Headlines

|

|

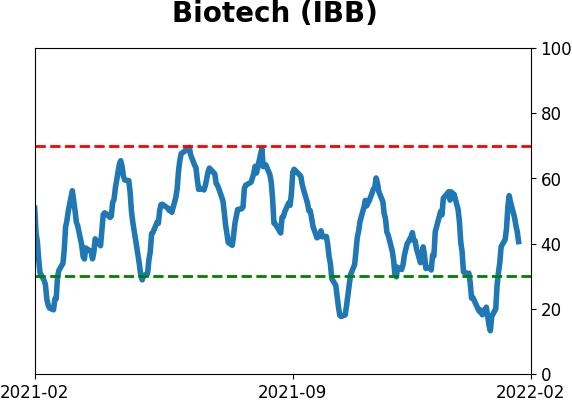

Taking another stab at extremes in Biotech:

The Biotechnology sector has suffered some of the worst selling pressure out of all sectors and industries over the past few months. In January, breadth in the sector hit some of the worst levels in 23 years. It has since recovered, suggesting the worst is behind us.

|

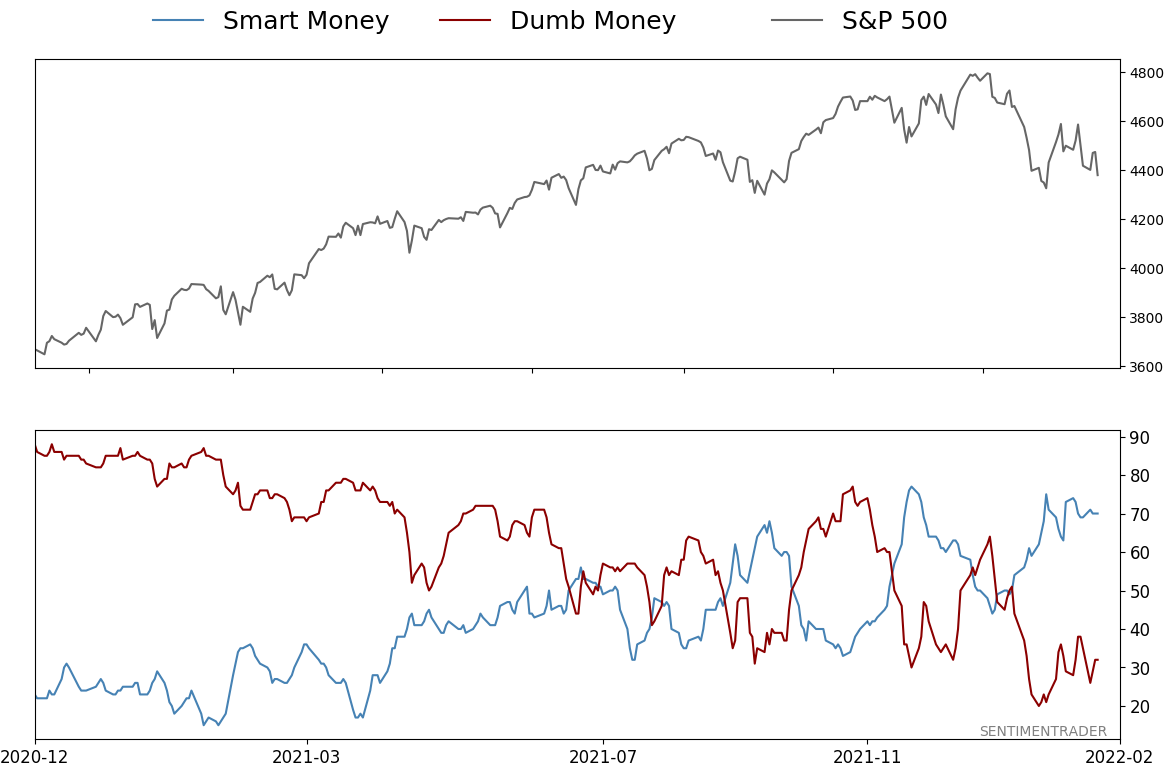

Smart / Dumb Money Confidence

|

Smart Money Confidence: 70%

Dumb Money Confidence: 32%

|

|

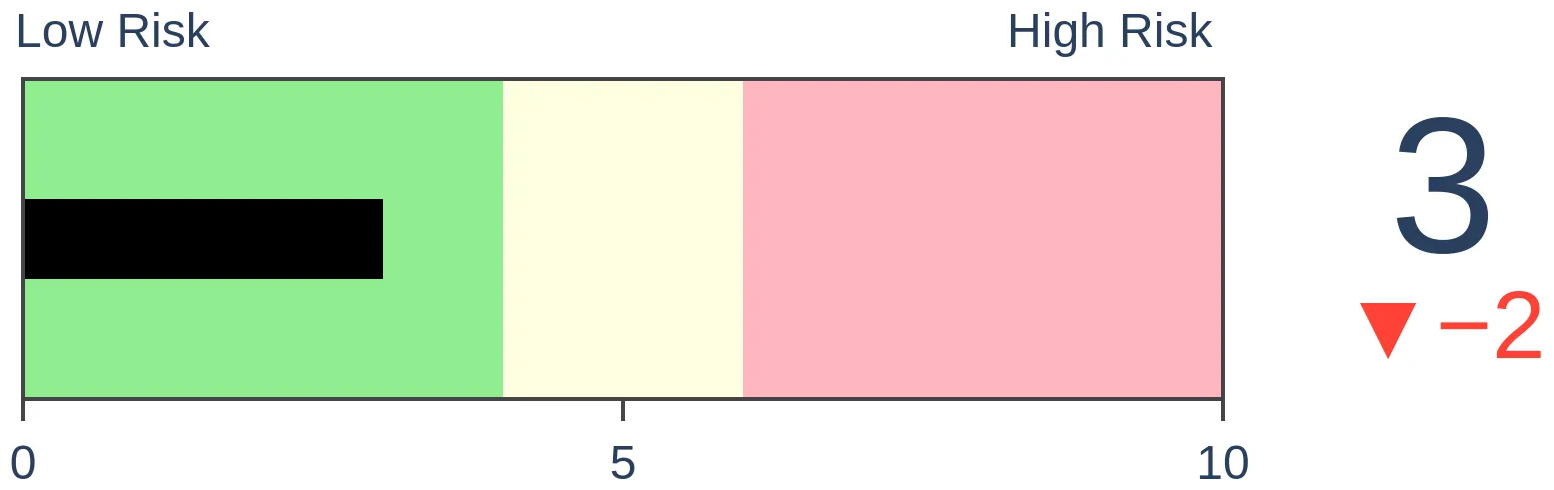

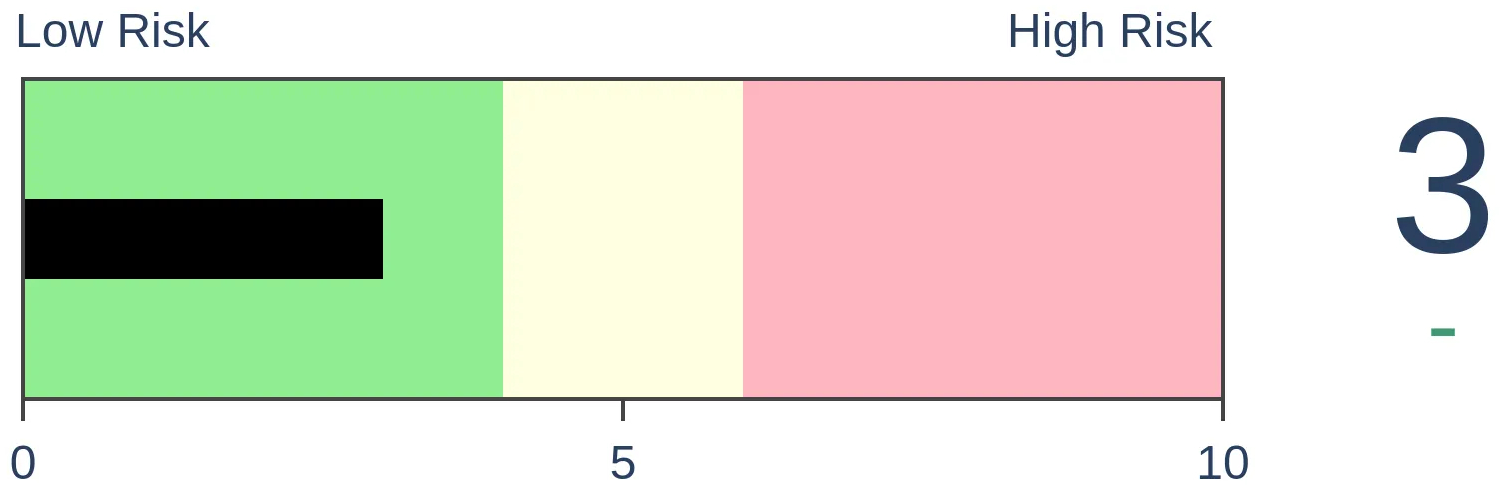

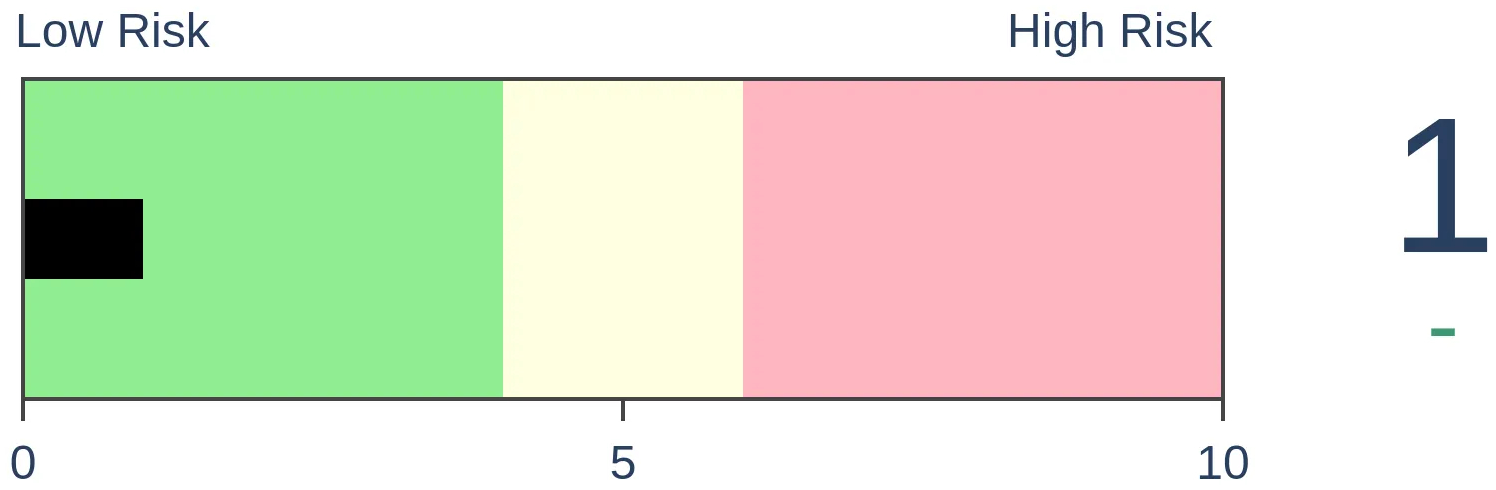

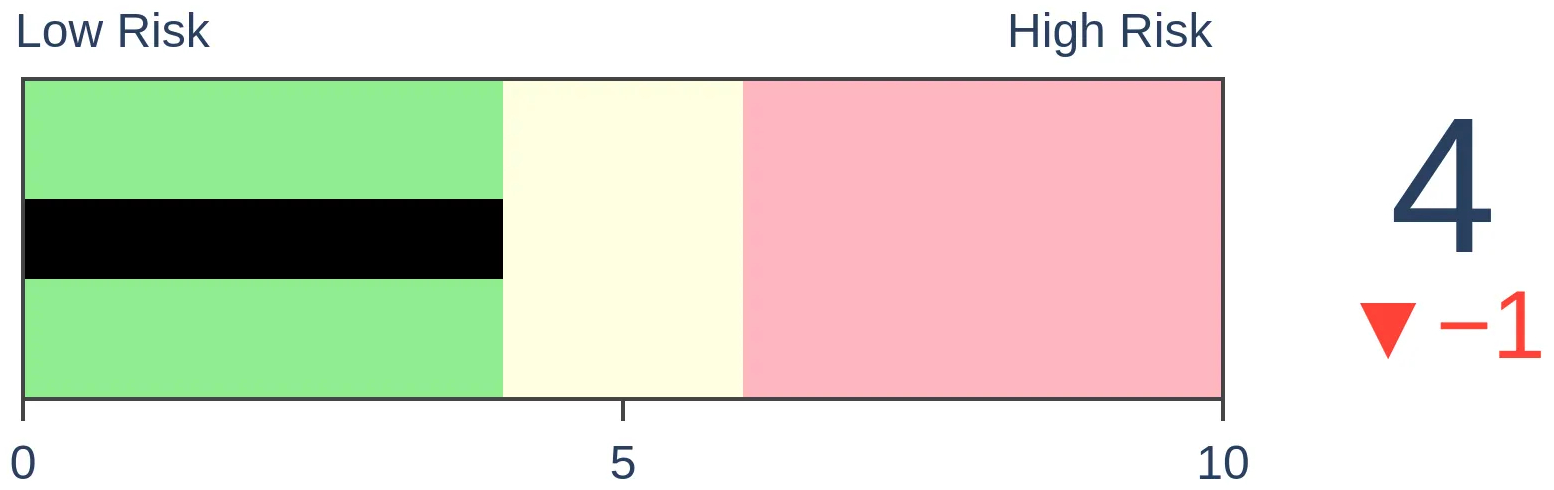

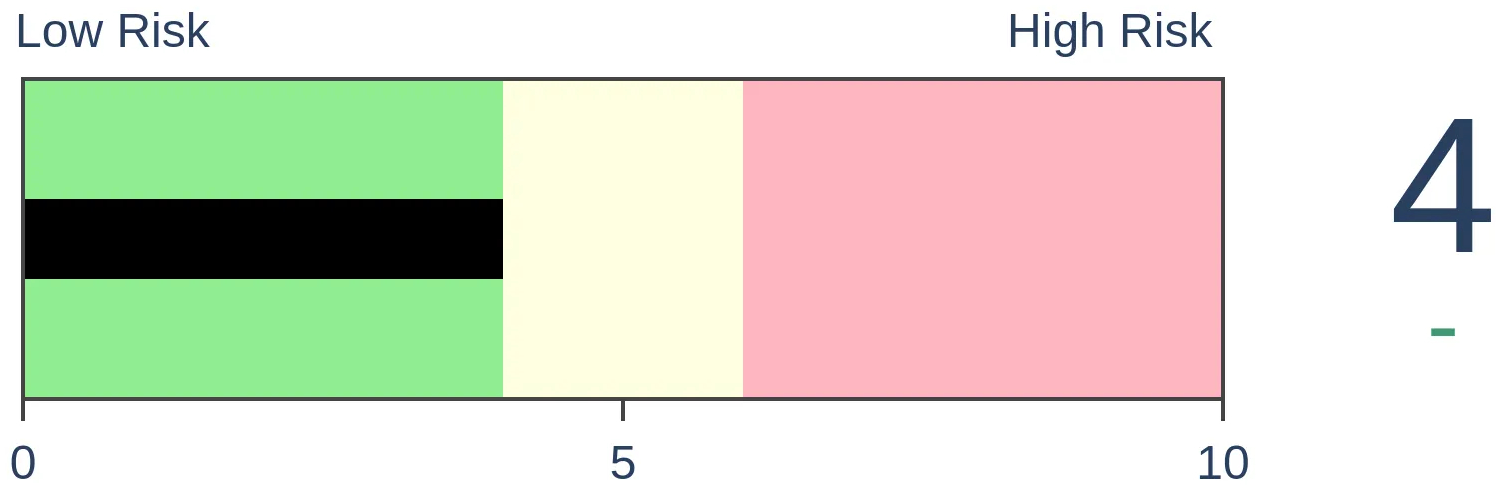

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

