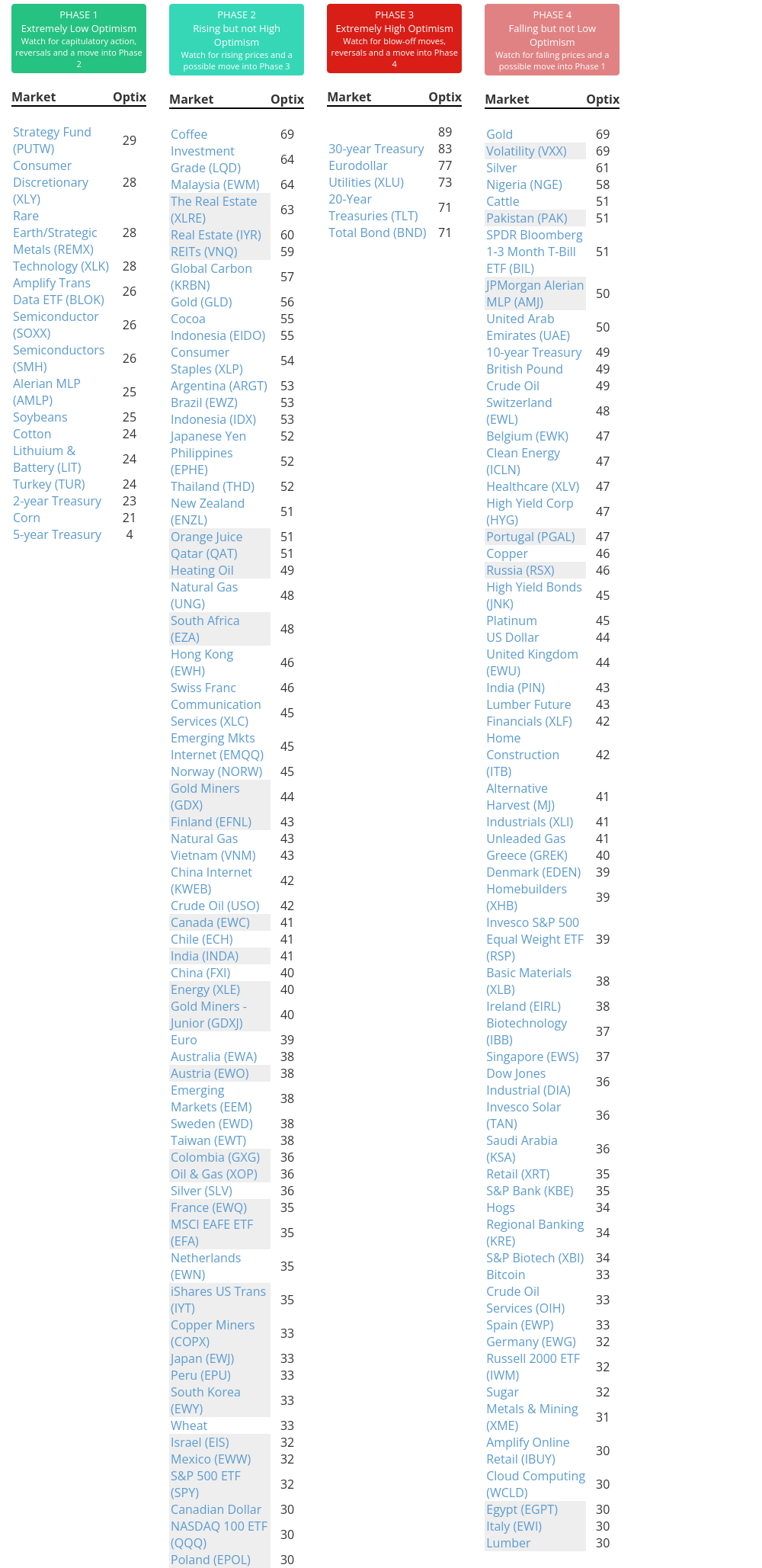

Indicators at Extremes

Phase Table

Ranks

