Headlines

|

|

Small traders continue to make big bearish bets:

Small speculators in index futures are once again carrying a near-record amount of short exposure against major equity indexes. And they continue to buy protective put options at a much greater than usual pace relative to speculative calls. Behavior like this has tended to lead to a rebounding market.

|

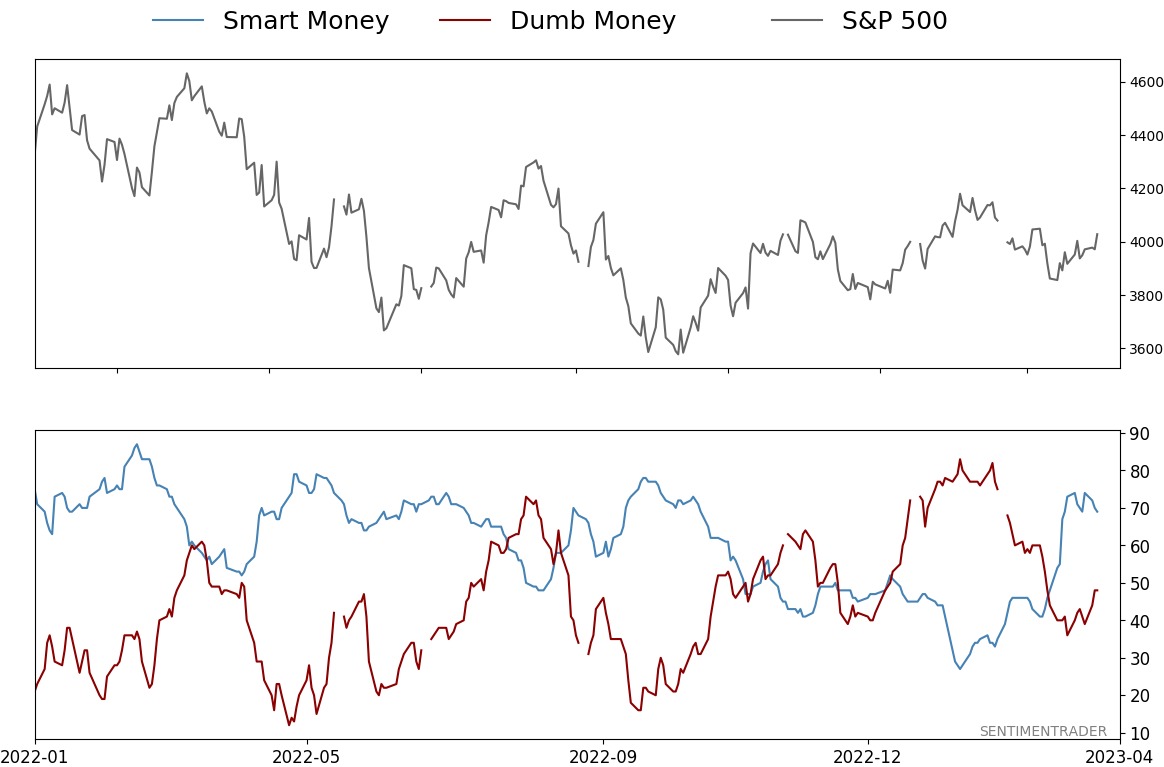

Smart / Dumb Money Confidence

|

Smart Money Confidence: 69%

Dumb Money Confidence: 48%

|

|

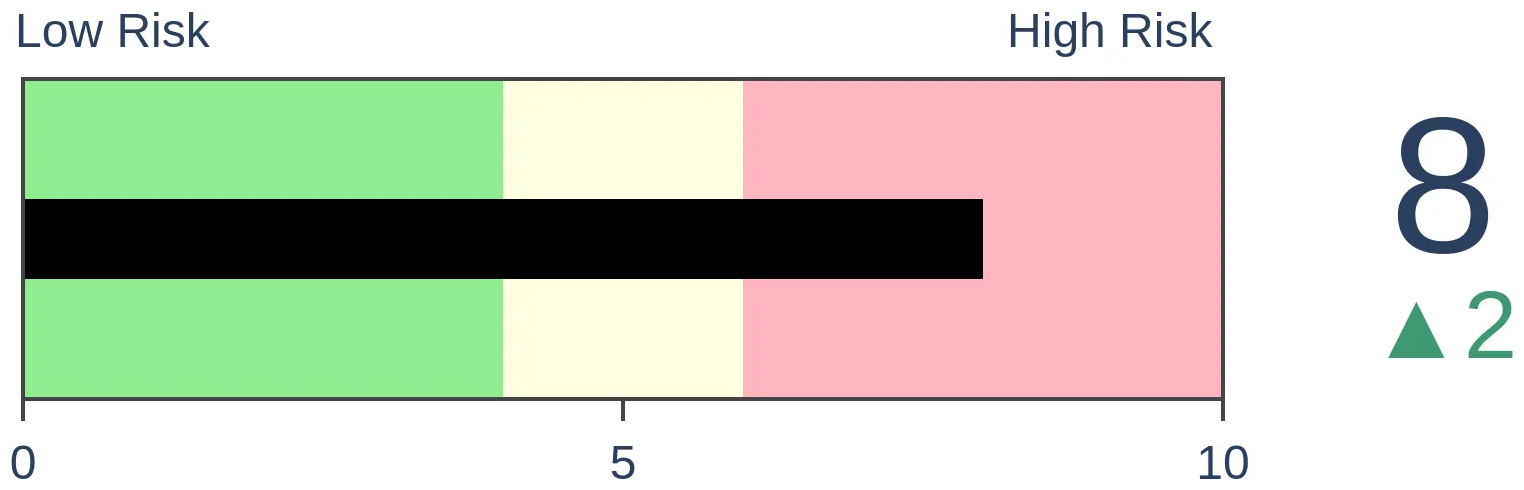

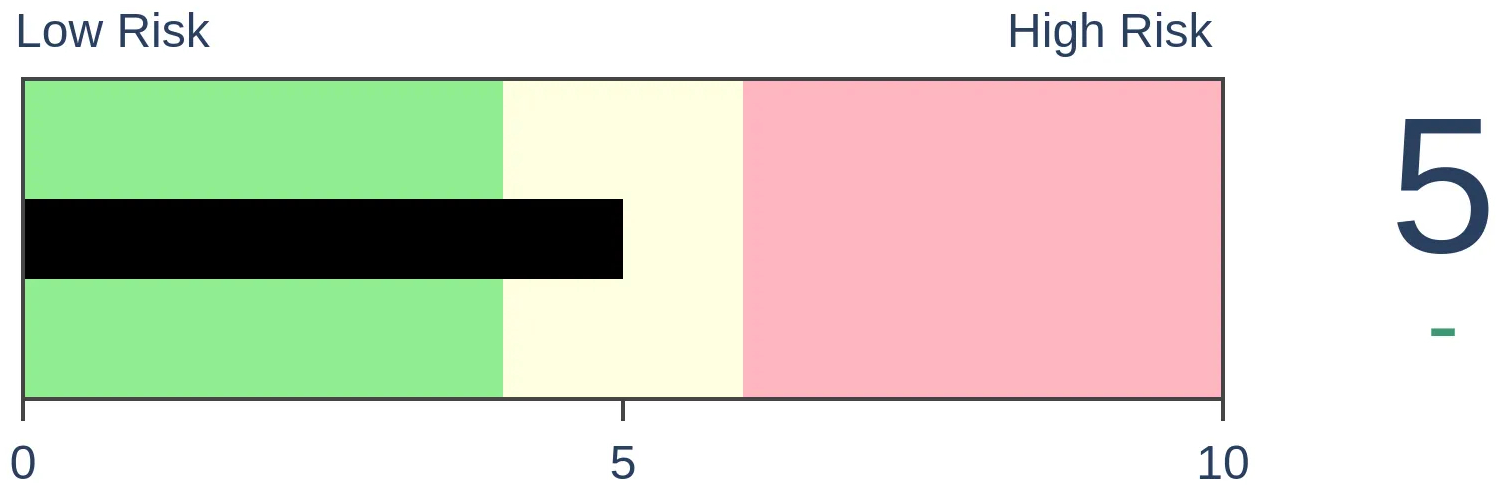

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

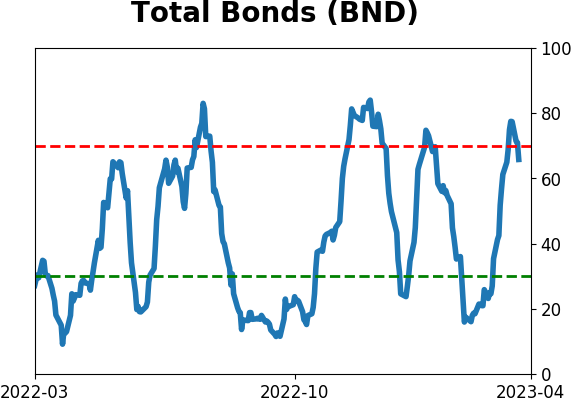

Bonds

|

Crude Oil

|

|

Gold

|

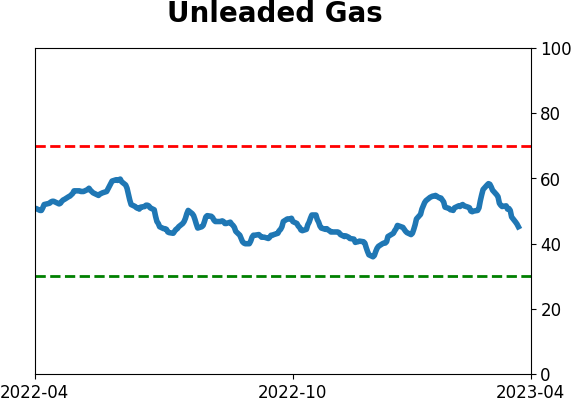

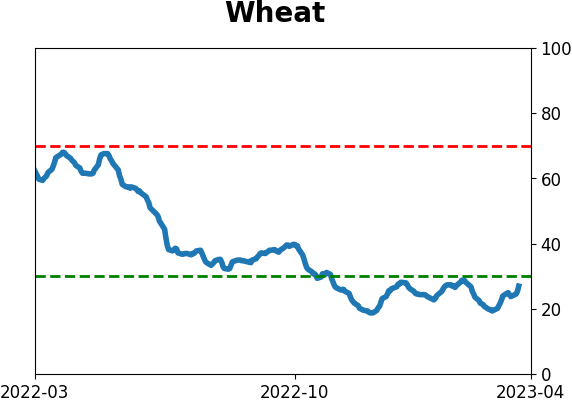

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

Small speculators in index futures are once again carrying a near-record amount of short exposure against major equity indexes. And they continue to buy protective put options at a much greater than usual pace relative to speculative calls. Behavior like this has tended to lead to a rebounding market.

FORECAST / TIMEFRAME

None

|

Key points:

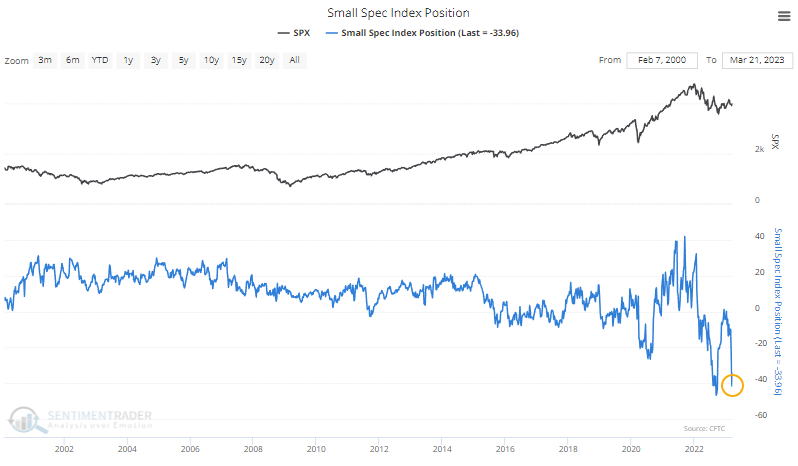

- Small speculators in index futures have moved back to a near-record short position

- Retail traders in the options market have been betting aggressively on a market decline

- When those traders behave this way in such leveraged instruments, stocks have a strong record of rallying