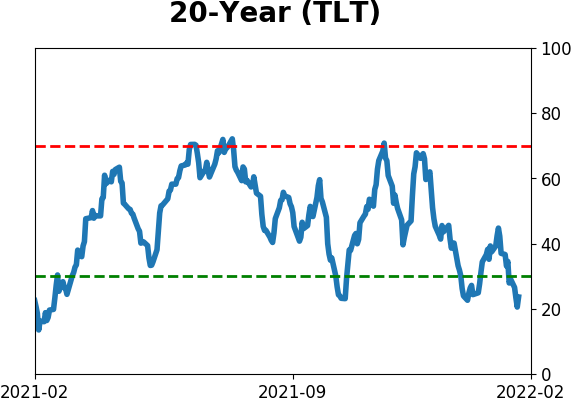

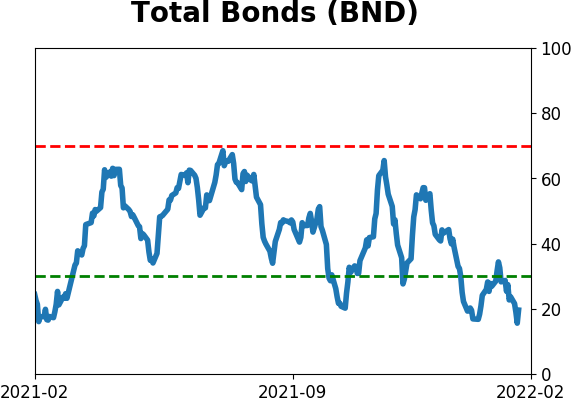

Bonds

|

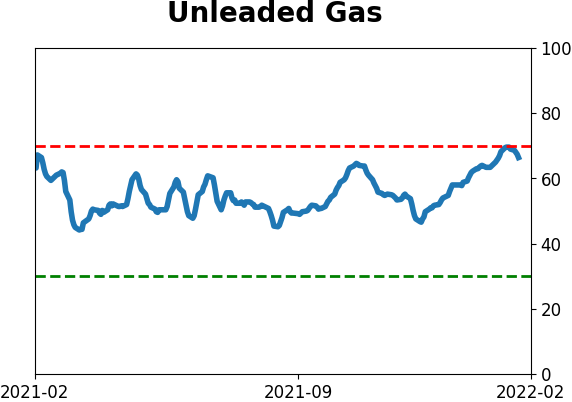

Crude Oil

|

|

Gold

|

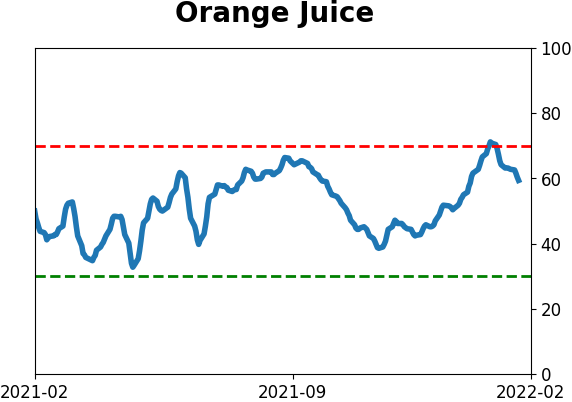

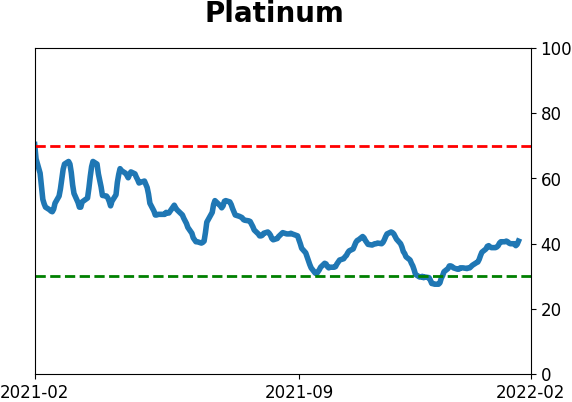

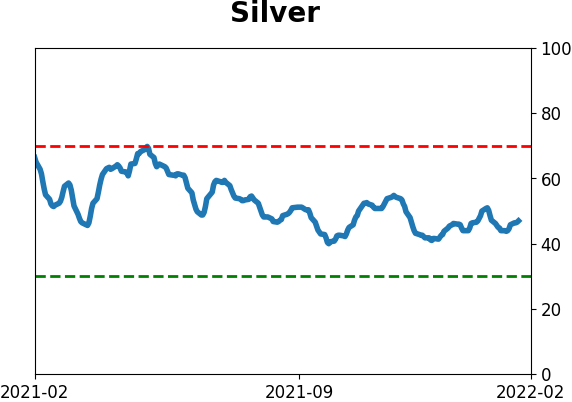

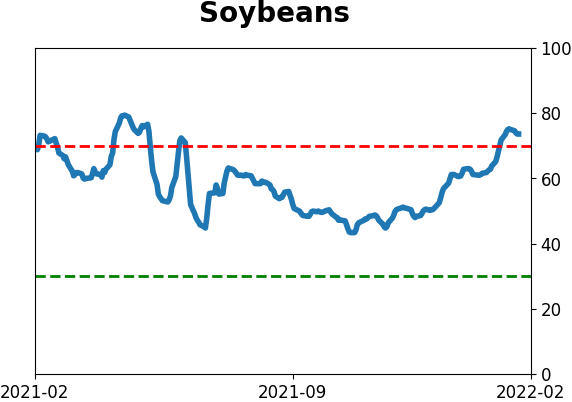

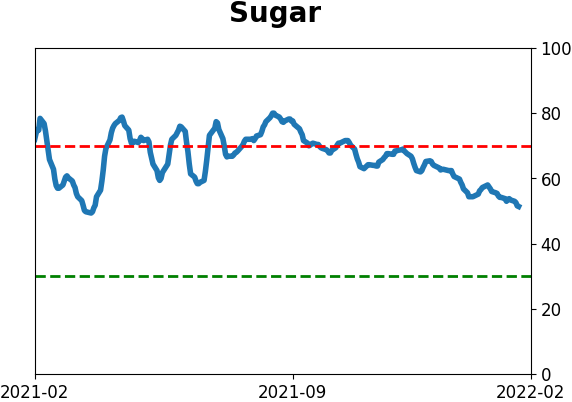

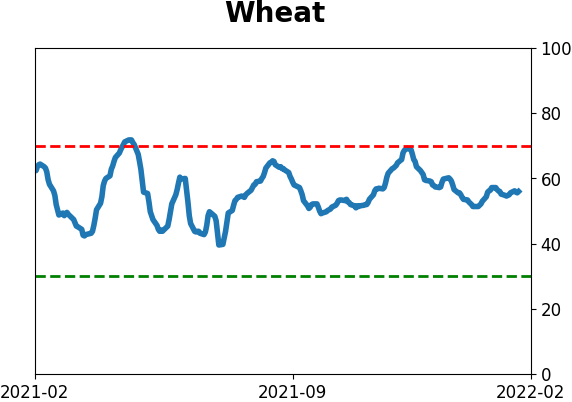

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

The Biotechnology sector has suffered some of the worst selling pressure out of all sectors and industries over the past few months. In January, breadth in the sector hit some of the worst levels in 23 years. It has since recovered, suggesting the worst is behind us.

FORECAST / TIMEFRAME

XBI -- Up, Long-Term

|

Key points:

