Headlines

|

|

Traders show more concern in bonds than stocks:

The VIX "fear gauge" has dropped more than 25% from its 52-week high, showing equity investors see less risk ahead. But some measures of bond market "fear" remain elevated, nearing their highest level in a year. Similar behavior between the markets preceded some large losses in stocks, but those were more the exception than the rule.

|

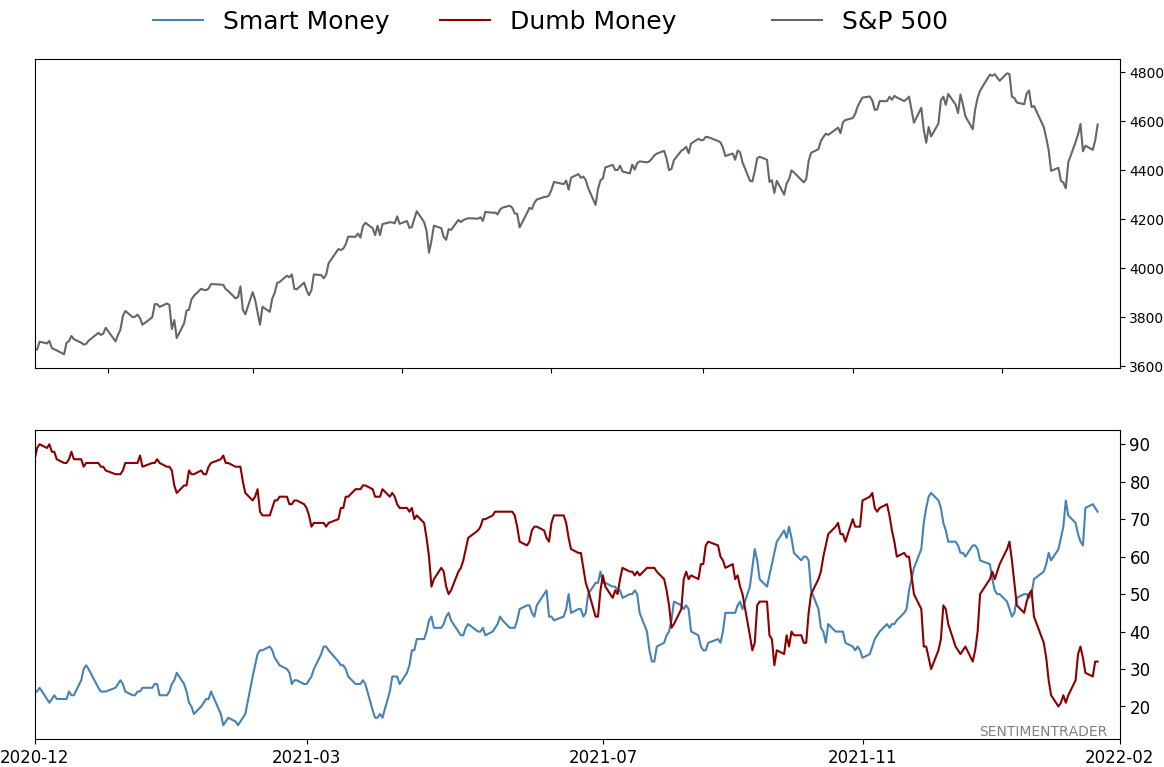

Smart / Dumb Money Confidence

|

Smart Money Confidence: 72%

Dumb Money Confidence: 32%

|

|

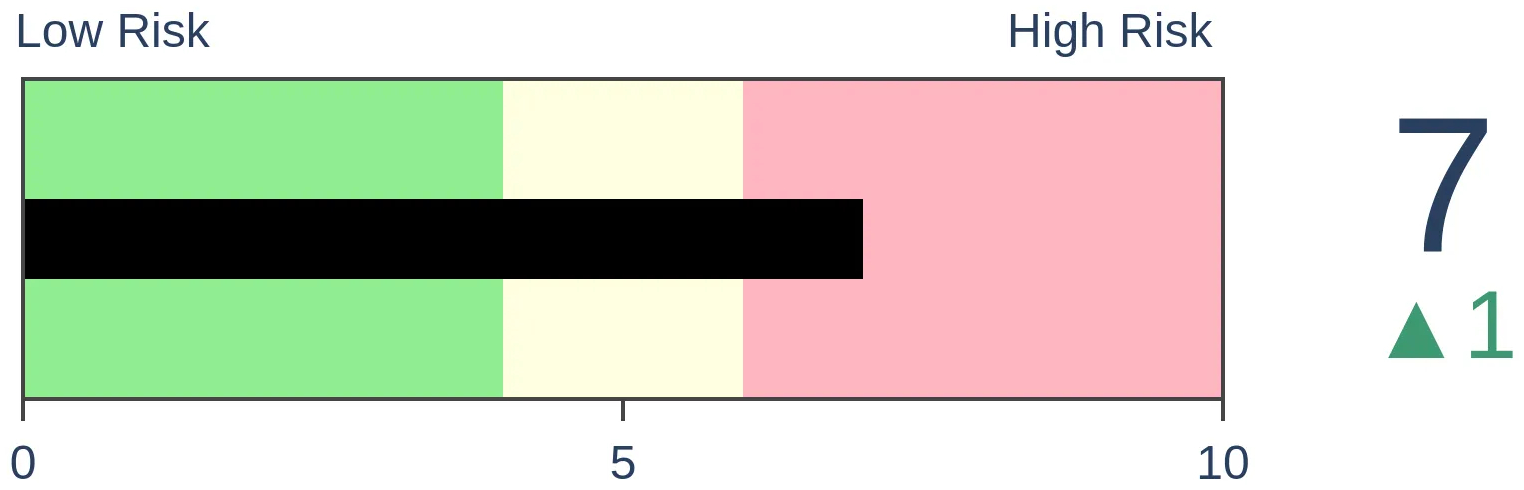

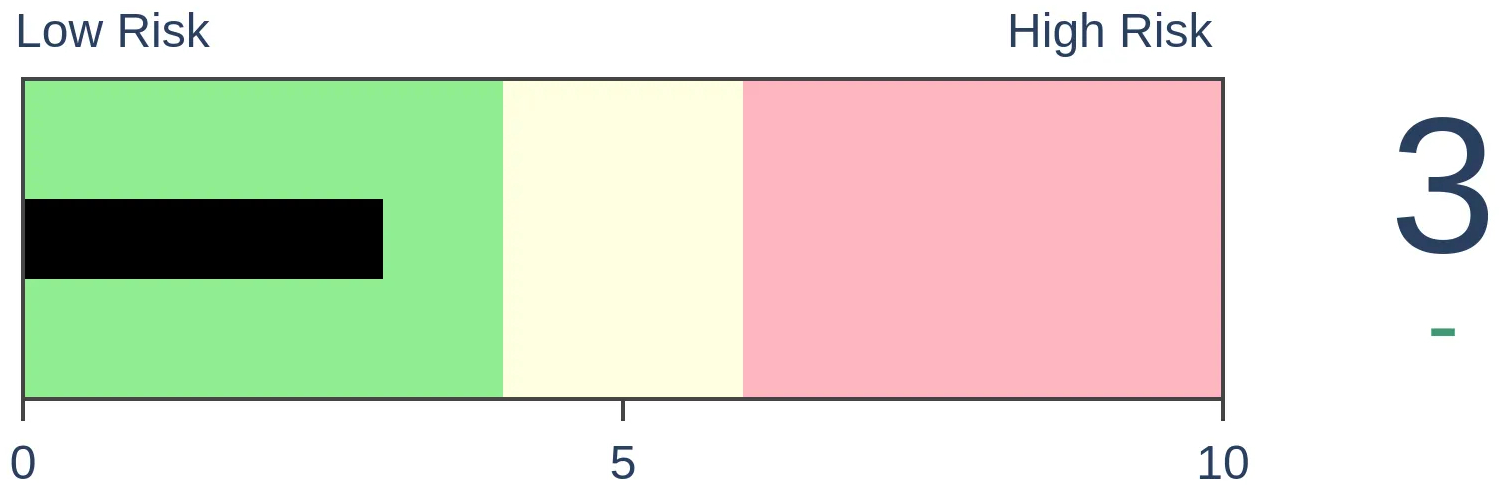

Risk Levels

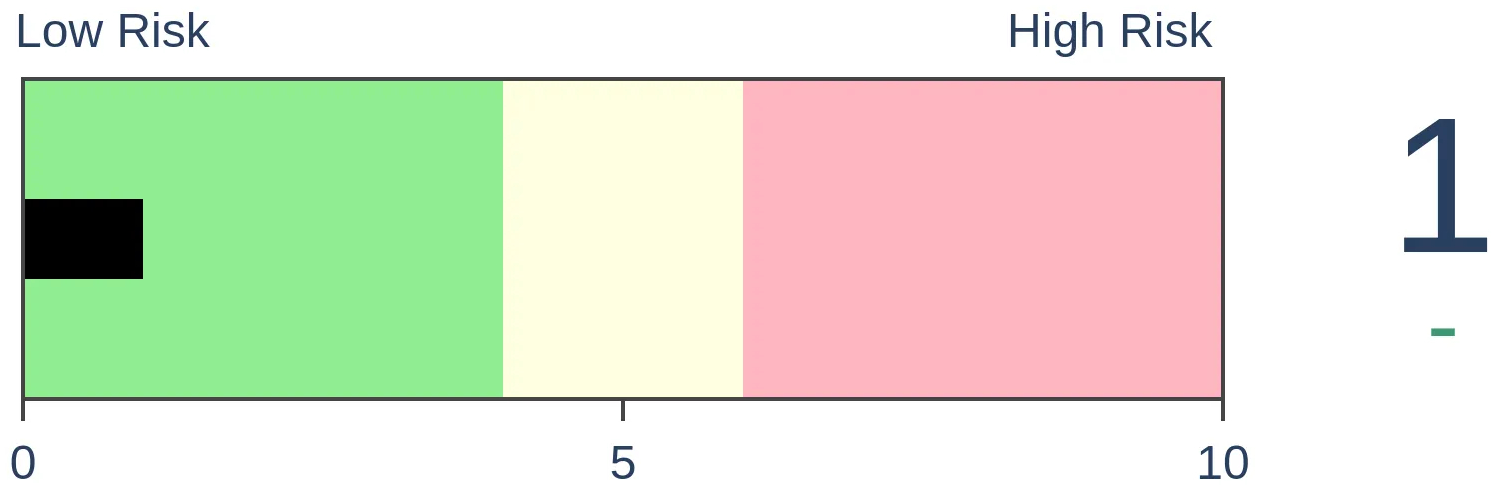

Stocks Short-Term

|

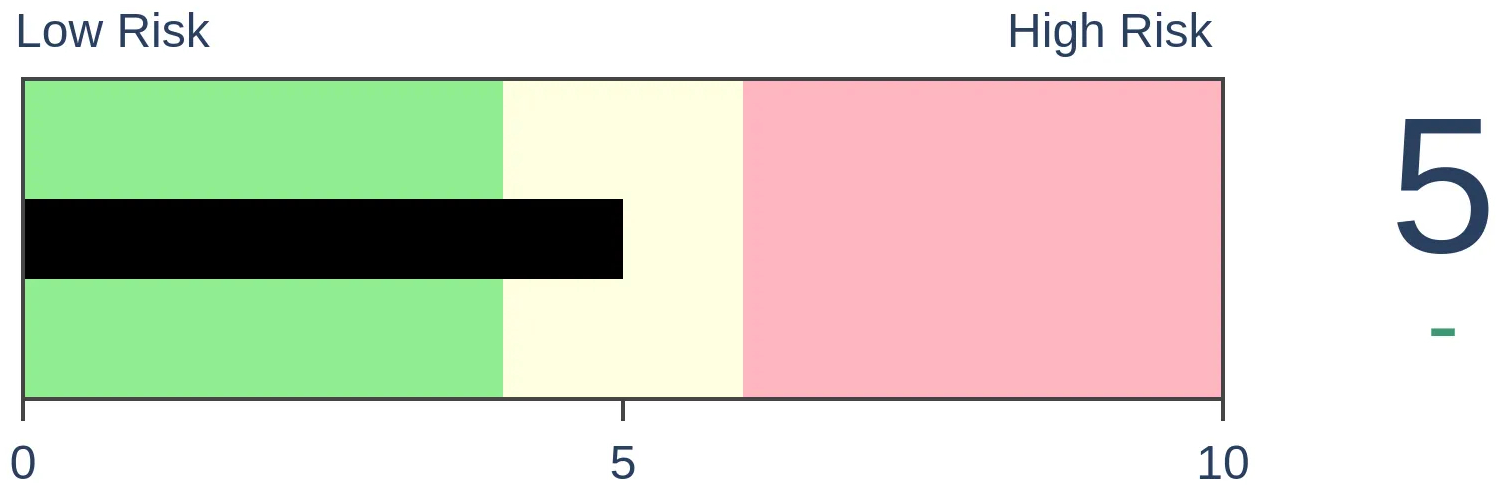

Stocks Medium-Term

|

|

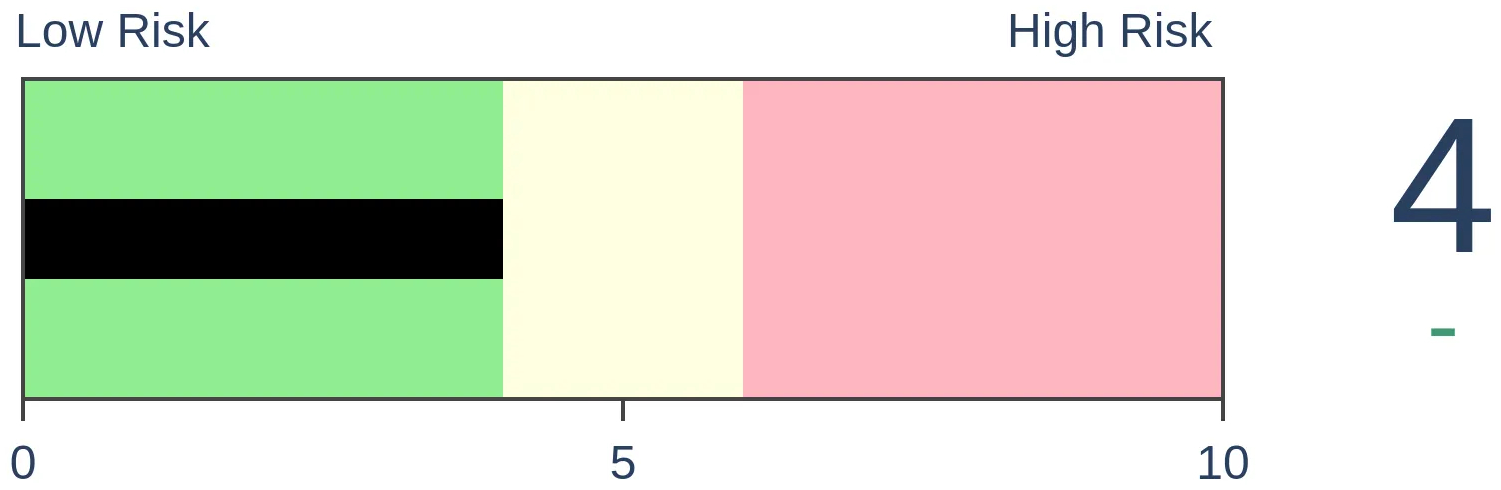

Bonds

|

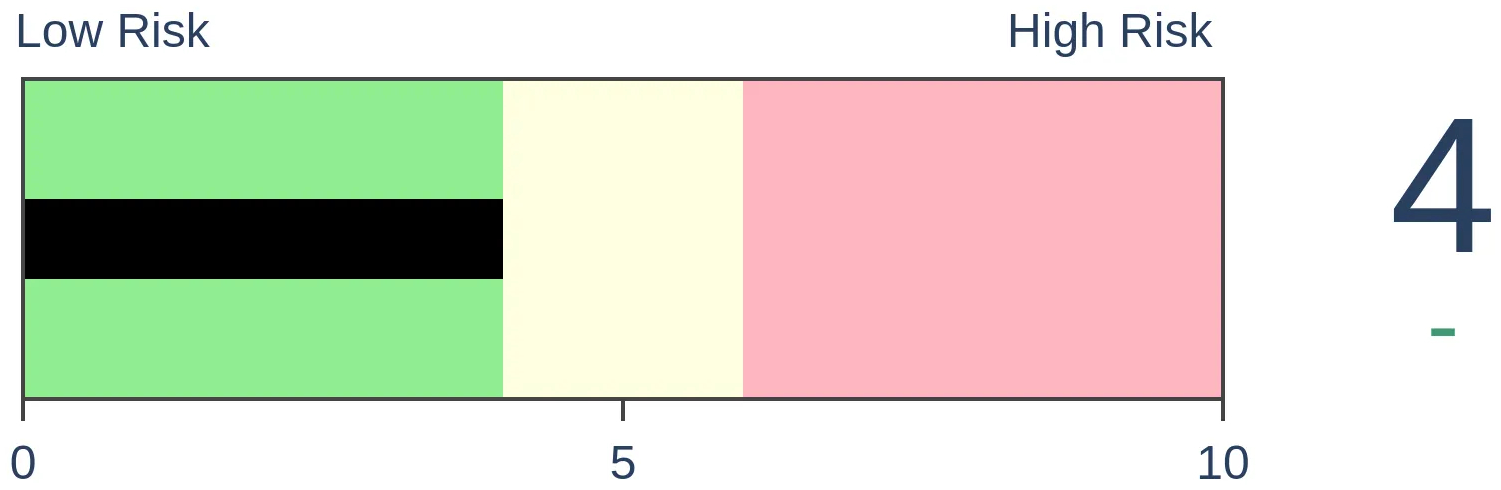

Crude Oil

|

|

Gold

|

Agriculture

|

|

Research

By Jason Goepfert

BOTTOM LINE