Futures and options markets both show extreme retail bearish bets

Small traders are having none of it. Despite most major equity indexes holding well above their October lows, retail traders in the futures and options markets behave like lower lows are in store.

Perhaps the indexes will head to new lows, but small traders aren't exactly known for forecasting too far in the future. More than anything, they rely on the immediate past to project the future. That's why it's unusual to see stocks holding up fairly well while traders' bets lean heavily bearish.

Due to data issues, the CFTC suffered delays in reporting positions in futures contracts. Now that it's catching up, we can see that small speculators have re-established near-record short positions against stocks in major equity index futures. It's a stark change from January when they flipped to net long.

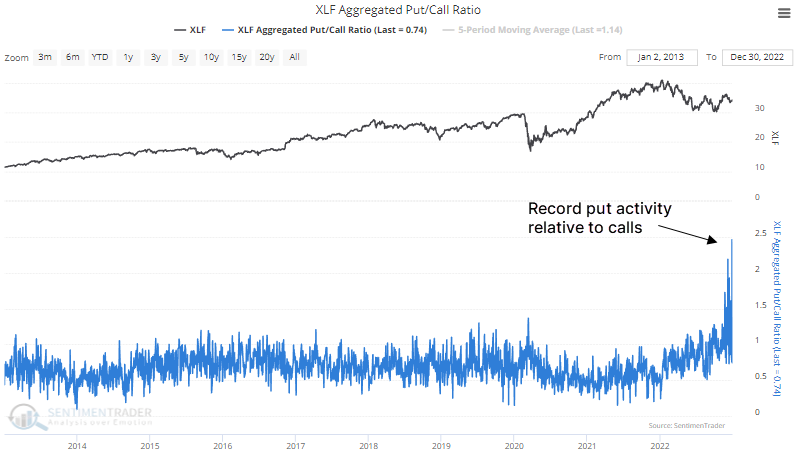

In the options market, small traders have continued to focus heavily on buying put options to open while relatively shunning calls. This is due, in large part, to a focus on hedging against systemic bank risk. The Aggregated Put/Call Ratio among companies in the Financial sector is through the roof - more than half again as active as it was during the pandemic panic.

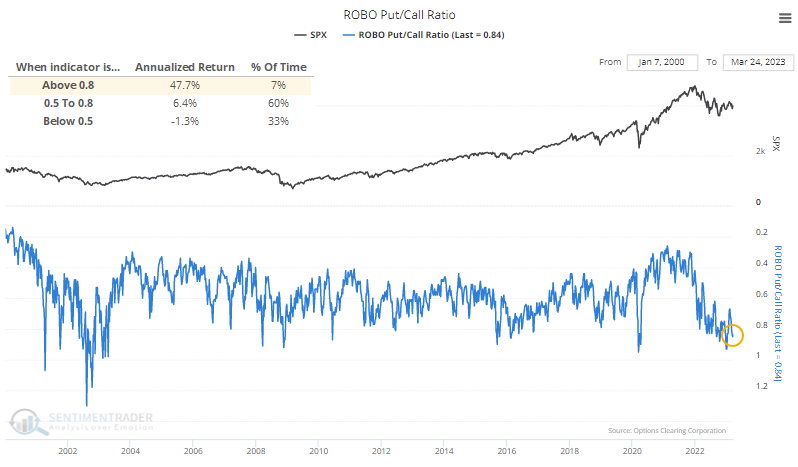

Such heavy put activity relative to calls has pushed the ROBO Put/Call Ratio to an extreme. It is once again among the most extreme 5% of all readings in 23 years (the scale in the chart below is inverted).

