Companies that haul stuff are diverging widely

Key points:

- The S&P 500 has been recording record highs while the Dow Transports is stuck in correction territory

- This is the starkest divergence in 8 years and one of only a dozen in 120 years

- While theoretically troubling, these divergences were not consistent worries

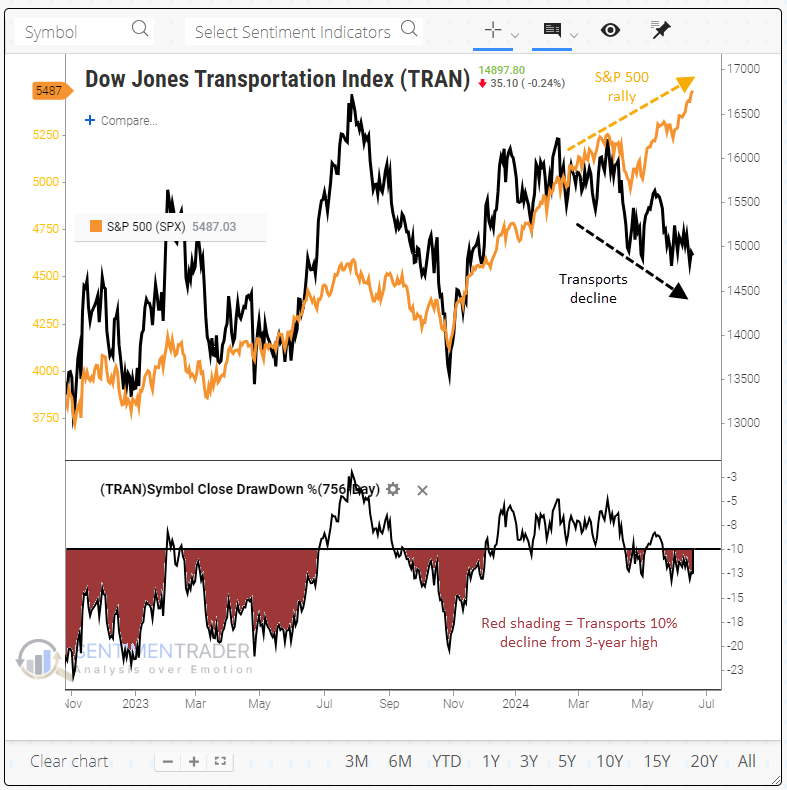

Stocks of companies that move stuff are falling

Over the last year and a half, we've examined many reasons why the 2022 bear market should resume. These ranged from "not quite there" breadth thrusts to excessive investor sentiment to a bevy of fundamental warnings. However, when looking at their historical records, few were compelling reasons to doubt the recovery.

That has started to change some in the past month or so. We're seeing a historic level of deterioration in the number of stocks holding in uptrends, and a disturbingly large number are falling to multi-month or even yearly lows. A split market like this is not healthy - it can resolve to the upside; it usually does not.

Adding to the potential concerns, and in line with the delineation between winners and losers, the Dow Jones Transportation Average has not only not kept up with the S&P 500, it has been mired in correction territory. This is worrying to any long-term followers of Dow Theory.

"According to Dow Theory, strong economies bring increased shipping of goods, benefiting transportation companies and their stocks," said Yardeni. "But that hasn't been the case this year."

The divergence is easy to spot. As the S&P 500 has soared to ever greater heights, the Transports have gone in the opposite direction.

Not a consistent concern

While there are numerous reasons to be cautious about stocks over the coming month(s), we haven't seen much that has been a long-term concern. We can add the lagging Transports to that list.