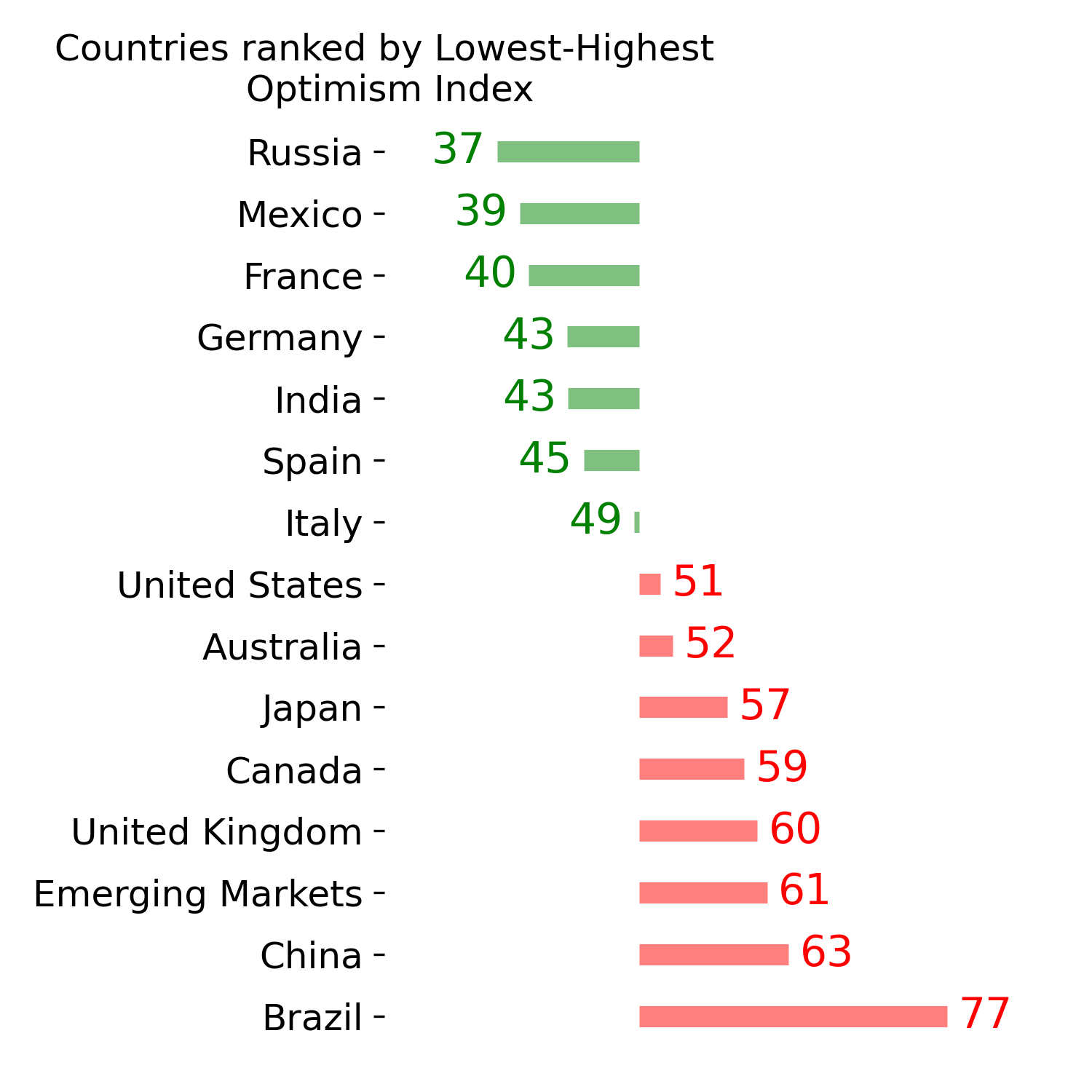

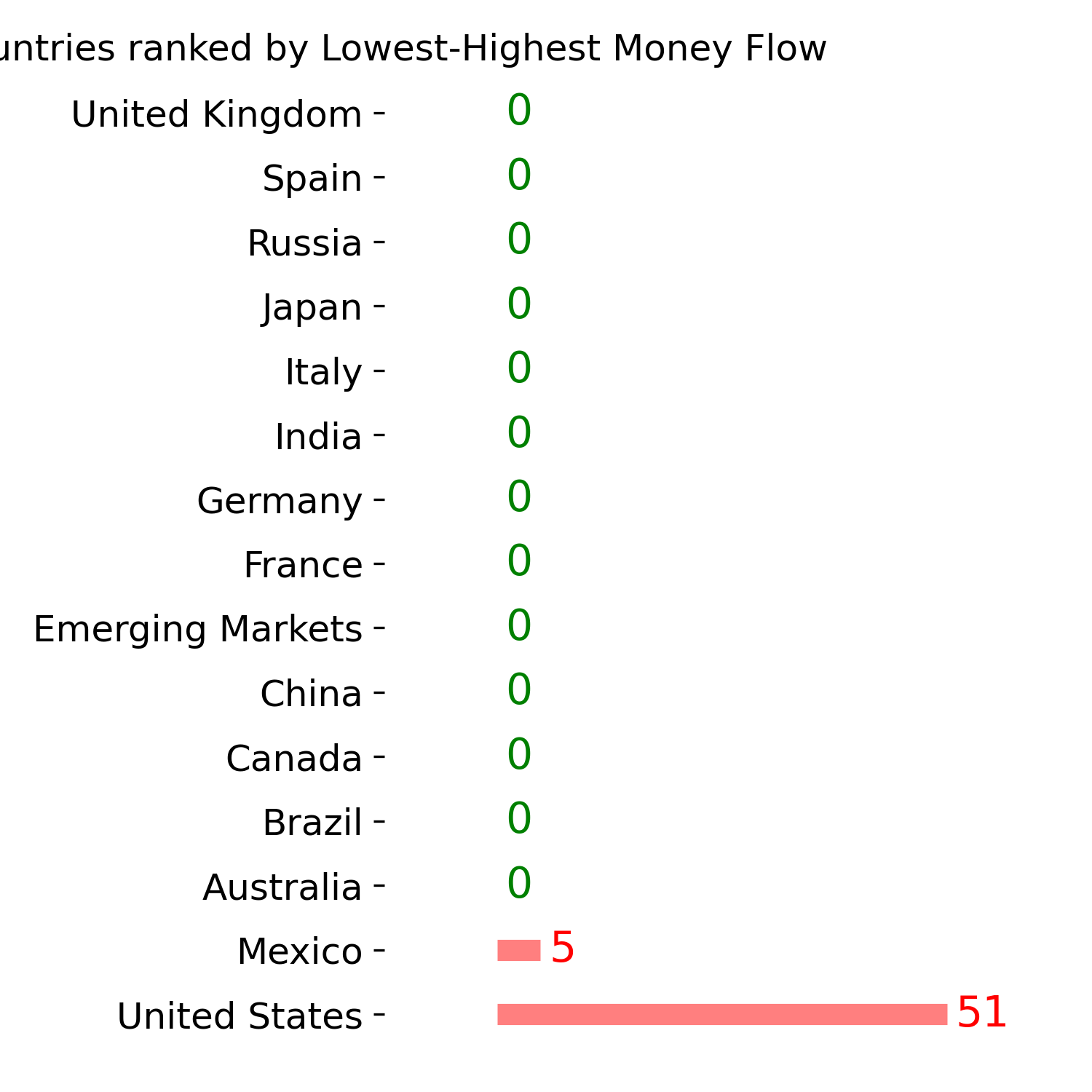

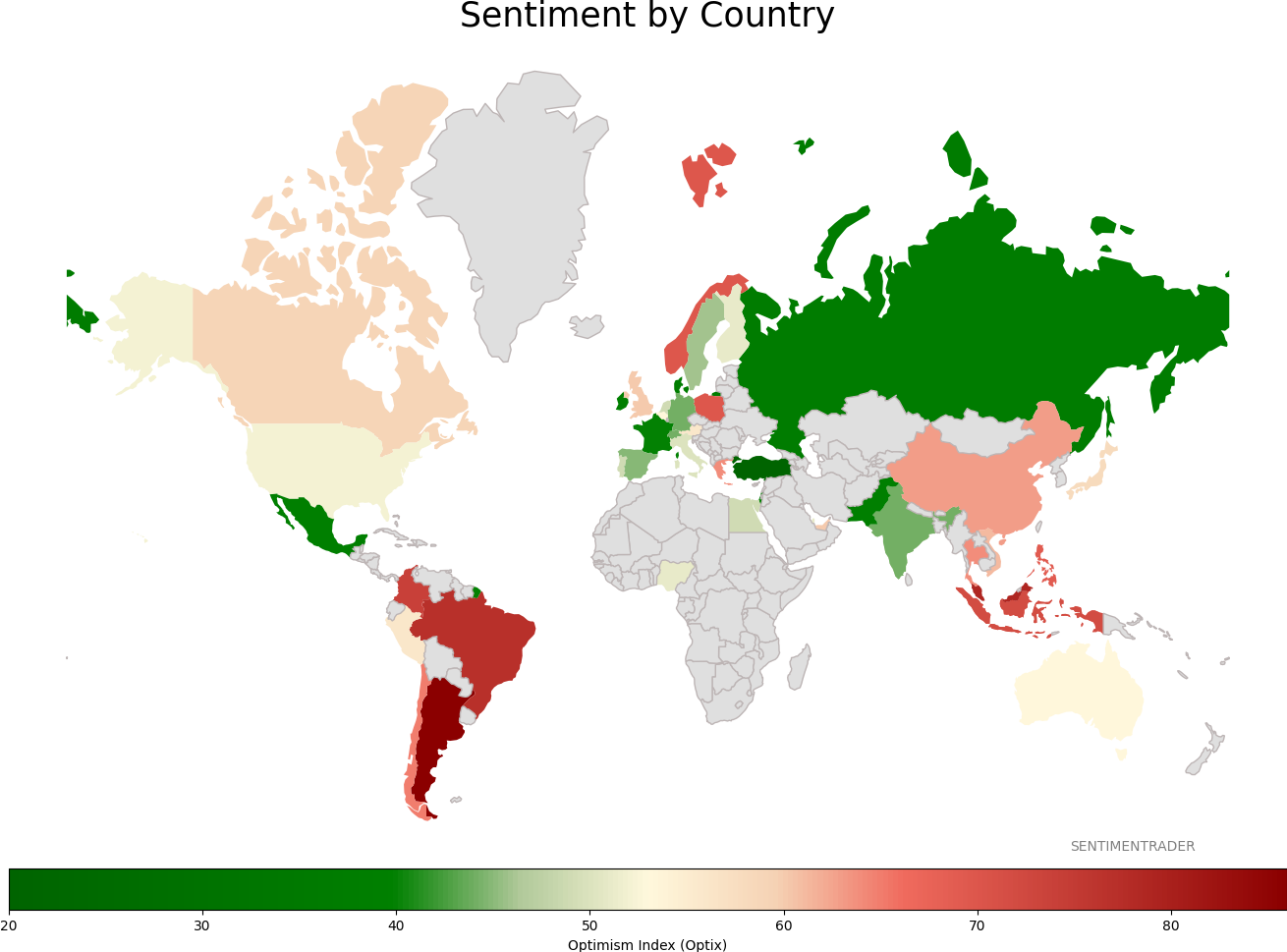