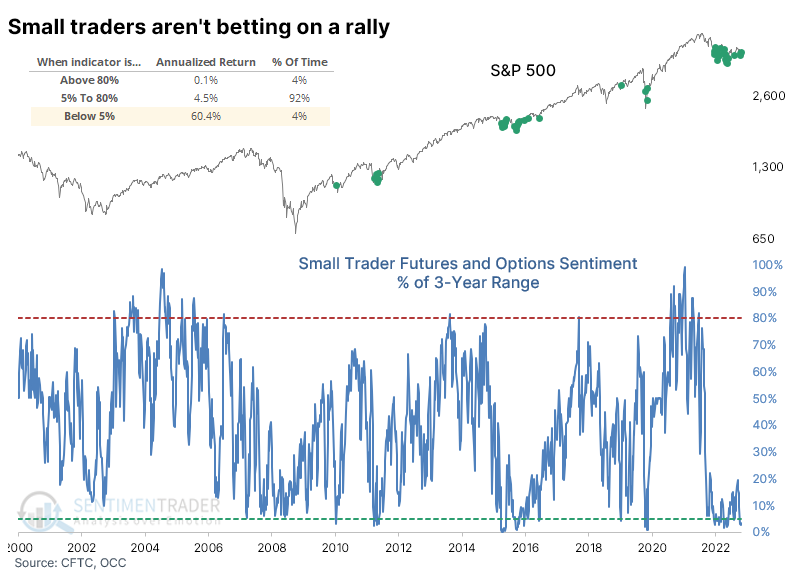

When we combine the two measures and look at their current level relative to their ranges over the past three years, both are at least in the most extreme 5% of readings. Extremes in these measures have profoundly impacted the S&P 500's future annualized return.

What the research tells us...

There was a remarkable amount of carnage under the surface of the indexes in 2022. Many of the most speculative issues that attracted the most attention and leverage were decimated. Even though most stocks bottomed five months ago, investors are still prone to quickly switch back to a bearish mentality, fearing that the destruction is only in the middle innings. But when we see behavior as we have since last summer, there is really no precedent since at least 1950 when it occurred amid a bear market, only at the ends of them. The fact that retail traders in the most leveraged instruments are still betting on a significant decline should further support stocks.

