Commodities doldrums may last a bit longer

Key points:

- The commodity sector is a very diverse group, each contract having its own supply and demand fundamentals

- There are still times of the year when commodities as an asset class tend to move decisively in one direction

- The weakest time of the year by far is now upon us

Seasonal headwinds for the commodity sector

Commodities were red-hot from mid-2020 into June 2022 but have since cooled off. Near the end of September, Dean noted the rapid deterioration in commodity trends. Seasonality now suggests the possibility of a continuation of the recent cooling off in the commodity sector.

Each commodity has its supply and demand factors that drive price. Still, it is not uncommon for the entire commodity sector to move persistently in one direction or the other, and it has now entered the weakest time of year.

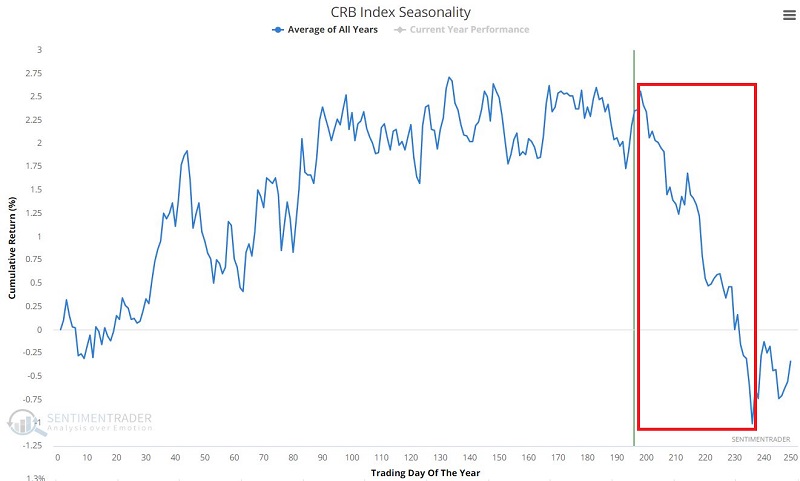

The chart below displays the annual seasonal trend for the CRB Index - an index comprised of 19 commodities.

The period between Trading Day of Year (TDY) #198 and TDY #236 is clearly the most unfavorable time of year. For 2022 this period extends from the close of October 14 through the close of December 8.

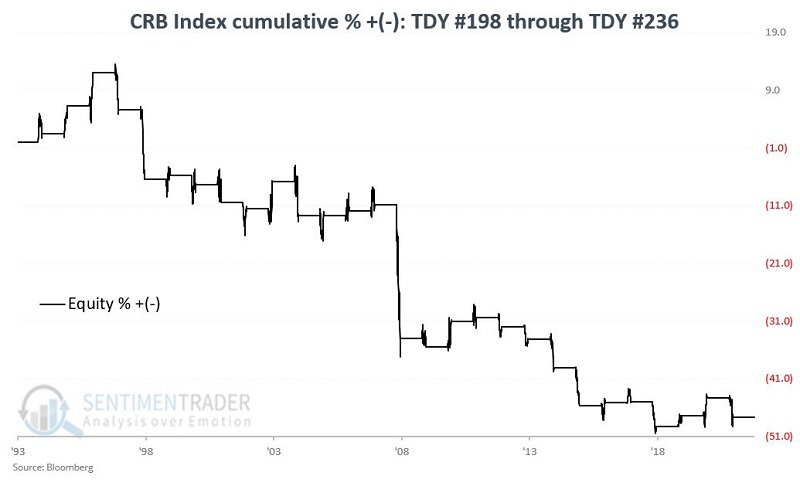

The chart below shows the cumulative percentage performance of the CRB Index during this unfavorable period since 1994.