The VIX "fear gauge" has dropped more than 25% from its 52-week high, showing equity investors see less risk ahead. But some measures of bond market "fear" remain elevated, nearing their highest level in a year. Similar behavior between the markets preceded some large losses in stocks, but those were more the exception than the rule.

FORECAST / TIMEFRAME

None

|

Key points:

- The VIX has dropped more than 25% from its high

- At the same time, bond market "fear" has remained elevated, near 52-week highs

- Similar behavior preceded some significant declines in stocks, but those were the exceptions

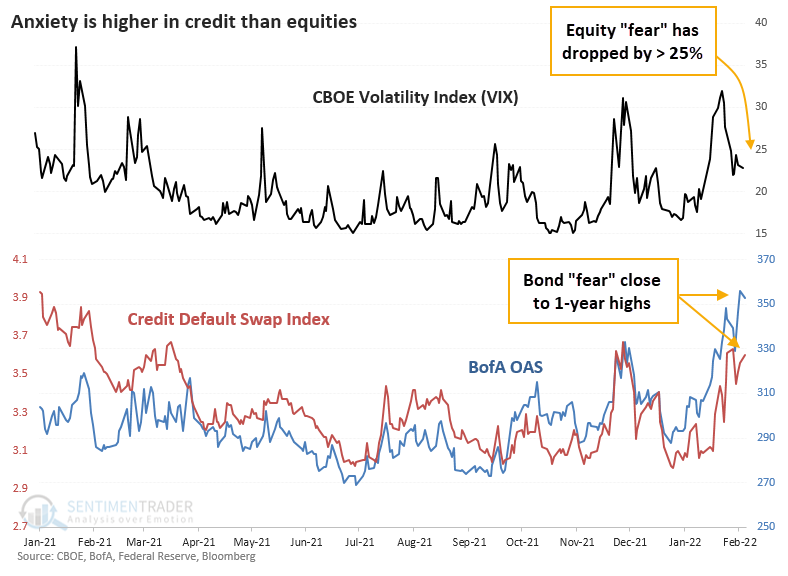

Bond market fear nears 1-year highs as equity market fear drops

We saw on Monday that investors have picked up their hedging activity. One of those metrics was their willingness to pay more for protection against a major credit event.

An alternative measure of this concern, with a longer history, is option-adjusted credit spreads. Bond traders will cringe at this, but if we use CDX spreads or option-adjusted spreads as a sign of bond market "fear", they're just off their 52-week highs. But equity market "fear" via the VIX is down by more than 25%.