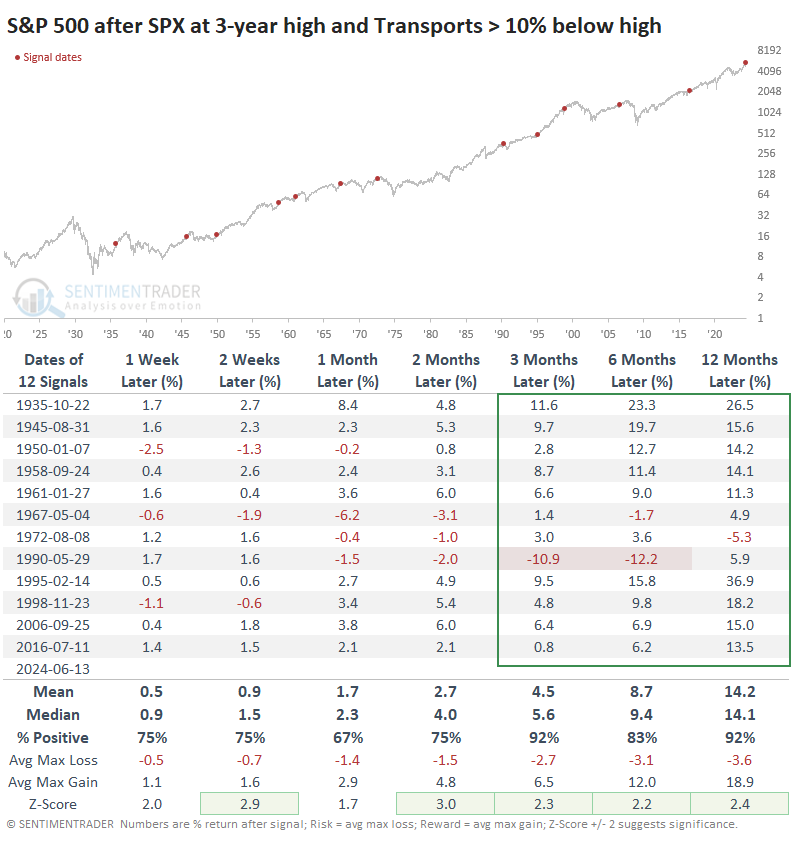

The table below shows returns in the S&P 500 any time it reached a 3-year high, while the Transports were at least 10% below their own 3-year high. From 3-12 months later, the S&P's returns were significantly above average. There was only one loss of note heading into the 1990 recession.

Up to a year later, that was the only signal that saw the S&P pull back more than -10%. While arguably eight of the signals preceded some trouble at some point, that "at some point" sometimes took a couple of years to appear.

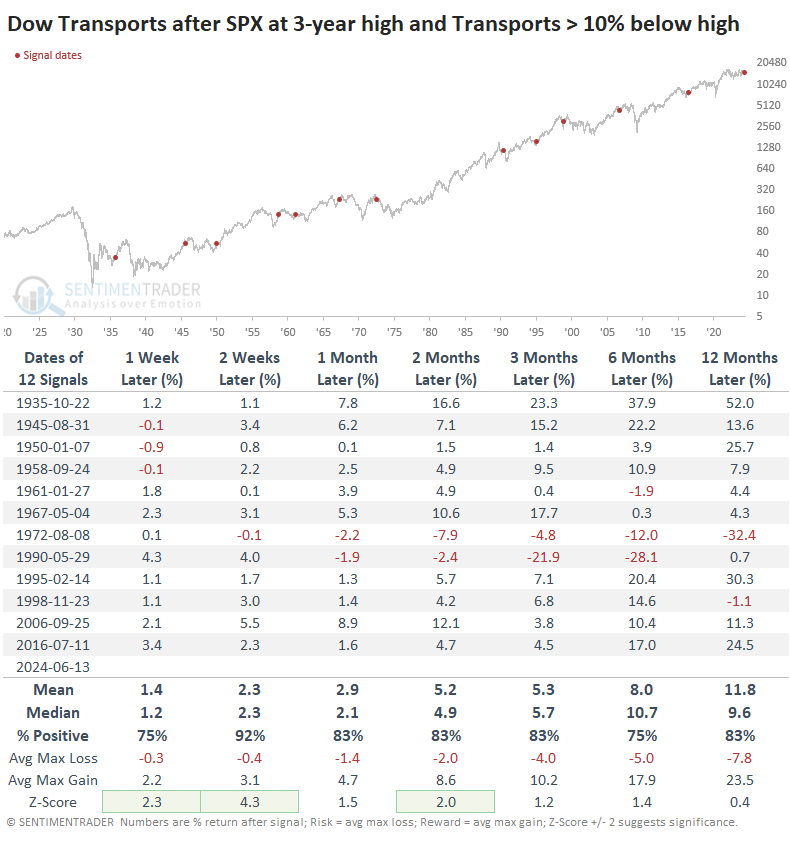

For the Transports, it was more positive as a shorter-term mean reversion signal, as the index popped higher over the next couple of weeks every time except once. It tended to keep the gains coming, but its returns weren't exceptional.

