Consumers are all-in on stocks AND bonds

Key points:

- A monthly consumer survey shows that people are optimistic about both stock and bond prices

- It's unusual to see optimism high on both asset classes at the same time

- This particular survey has not been a consistent contrary indicator, including times when overall sentiment is so optimistic

Everyone's bullish on everything

The Most Important Election of All Time happened yesterday, but this isn't about that. It wasn't really, and after the immediate and extreme reactions, nobody knows what the shakeout will be for a while. I'm going to ignore it for a bit.

Instead, it might be helpful to consider the idea that everyone is bullish. Stocks, bonds, it doesn't matter - everyone's in the pool.

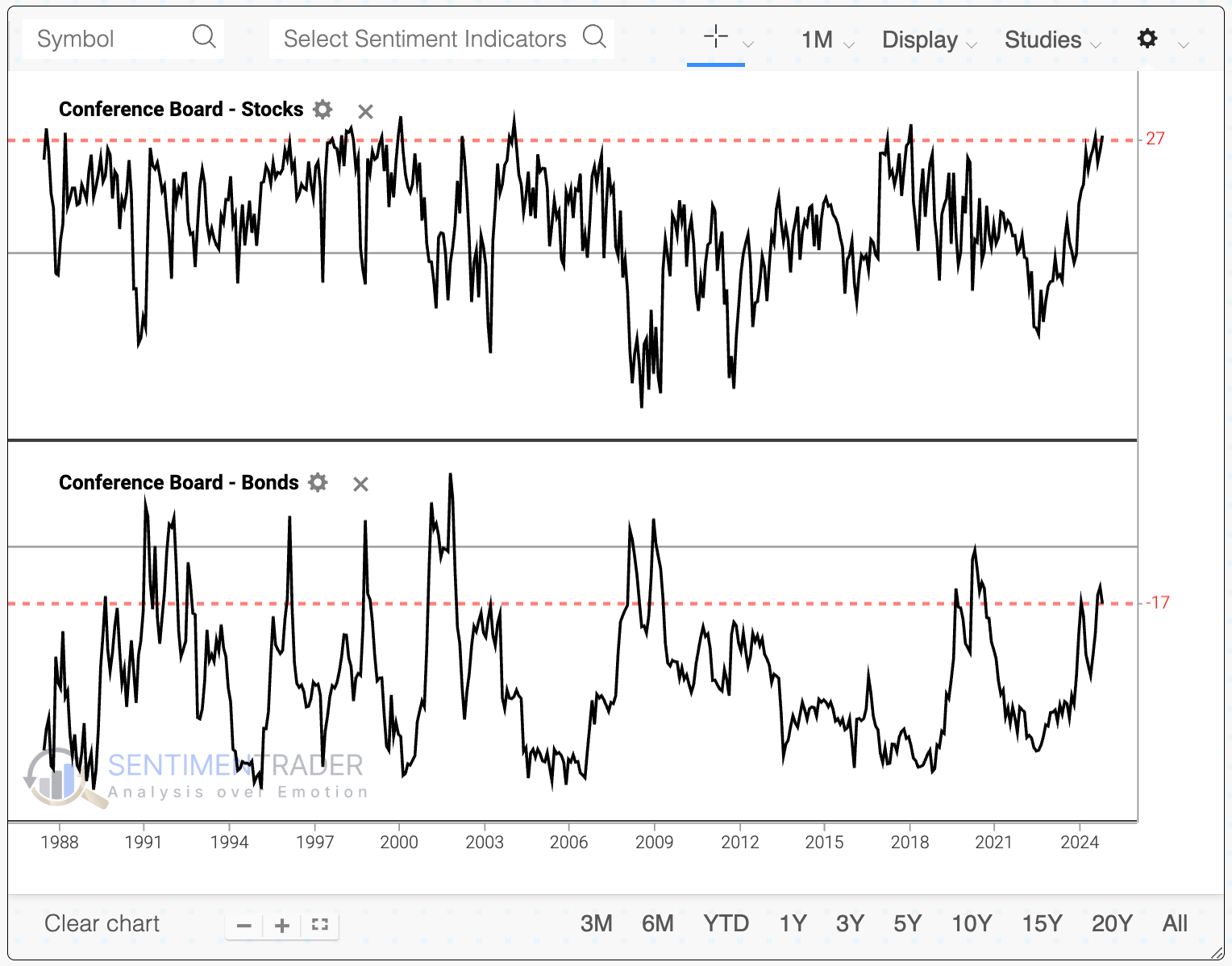

According to the Conference Board, there have rarely been times when so many consumers/investors were so optimistic about the future of stock and bond prices simultaneously.