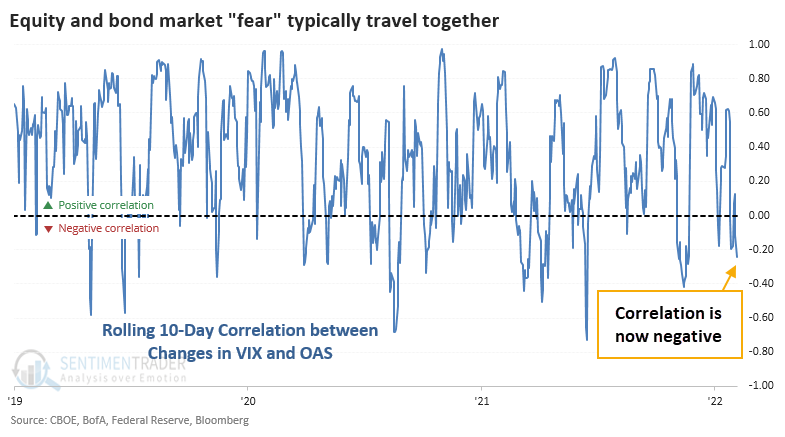

It's relatively rare to see these equity and bond metrics diverge for long. The chart below shows a 10-day rolling correlation between daily changes in the VIX and option-adjusted spreads. Over the past few years, it has spent 82% of the time in positive territory. The current reading is in the bottom 7% of readings.

A market clichè is that the bond market is smarter. We've looked at that from dozens of different directions over the decades, and there is no clear edge one way or the other. Sometimes, bond traders panic just as foolishly (in hindsight) as stock traders.

Similar bond vs. stock market "fear" showed gains for stocks...with a caveat

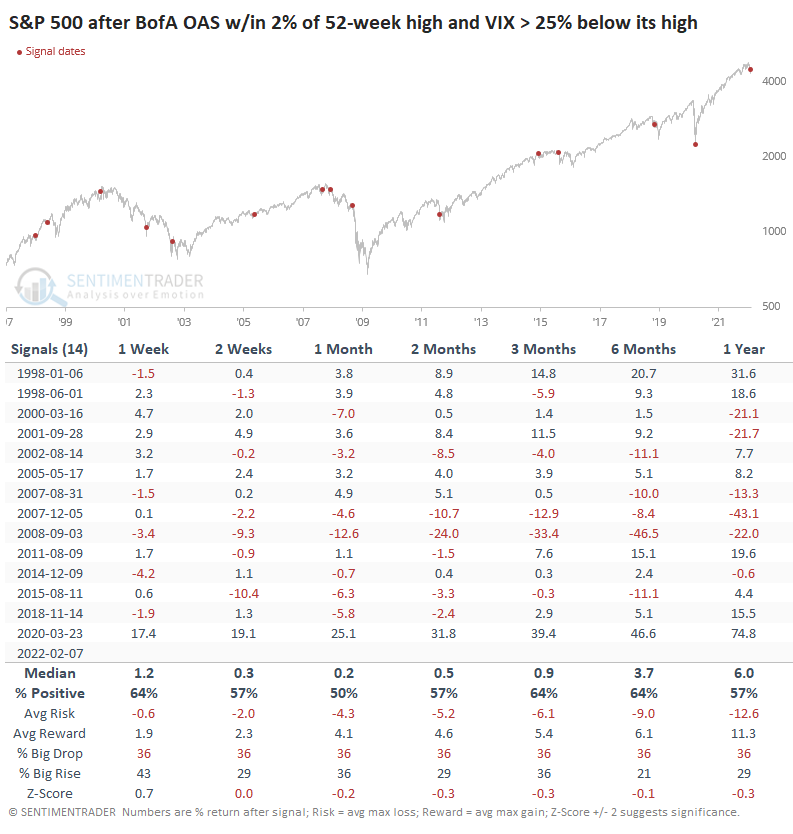

To see if there's anything to this current situation of elevated bond market fear while stock investors see easing concerns, the table below shows all similar days since 1997.

