Catching the falling safe - from a distance

Key Points

- When a stock plummets, implied option volatility often "spikes" (as demand for put options from fearful traders explodes) which causes option premiums to rise sharply

- Selling a far out-of-the-money put can give a trader the opportunity to a) potentially buy the underlying stock at a much lower price and/or b) generate income

- Since Implied volatility spikes often do not last long, a sharp decline in IV can create the potential for early profit-taking

Laying the groundwork

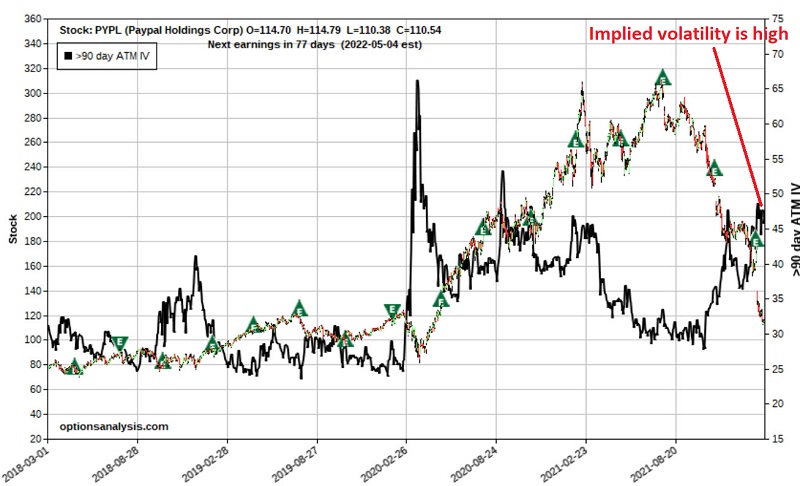

Consider the plight of Paypal Holdings, Inc. (PYPL) in the chart below courtesy of StockCharts). After years of being a market darling, it missed on earnings and has plummeted -64% since July 2021. It presently remains in a freefall.

I keep reading articles arguing that PYPL is now a "bargain" at this new lower price. Maybe, maybe not. In any event, buying shares of PYPL at this exact moment is an exercise in that age-old adage of "trying to catch a falling safe." No thanks. However, another adage states that "opportunity is where you find it." An opportunity may be forming regarding PYPL - just not the "BUY NOW" variety.

In the chart below (all subsequent screenshots are courtesy of Optionsanalysis), we see that the implied volatility on options on PYPL has risen to a very high level - which has only been reached a few times before. Previous such "spikes" in IV typically did not last long (but more on this later).

This elevated IV tells us that PYPL options are presently "expensive," i.e., the prices incorporate a great deal of time premium (as option sellers demand more time premium from option buyers to compensate them for taking the risk of selling options in the first place). This creates potential opportunities.

Selling a far-out-of-the-money put

Our example trade is as follows:

- Sell 1 PYPL Jan19 2024 put @ $5.15

This strategy is referred to as "naked put selling." The particulars and the risk curves for this trade appear in the screenshots below.

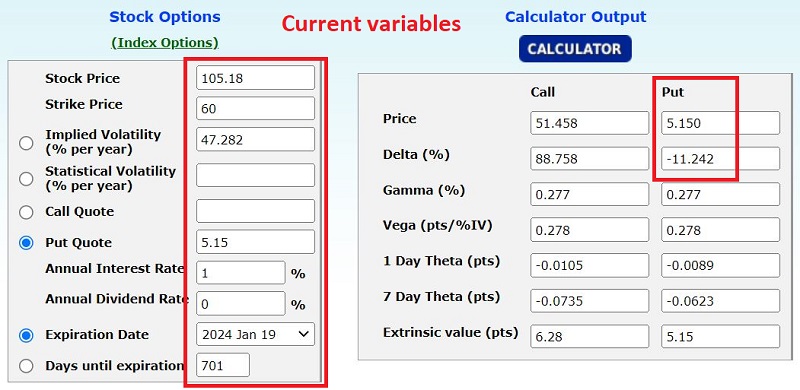

Selling this put option at a strike price of $60 (using a limit order at the midpoint of the bid/ask spread, which is recommended) at $5.15 implies the following - the option seller:

Selling this put option at a strike price of $60 (using a limit order at the midpoint of the bid/ask spread, which is recommended) at $5.15 implies the following - the option seller:

- Receives $515 from an option buyer

- Is obligated to buy 100 shares of PYPL at $60 a share (current stock price is $105.18) if the stock drops below that price and the option buyer exercises the put

- Must put up $5,485 to maintain the position ($60 strike price minus $5.15 option premium received times 100 shares)

The worst-case scenario is simple - if PYPL were to go bankrupt and the shares became worthless, the trader would buy the stock at an effective price of $54.85 and watch it go to zero, resulting in a loss of $5,485. Needleless to say, if you are concerned that PYPL will go out of business, you would likely not take the trade in the first place.