- Selling in Biotech stocks reached a historic extreme in late January

- Since then, the stocks have tried to recover, and a composite breadth indicator has been rebounding

- Similar reversals preceded excellent returns, but there was a failure in December

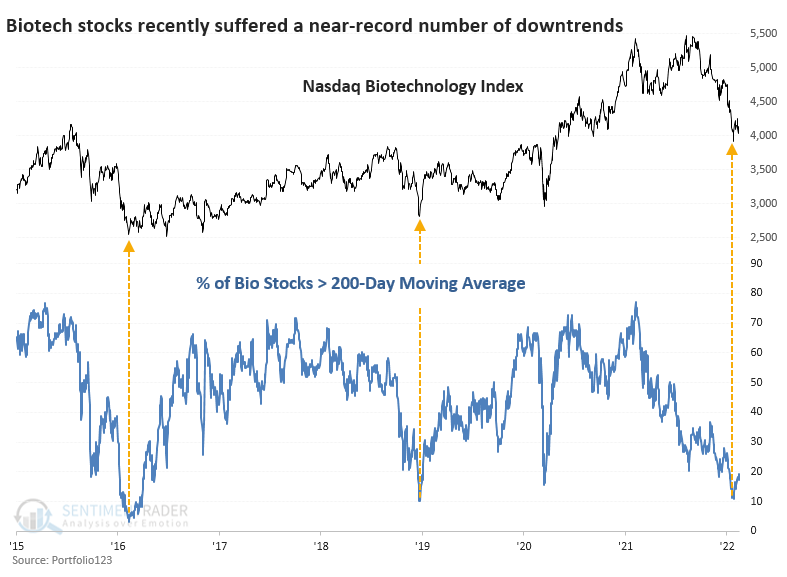

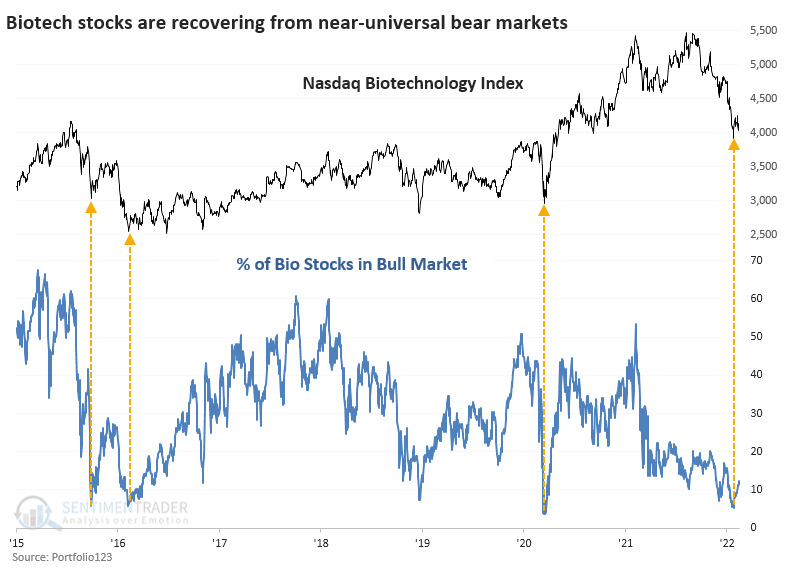

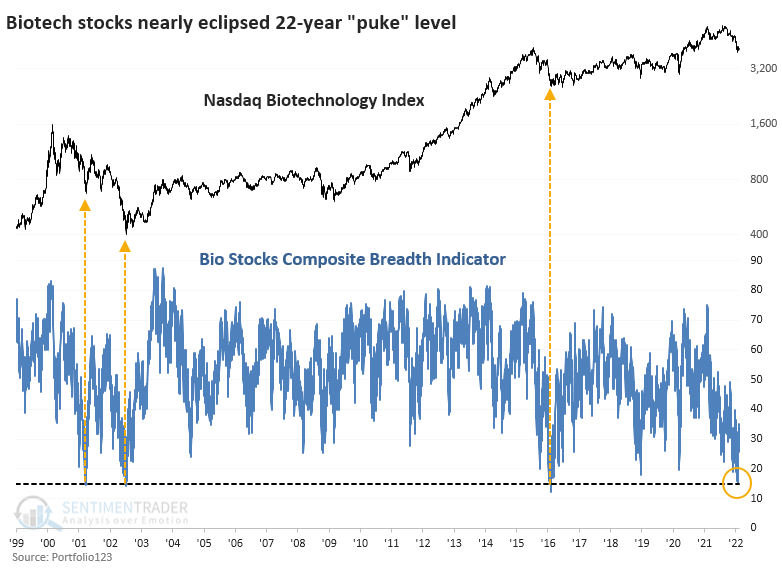

In Biotech, extreme got even more extreme

In December, we looked at the near-washout in Biotechnology stocks. As we saw with the high level of stocks in the Nasdaq cut in half, many of those were in Health Care, specifically Biotechnology.

It turns out it wasn't quite the washout. Sellers returned in force and pushed the stocks to lower lows. That false bottom in December triggered several new extremes now attempting a reversal.

