Headlines

|

|

High valuations and competing investments as fall looms:

Valuations have jumped. Investors have viable alternatives to stocks from ultra-safe Treasuries. All as we head into the volatile September and October time frame. Similar setups preceded weak short-term returns for the S&P 500.

|

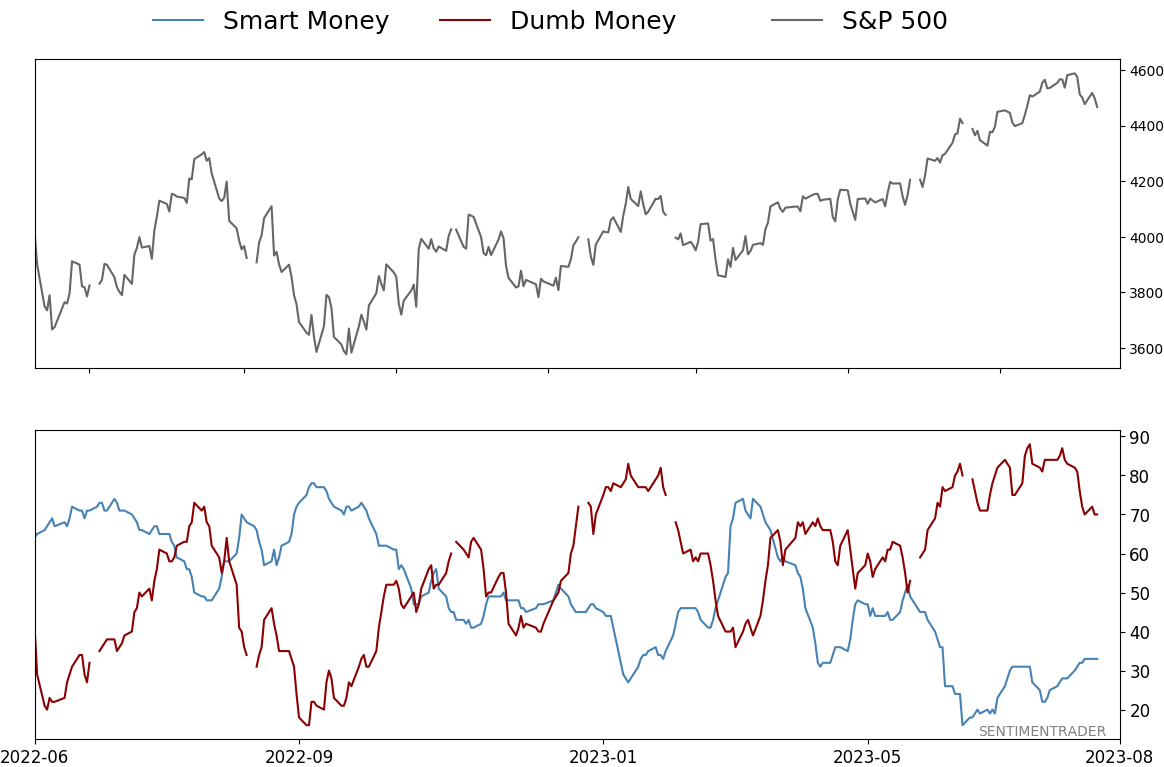

Smart / Dumb Money Confidence

|

Smart Money Confidence: 33%

Dumb Money Confidence: 70%

|

|

Risk Levels

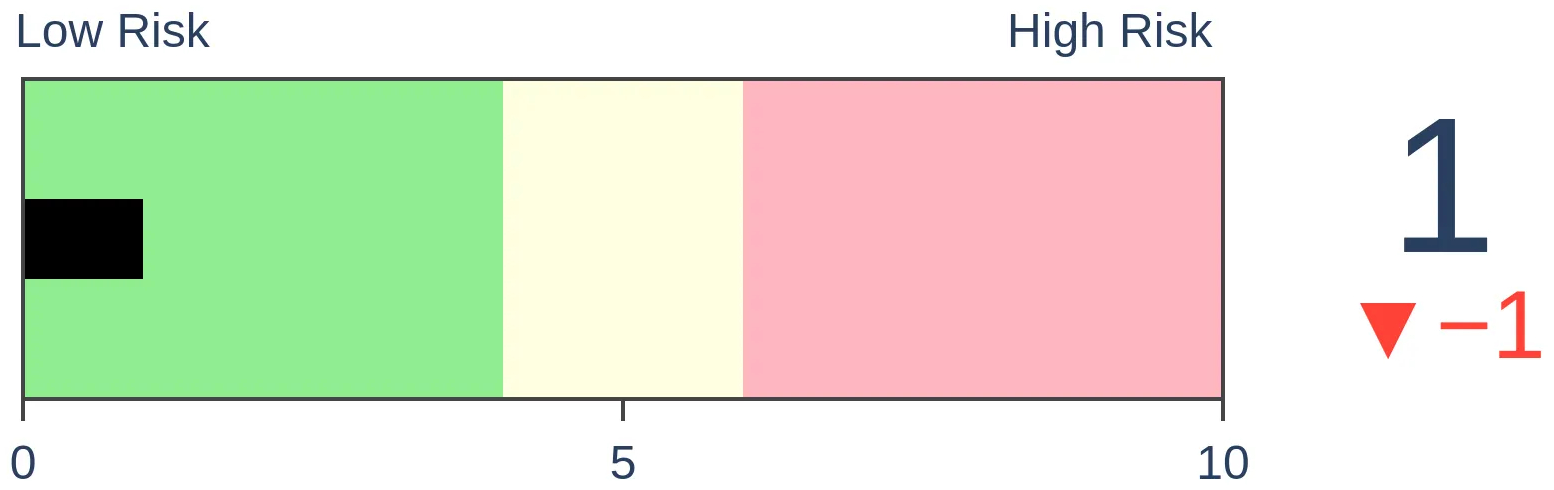

Stocks Short-Term

|

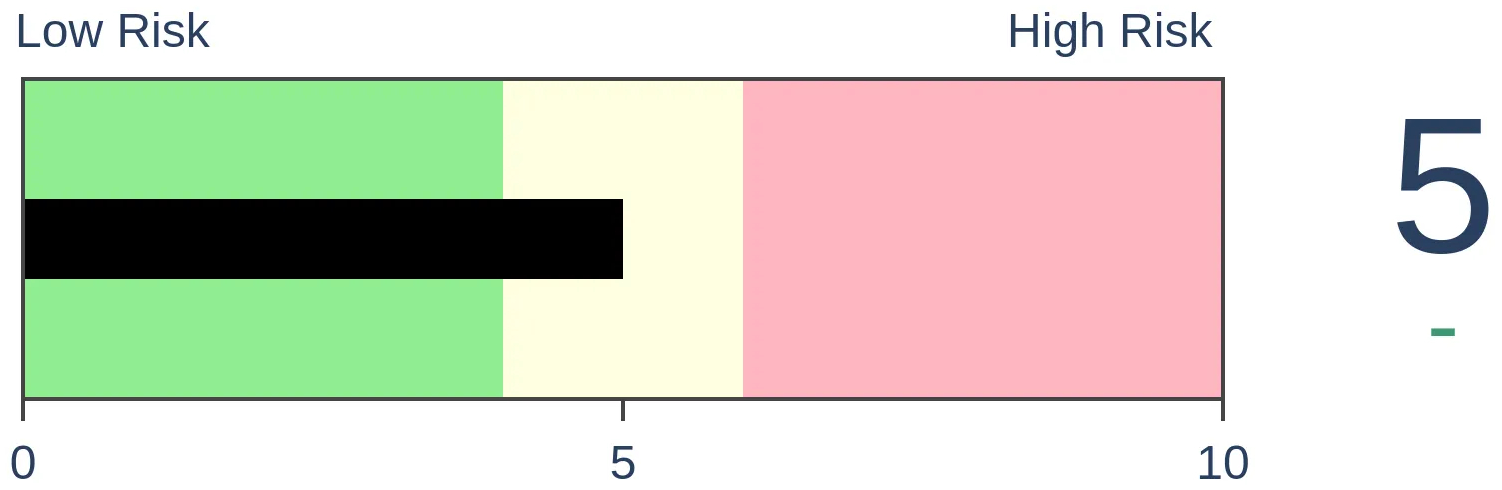

Stocks Medium-Term

|

|

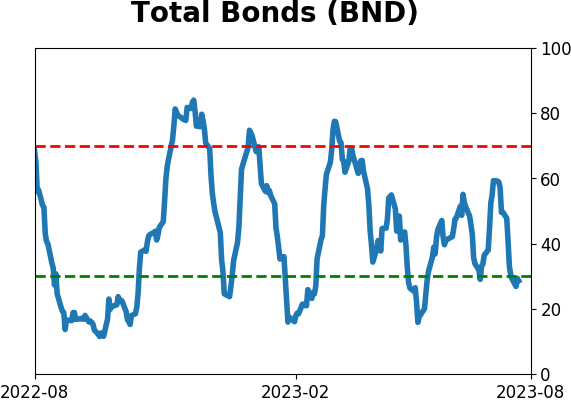

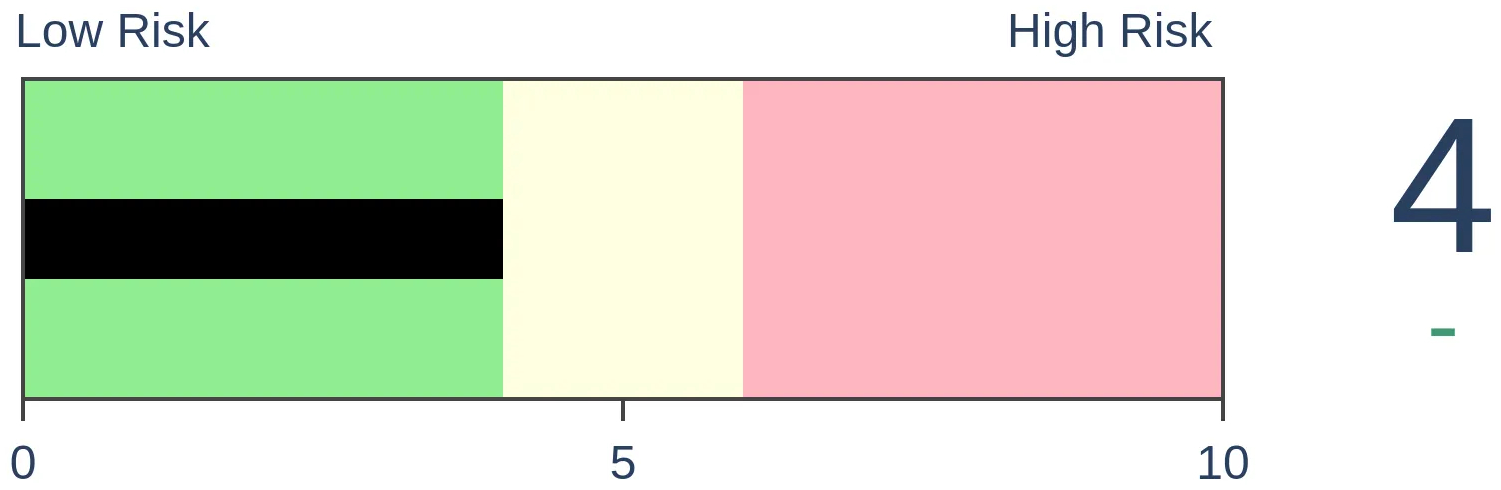