Several times, concern in the bond market was a good tip-off that stock investors weren't pricing in enough risk. Near the market peaks in 2000, 2007, and 2015, we saw a divergence like this, leading to large losses in the S&P 500. Most of the time, though, the S&P rose in the weeks and months ahead. Its median return was below average but still positive.

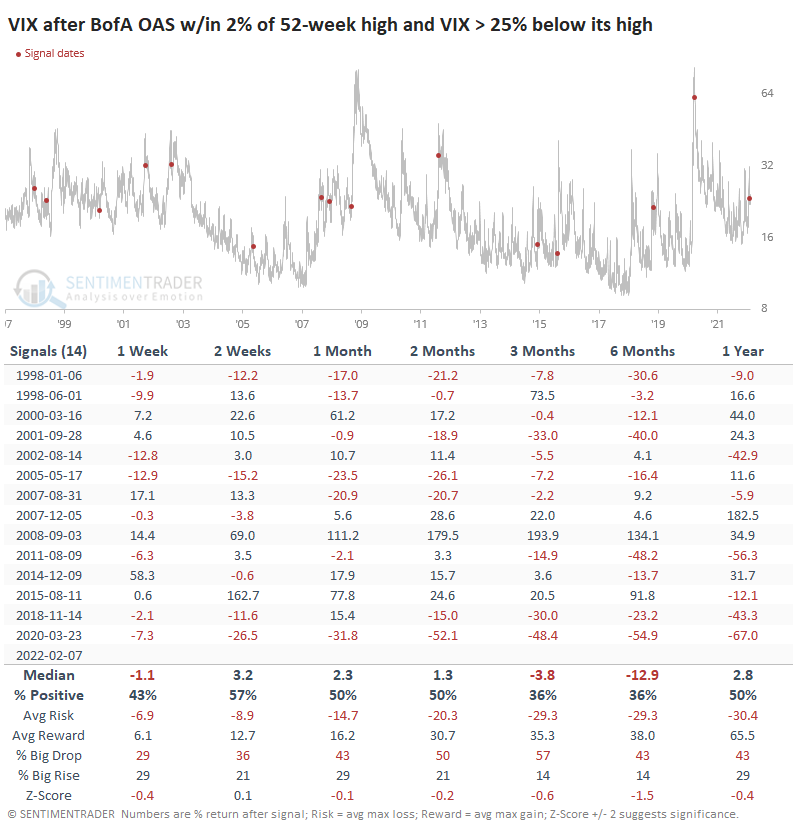

For the VIX, it was not a consistent enough signal suggesting it would spike. Over the next 3-6 months, the VIX rose after only 5 of the 14 signals.

What the research tells us...

With the market environment currently unhealthy, we're constantly looking for signs that the recent recovery from pessimism will fail. That's what unhealthy markets do. The rise in concern in the bond market is a potential tip-off that stock investors are too complacent, with some supporting evidence from prior peaks. But it has not been a consistent enough signal to suggest we dismiss the recent positives over a medium-term time frame.

Active Studies

| Time Frame | Bullish | Bearish | | Short-Term | 3 | 0 | | Medium-Term | 17 | 2 | | Long-Term | 15 | 5 |

|

Indicators at Extremes

Portfolio

| Position | Description | Weight % | Added / Reduced | Date | | Stocks | RSP | 21.4 | Added 10.2% | 2022-01-28 | | Bonds | 32.7% BND, 7.1% SCHP | 40.1 | Added 8.3% | 2021-10-26 | | Commodities | GCC | 2.4 | Reduced 2.1%

| 2020-09-04 | | Precious Metals | GDX | 4.6 | Reduced 4.2% | 2021-05-19 | | Special Situations | 8.1% KWEB, 3.6% XLE, 1.7% PSCE | 13.4 | Reduced 3.9% | 2022-01-18 | | Cash | | 17.9 | | |

|

Updates (Changes made today are underlined)

With a typical time frame of several months in this account, I normally don't make changes so quickly. I've added back part of the stock exposure I took off earlier in January due to the washed-out conditions and extreme pessimism we're seeing across a wide array of metrics. The biggest issue is that the environment is unhealthy and we could be in the throes of a protracted bear market. Even so, the readings we've seen recently have a good record at preceding relief rallies, so we'll have to see how that pans out. Bond sentiment is trying to recover from a recent bout of pessimism, and gold stocks are doing their thing which is not much at all. They've been flat for six months. Chinese tech stocks were doing exactly what they're supposed to do, then did *not* by plunging to new lows. This is troubling on a shorter-term time frame, but this was never meant for a trade, rather a multi-year investment. Recent behavior is troubling and I will not be adding any exposure as long as that's the case. RETURN YTD: +0.8% 2021: +8.7%, 2020: +8.1%, 2019: +12.6%, 2018: +0.6%, 2017: +3.8%, 2016: +17.1%, 2015: +9.2%, 2014: +14.5%, 2013: +2.2%, 2012: +10.8%, 2011: +16.5%, 2010: +15.3%, 2009: +23.9%, 2008: +16.2%, 2007: +7.8%