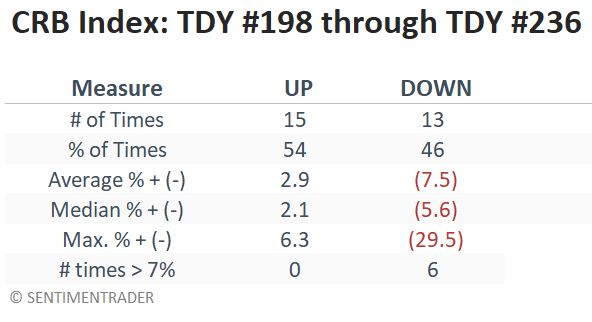

Over these 28 years, the CRB Index was positive 15 times and negative 13 times, but the up years tended to show modest gains, while the down years often suffered significant losses. It endured a loss of over -7% on six occasions; there were no gains greater than +6.3%.

The bottom line seems to be that a trader must have a compelling reason to hold long commodities during this period, given the unfavorable reward-to-risk ratio.

Results are similar using a commodity ETF

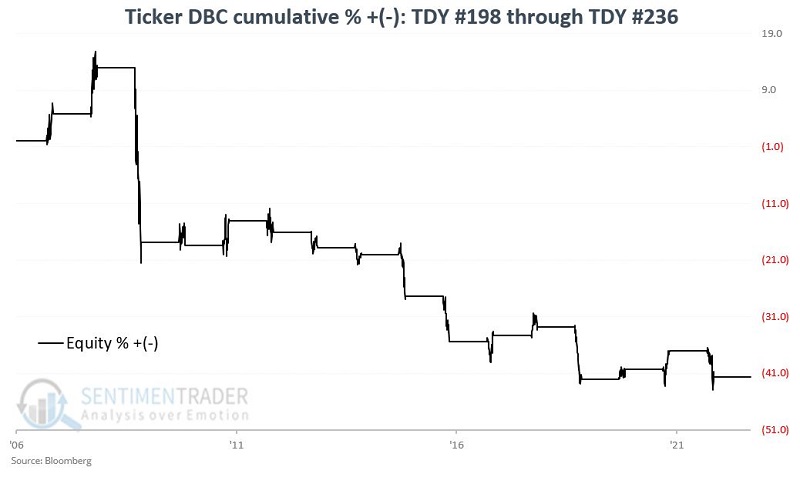

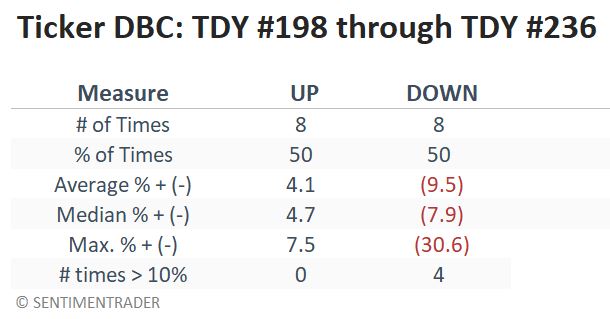

The CRB Index is not a tradable security. So, to look at real-world results, let's replace the CRB Index with the Invesco DB Commodity Tacking Fund (ticker DBC).

The chart below displays the cumulative percentage performance of DBC during this unfavorable seasonal period since it started trading in 2006.

The table shows that DBC had a 50% win rate, but again, the losses during the down years tended to swamp the gains during the up years.

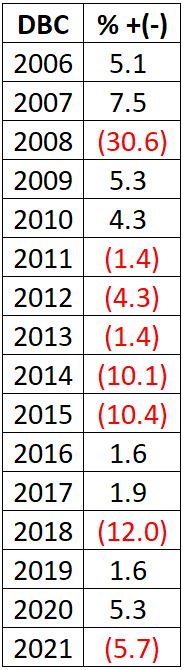

The table below displays the year-by-year returns for DBC during these seasonal stretches.

What the research tells us…

Do the results above suggest we rush out and sell short every commodity we can get our hands on? Not necessarily, because history shows that the likelihood of a drop is roughly equal to a coin flip. On the one hand, if commodities trend lower in the weeks ahead, the decline could be substantial. The real message in the data is that there may be better places to allocate capital than commodities between now and early December.