Indicators at Extremes

Phase Table

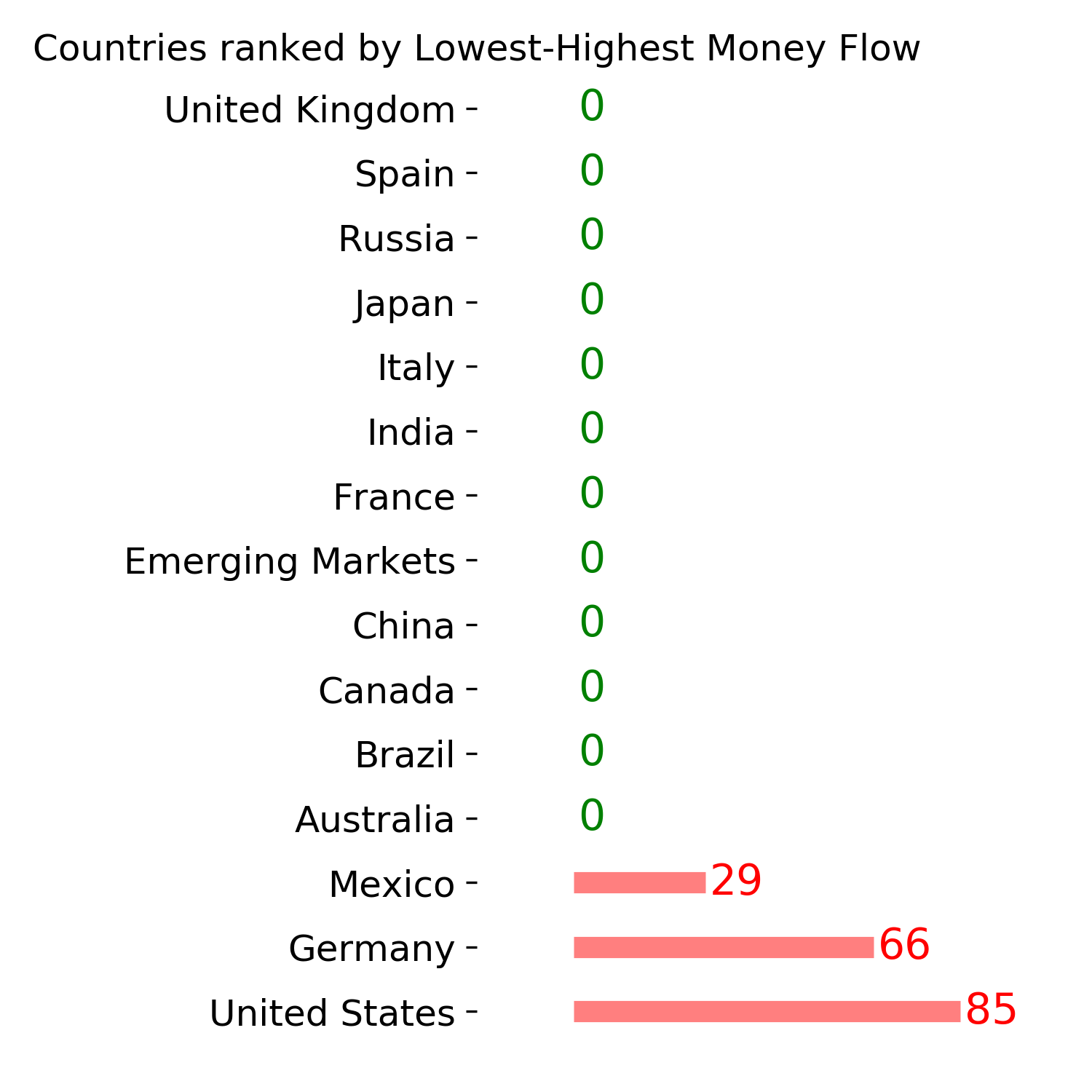

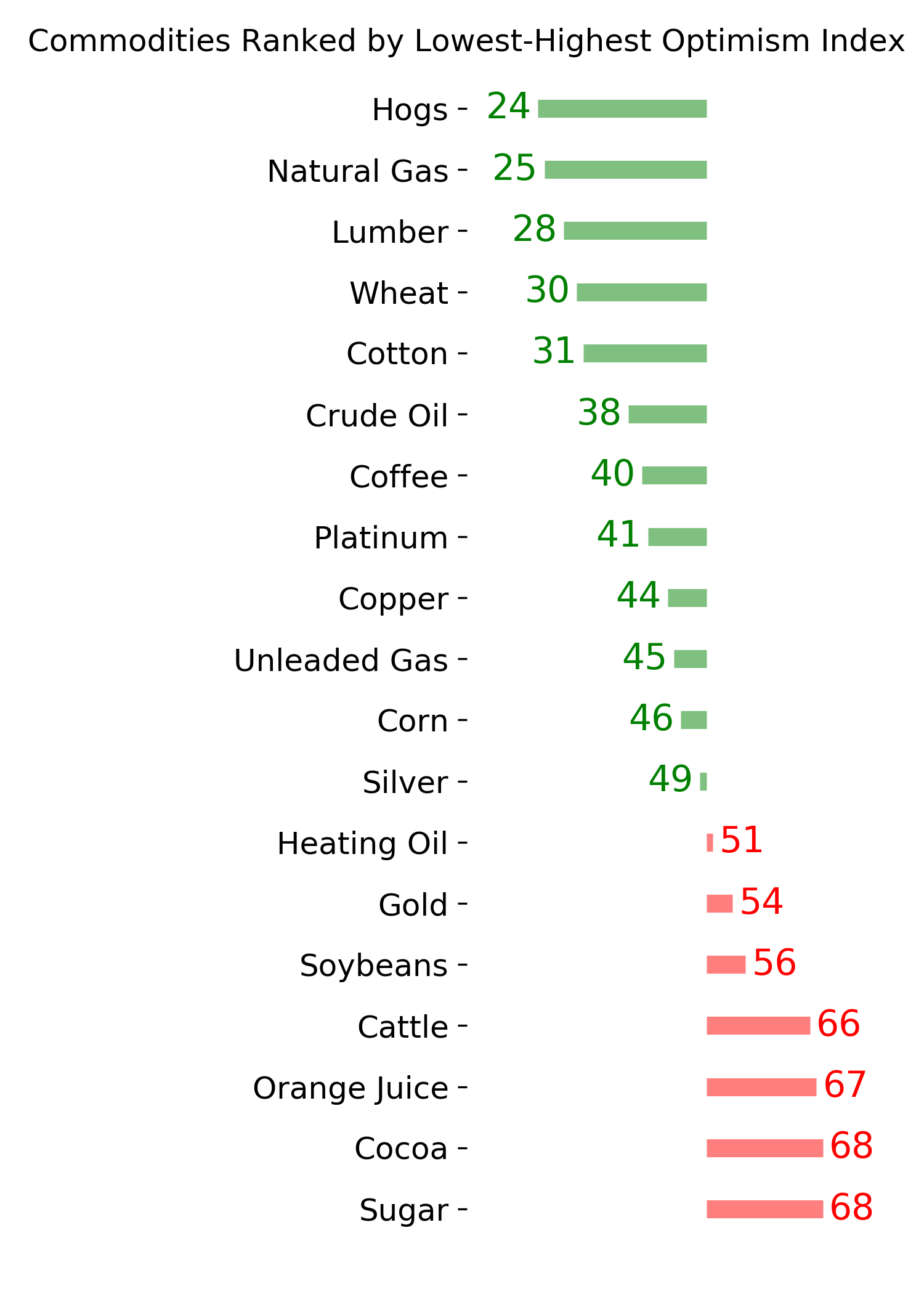

Ranks

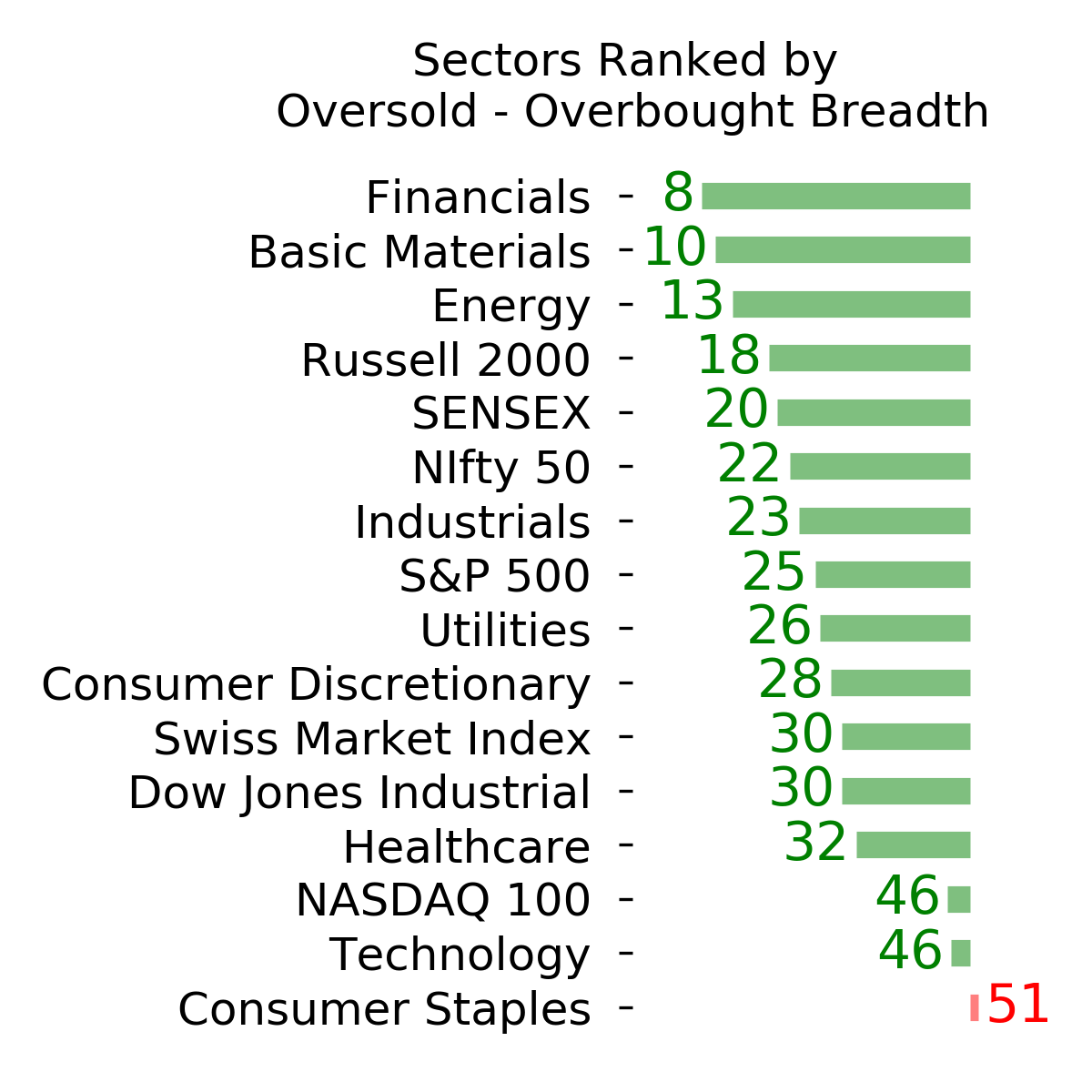

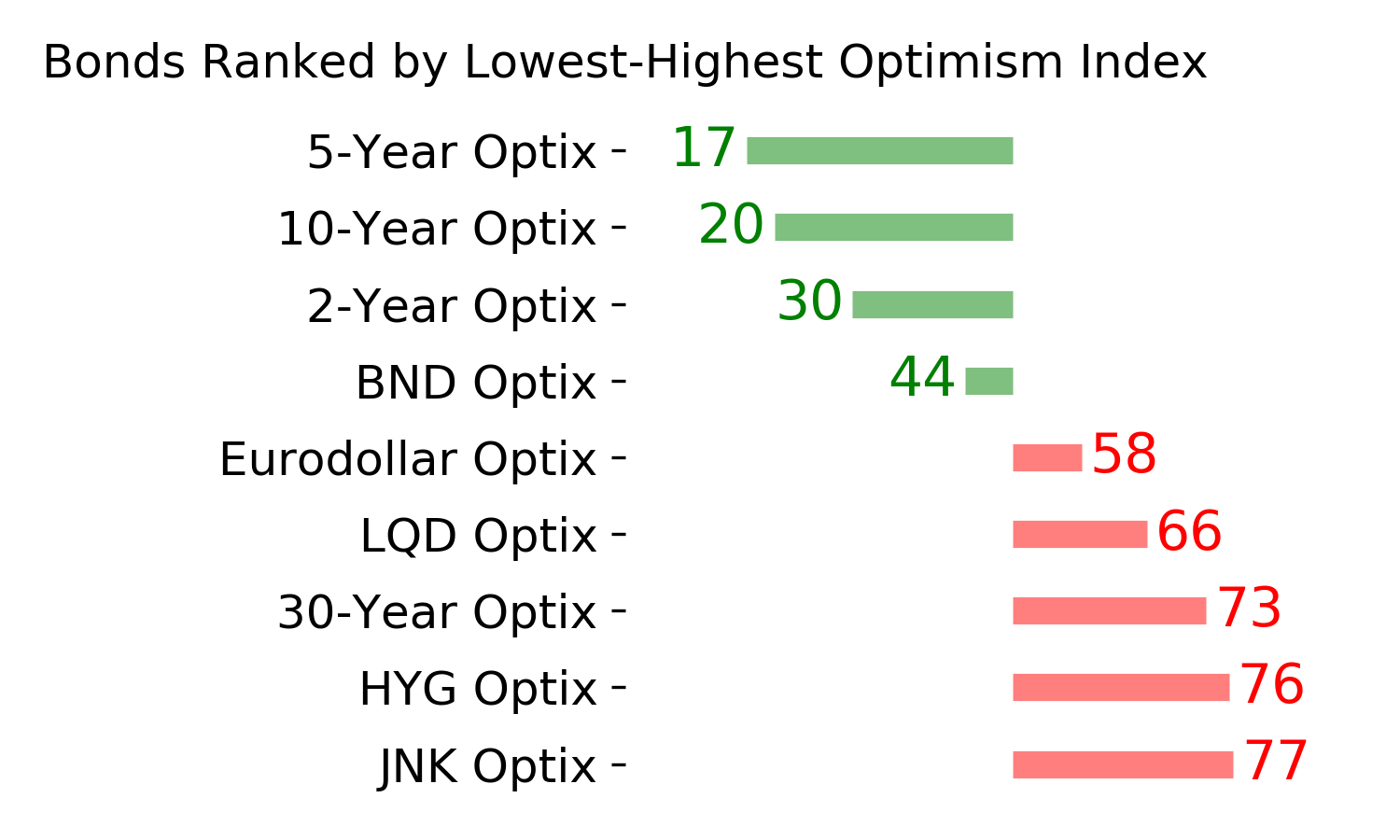

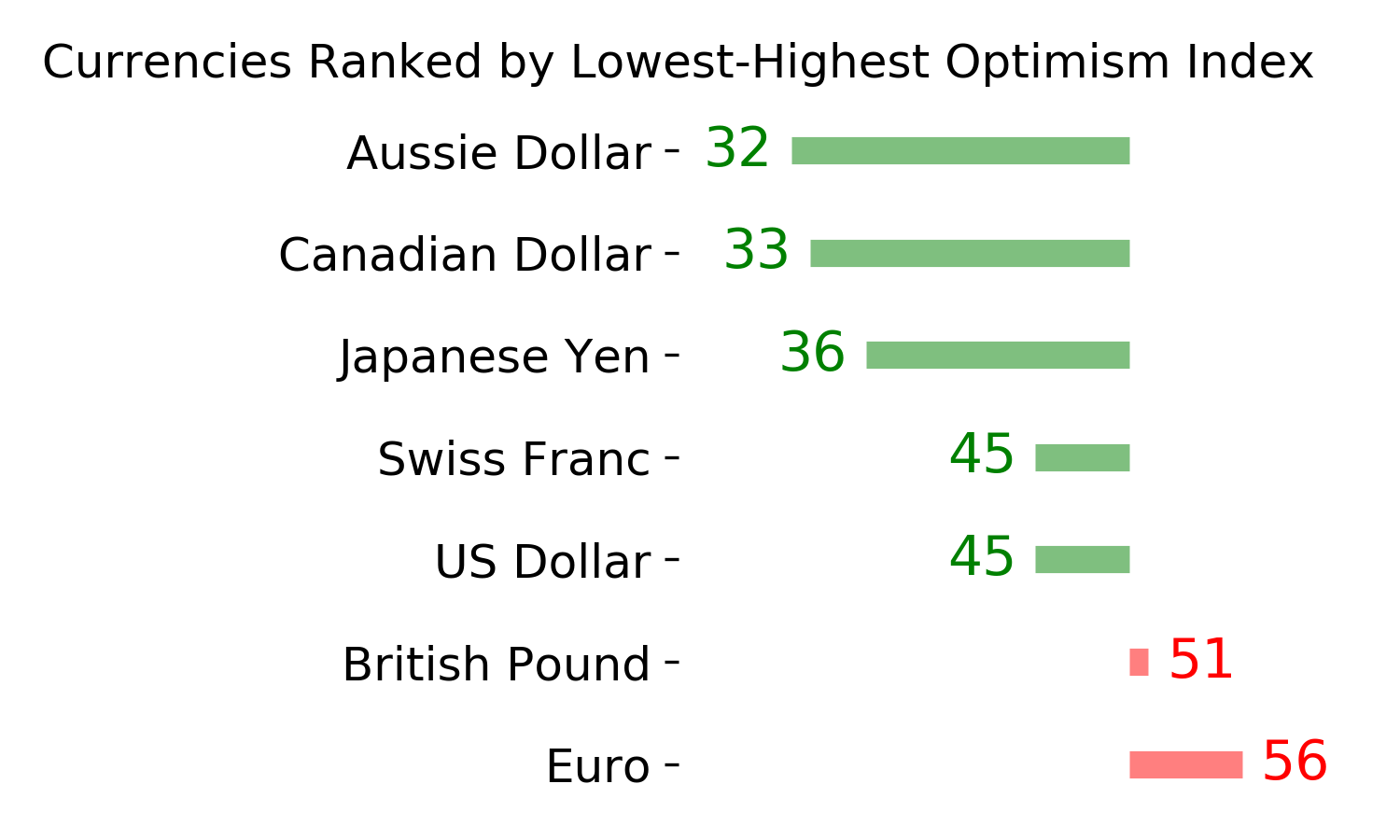