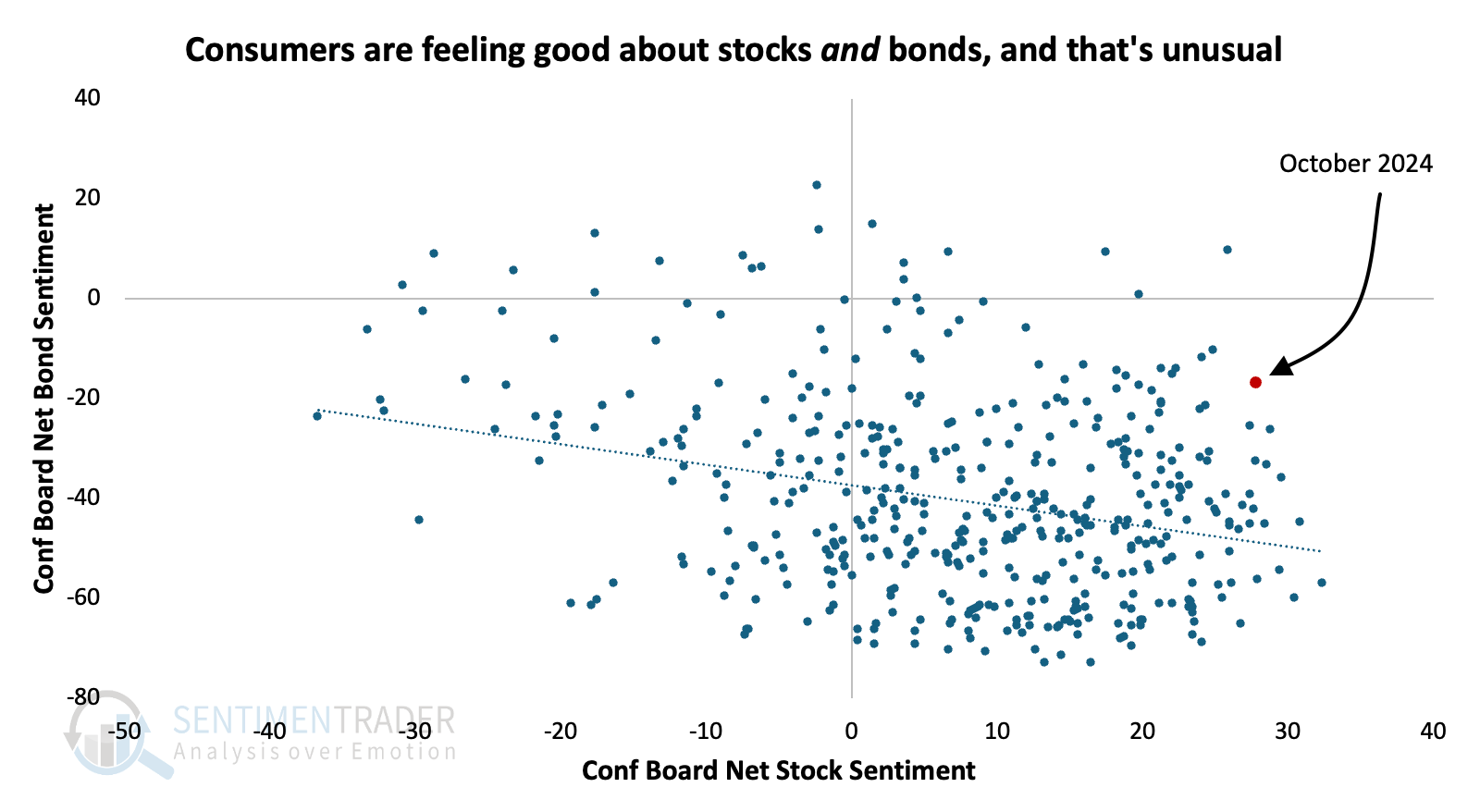

There is a distinct inverse correlation between optimism in the two asset classes. The scatter plot below shows how much of an outlier the current reading is relative to the 448 other months since the surveys' inception.