Sentiment Around The World

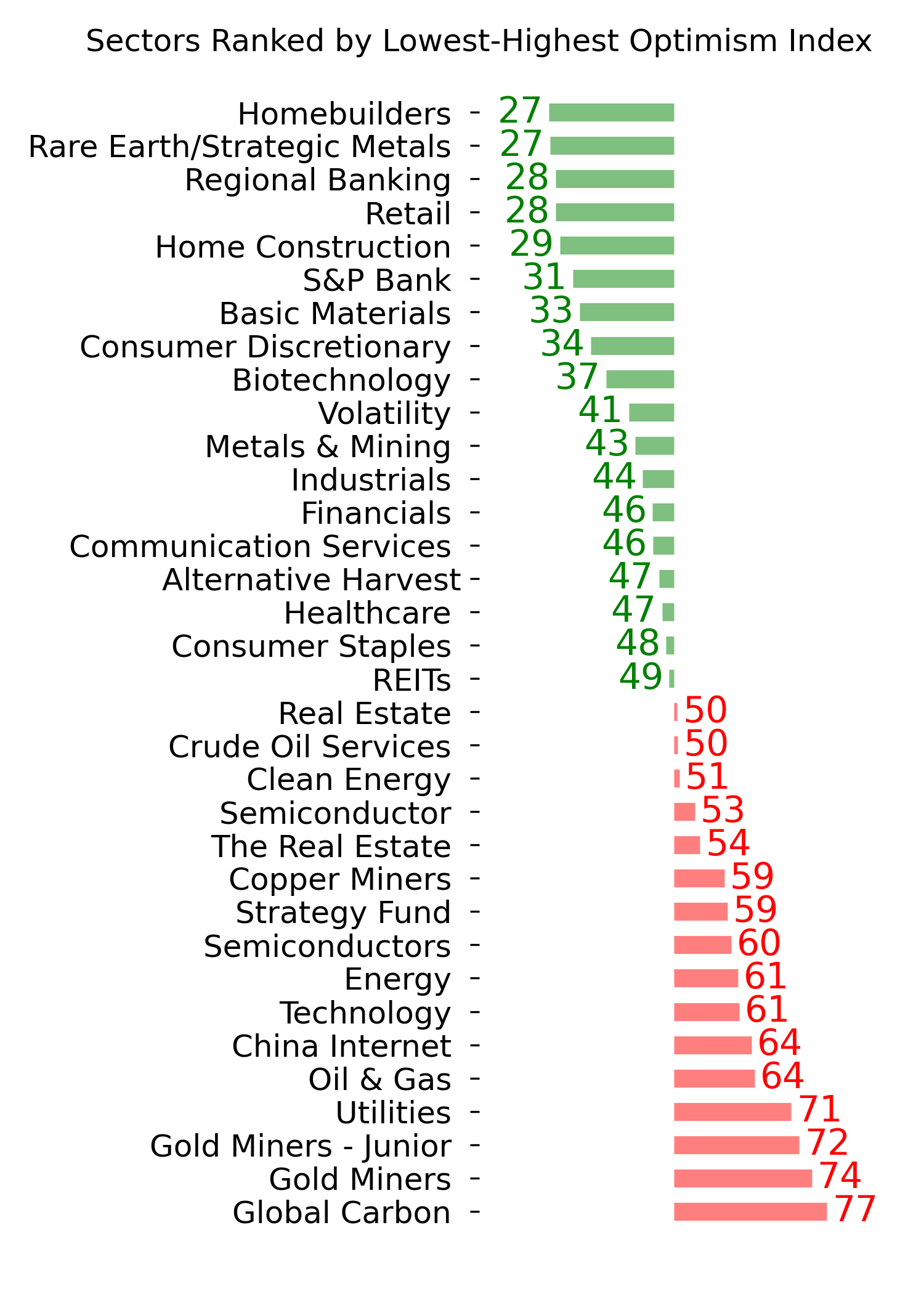

Optimism Index Thumbnails