|

|

Phase Table

Ranks

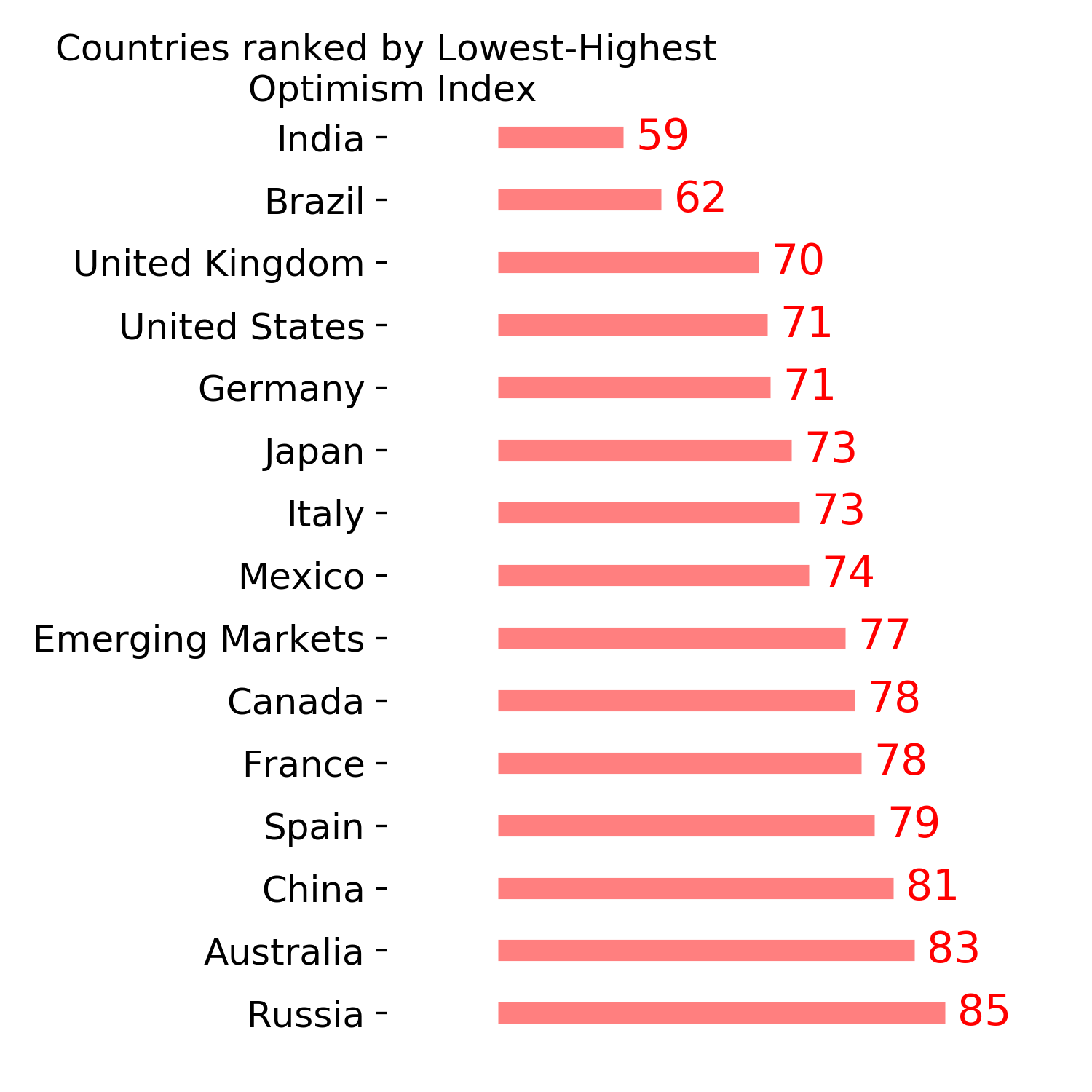

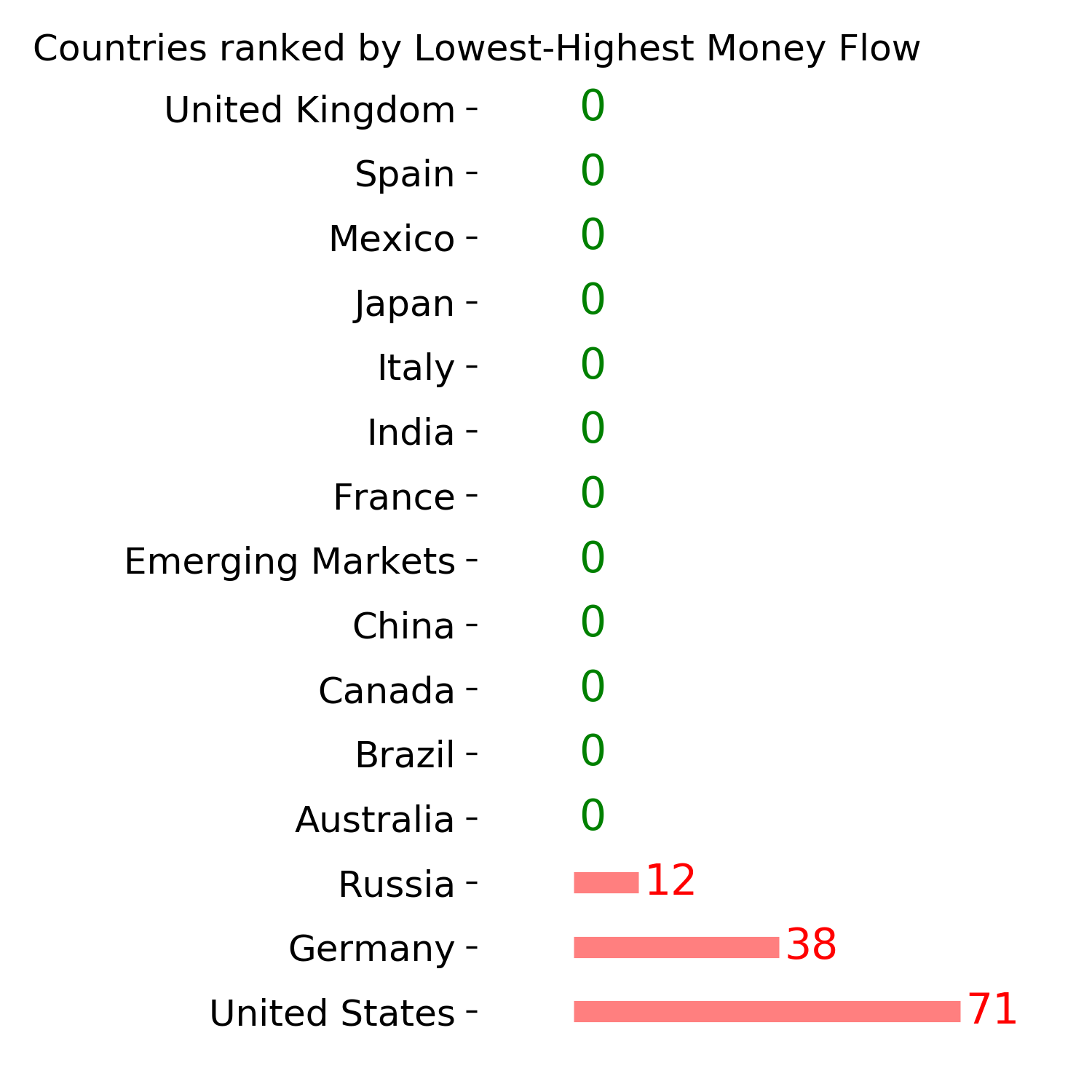

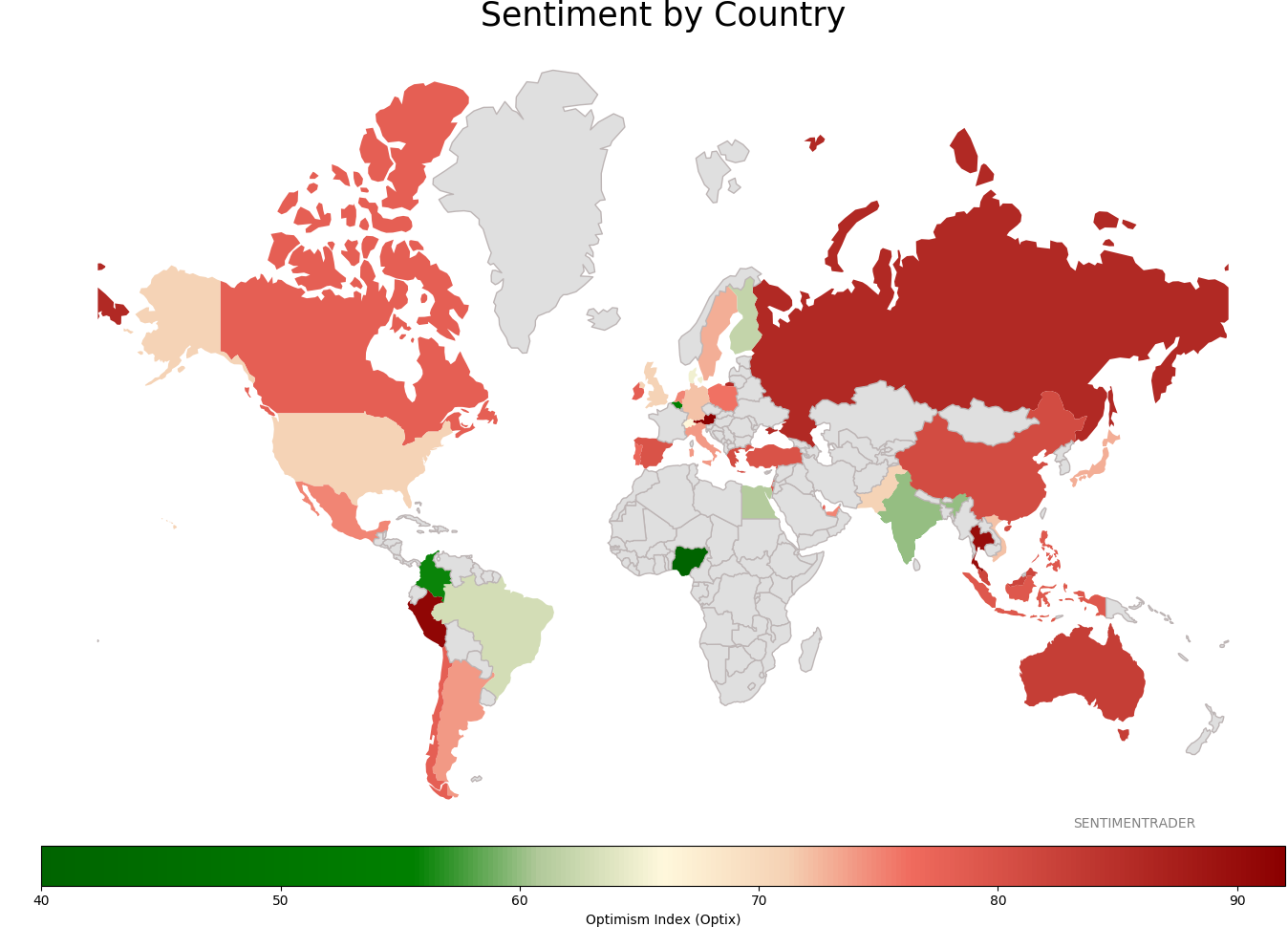

Sentiment Around The World