Touching on some of the longer-term metrics we looked at in December, fewer than 10% of the stocks managed to hold above their 200-day moving averages at the worst point last month. Only the cascading declines in 2016 and 2018 matched this in recent years.

That selling pressure pushed more than 95% of the stocks into bear markets - more than 20% off their peaks. Again, that level of wholesale and heavy pressure has been matched only a few times in recent years.

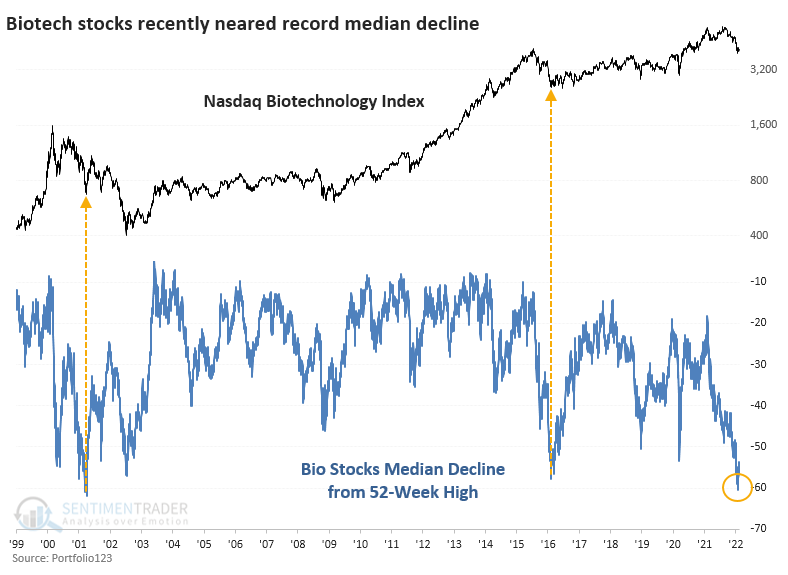

Even more notably, the median decline these stocks suffered was so massive that we need to go back to at least 1999 to see similar behavior. Near the end of January, the average Biotech stock had lost more than 60% of its value from its 52-week high. The only dates that exceeded this were a couple in late March and early April 2001. It got close in February 2016 when the median drawdown reached -57%.

Aggregate breadth reached a historic extreme and is trying to recover

The chart below shows the overall breadth composite we looked at in December. It dropped below 15% in late January, which matches the lowest readings in 23 years, on par with March 2001, July 2002, and February 2016.

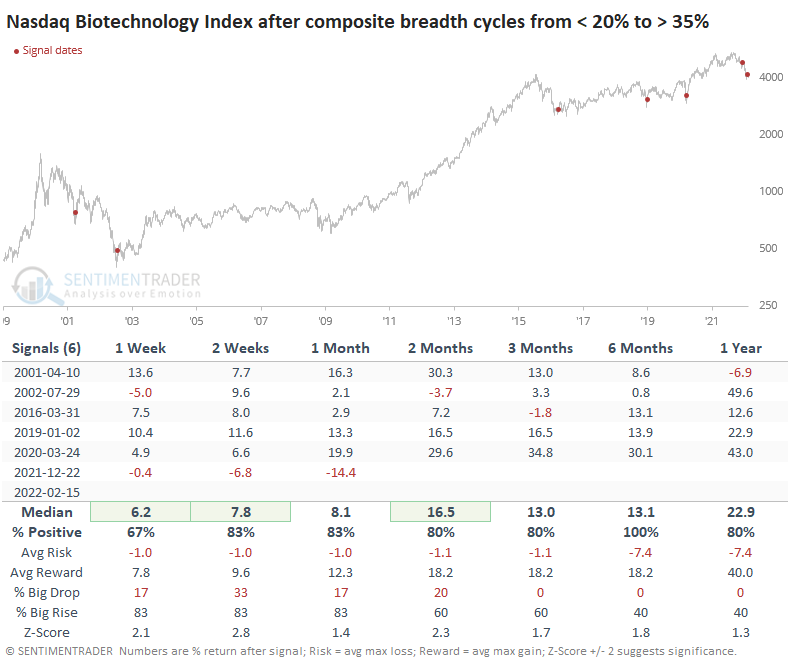

The table below shows every time the composite fell below 20% and then recovered above 35%, which it just did. Returns in the months ahead were excellent, though that terrible December failure shows up.

What the research tells us...

There was a reasonable basis to expect long-term returns to be positive for Biotechnology in mid-December. This was one of those times when extreme got even more extreme, and anyone who was early is sitting on significant losses. Now there has been another round of extremes, even more profound than a couple of months ago, and on par with the very worst panics in 23 years. There has been something of a recovery, and other than December's folly, returns after similar behavior were excellent over the medium- to long-term.

Active Studies

| Time Frame | Bullish | Bearish | | Short-Term | 3 | 0 | | Medium-Term | 18 | 2 | | Long-Term | 15 | 5 |

|

Indicators at Extremes

Portfolio

| Position | Description | Weight % | Added / Reduced | Date | | Stocks | RSP | 21.4 | Added 10.2% | 2022-01-28 | | Bonds | 32.7% BND, 7.1% SCHP | 40.1 | Added 8.3% | 2021-10-26 | | Commodities | GCC | 2.4 | Reduced 2.1%

| 2020-09-04 | | Precious Metals | GDX | 4.6 | Reduced 4.2% | 2021-05-19 | | Special Situations | 8.1% KWEB, 3.6% XLE, 1.7% PSCE | 13.4 | Reduced 3.9% | 2022-01-18 | | Cash | | 17.9 | | |

|

Updates (Changes made today are underlined)

With a typical time frame of several months in this account, I normally don't make changes so quickly. I've added back part of the stock exposure I took off earlier in January due to the washed-out conditions and extreme pessimism we're seeing across a wide array of metrics. The biggest issue is that the environment is unhealthy and we could be in the throes of a protracted bear market. Even so, the readings we've seen recently have a good record at preceding relief rallies, so we'll have to see how that pans out. Bond sentiment is trying to recover from a recent bout of pessimism, and gold stocks are doing their thing which is not much at all. They've been flat for six months. Chinese tech stocks were doing exactly what they're supposed to do, then did *not* by plunging to new lows. This is troubling on a shorter-term time frame, but this was never meant for a trade, rather a multi-year investment. Recent behavior is troubling and I will not be adding any exposure as long as that's the case. RETURN YTD: +0.1% 2021: +8.7%, 2020: +8.1%, 2019: +12.6%, 2018: +0.6%, 2017: +3.8%, 2016: +17.1%, 2015: +9.2%, 2014: +14.5%, 2013: +2.2%, 2012: +10.8%, 2011: +16.5%, 2010: +15.3%, 2009: +23.9%, 2008: +16.2%, 2007: +7.8%