|

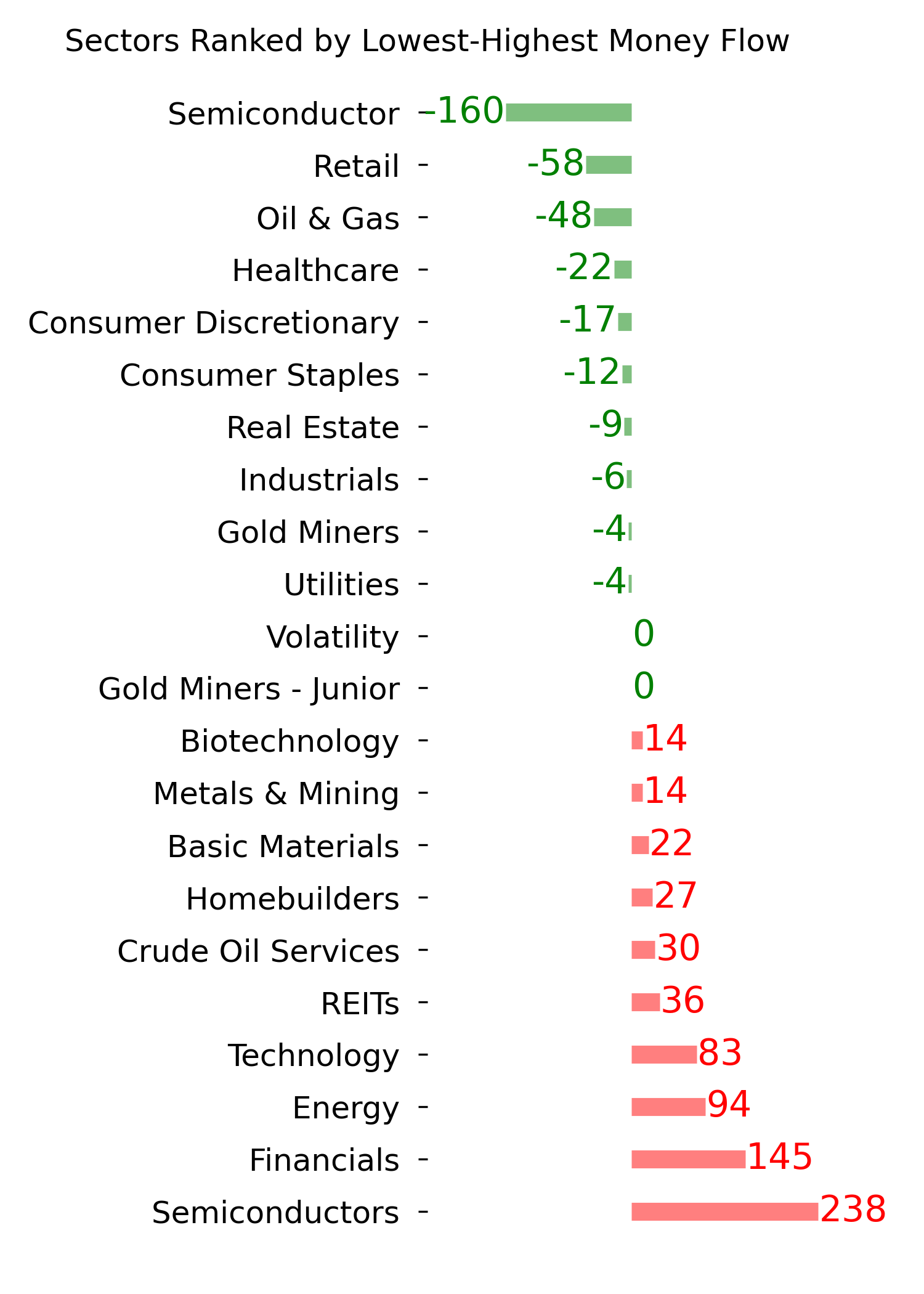

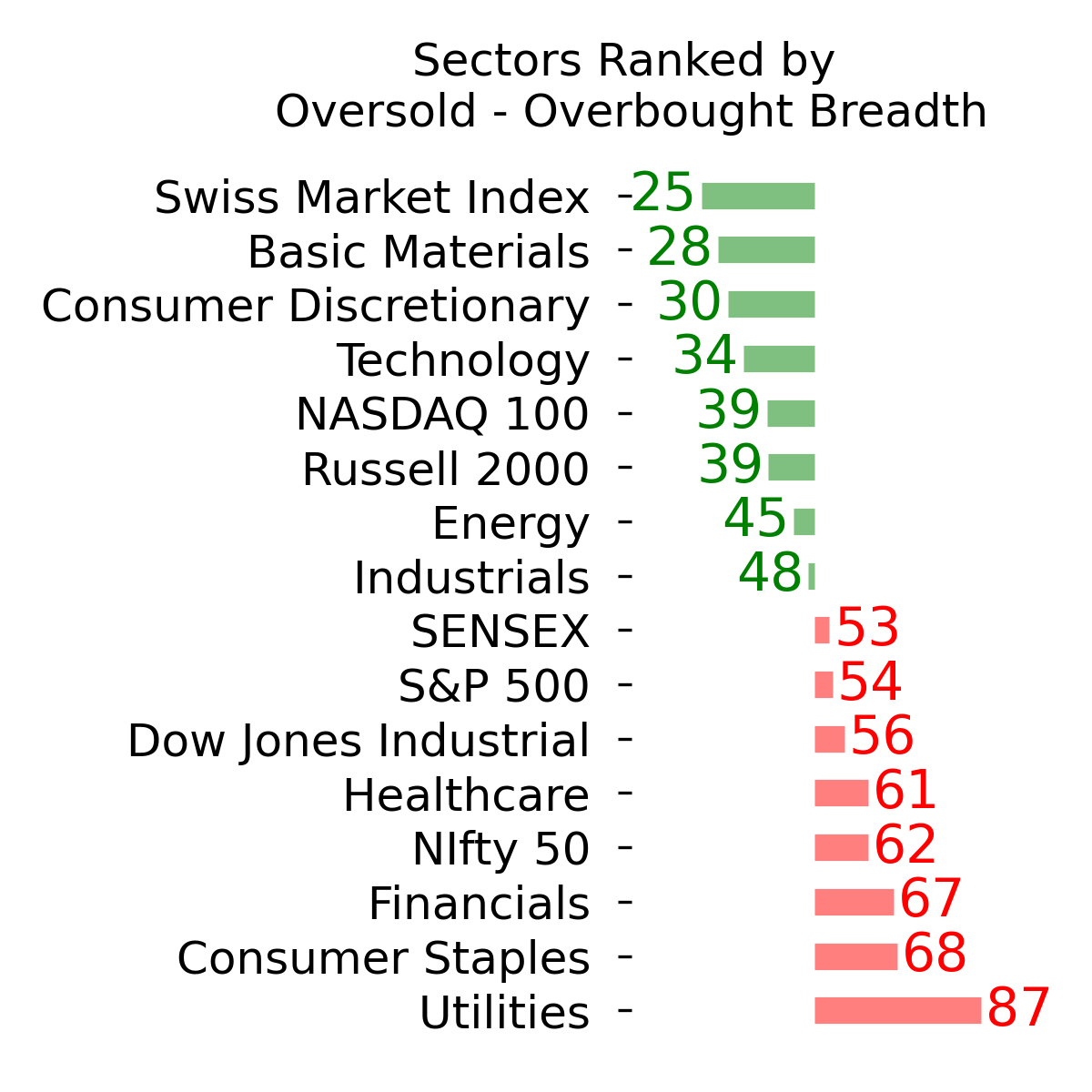