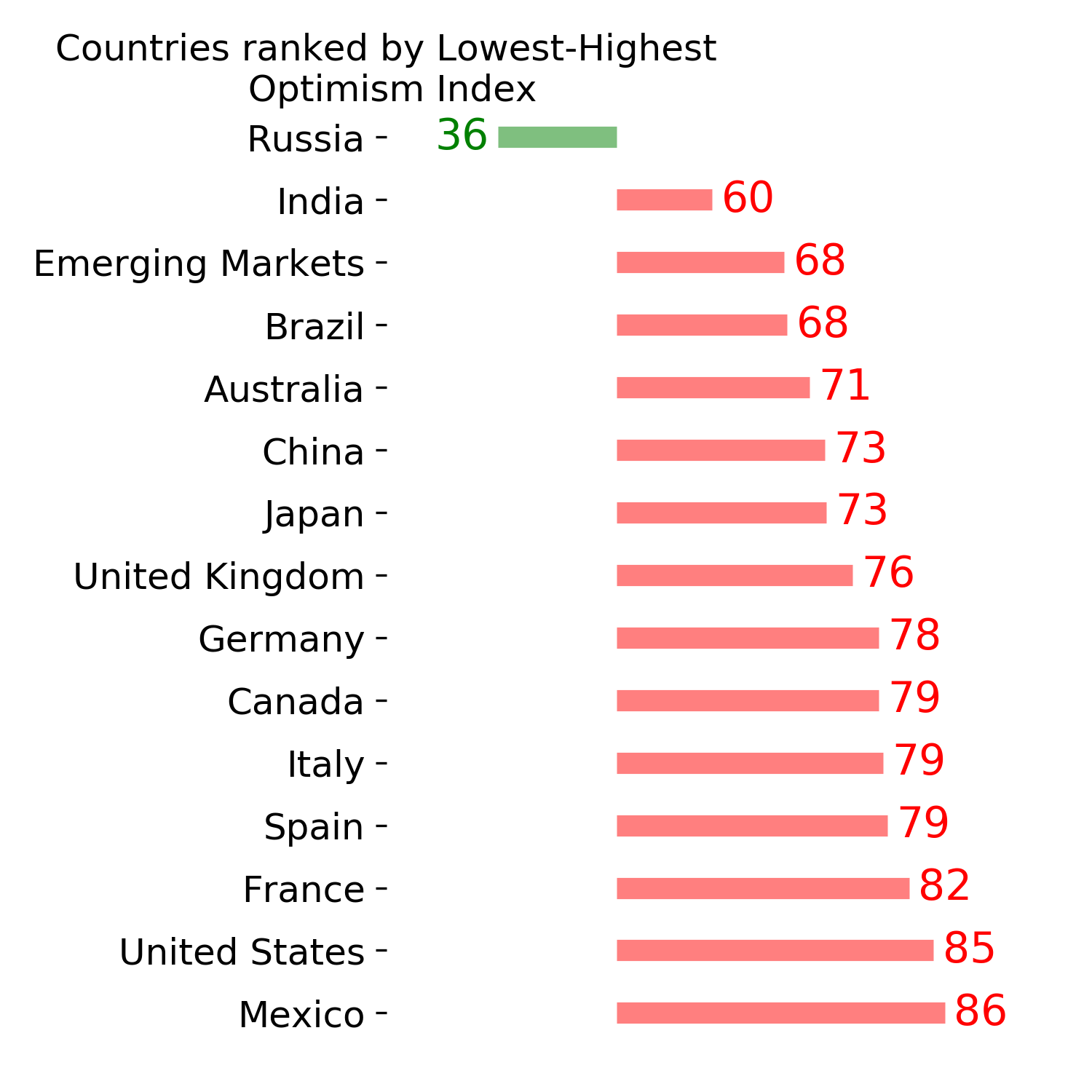

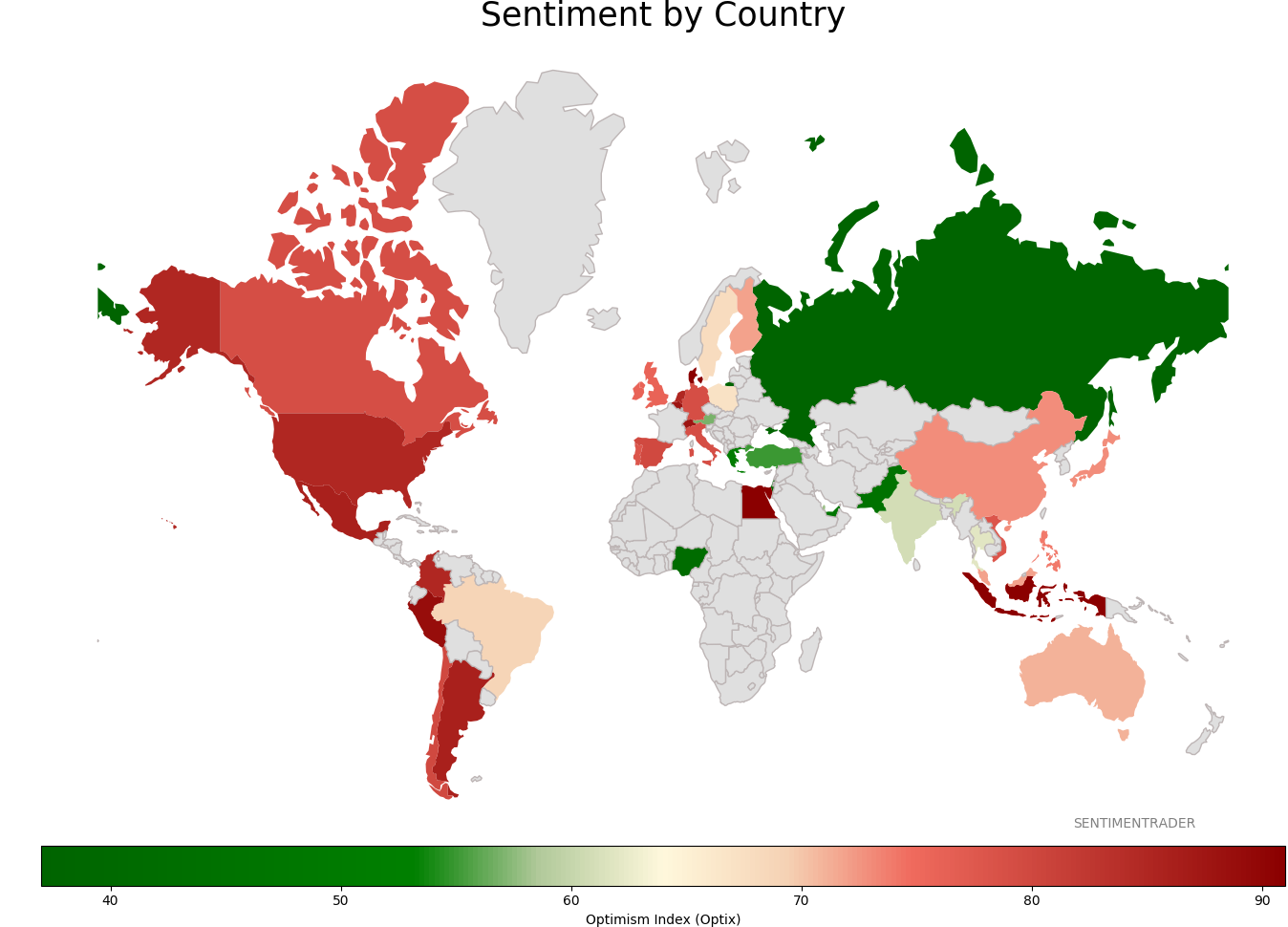

Sentiment Around The World

Optimism Index Thumbnails

|

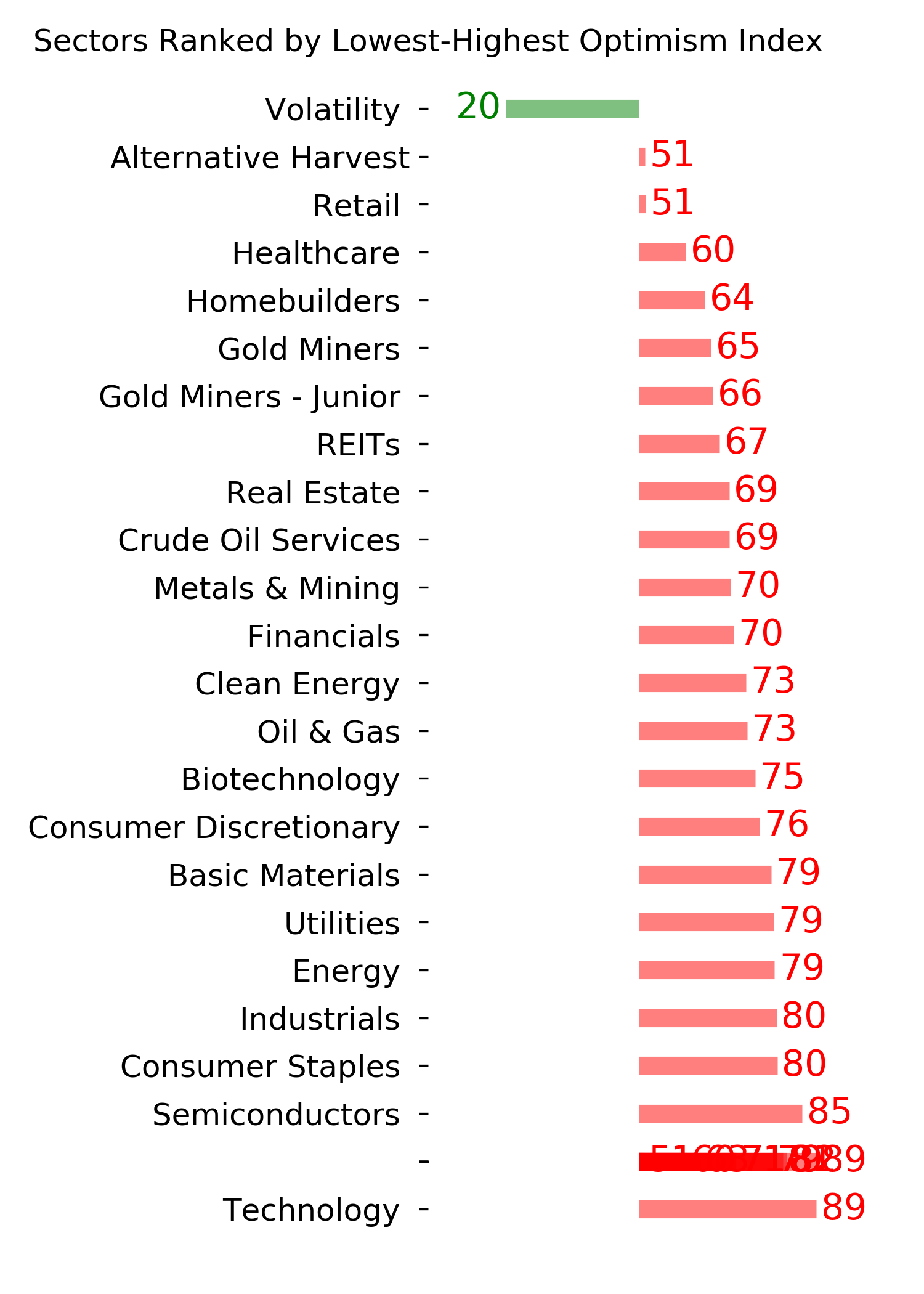

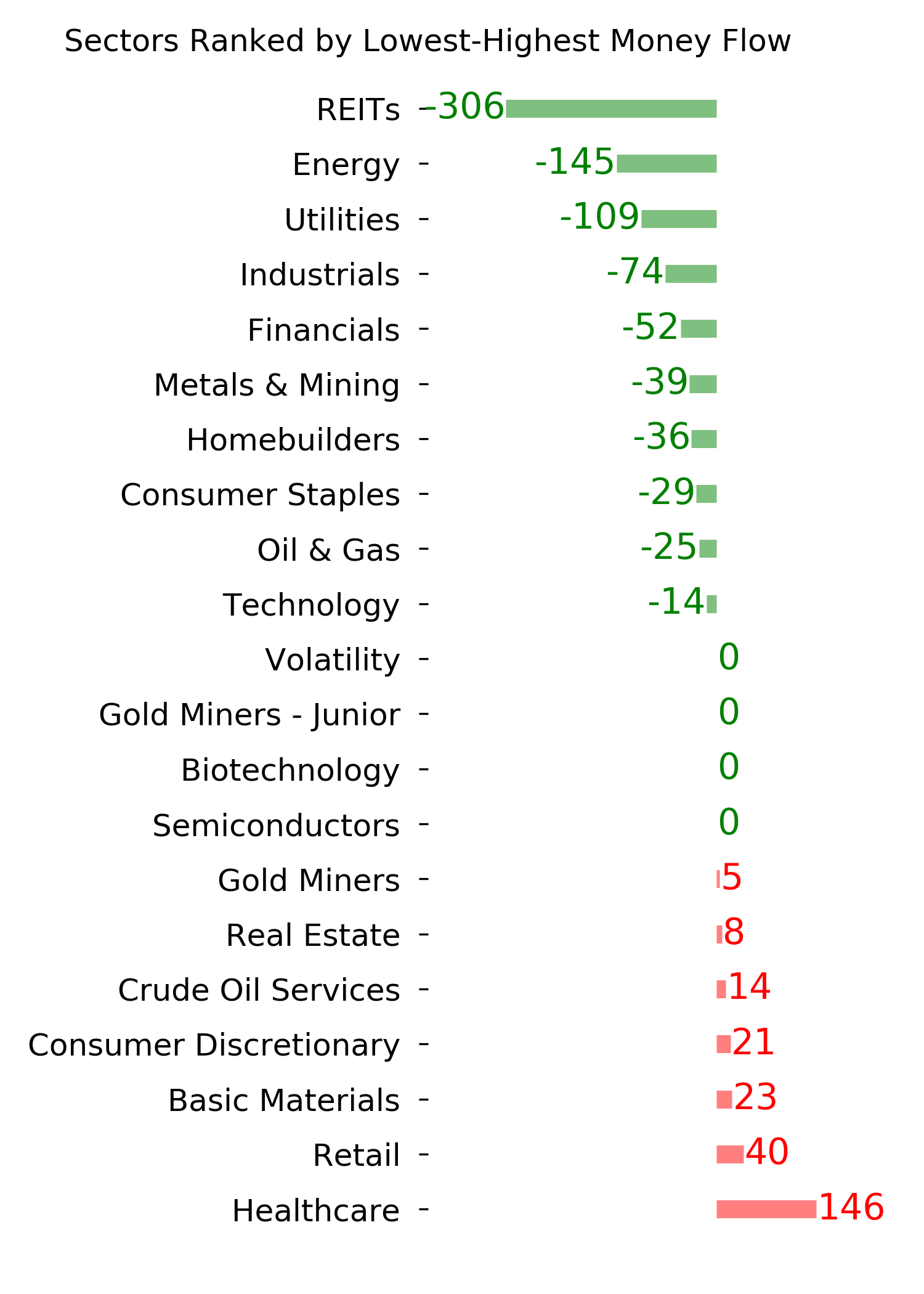