Optimism Index Thumbnails

|

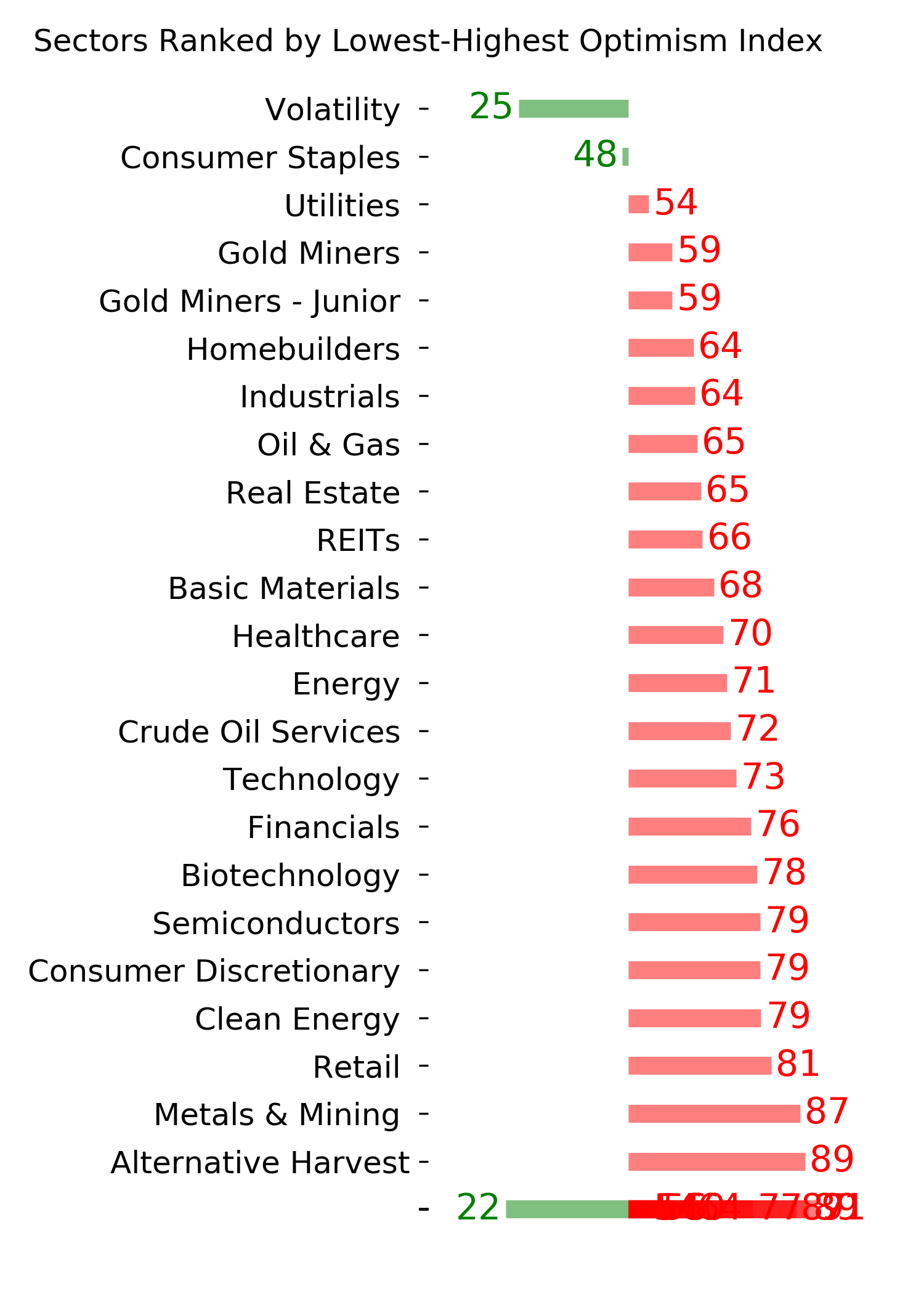

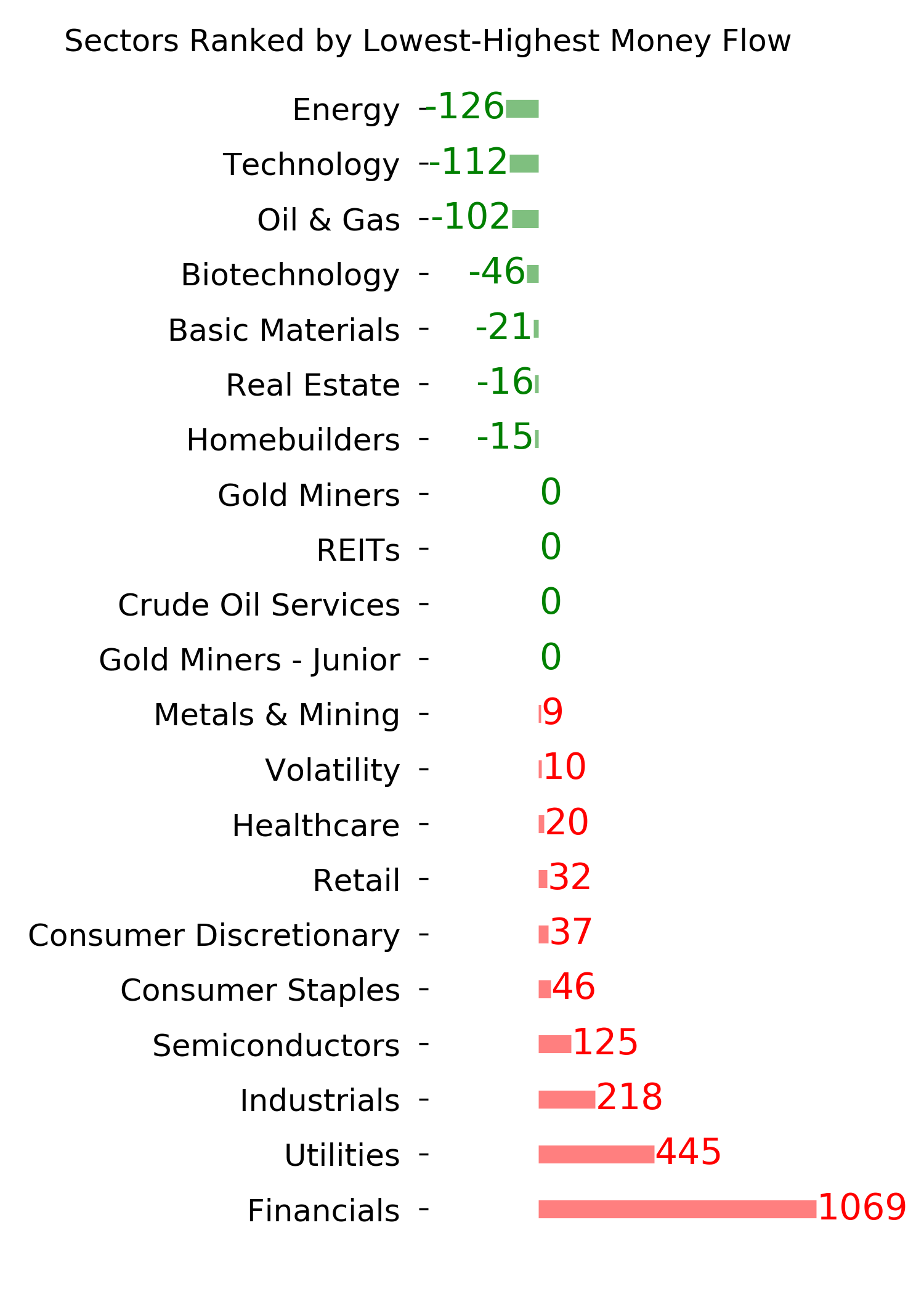

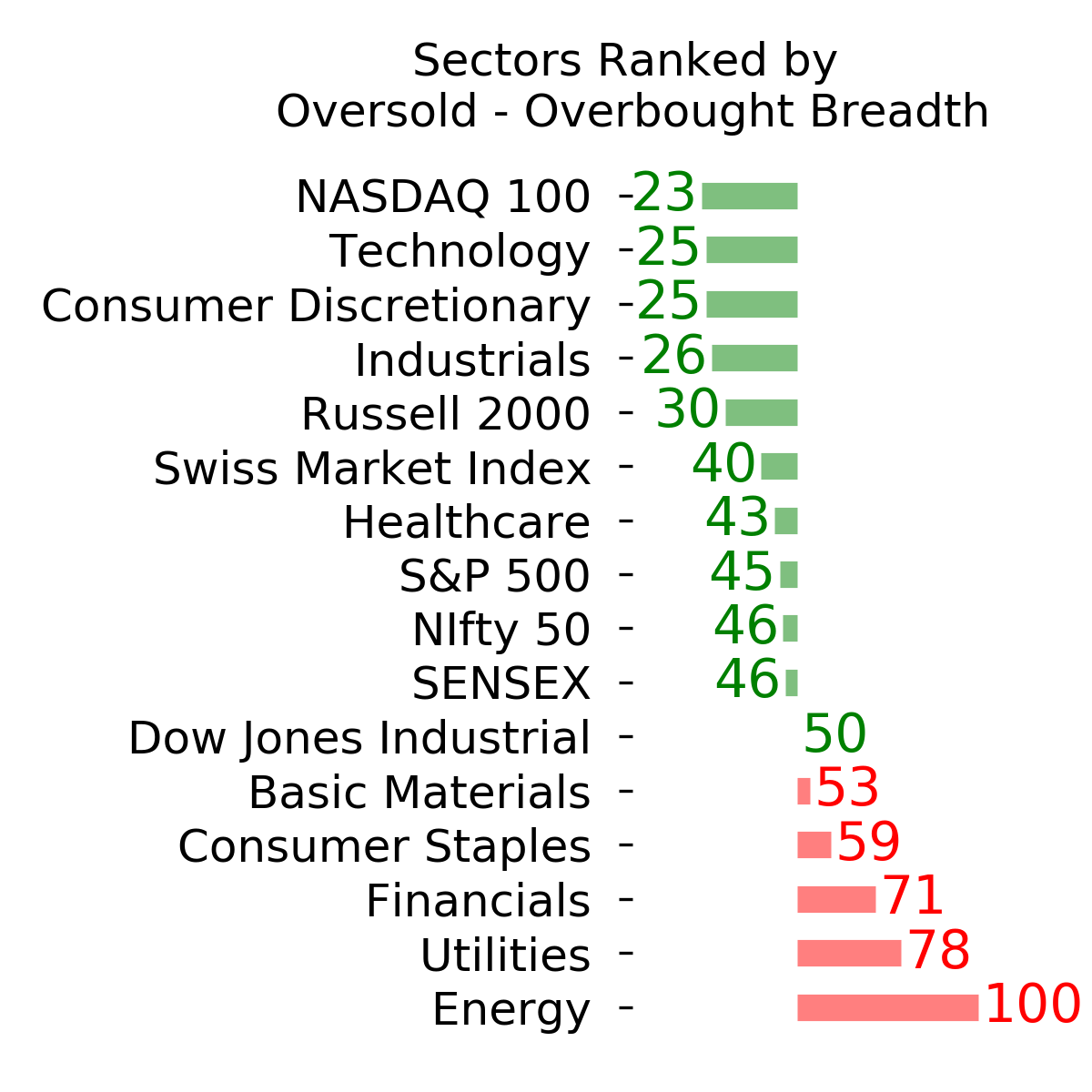

