Cheap homebuilder speculation

Key Points

- Dean has written several compelling notes lately regarding crude oil and homebuilders

- This piece focuses on homebuilders

- Below, we present an example of one inexpensive way to play a potential breakdown in homebuilders

Betting on homebuilder weakness

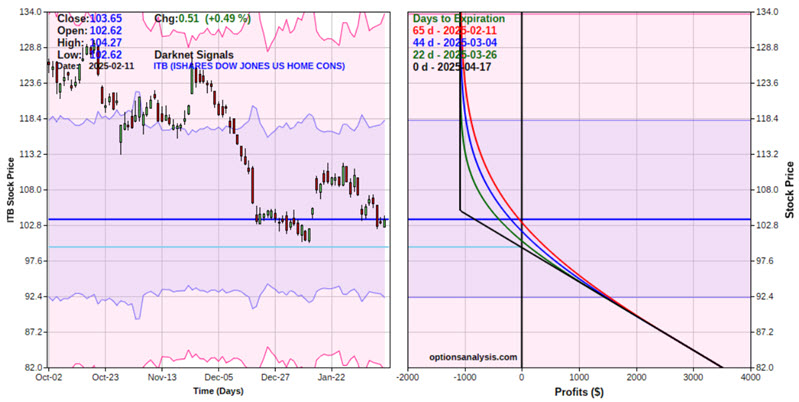

In this piece dated 2025-02-10, Dean's research suggested the potential for continued weakness in the homebuilder sector. We will use the iShares US Home Construction ETF (ticker ITB) as a proxy for the sector. As you can see in the chart below, the sector has been relatively weak, recently breaking below its 200-day moving average/

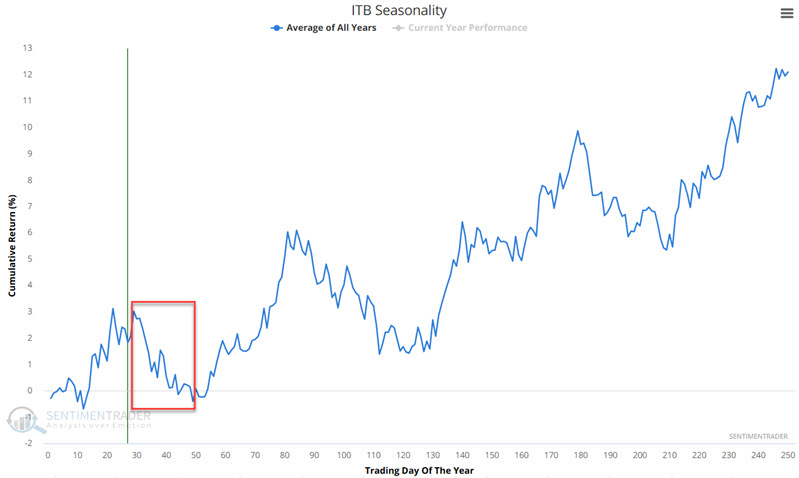

As you can see from the annual seasonal chart for ticker ITB futures below, this sector does tend to show weakness during the period just ahead.

As always, seasonality is merely an average of past events and is NOT a roadmap to what will happen in any given year. With that caveat in mind, I looked for a potential example trade using options on ticker ITB to take advantage if the sector weakens further, while - significantly - limiting our risk to a reasonable and predetermined amount if homebuilders rally instead.

Betting against homebuilders - cheaply

For the record, what follows is an "example" and not a specific "recommendation" (at Sentimentrader, we are analysts and not advisors). With that in mind, consider a trader who thinks that homebuilders will continue to decline in the weeks and months directly ahead but is not willing to assume the risk of selling short shares of ticker ITB (which involves margin and theoretically unlimited risk).

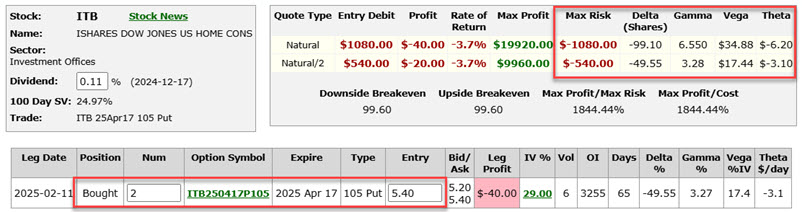

A simple alternative would be to buy the ITB April 17 2025 105 strike price put option at $5.40, requiring a capital commitment of $540.

The particulars for this position appear below (courtesy of Optionsanalysis.com).

The risk curves-i.e., the expected dollar gain or loss based on the price of ITB shares as of four different dates (the red line is today) leading up to options expiration (the black line)-appear in the chart below.

Things to note:

- The cost to enter this position trading a 1-lot is $540

- The worst-case scenario is that the position is held until expiration (April 17) and that ITB shares are trading at $105 or above, in which case the entire $540 will be lost

- The Delta for this position is -49.55 (which means that this position is presently roughly equivalent to shorting 49 shares of ITB - though note that Delta will change as time goes by and ITB price fluctuates)

- The Gamma for this position is 3.27 (which means that for each $1 ITB shares gain or lose, this position will gain or lose 3.27 Delta points)

- The Vega for this position is $17.40 (which means that if option implied volatility rises one percentage point, this position will gain roughly $17.40, and vice versa; In other words, an increase in volatility will result in more time premium being built into the price of the option)

- The Theta for this position is -$3.10 (which means that this position will lose $3.10 in time premium due solely to the passage of one day's time)

- The breakeven for this price is $99.60 (strike price of $105 minus premium paid of $5.40)

- Below $99.60, the option price will gain one point for each point the stock price declines

- Note also that the trading volume for this option on 2/11 was only six contracts - limit orders are highly recommended for options with low trading volume

Thoughts on position sizing and position management

Let's say a trader with a $50K account is willing to commit a maximum of 3% to an option trade. 50K x 0.03 = $1,500. So, this trader could buy two puts for $1,080 ($540 premium x 2 options).

Deciding how to manage the position is up to each individual trader. The first question to answer is, "If ITB rallies, will I simply hold until expiration in hopes of a sell-off (risking the entire premium), or will I consider cutting a loss early." Note that there is no correct answer; it is only a matter of personal preference.

As an example of a plan for managing the position, if things go right, a trader holding a 2-lot might consider selling half the position if ITB declines one standard deviation (see horizontal line at roughly $92.40 a share in the risk curves chart above) and letting the other ride in hopes of a more significant gain.

Again, the above are "examples" of one approach to managing the position, not specific recommendations.

What the research tells us...

Dean's research suggests that the decline in homebuilders may worsen in the months ahead. While ITB might technically be considered "slightly oversold" at the moment, the breakdown below the 200-day moving average suggests a change in the primary trend. For traders looking to make a play but unwilling to make significant capital commitments, an option position can be a viable alternative. However, remember that 100% of the premium options paid can be lost if the underlying security does not do what you hope.