There are three likely scenarios:

- PYPL stock ultimately drops below $60 a share, the option is exercised, and the trader buys 100 shares of PYPL at an effective price of $54.85. What to do with the shares from there is entirely up to the trader.

- PYPL never falls to $60, and the option ultimately expires worthless in January 2024. In that scenario, the trader makes roughly 9.4% ($515/$5,485) over the course of the next 23 months.

- Implied volatility declines in the meantime. This is the opportunity to focus on below.

If IV plummets

The chart below displays the implied volatility history on >90-day PYPL options again. Note the historical tendency for IV to "spike" in fairly short order and for that spike to dissipate relatively quickly (i.e., within a few months).

So, what happens if the same thing happens this time around? The screenshot below shows an options calculator screen for the PYPL Jan2024 60 put at the moment. Note that with Implied Volatility at 47.282% and 701 days left until expiration, the option's market price is $5.15.

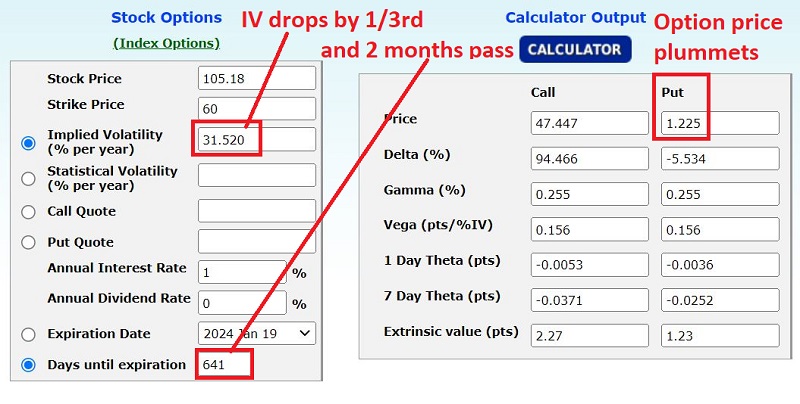

Now let's consider the following scenario:

- Stock price remains unchanged

- IV drops by 1/3rd (which would be in line with previous "post IV spike" actions)

- 60 days go by

The screenshot below shows an options calculator with these updated variables. Note that the expected price of the put option under this scenario plummets from $5.15 to $1.22.

Under this hypothetical scenario, the numbers work out as follows:

- The option seller originally sold a put for $515 and put up $5,485 to cover the risk of having the stock put to them

- After 60 days, the trader buys back the put at $1.22. This results in a profit of $393, or 7.2% in 60 days

- The trader is also released from the obligation to buy PYPL shares, and the $5,485 in collateral is released and can be used on other trades

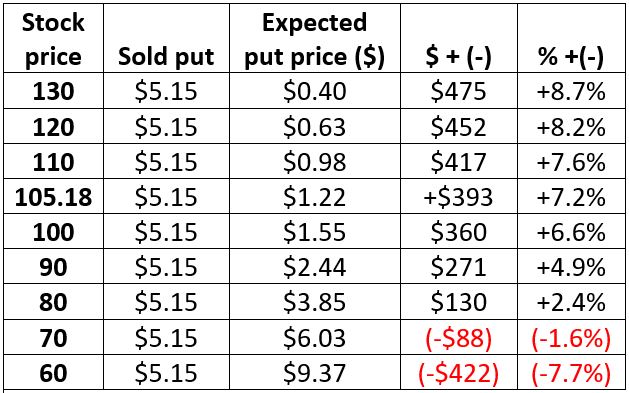

Just to carry this example out fully, note that the price of the stock is an important input. The example above assumes PYPL stock price remains unchanged at$105.18. The table below displays the expected results (assuming implied volatility declines by 1/3rd over the next 60 days) based on the price of PYPL at that time.

Other potential opportunities

The type of trading described above requires a certain investment mindset and is not for everyone. Likewise, one needs to be careful about getting too carried away in trying to make bullish plays on plummeting stocks. That said, two other stocks that may offer similar potential opportunities are Facebook (OK, fine, Meta Platforms, Inc., ticker FB) and DoorDash (ticker DASH). Again, neither of these stocks are "recommended." They simply fit the "plummeting price/high implied volatility" mold.

What the research tells us…

Is any of this a good idea? That's up to each trader to decide based on their own experience and risk profile. It is impossible to predict at what price PYPL will bottom out. However, it is possible to assess your own willingness to buy it at $54.85 a share.

More importantly, it is almost certain that sometime between now and January 2024, implied volatility for PYPL will decline significantly. When that happens, the hypothetical option seller in our example above may have the opportunity to buy back the put at a lower price and book an early profit - assuming PYPL doesn't plummet below $54.85 a share in the meantime.