Sector ETF's - 10-Day Moving Average

|

|

|

Country ETF's - 10-Day Moving Average

|

|

|

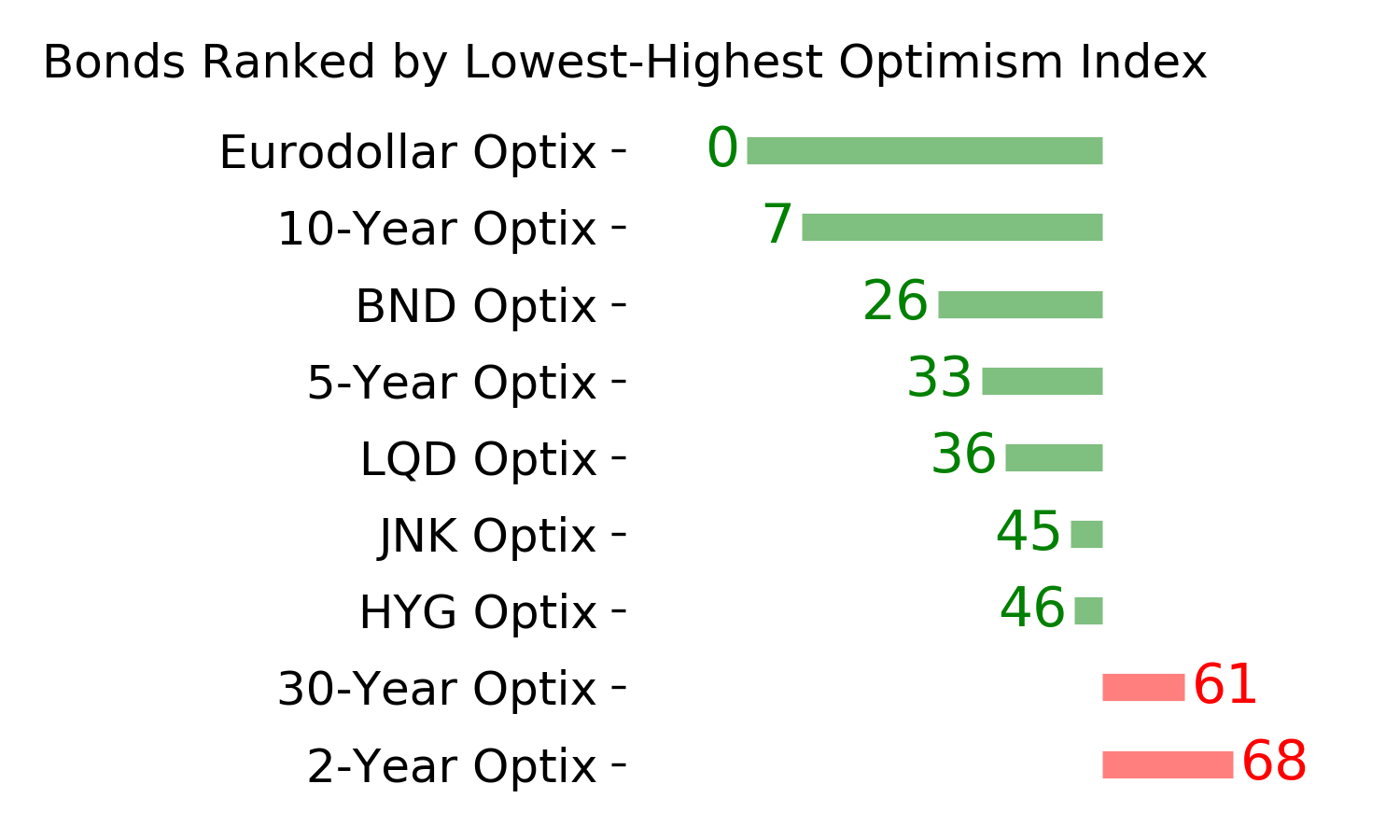

Bond ETF's - 10-Day Moving Average

|

|

|