Bonds

|

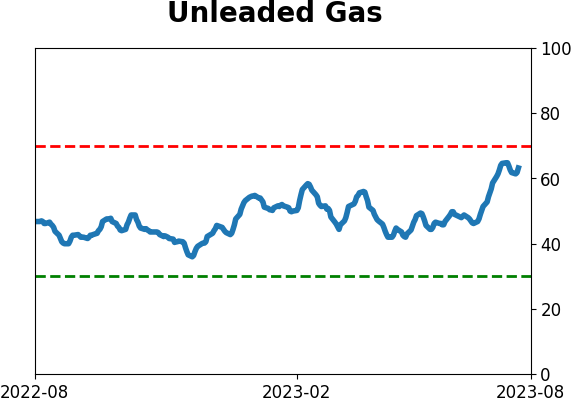

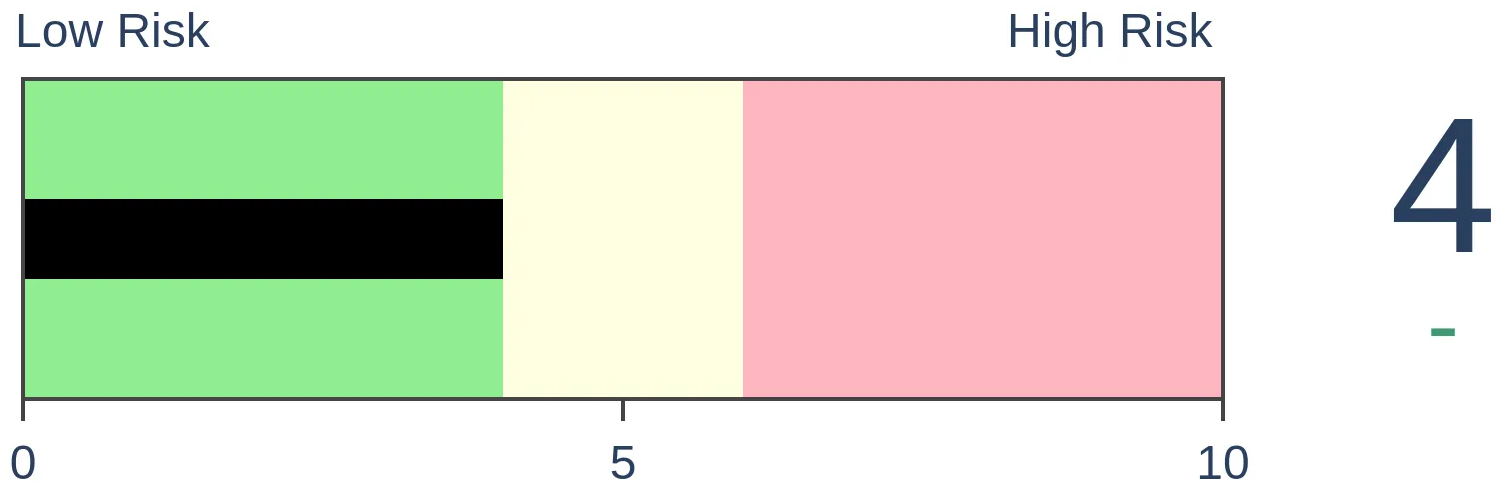

Crude Oil

|

|

Gold

|

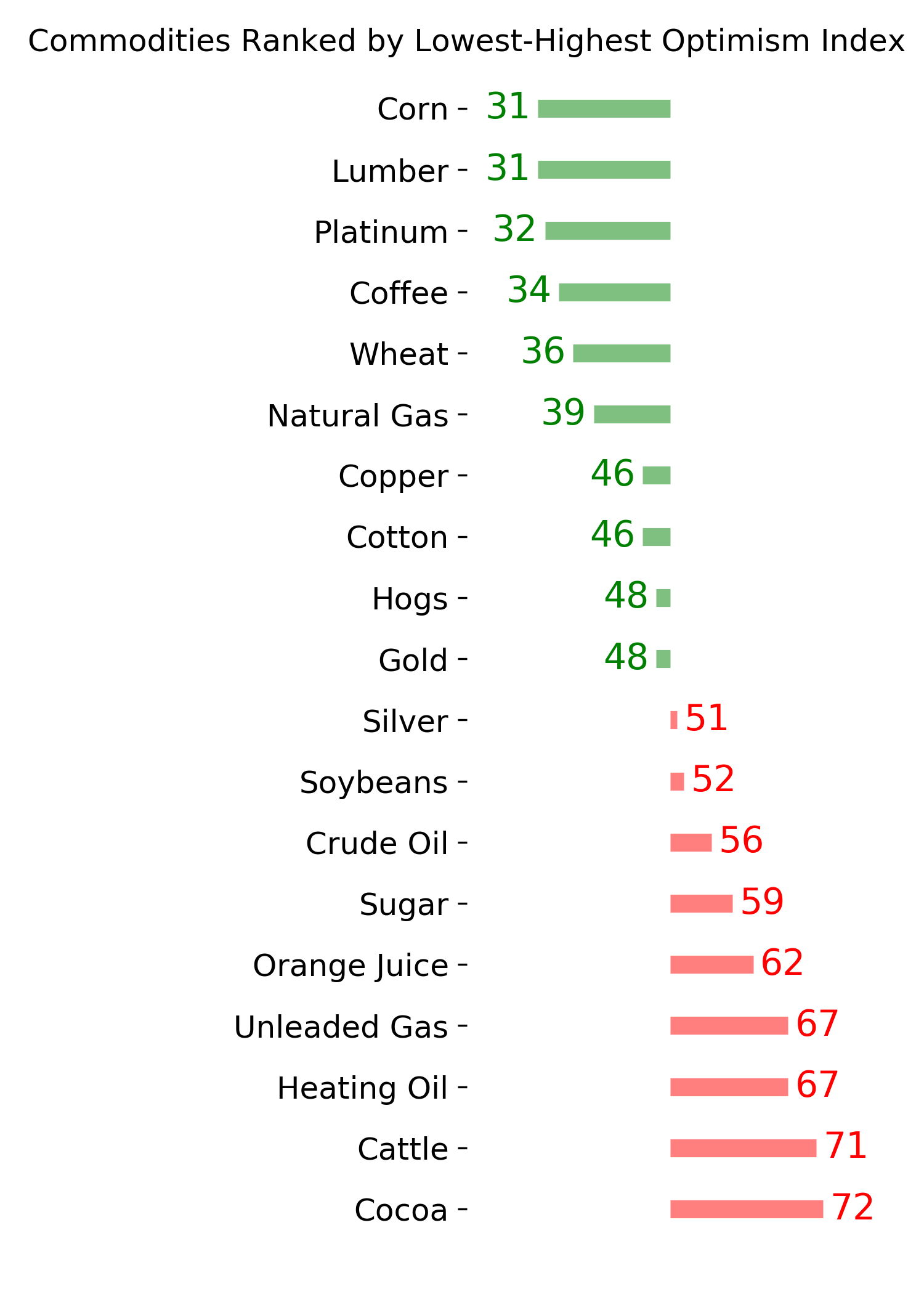

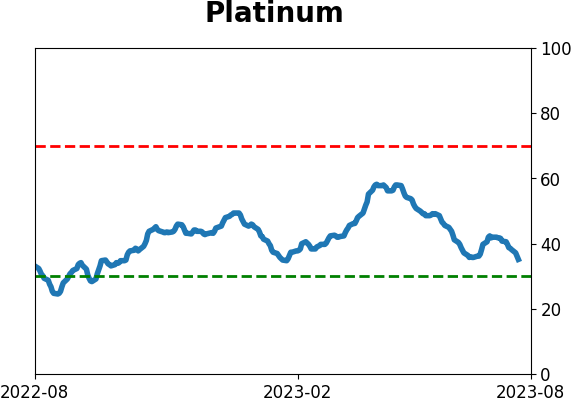

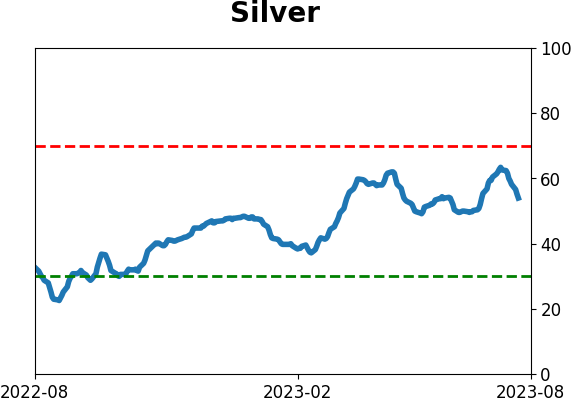

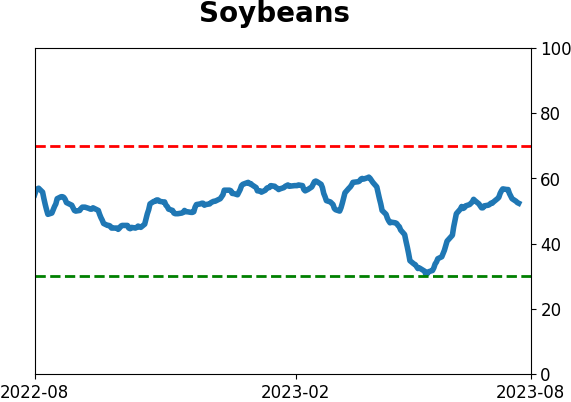

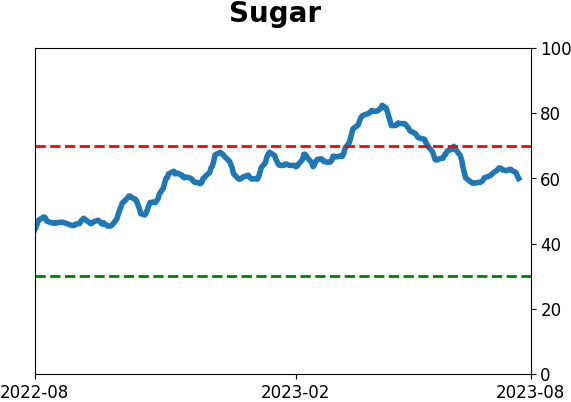

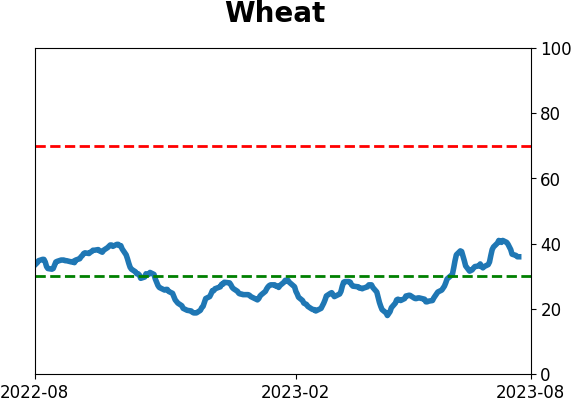

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

Valuations have jumped. Investors have viable alternatives to stocks from ultra-safe Treasuries. All as we head into the volatile September and October time frame. Similar setups preceded weak short-term returns for the S&P 500.