|

|

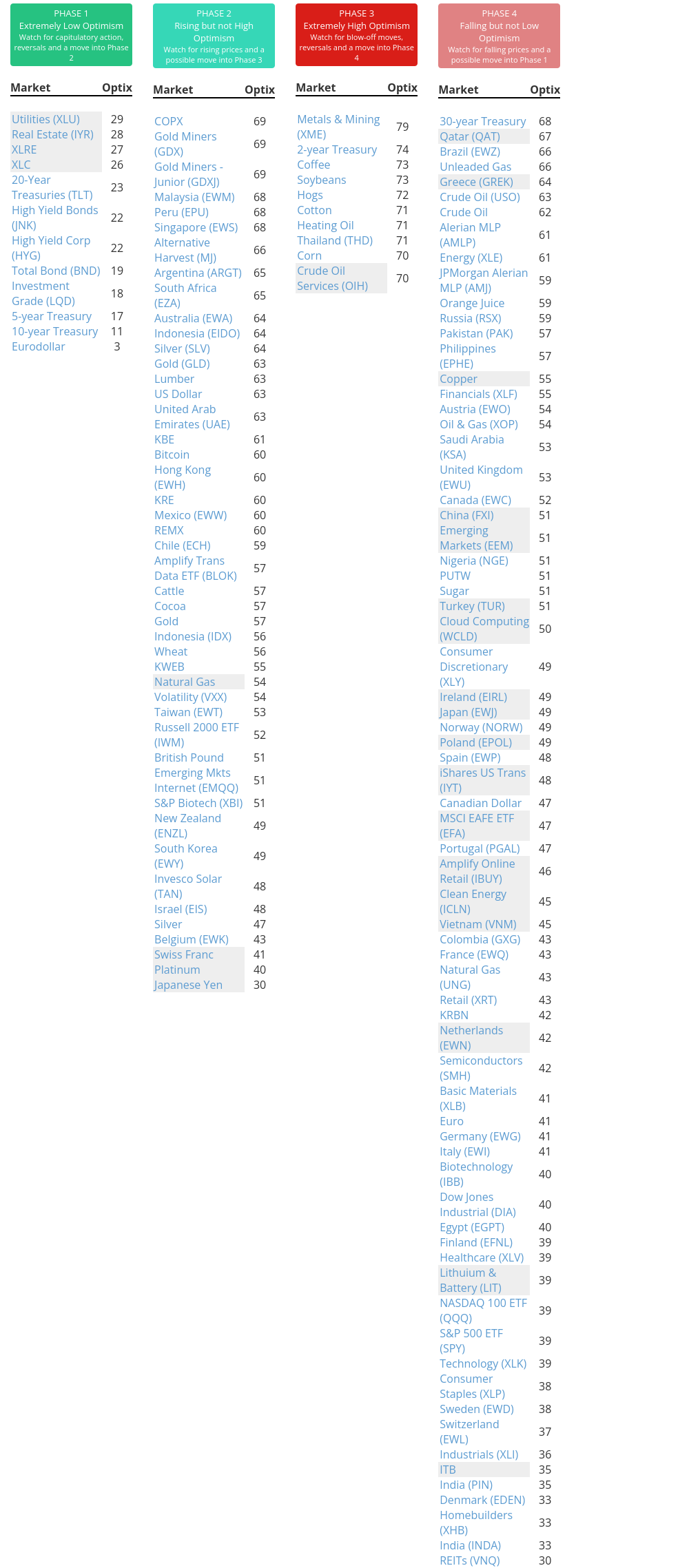

Phase Table

Ranks

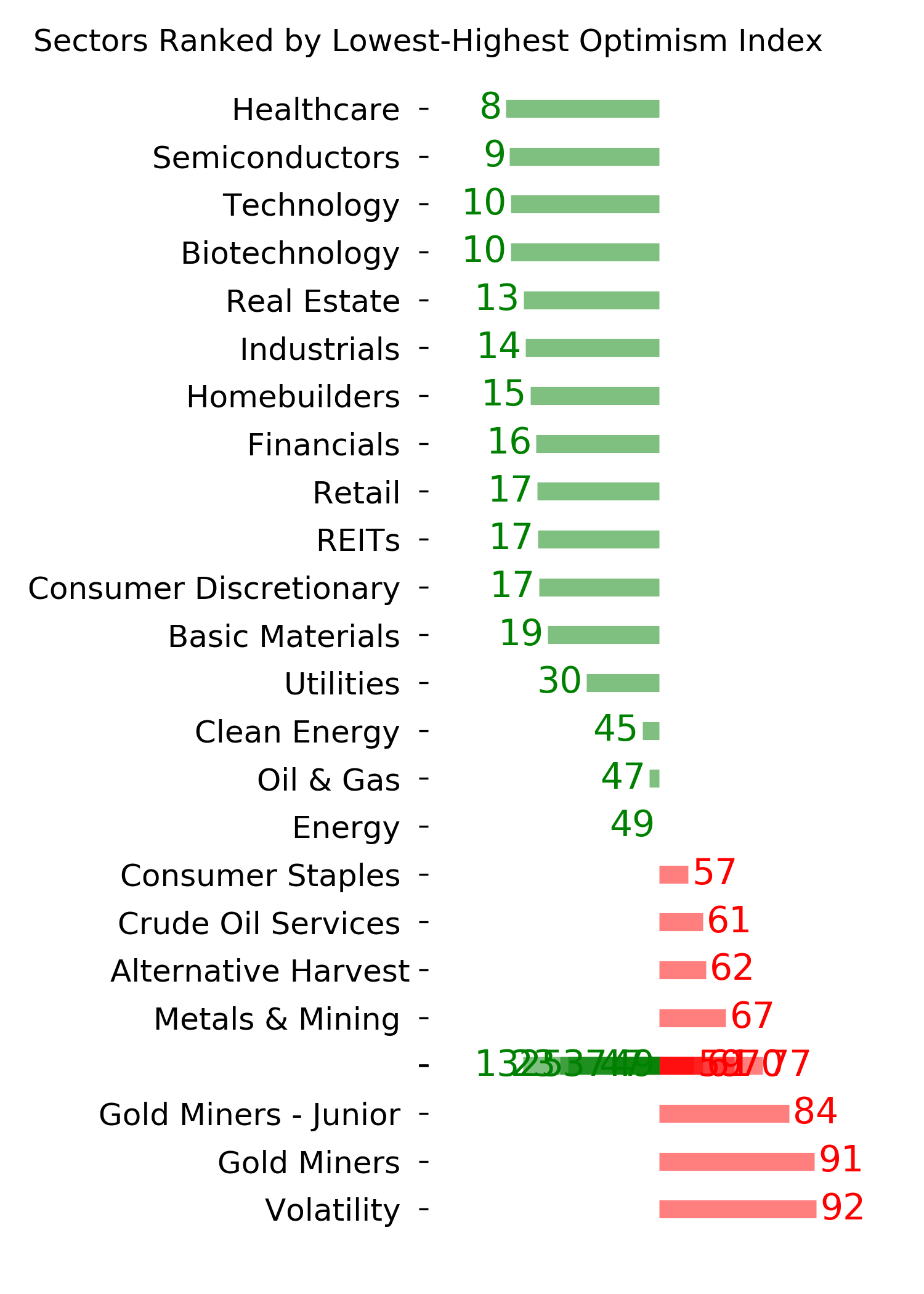

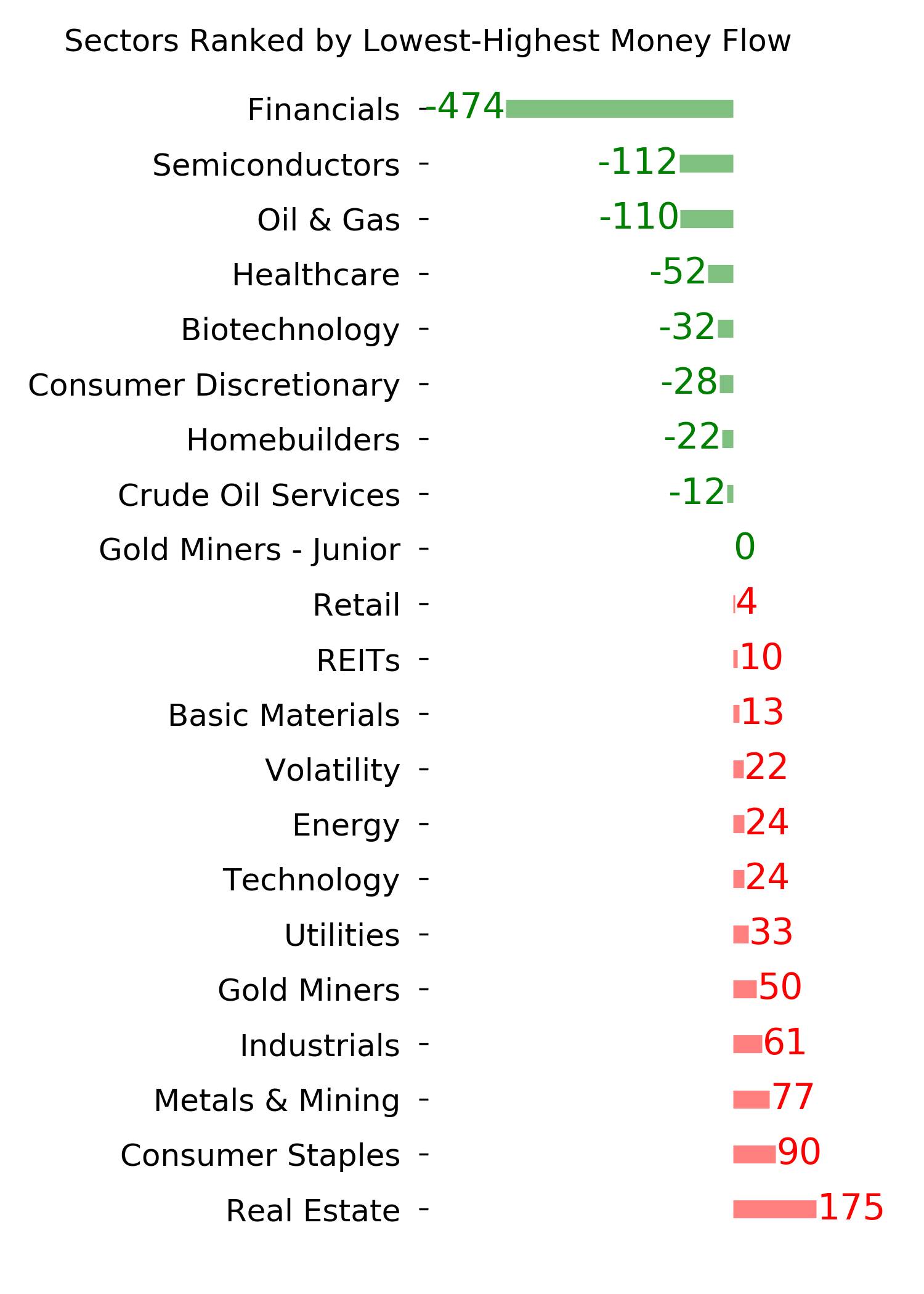

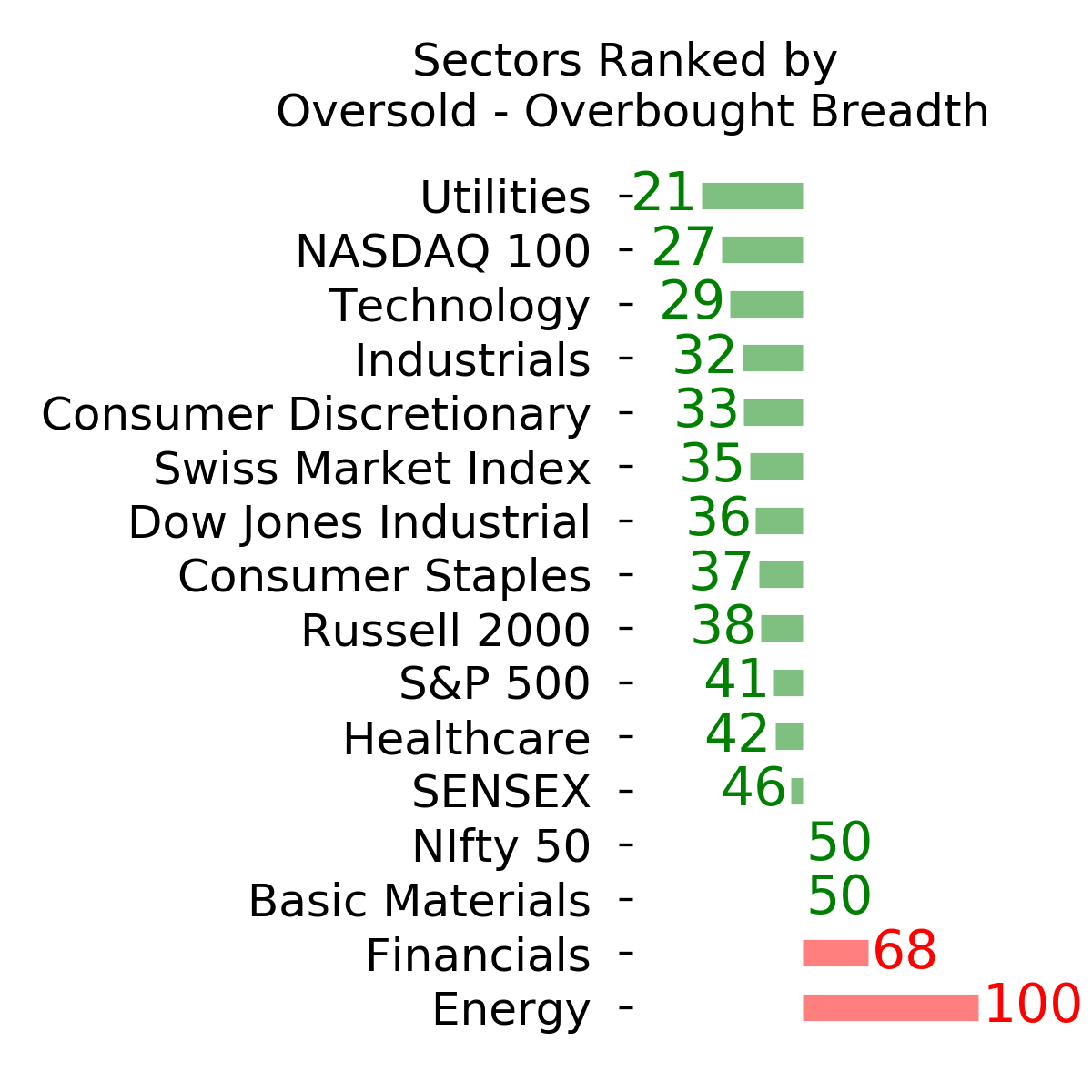

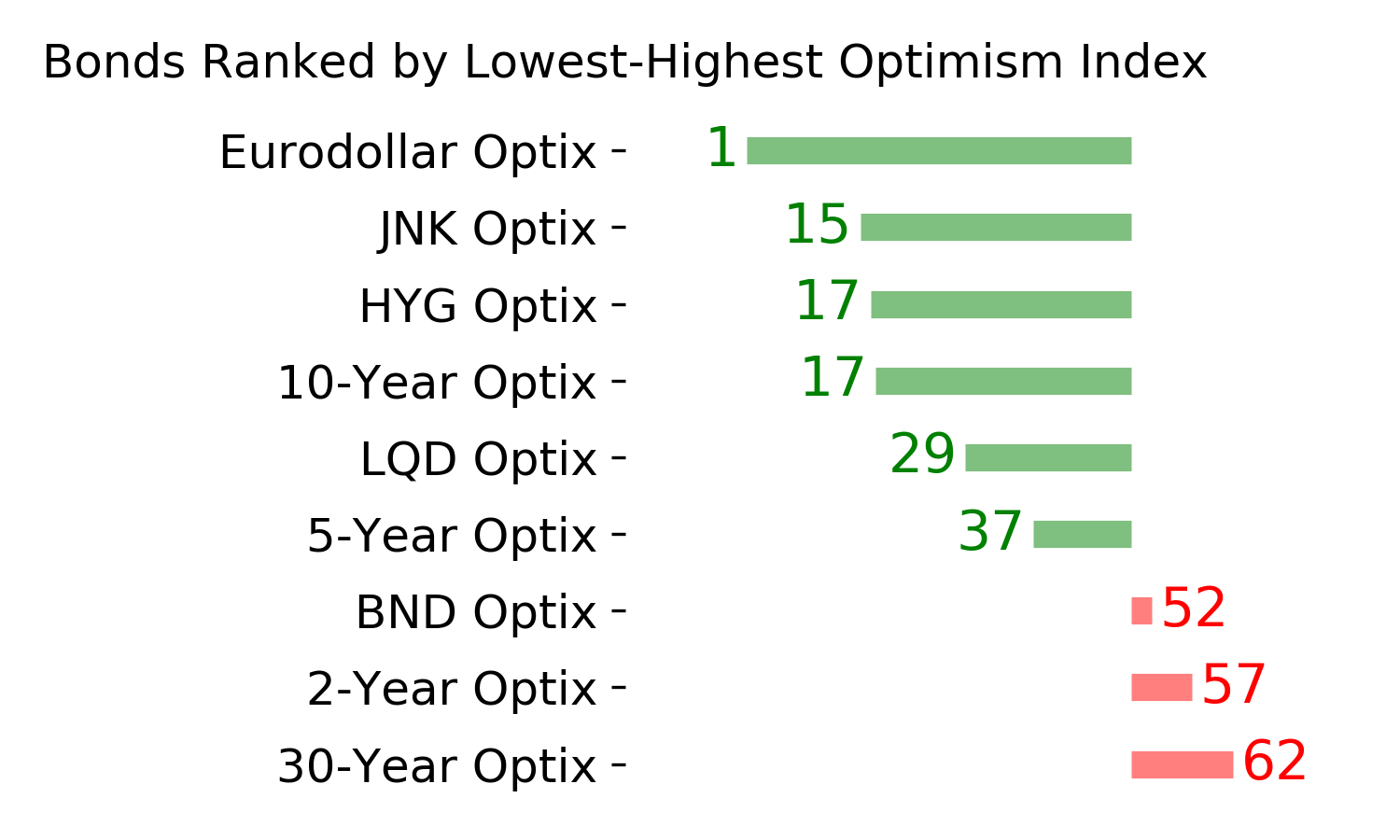