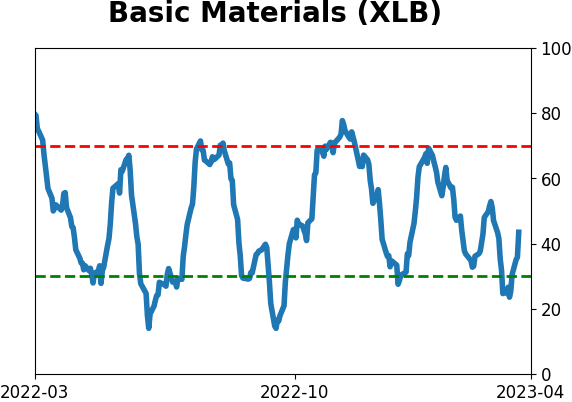

Sector ETF's - 10-Day Moving Average

|

|

|

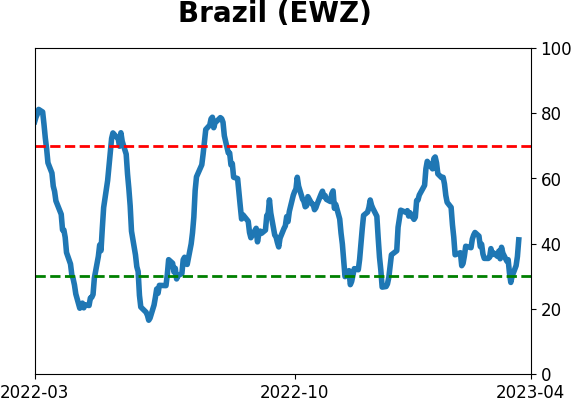

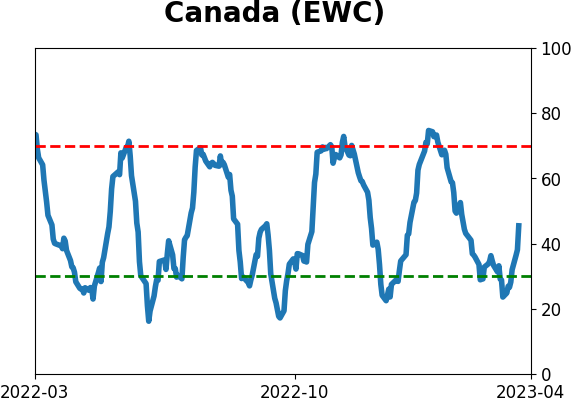

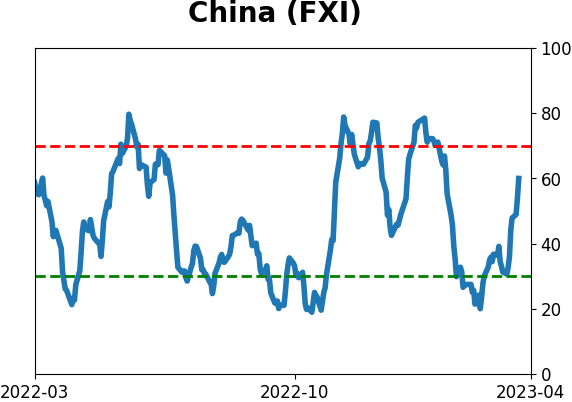

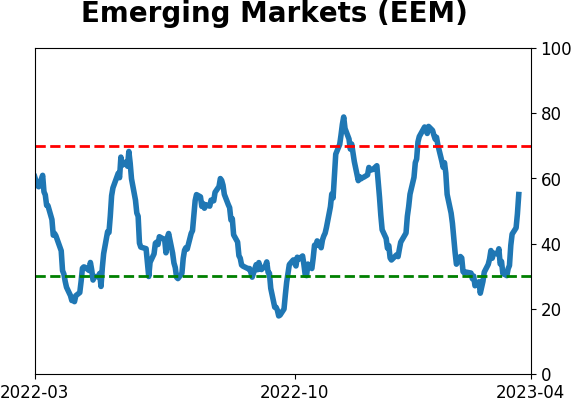