FORECAST / TIMEFRAME

None

|

Key points:

- As we head into the oft-volatile September/October period, valuations and competing yields have jumped

- Similar setups preceded weak short-term returns for the S&P 500

- The opposite scenarios preceded above-average returns, lending some credence to the warnings

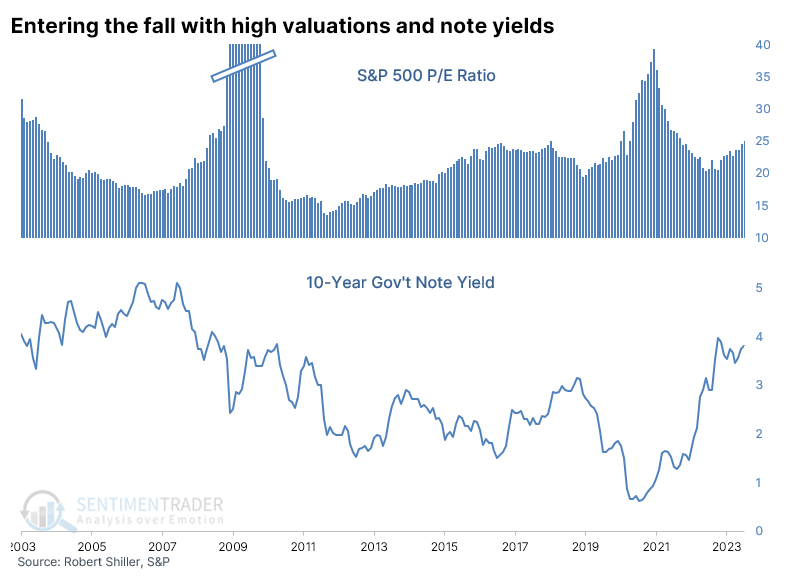

Valuations have jumped, as have fixed income yields, as we enter the fall

We saw yesterday that stocks are on track to have three consecutive quarterly earnings declines. Because prices have held up and earnings have declined, the widely-watched price/earnings valuation measure has increased. That's happened even though bond prices have declined, so investors have a reasonable alternative in ultra-safe Treasuries-all this as we careen toward the oft-cited volatility of September and October.

The Wall Street Journal notes:

September is traditionally the weakest month for U.S. stocks. This year, investors say the turning of the calendar should be especially worrying.[] But there are warning signs that this year's rally could lose steam. Valuations are above their recent norms, with the S&P 500 trading at around 19 times forward earnings estimates, according to FactSet. The one-year average is 17.7 times. Inflated valuations alone don't cause stocks to drop, but they can make a decline more severe. Meanwhile, the 10-year Treasury yield is at its highest level in nearly a year, making it less attractive to hold stocks instead of bonds.

There is little debating the facts: 1) September has been historically weak for stocks, 2) valuation measures are on the upper ends of their ranges, and 3) rising bond yields offer a reasonable alternative for investors.

Whether those factors have mattered is the question, so let's check it out.

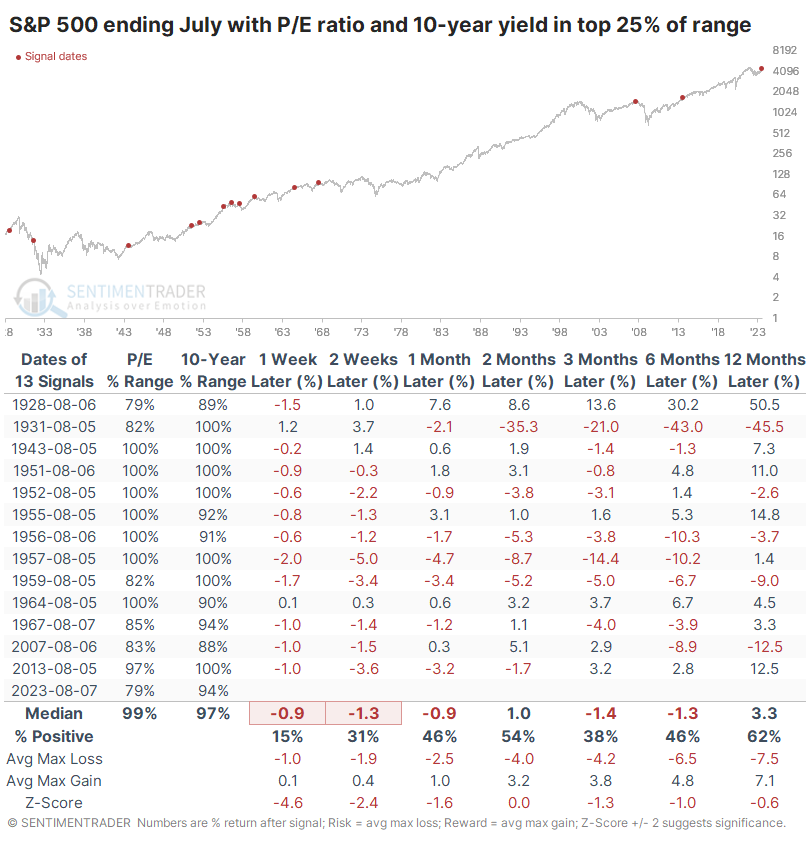

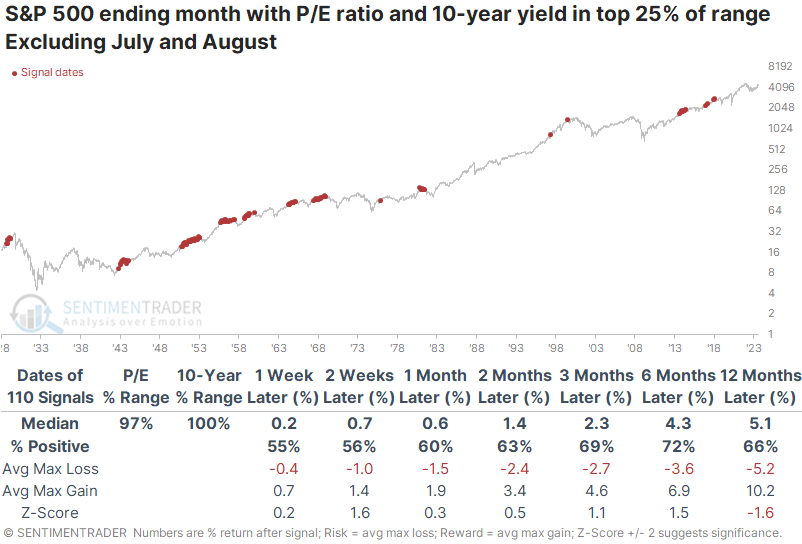

High valuations + Rising Yields + Weak Seasonality = Trouble

The table below shows when we ended July with the S&P's P/E ratio in the top 25% of its 2-year range. The yield on 10-year Treasuries also needed to be in the top 25% of its range. We added a week to month-end to better equate with our current situation.

There was some reason to worry. After other late summers with high valuations and note yields, the S&P struggled during August and into September. Even its three- and six-month returns were lacking. Its average return underperformed a random return across all time frames.

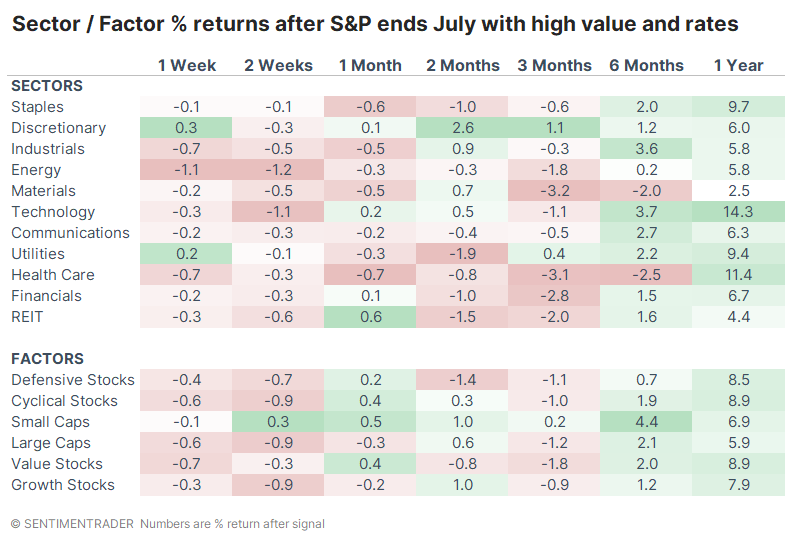

Across sectors and factors, there weren't many places to hide, especially during August. Small-caps held up the best, but oddly, the Defensive factor and sectors didn't provide much solace.

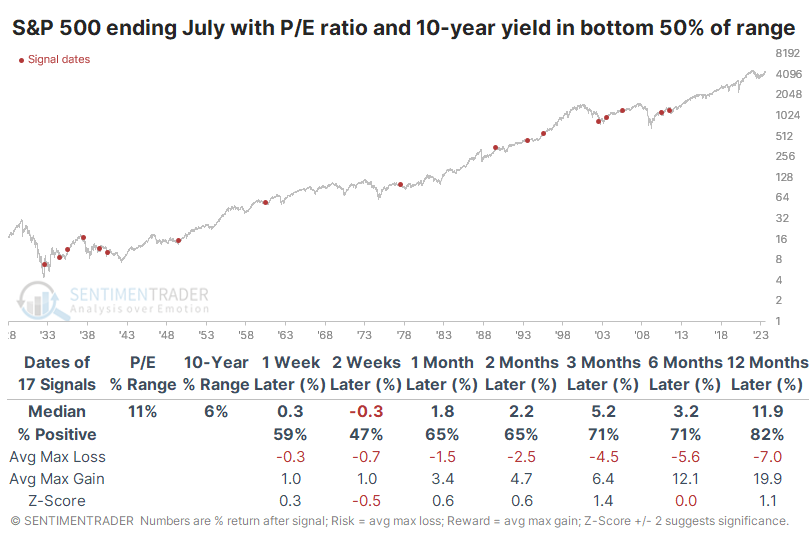

To have more confidence in the idea that high valuations and competing yields at the end of July is a reason to worry, two other things should be true:

- Low valuations and yields should lead to better returns

- High valuations and yields in other months should lead to better returns

Below, we can see that both of those things are true. When the S&P ended July with valuations and yields in the bottom half of their 2-year ranges, its returns in the months ahead were pretty good. The next couple of weeks were still weak, but not like the above.