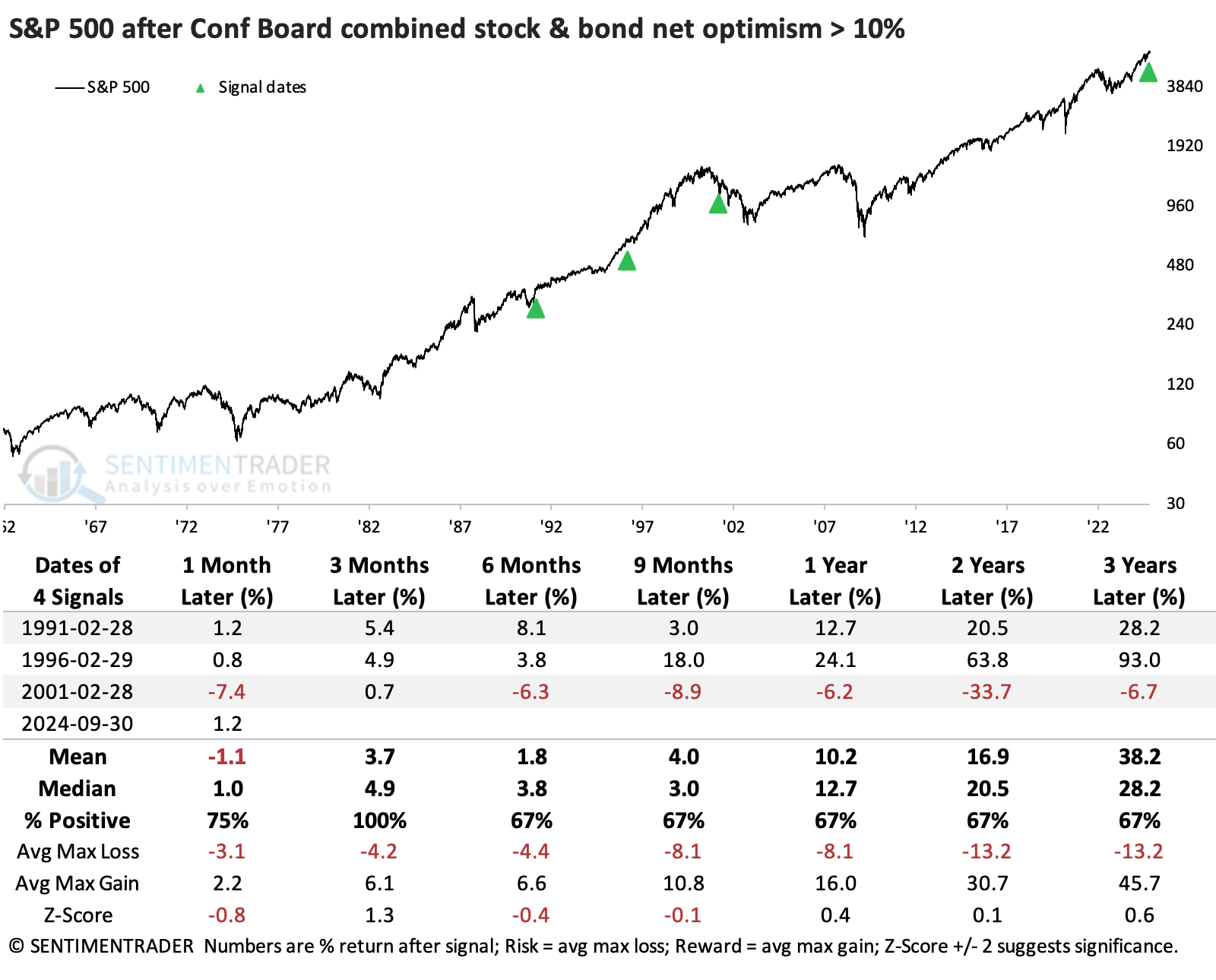

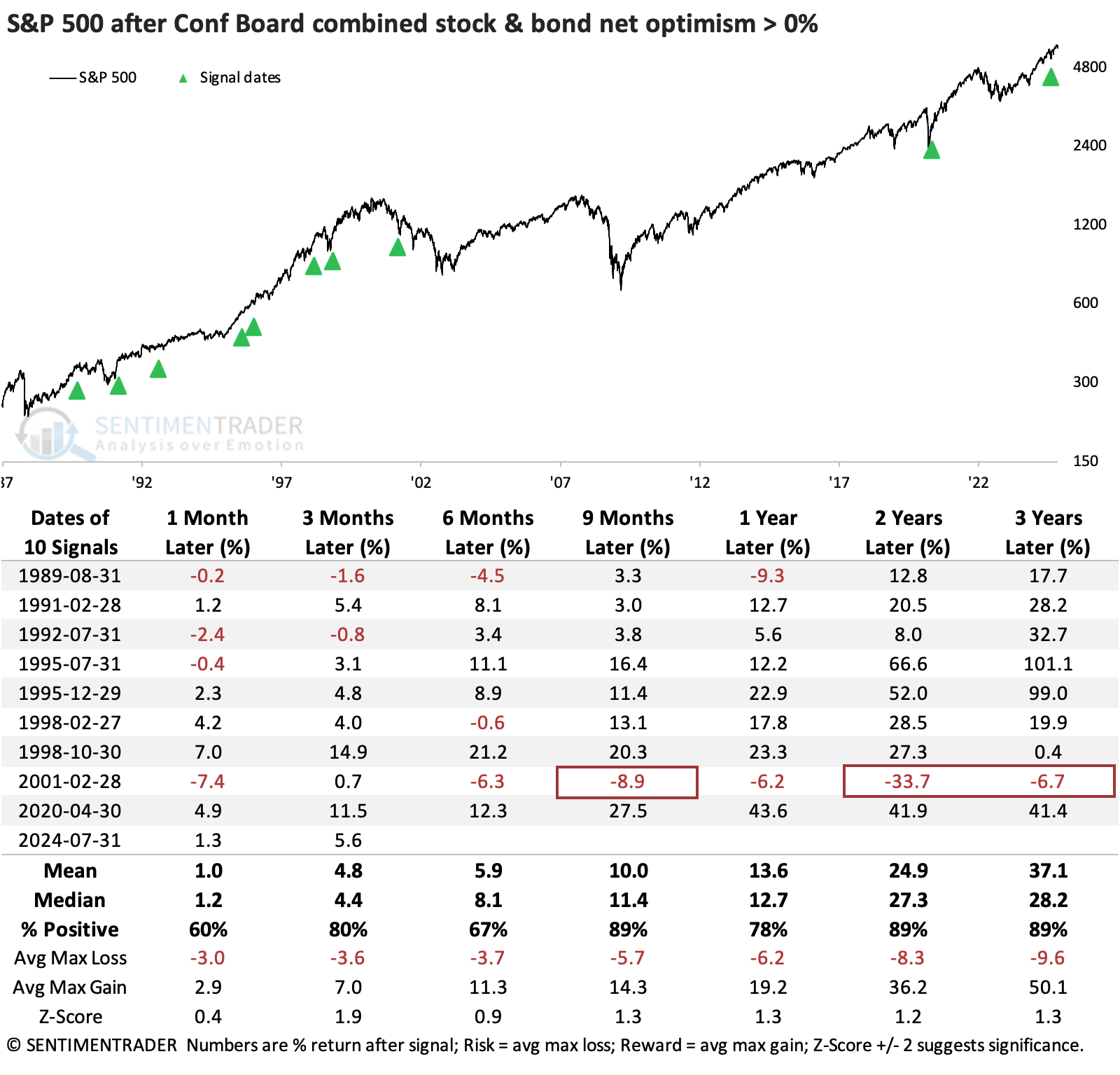

The combined net percentage of consumers expecting rising stock prices and rising bond prices (declining yields) is the highest since 2001. Only a few times has the combined net optimism for stocks and bonds reached the current level. The 2001 instance was immediately and persistently bad for the S&P 500, but the other two instances preceded impressive, sustained advances.