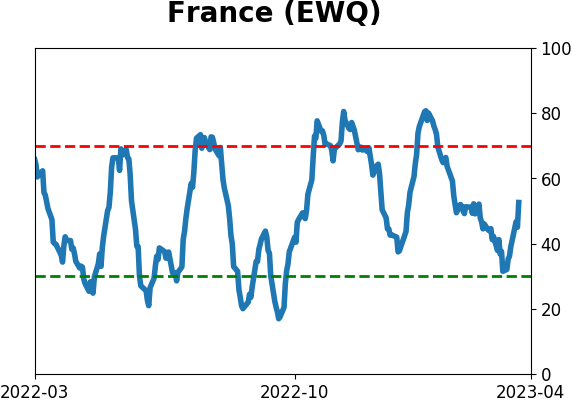

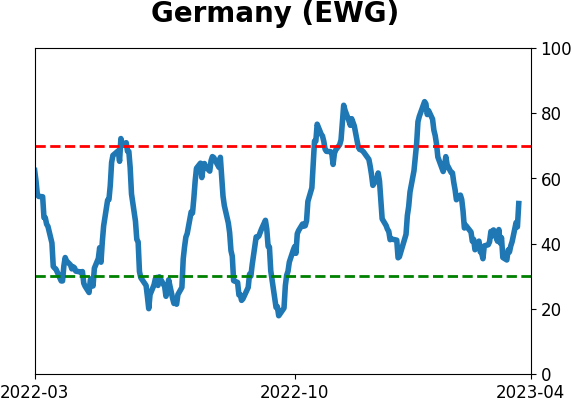

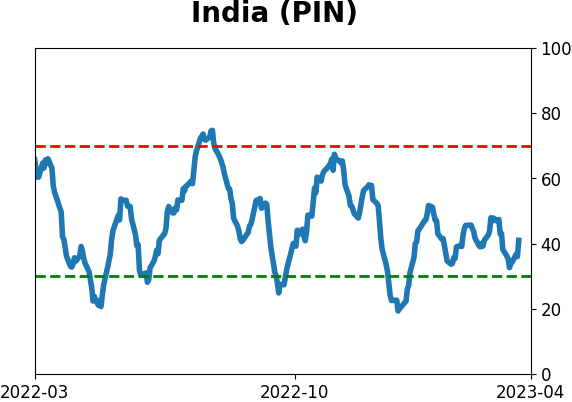

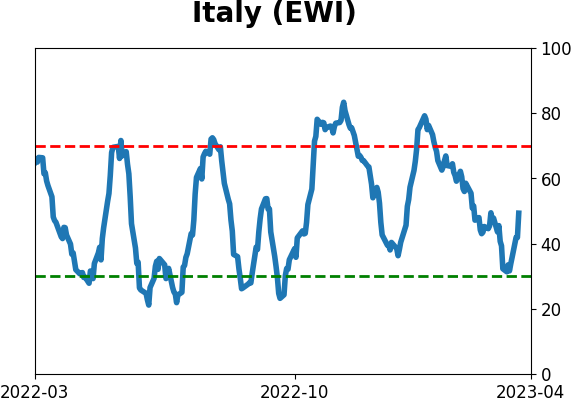

Country ETF's - 10-Day Moving Average

|

|

|

Bond ETF's - 10-Day Moving Average