When the S&P ended months other than July (or August) with high valuations and yields, its returns in the weeks and months ahead were fine and mostly above average.

What the research tells us...

High valuations alone are not very predictive of future returns. Neither are high bond yields. And seasonality isn't all that reliable, either. But when we combine the three factors, stock prices have struggled in the short term as we head into the late summer and early fall. Even medium-term returns have been weak, though we have less confidence in that as a predictor. Still, it's one of the rare warnings in the mainstream media that has some empirical support over the past 95 years.

Indicators at Extremes

Phase Table

Ranks

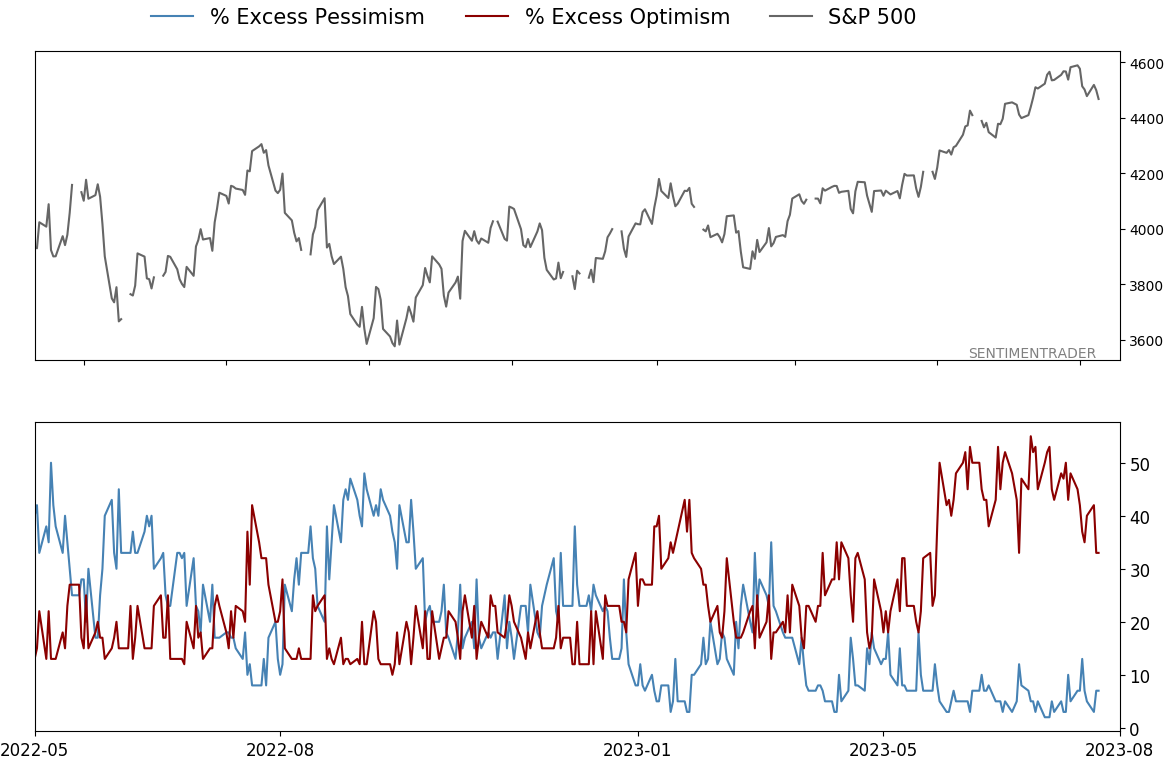

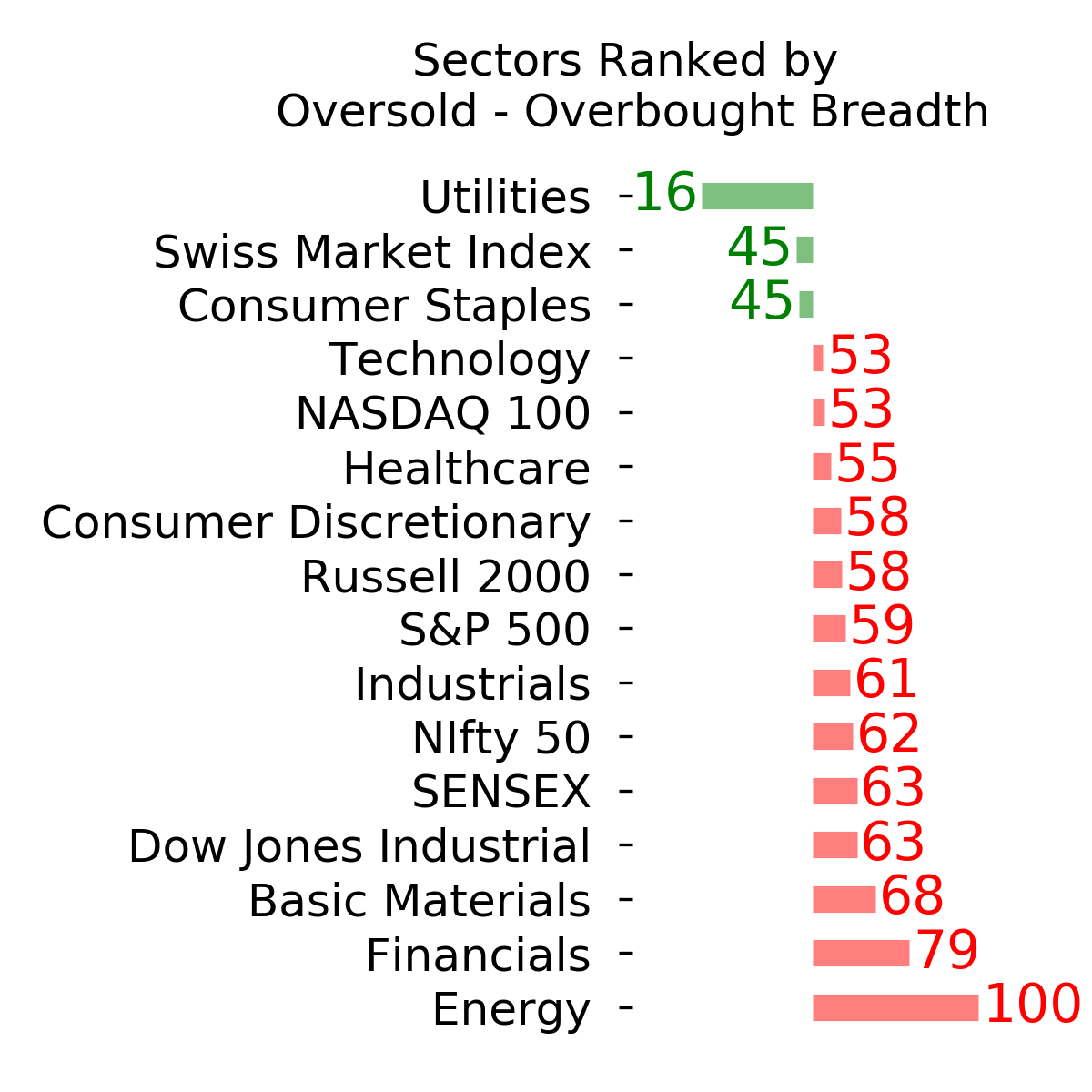

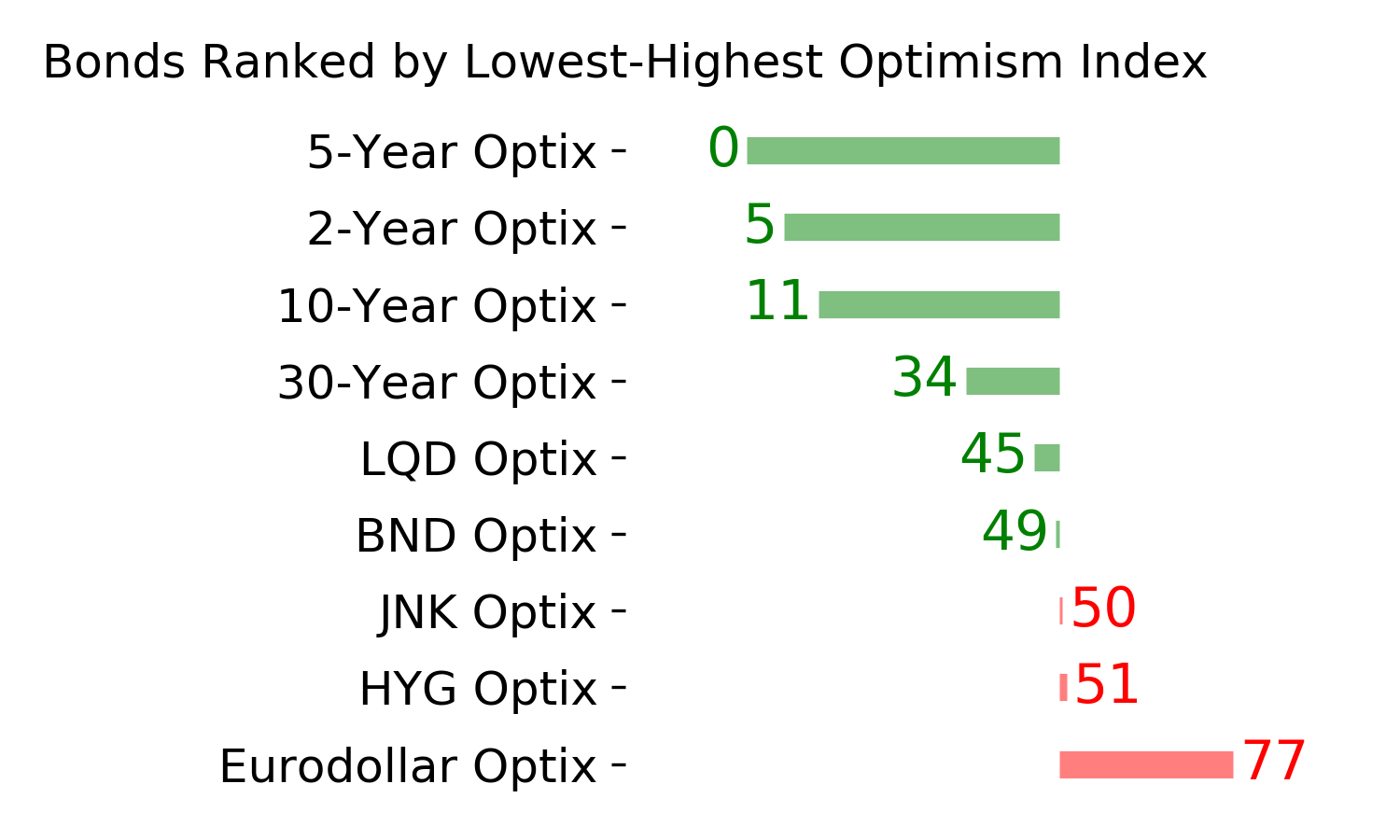

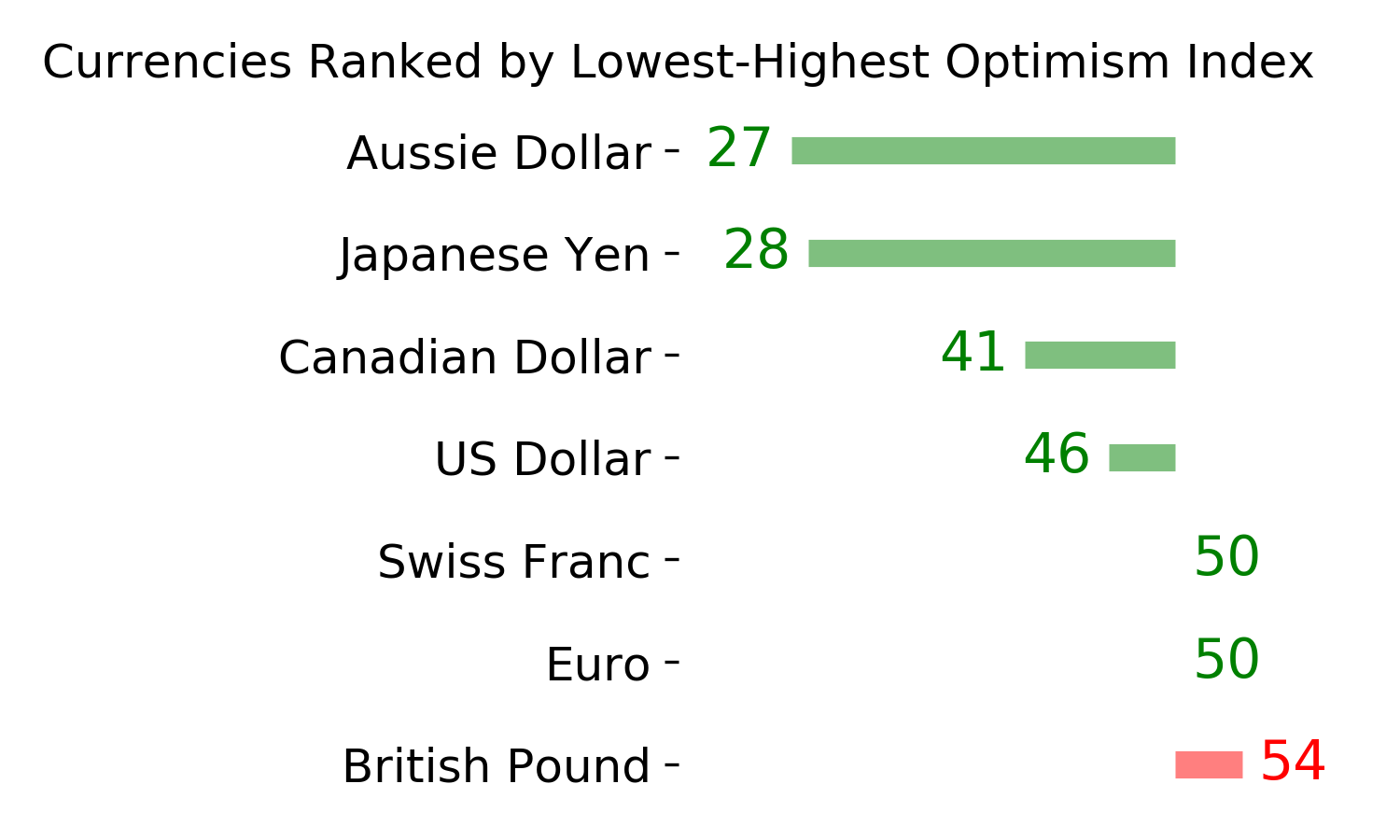

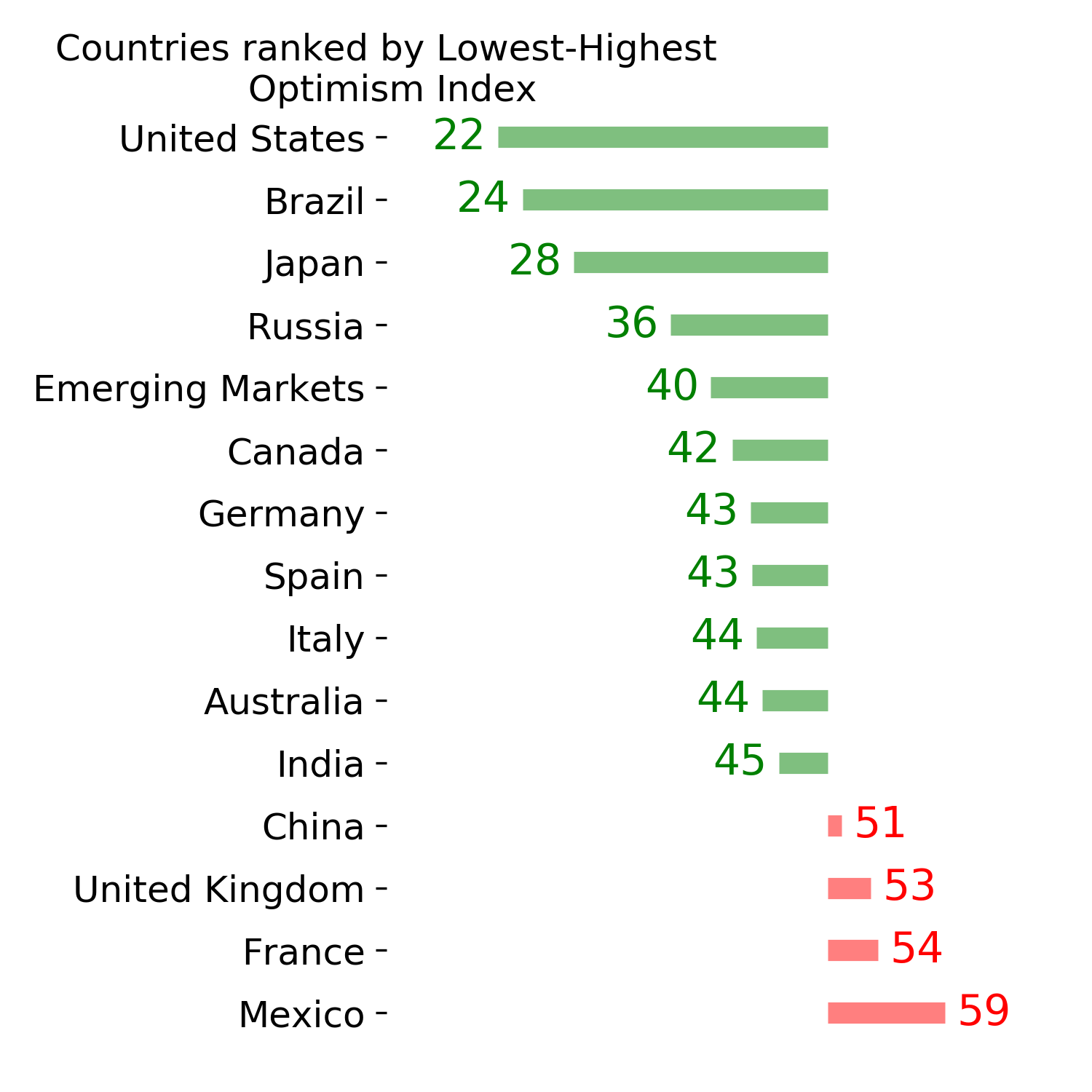

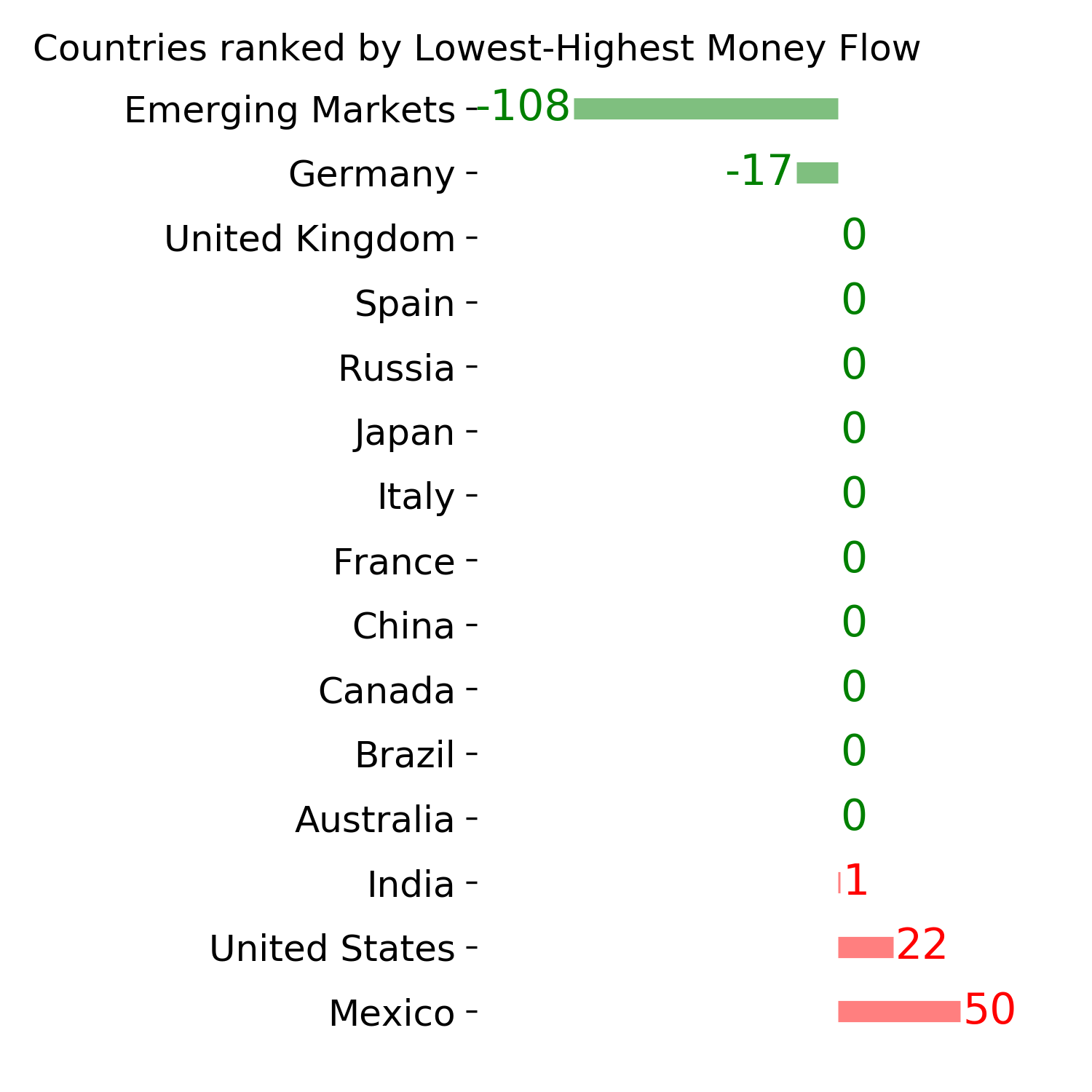