Sector ETF's - 10-Day Moving Average

|

|

|

Country ETF's - 10-Day Moving Average

|

|

|

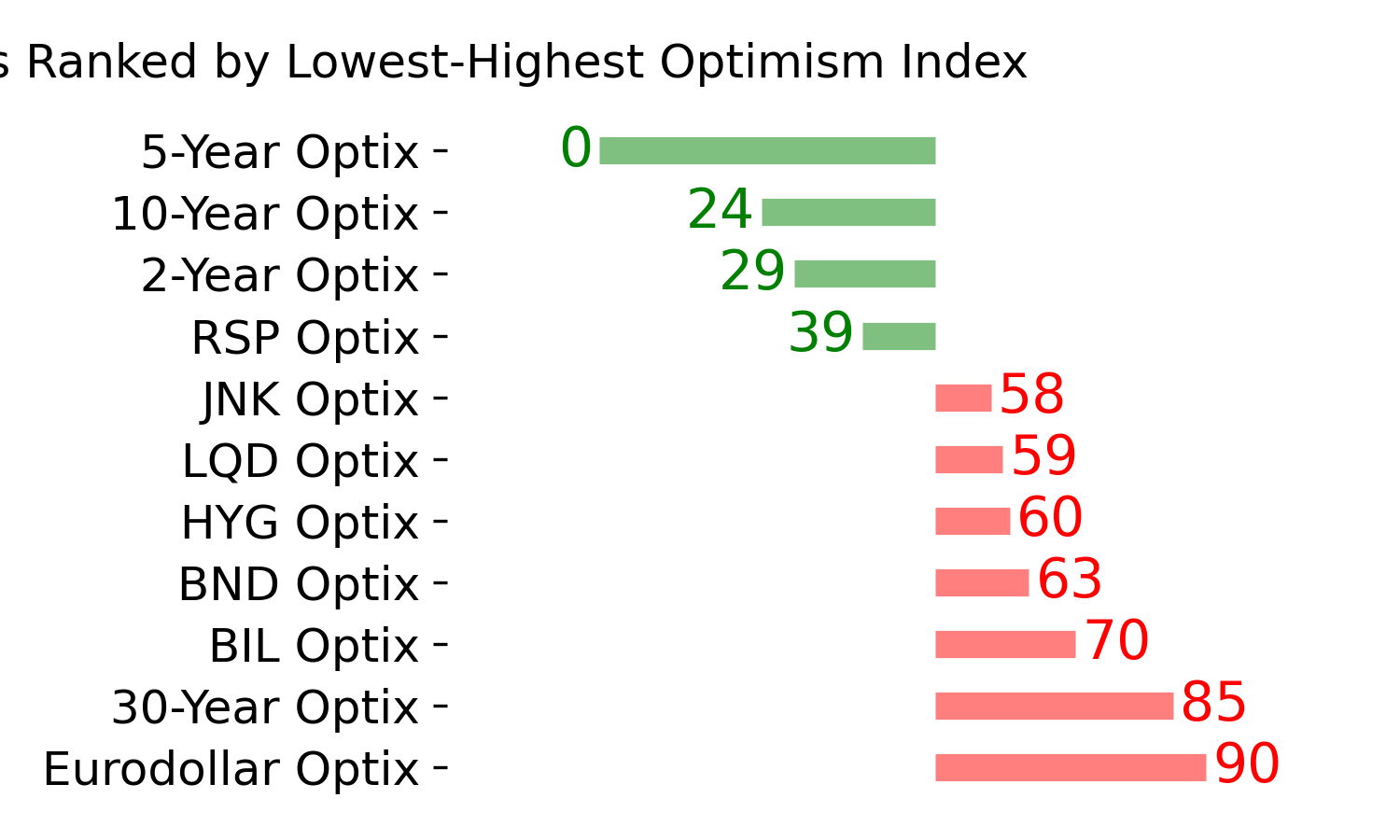

Bond ETF's - 10-Day Moving Average

|

|

|

