Credit Filtering for QQQ Signals, But Risks Remain

Key Points:

- QQQ has triggered a long-term positive technical signal, with favorable average 1-year returns historically.

- Its short-term pullbacks show significant divergence; credit markets (CDX Ratio) are needed to filter risks.

- Current credit risks are contained, reducing extreme pullbacks, but short-term volatility and pullback risks persist.

A Historic Long-Term Positive Signal

After months of strong momentum, the Nasdaq 100 Index-dominated by large-cap tech stocks-has been experiencing volatility at elevated levels. Increased market corrections have raised investor concerns.

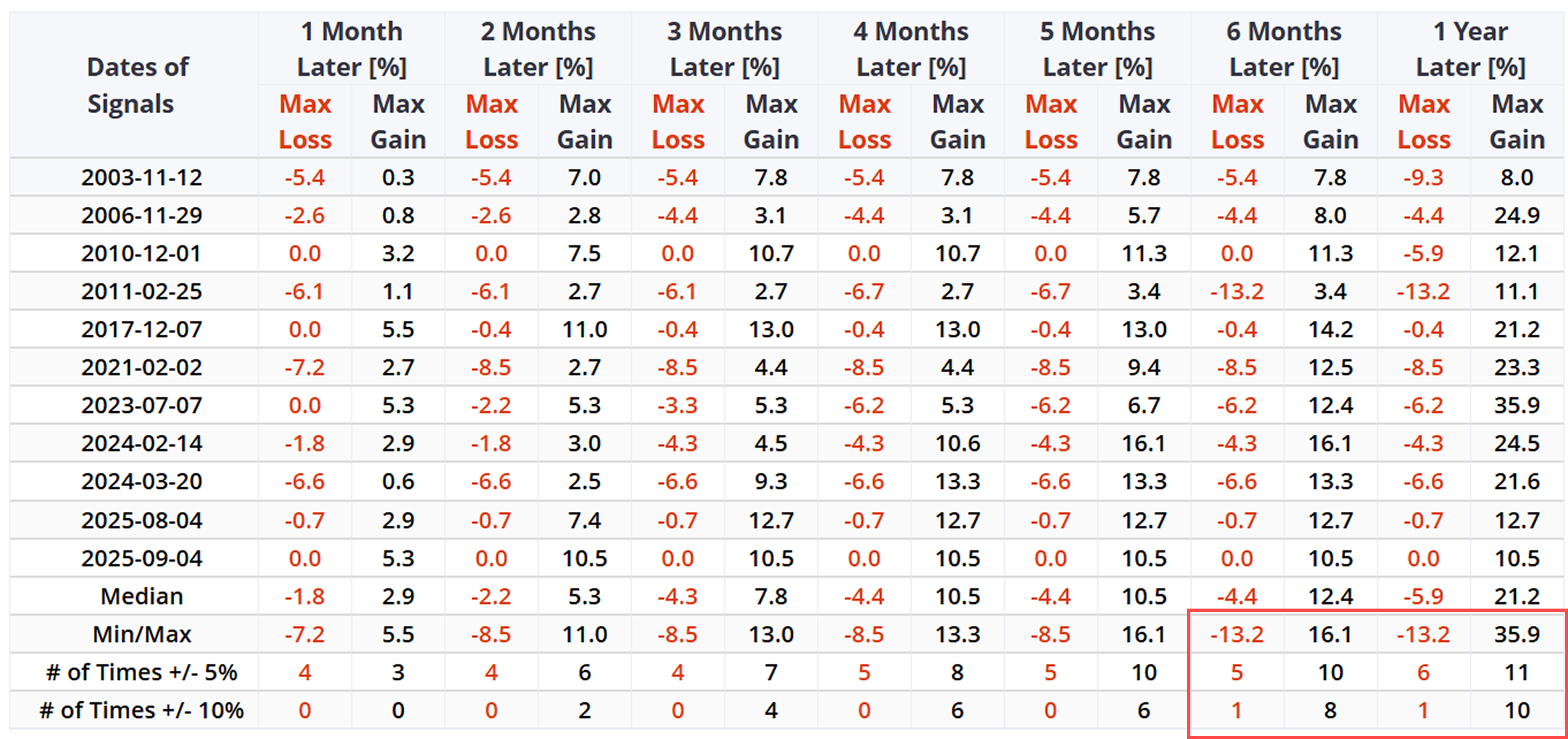

A specific technical signal based on the Nasdaq 100 Index has been triggered. The model requires the market to first be in a confirmed uptrend-trading above its 50-day moving average for 60 consecutive days-followed by a capture of an internal breadth "reset" where both 1-month and 3-month breadth (Which are QQQ 4/12 Week High/Low Spread%) recover simultaneously.Related Backtes Click Here.

Historically, the long-term performance of this signal is notable. As backtest data shows, among the 13 prior triggers, the signal delivered solid average returns one year later.

However, the short-term path of the signal is fraught with uncertainty. Its risk profile exhibits large disparities: the signal can trigger a mere minor pullback (as in 2017) or a sharp drawdown (as in 2020).

This divergence in short-term outcomes is undesirable. It indicates that relying solely on QQQ's breadth signal is insufficient, and a "macro context" indicator must be introduced to stratify risks.

Using Credit Markets for Filtering

Our hypothesis is that the two extreme pullbacks were essentially "systemic credit risk" events, not merely technical corrections.

We use the ratio of the CDX to its 50-day moving average as a filter. This ratio is a sensitive measure of market panic over corporate default risks.

Historically, the largest pullbacks all occurred when the CDX Ratio was above its moving average.

When we examine signals triggered against a backdrop of contained credit risks, the risk profile changes.Related Backtes Click Here.

In this "filtered" signal group, extreme scenarios are eliminated.

This does not mean risks disappear. The short-term (1-month) win rate of this group remains low. But the "worst-case scenario" pullbacks have narrowed-though significant drawdowns may still occur.

What the Research Tells Us...

Based on the recently triggered QQQ technical signal, we find that the signal's long-term (1-year) historical returns are positive.

However, we must focus on its short-term risks. The signal's historical short-term pullbacks show extreme divergence-ranging from nearly negligible corrections to "systemic" extreme sell-offs.

Our core hypothesis is that "credit risk" (CDX) is the key differentiator between these two outcomes. Data confirms this: historically, the worst sell-offs indeed occurred during periods of "exploding" credit risks.

Today's signal is triggered against a backdrop of relatively "contained" credit risks. But this does not mean there are no short-term risks-short-term volatility persists, and significant pullbacks remain possible.