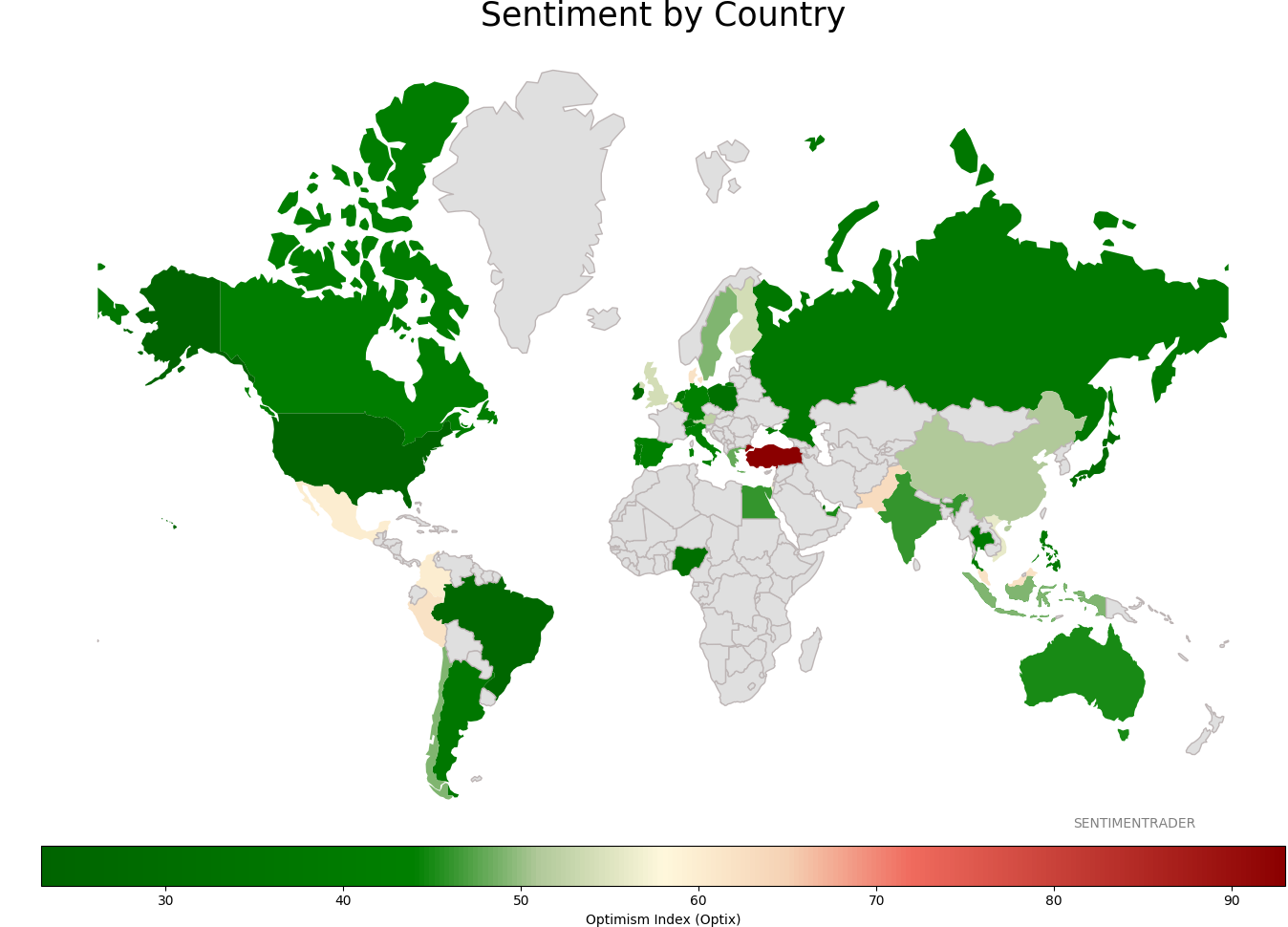

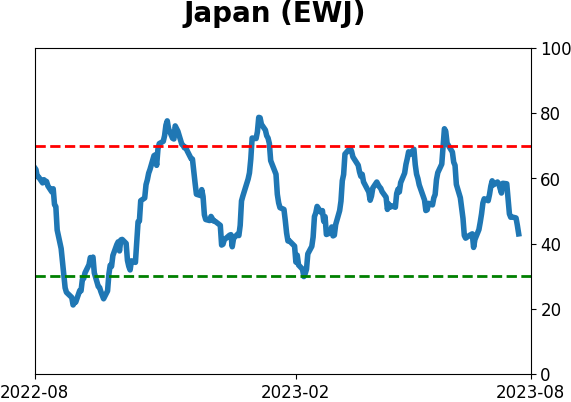

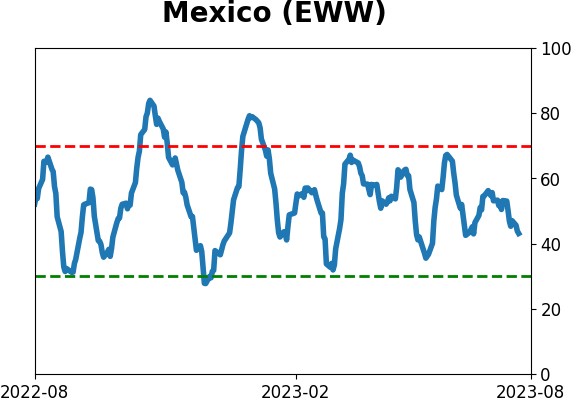

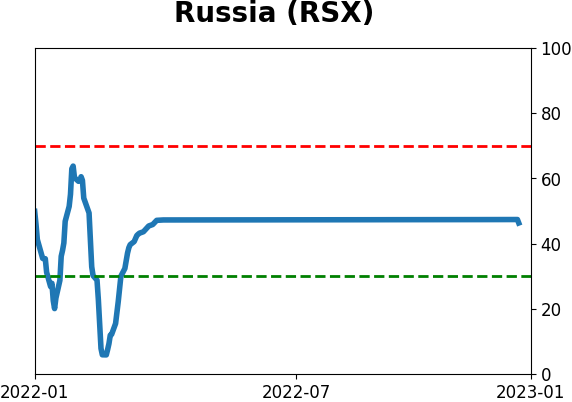

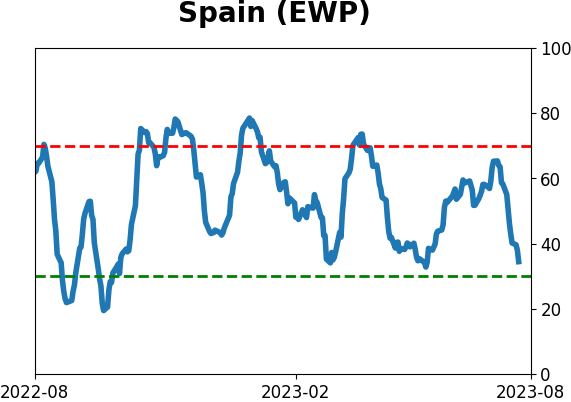

Sentiment Around The World

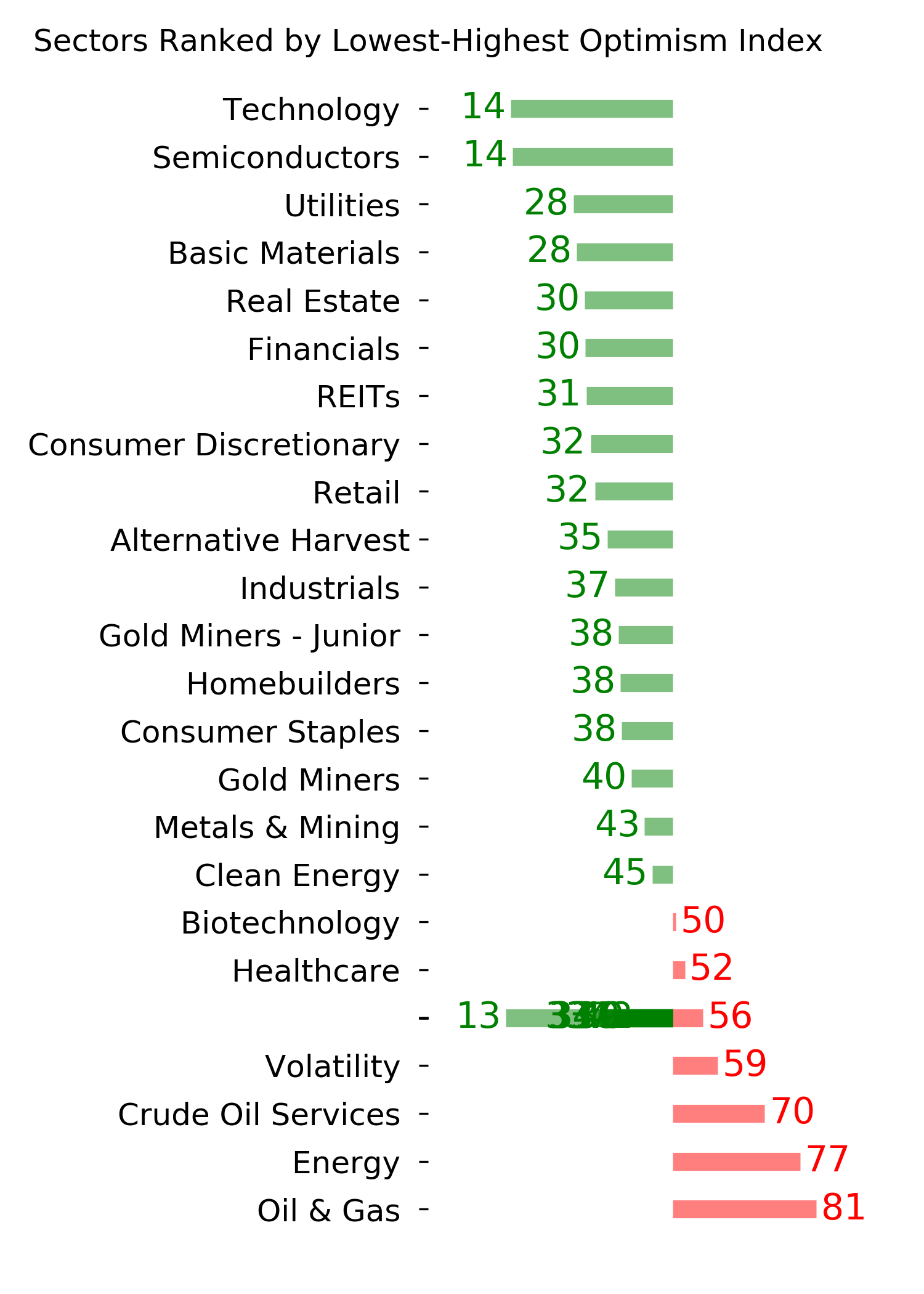

Optimism Index Thumbnails

|

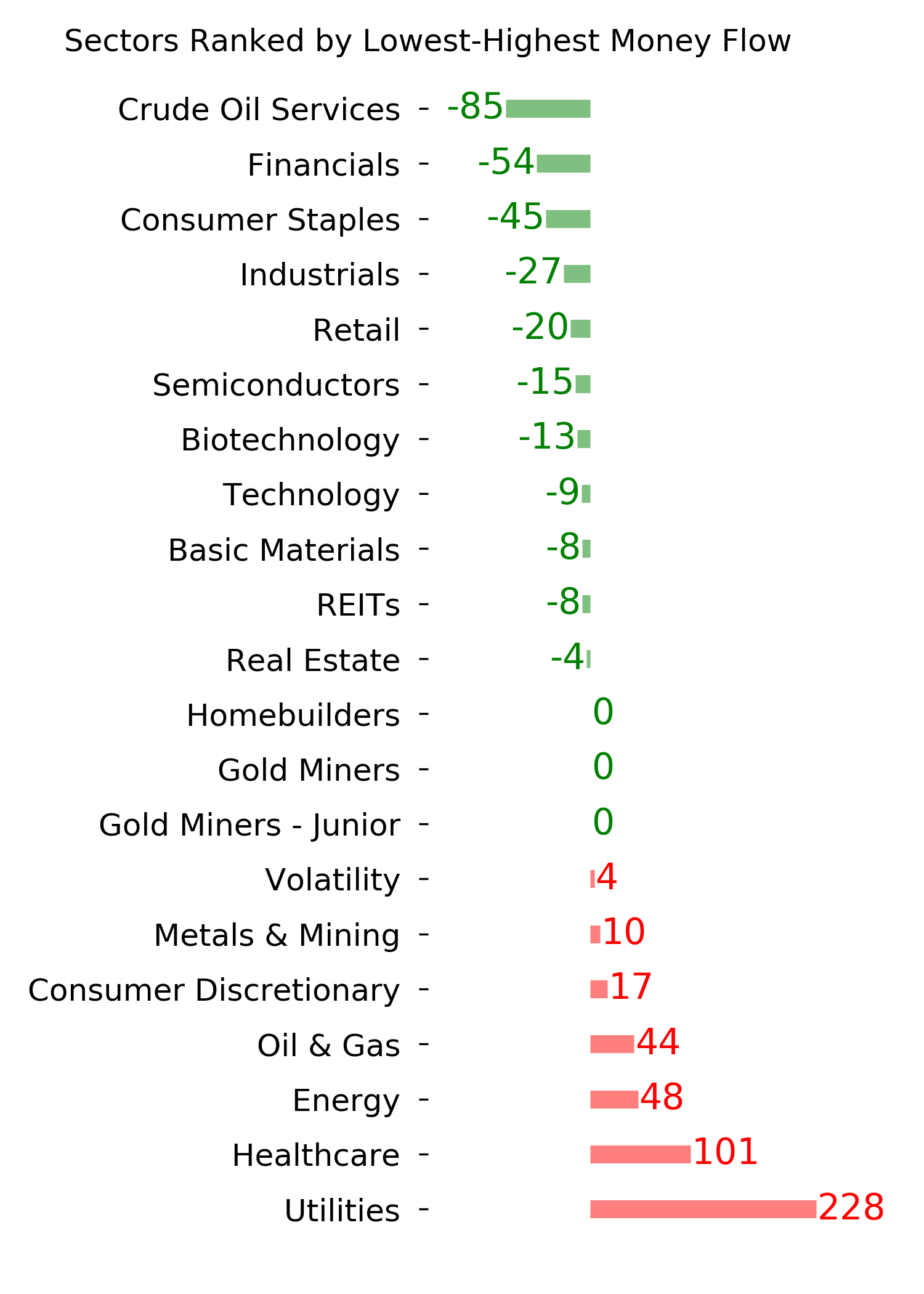

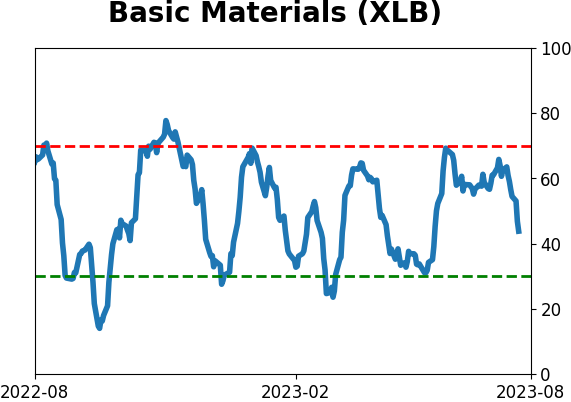

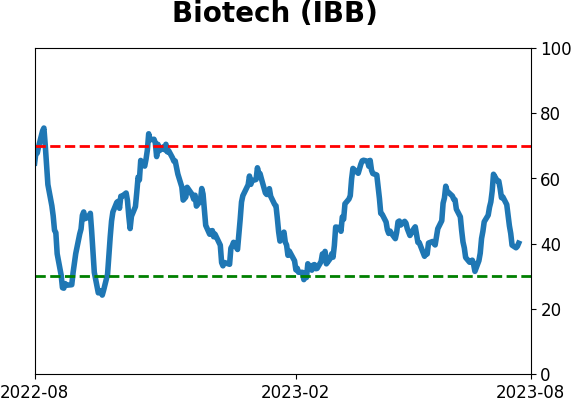

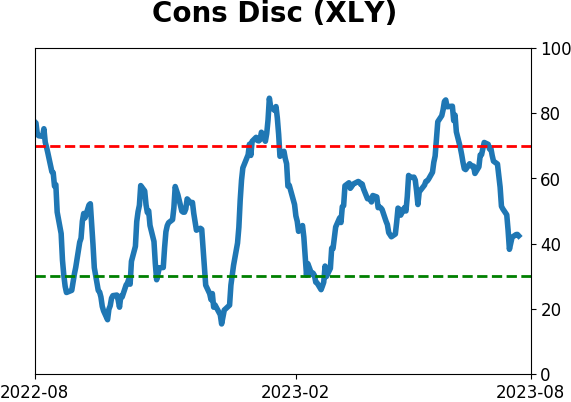