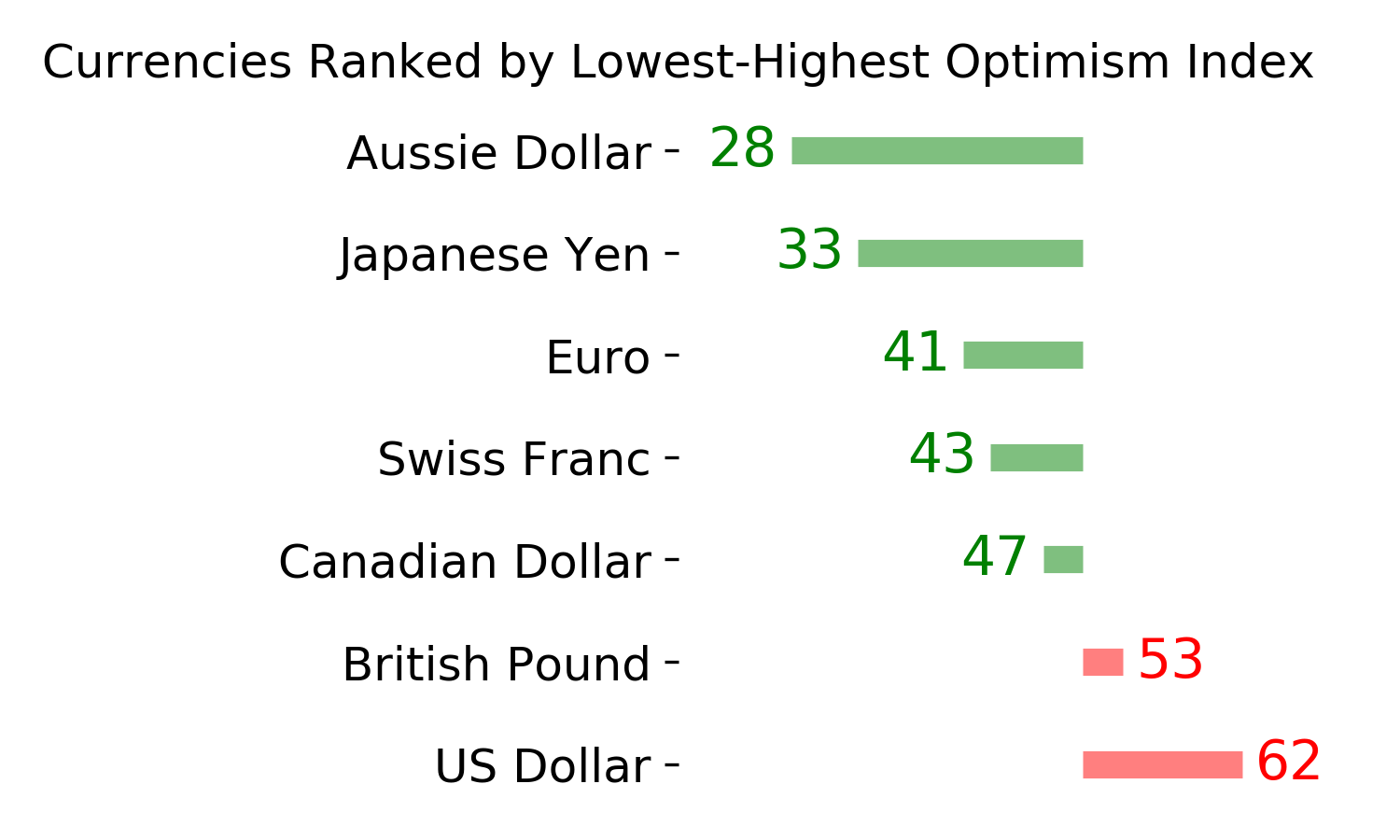

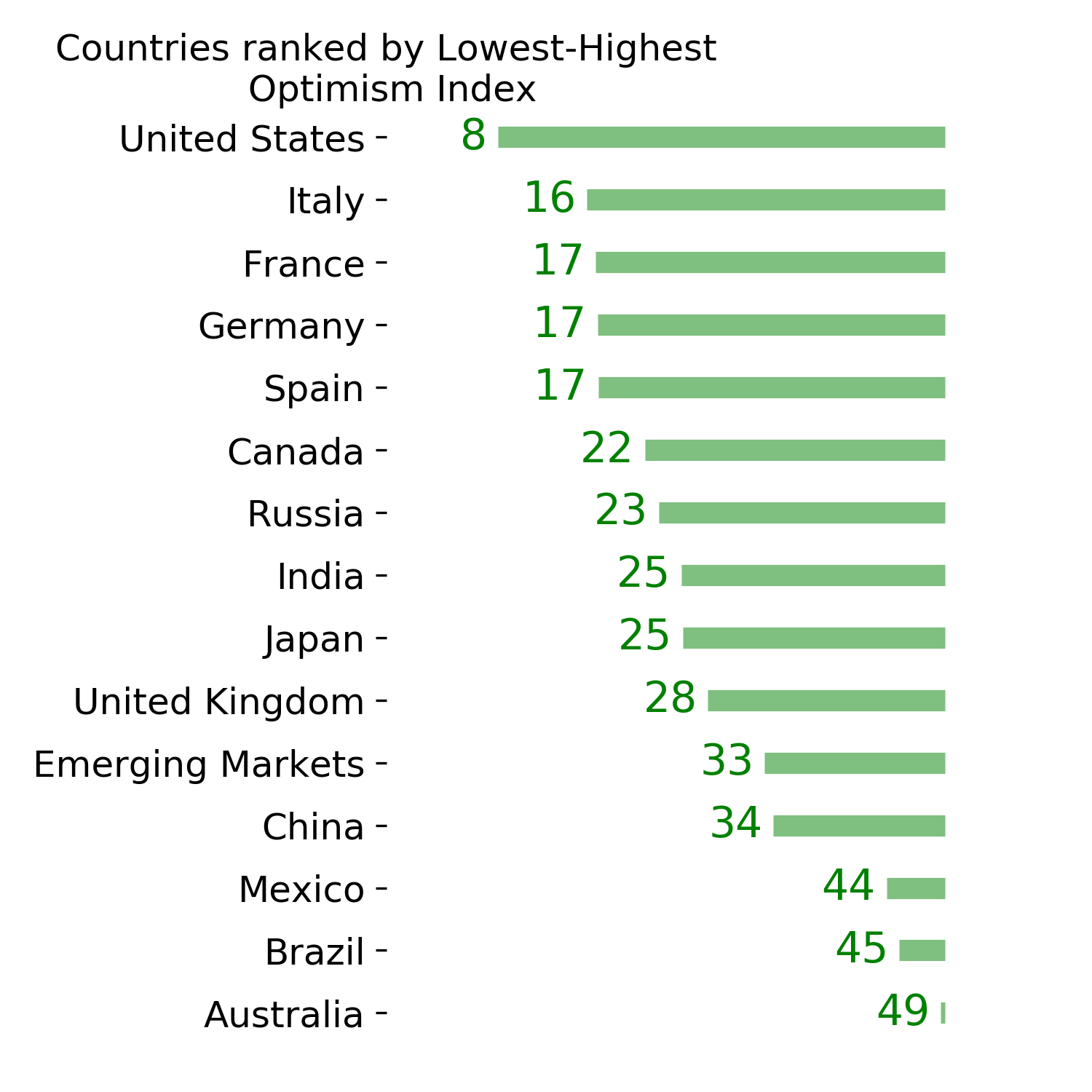

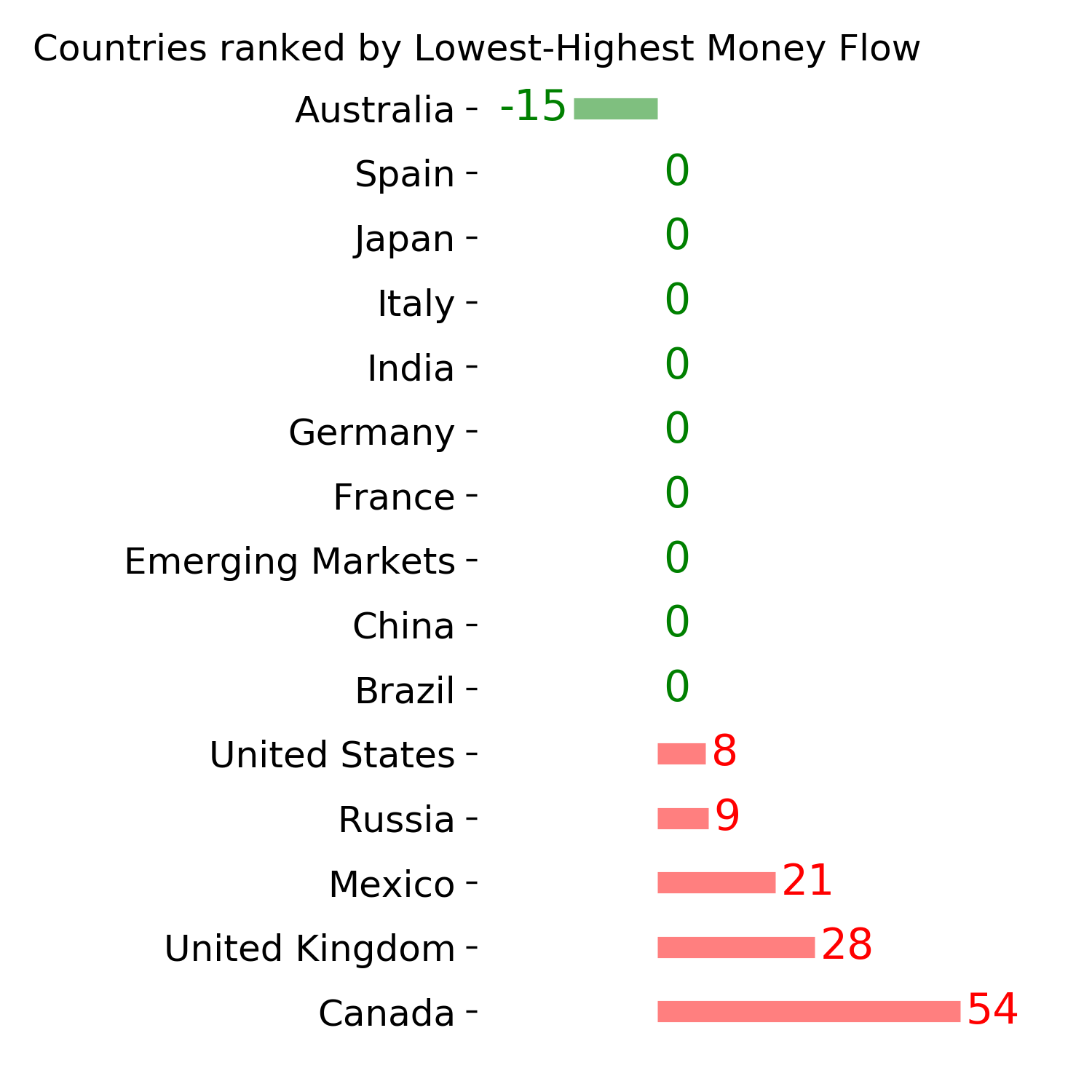

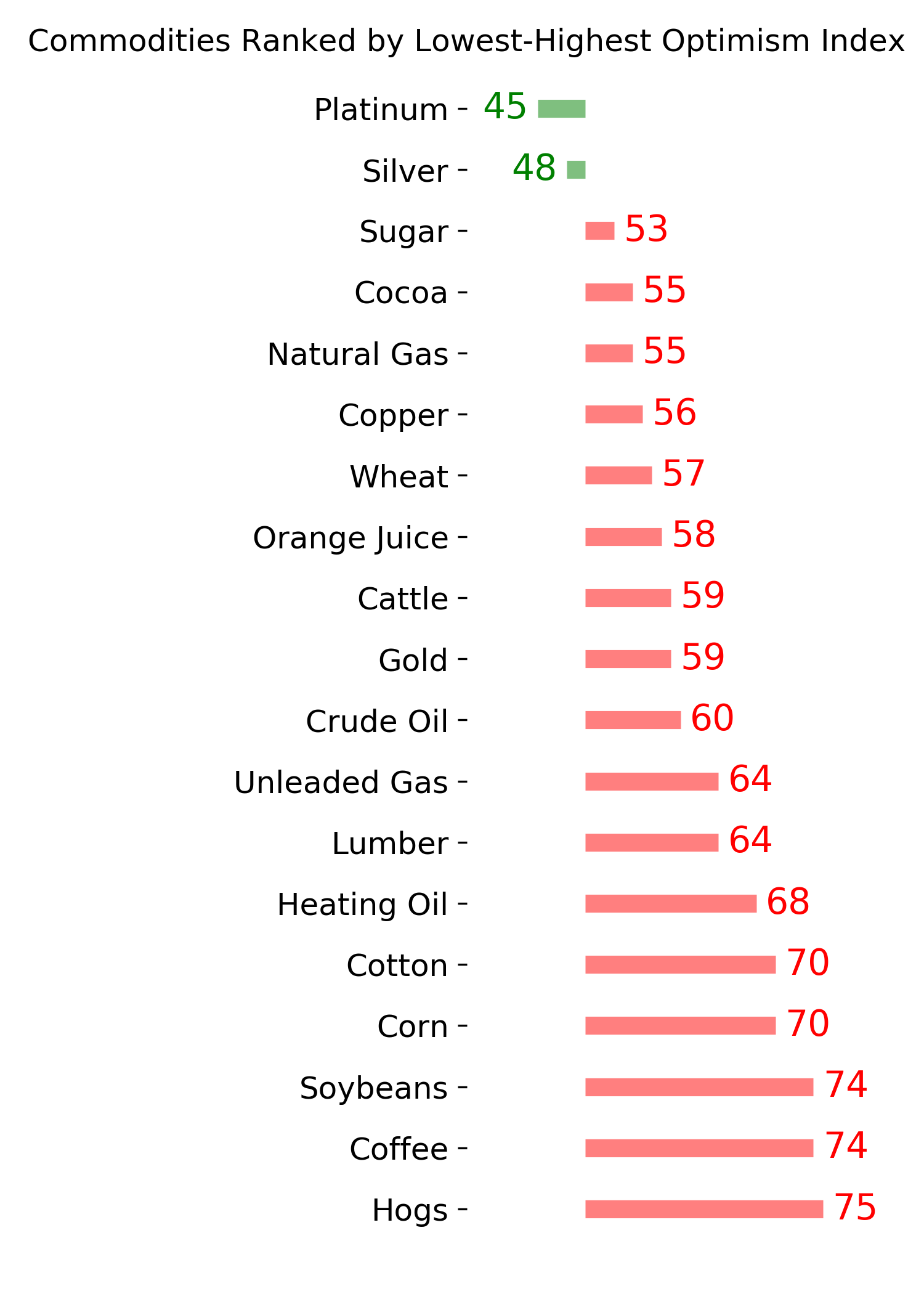

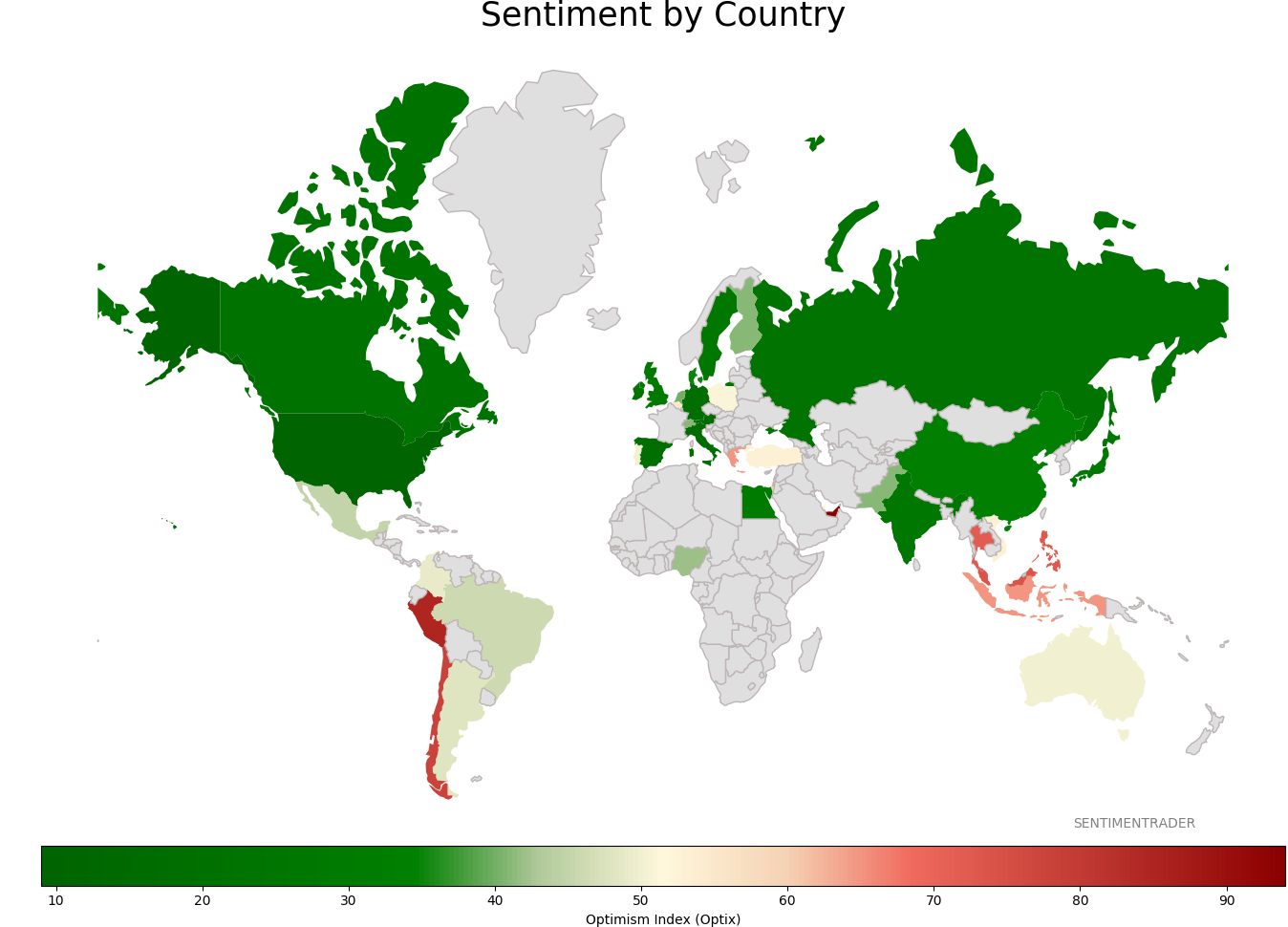

