Bond Market Moves

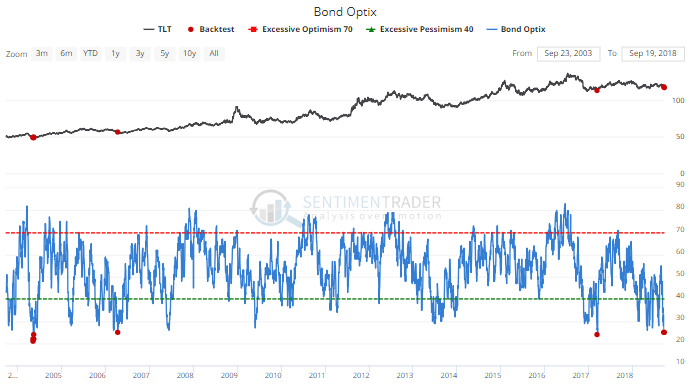

Bonds are getting hit again today, after already suffering a few weeks of declines. The move has been enough to push the Optimism Index for bonds down to one of its lowest levels in 15 years.

Forward returns in the TLT exchange-traded fund have been excellent the few other times sentiment got this stretched to the downside.

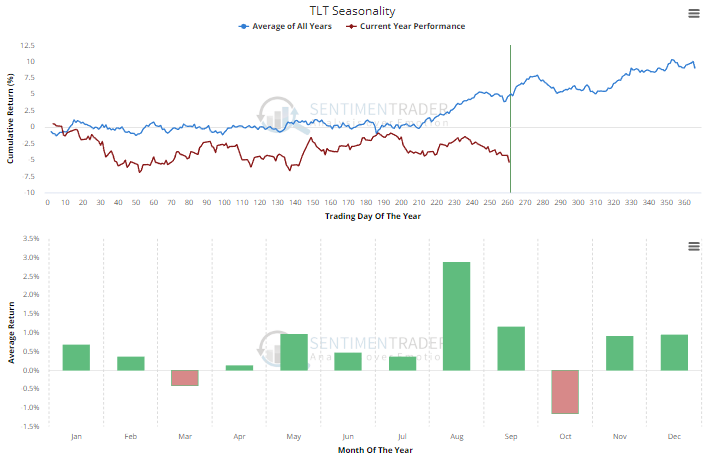

It's occurring at an interesting point in the year. TLT has followed it seasonal tendencies pretty closely this year, and it has tended to rally into early October before a rough stretch in the latter part of October-November.

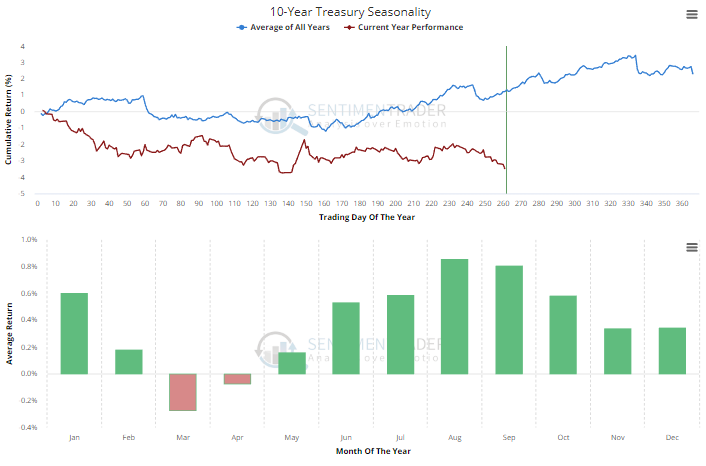

The 10-year Treasury doesn't show quite as pronounced a pattern, though.

What's also notable is the sudden jump in assets in TLT. Over the past few weeks, assets in the fund have jumped nearly 30%.

The automatic assumption is that this is bottom-fishers trying to time a rebound. But it could just as easily be short-sellers, with the fund company creating new shares to meet the demand of those selling the fund hoping to buy it back later at a lower price. Usually with TLT, rising fund assets correlate with rising price, so there's a good chance this is short-sale behavior. The only other time in the past 5 years that TLT lost more than 2% over a 3-week period while assets rose more than 25% was in late June 2013. TLT sold off a bit more, then rebounded strongly.

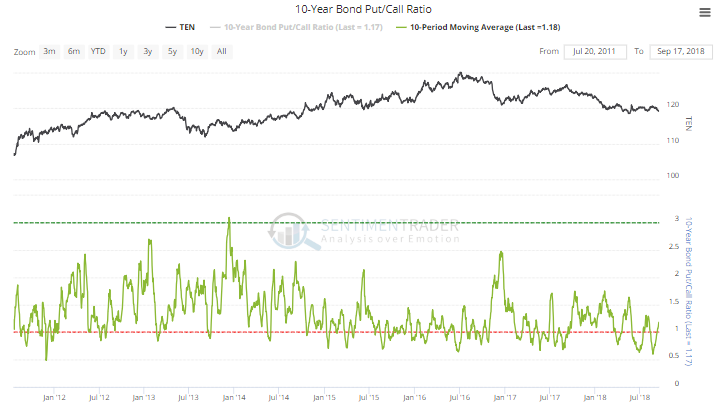

The setup isn't quite perfect, though. There is still no evidence of options traders betting heavily on a decline.

Options indicators on bonds aren't as consistently useful at extremes as they are in stocks, but it's still a worthy indicator. Past bottoms in bonds have usually coincided with a pickup in put option activity, which we're not seeing yet. In fact, the 10-day average of the 10-Year Treasury Put/Call Ratio is only now coming out of overbought territory.

That's also in line with extremely low implied volatility in bonds.

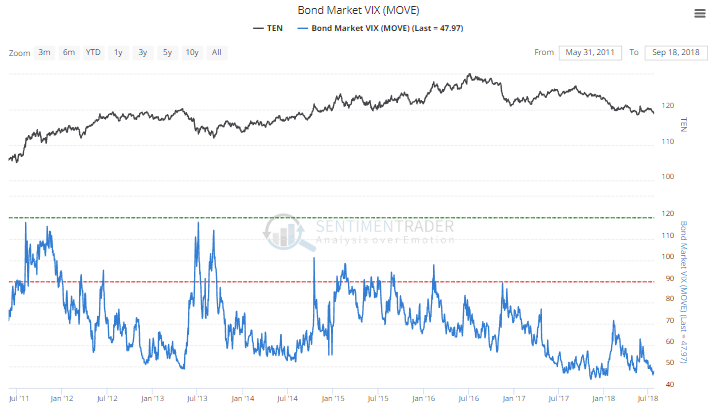

The "VIX" for the bond market is ticking along near all-time lows. This doesn't behave like the VIX for stocks, though. Volatility in bonds is just as likely to rise when bonds rally hard as when they fall, unlike stocks where stocks and volatility move almost exactly in opposite lockstep. There seems to be a slight bias toward lower prices in bonds when the MOVE index is low, but I'm not reading too much into it.

Most compelling is the Optimism Index, which takes into account a number of factors noted above. The fact that it's near the lowest level in 15 years is notable. There have been bold predictions that the decades-long bull market in bonds is over. If bonds (and TLT) continue to decline in the weeks ahead despite this negative sentiment, then those arguments will have some good support.