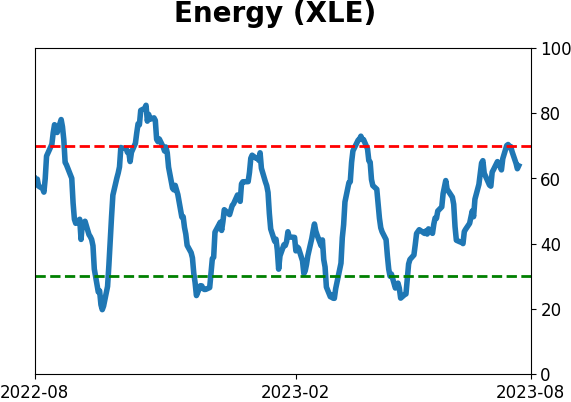

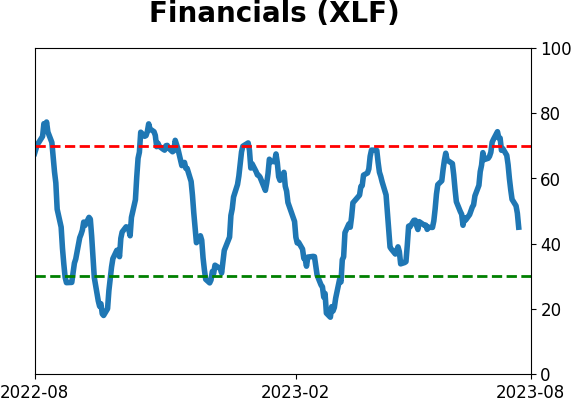

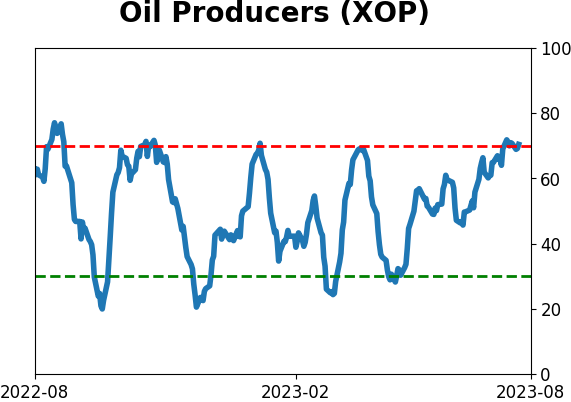

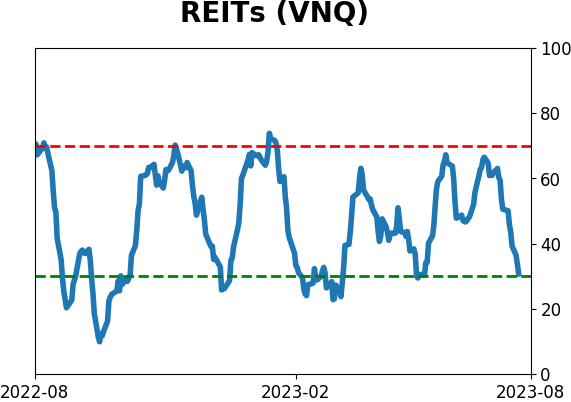

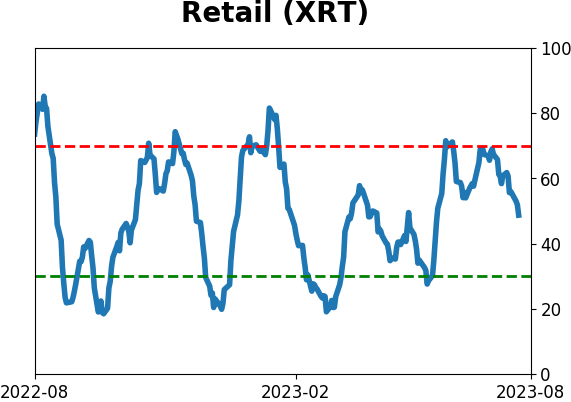

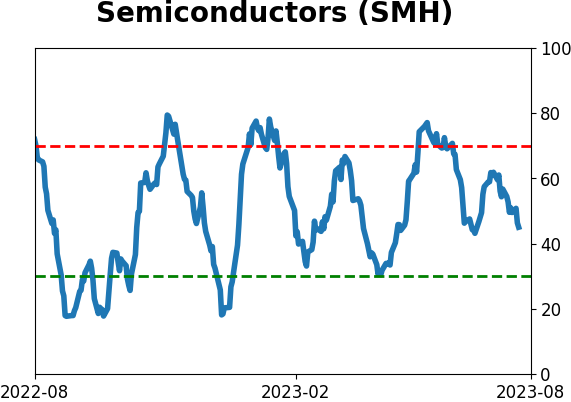

Sector ETF's - 10-Day Moving Average

|

|

|

Country ETF's - 10-Day Moving Average

|

|

|

Bond ETF's - 10-Day Moving Average

|

|

|

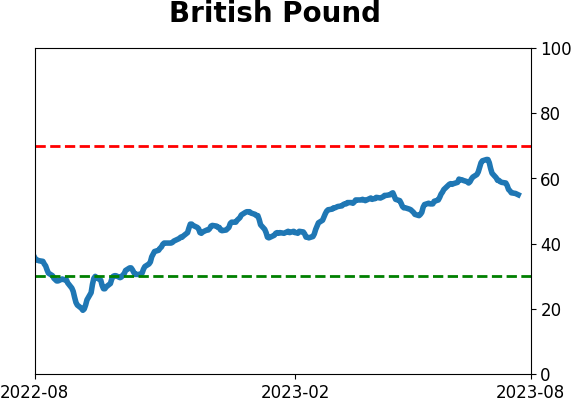

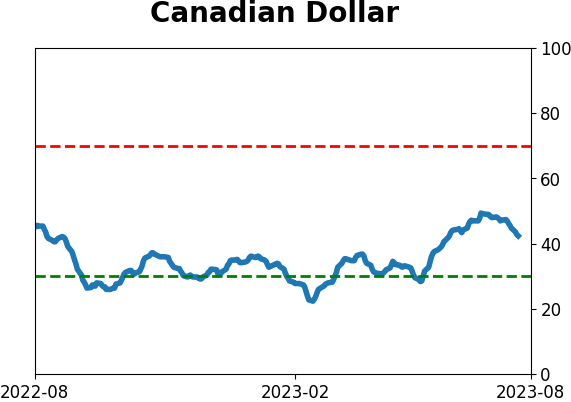