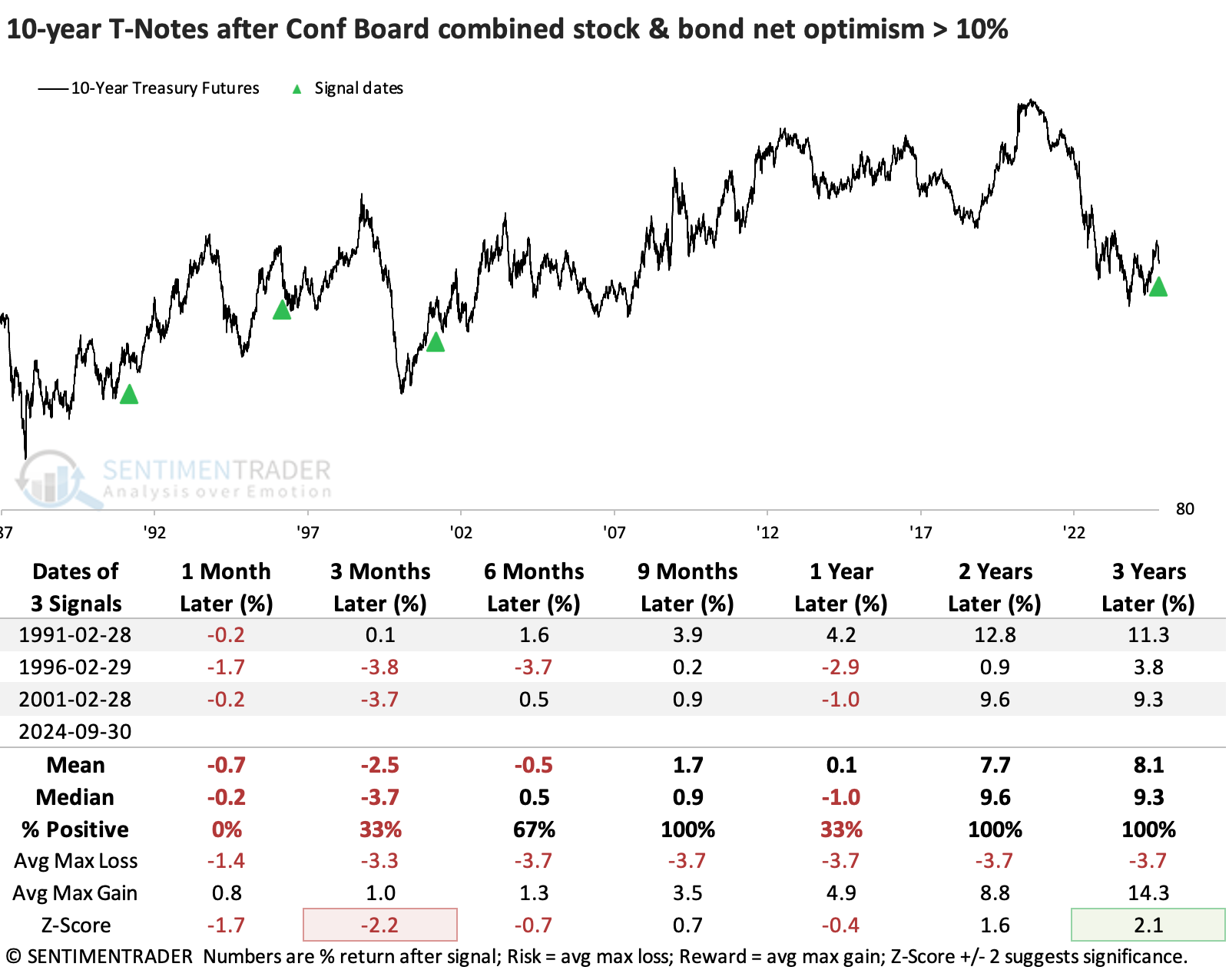

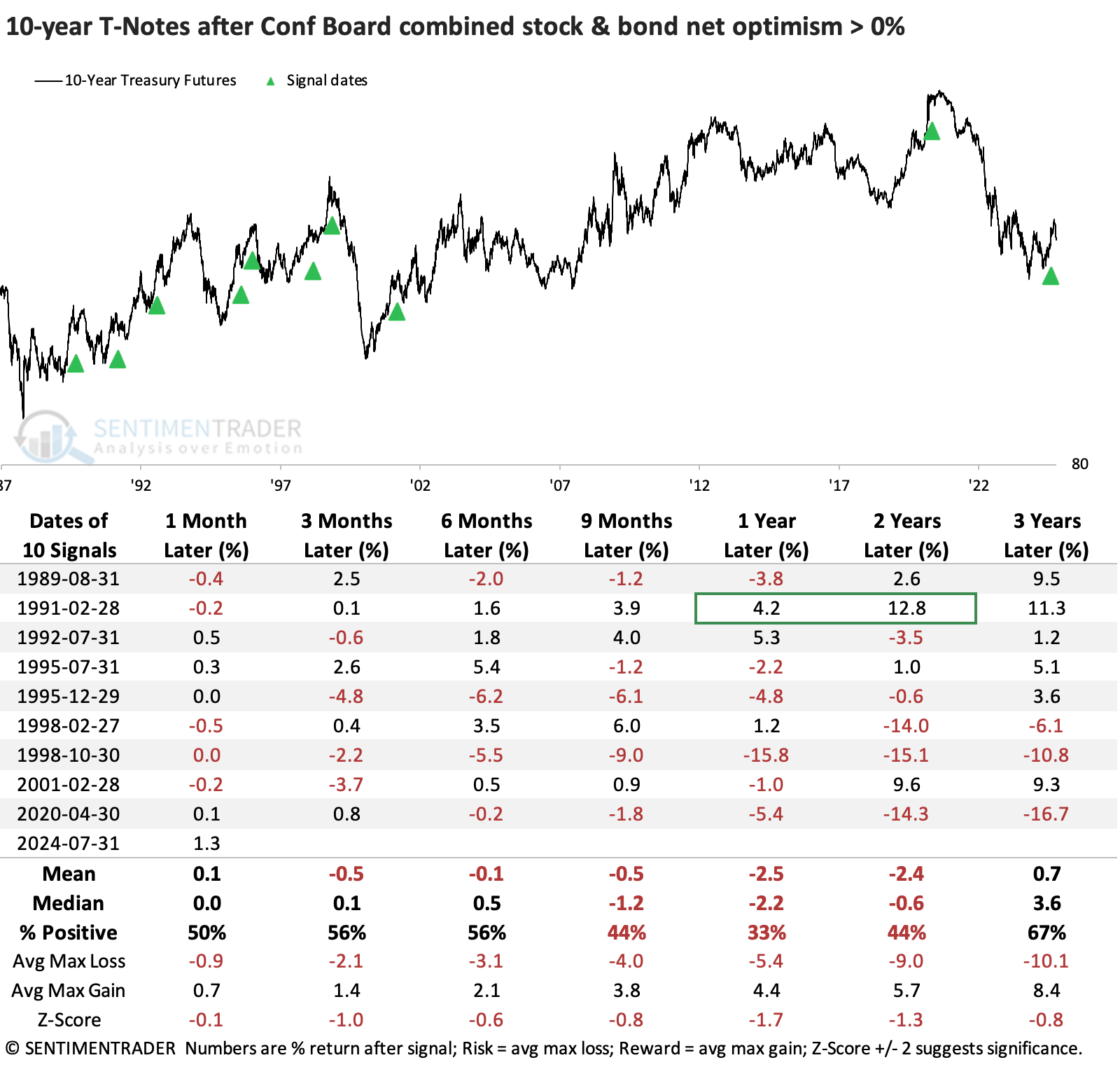

All three preceded a shorter-term dip in bond prices, but those were all reversed in the months ahead.

Broadening the sample

The minuscule sample size means we have to relax the parameters to generate more signals and perhaps gain some confidence in any conclusion. Even when we do that and look at lesser extremes, it is still a pretty good sign for stocks.

The 2001 signal is still there and still horrifically bad, but that was the only one. All of the others showed a gain in the S&P over the following nine months, as well as on long time frames. The S&P's returns were well above random across all time frames.

That was not the case for bonds, as 10-year Treasury note futures declined after nine of the ten signals either one or two years later. The optimistic conditions generally preceded good economic conditions, resulting in higher interest rates.