|

|

|

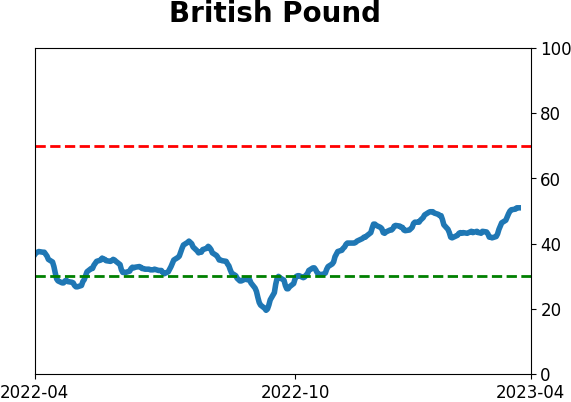

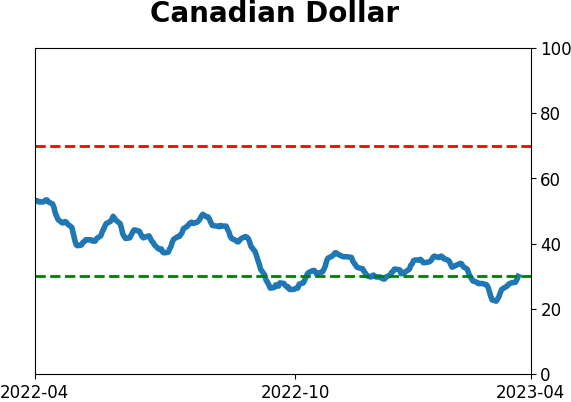

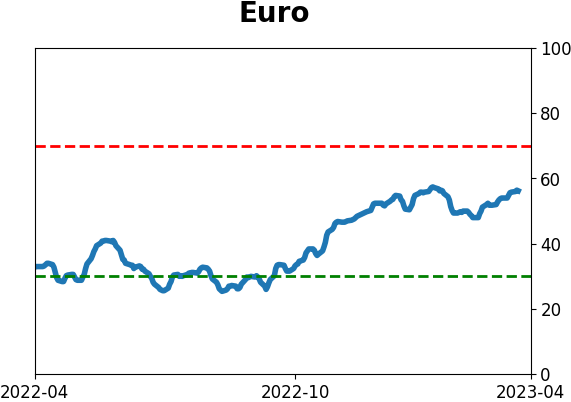

Currency ETF's - 5-Day Moving Average

|

|

|

Commodity ETF's - 5-Day Moving Average

|

|