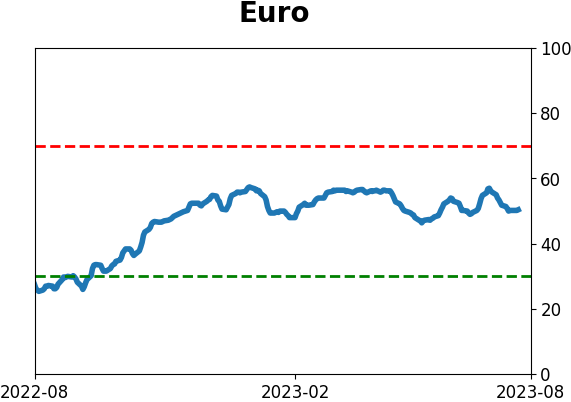

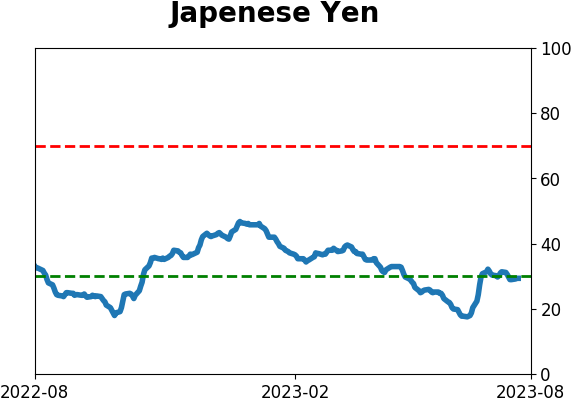

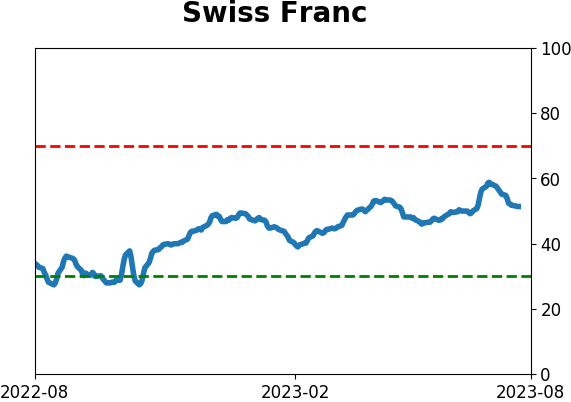

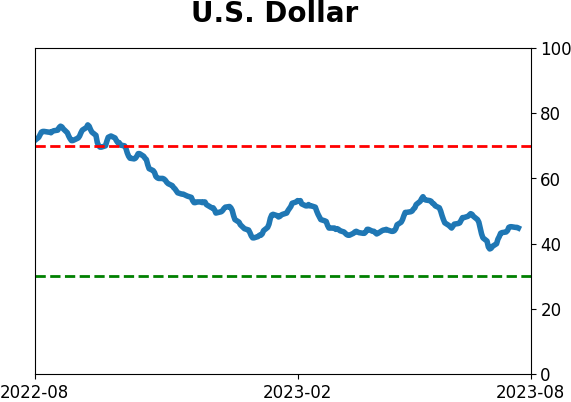

Currency ETF's - 5-Day Moving Average

|

|

|

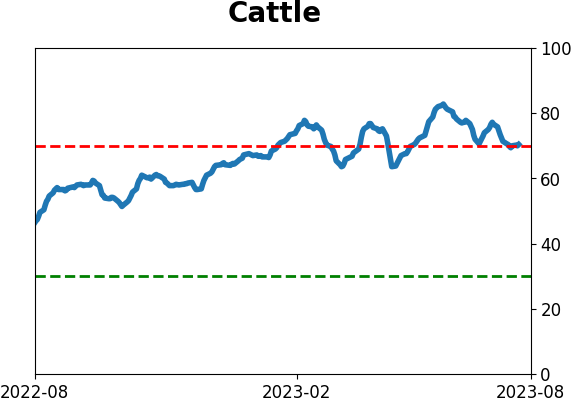

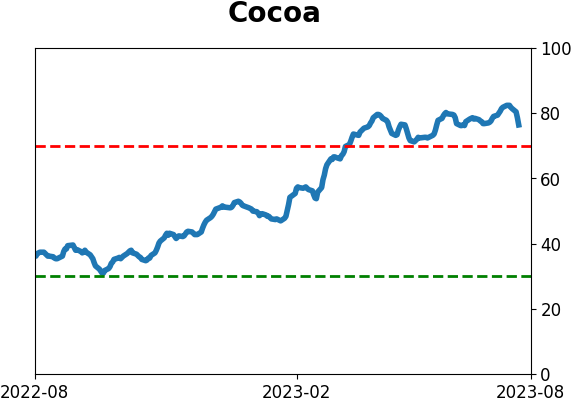

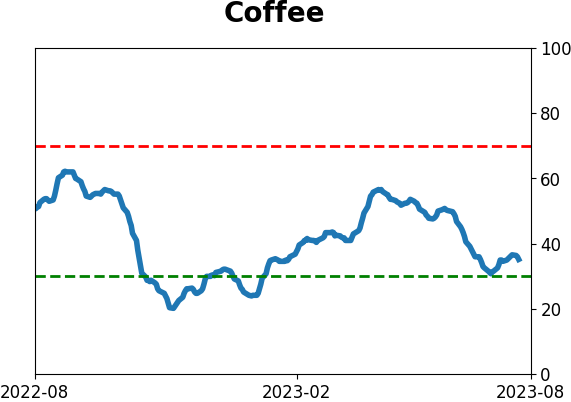

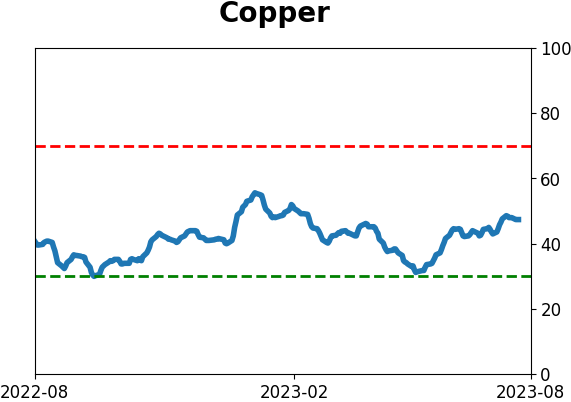

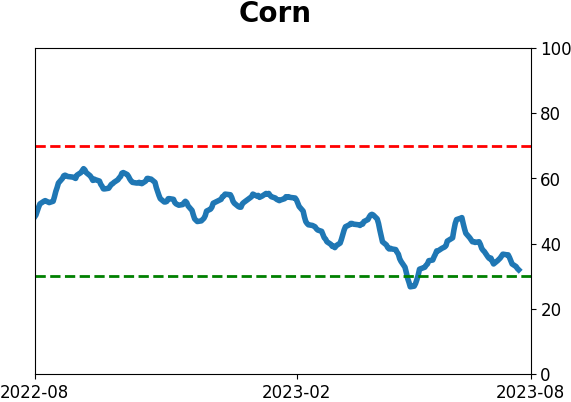

Commodity ETF's - 5-Day Moving Average

|

|