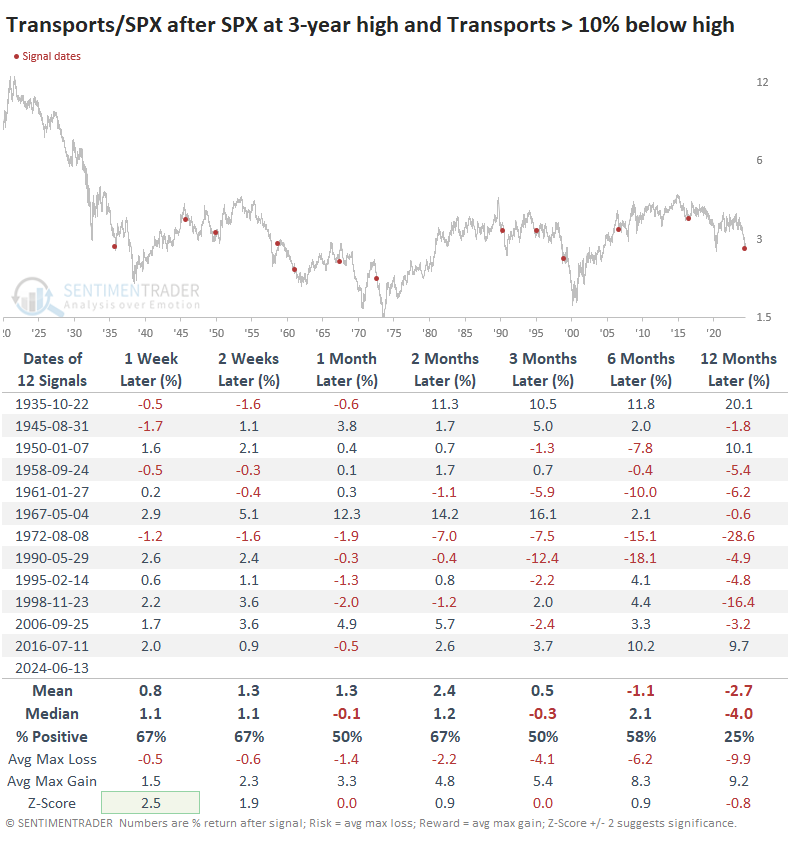

Relative to the S&P 500, Transports showed some grit over the next couple of months, regaining some ground most of the time. Only three signals were outright failures, with virtually no bounce in the ratio.

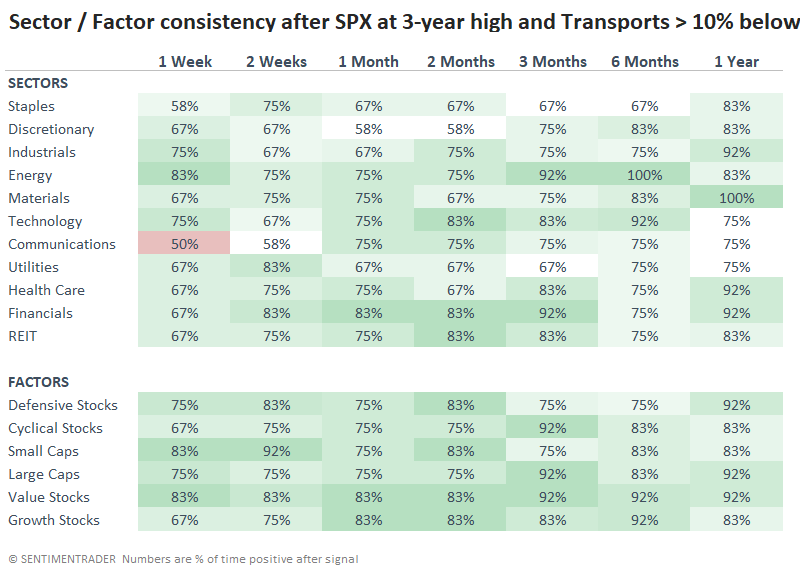

Looking across sectors and factors, we might assume this would be a good signal for defensive stocks, but it was not. Cyclicals showed more consistent gains over the next few months. Over the medium- to long-term, some of the most consistent gains came in the energy, industrial, and material sectors, which is a bit of a surprise.

What the research tells us...

There is a clear and objective lack of participation among a wide variety of stocks as the major indices have pushed to their most recent round of new highs. That is a legitimate concern.

Of less concern are some particular divergences, especially those based on theories developed decades ago in a completely different economy. While a healthy Transportation sector seems like a given for an overall healthy market, it has not proven to be so. We looked at this a little over a year ago, with pretty much the same conclusion. The struggle in these stocks seems more of a discussion for textbooks rather than for practicing investors.