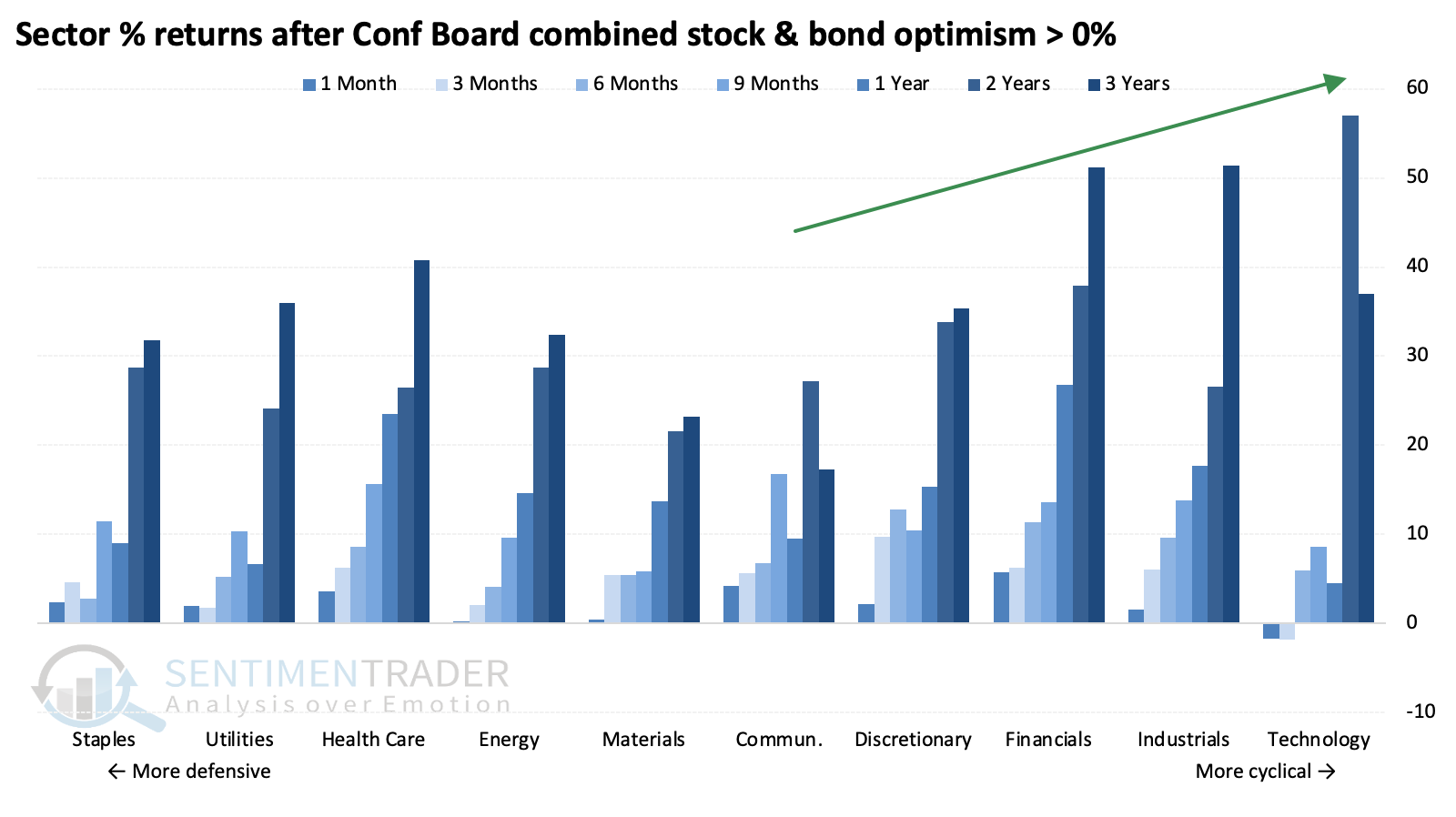

The broadly optimistic conditions favored more cyclical stocks among sectors. Even with the post-2000 bubble plunge, technology stocks exhibited the best two-year returns. Discretionary, financial, and industrial stocks were more consistently strong across time frames.

What the research tells us...

There is a strong tendency towards knee-jerk contrarianism, but that's generally a bad approach to markets. Most areas of the market tend to trend much of the time, and most indicators are simply not very good at being consistently contrary. Especially the ones that get a bunch of attention.

There are times and indicators that tend to be effective at highlighting times when investors may have gotten out over their skis, providing a potential warning about higher risk ahead. The Conference Board poll of consumers has not been one of those indicators. We'll see how the election reaction shakes out in the days ahead, but it looks like this will be another initial failure of "too much optimism" being bad for stocks.