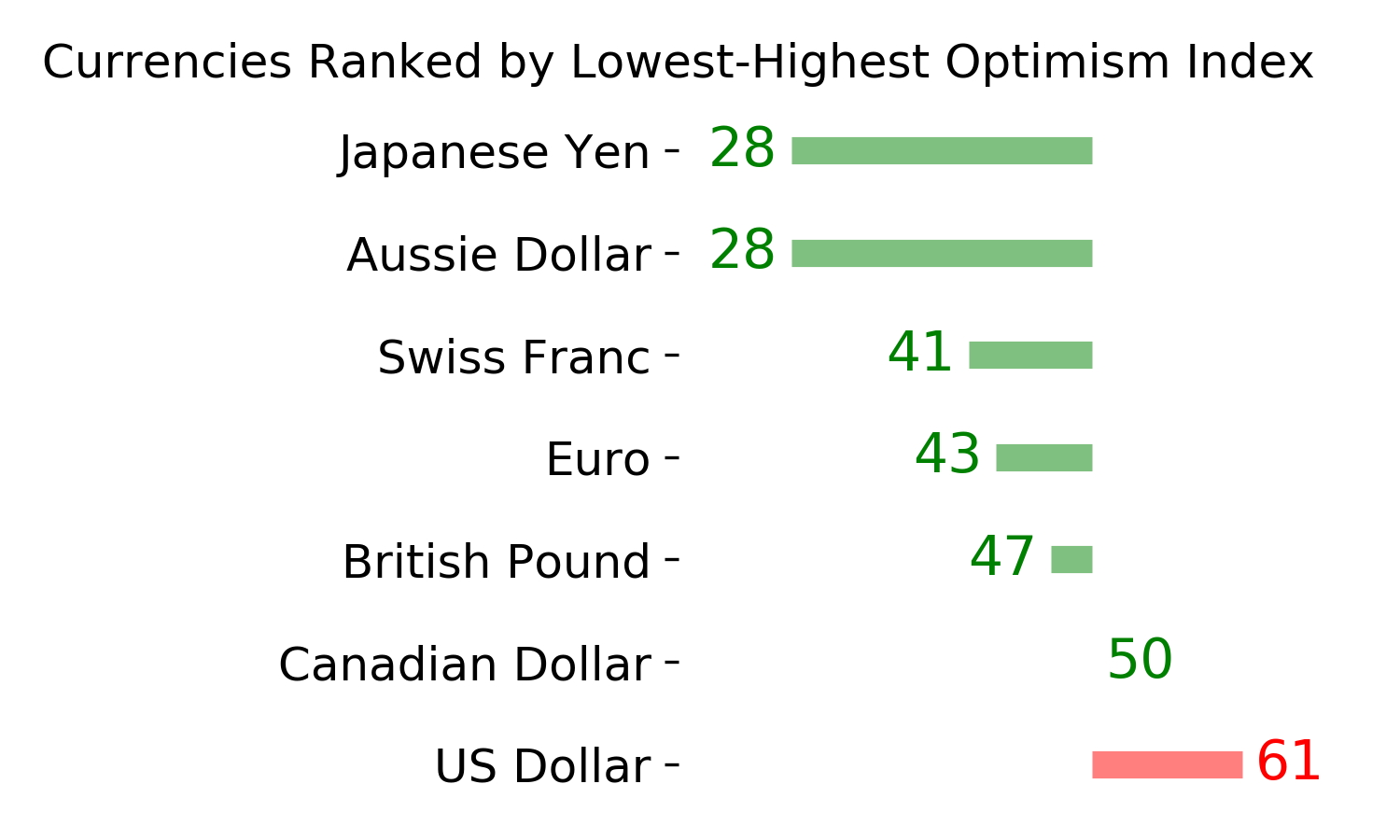

Currency ETF's - 5-Day Moving Average

|

|

|

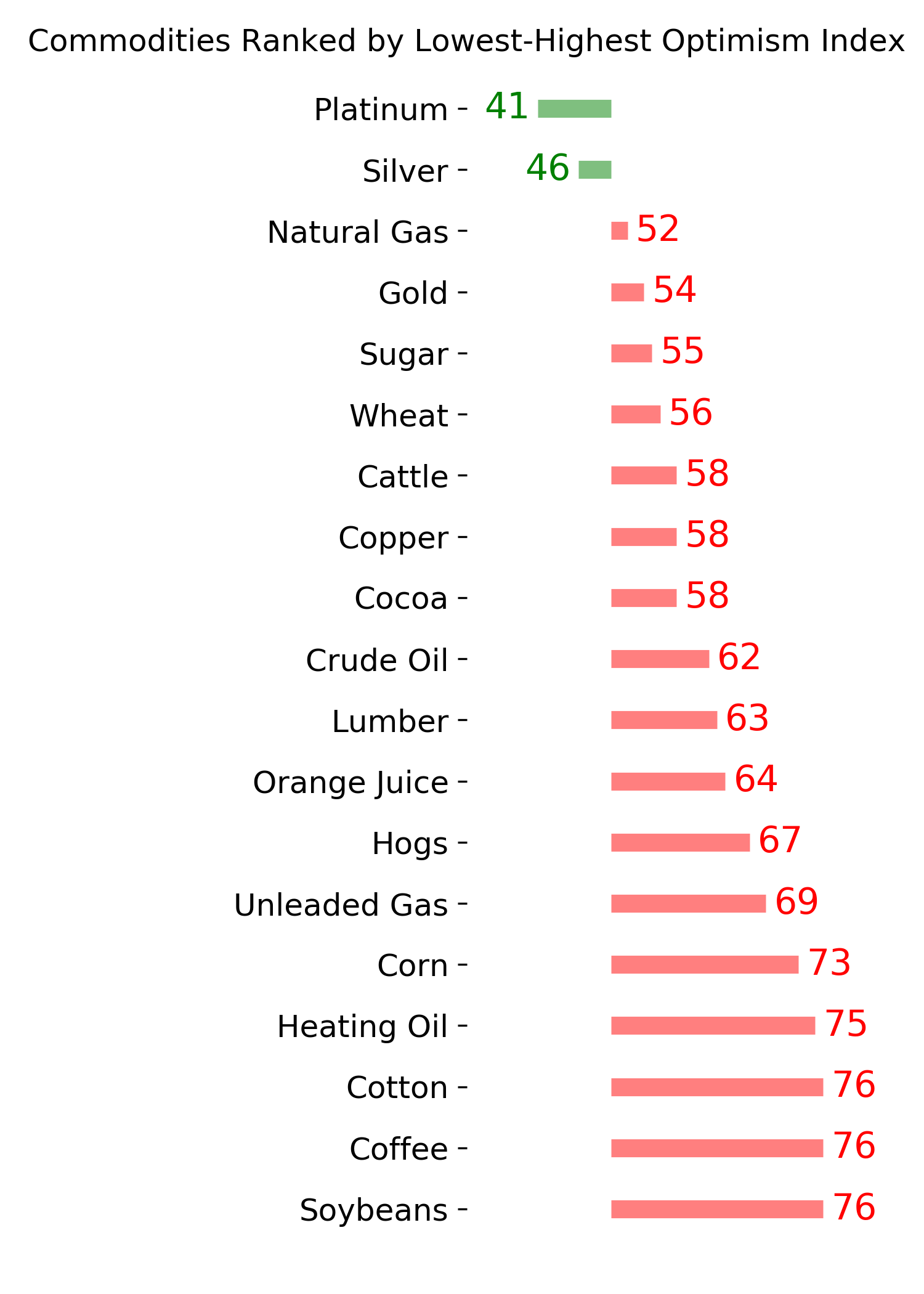

Commodity ETF's - 5-Day Moving Average

|

|