Sentiment Around The World

Optimism Index Thumbnails

|

Sector ETF's - 10-Day Moving Average

|

|

|

Country ETF's - 10-Day Moving Average

|

|

|

Bond ETF's - 10-Day Moving Average

|

|

|

Currency ETF's - 5-Day Moving Average

|

|

|

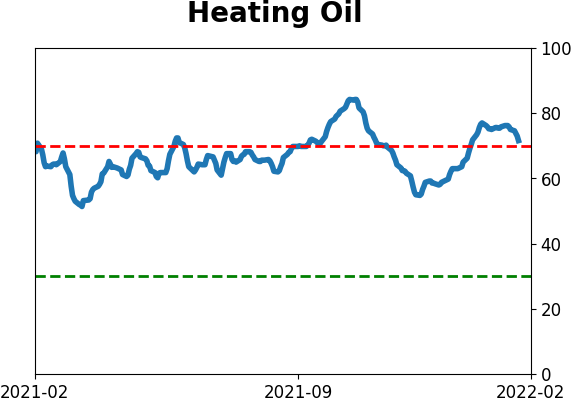

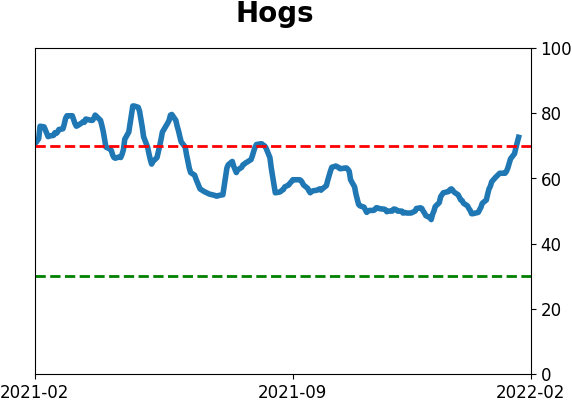

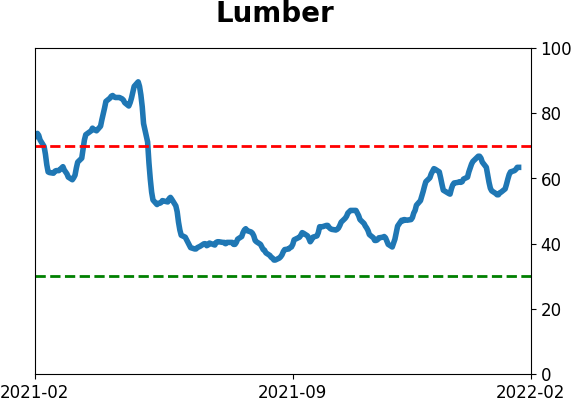

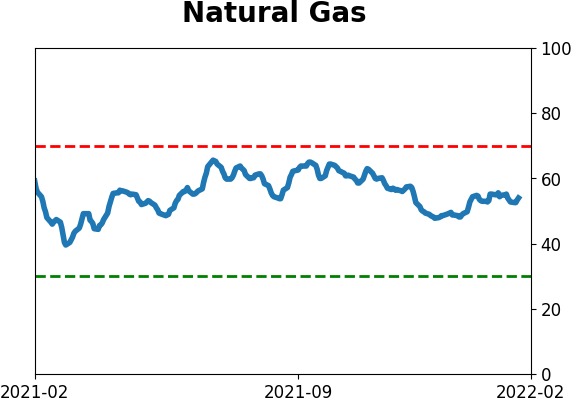

Commodity ETF's - 5-Day Moving Average

|

|