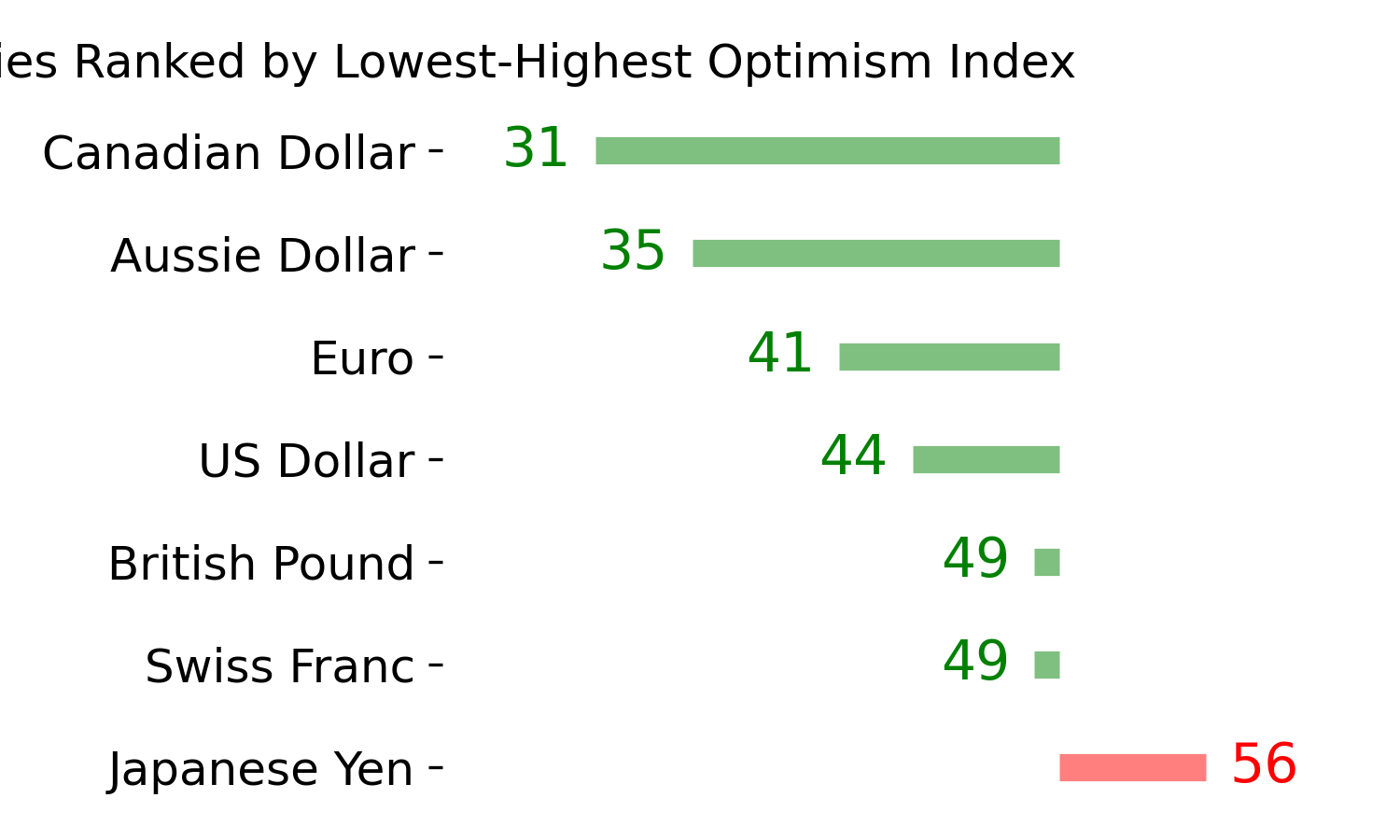

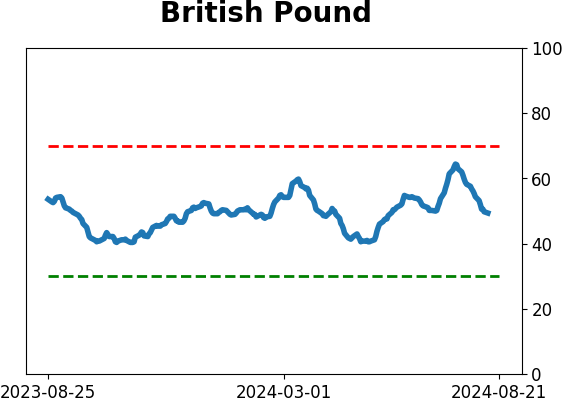

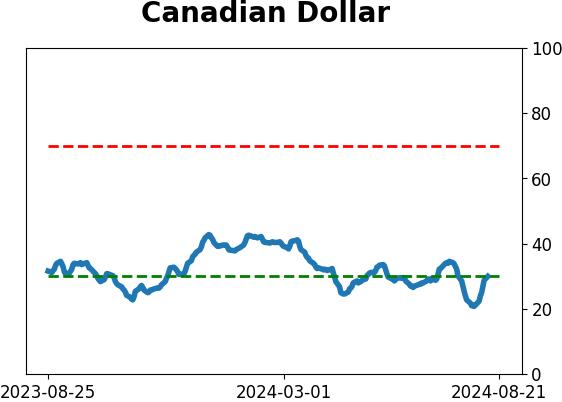

Currency ETF's - 5-Day Moving Average

|

|

|

Commodity ETF's - 5-Day Moving Average

|

|