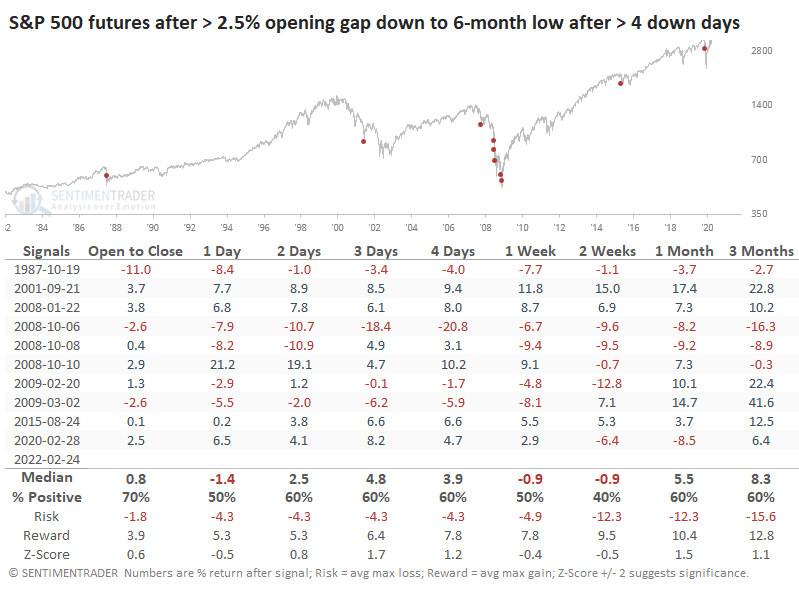

Big gaps down following heavy selling

Big gaps down in equity futures tend to generate questions about whether it's a good idea to step in. This is a quick note to show similar behavior, based solely on the price action and having nothing to do with the context of fundamentals, economics, or geopolitical events.

This morning's gap is currently indicated to be more than 2.5% below yesterday's close. We use the pit-traded S&P 500 futures contract for these figures until the pit was closed in March 2020 and SPY intraday prices following that.

When the futures gapped down more than 2.5% to at least a 6-month low, following what had already been at least 4 consecutive negative closes, there was a surprisingly weak buy-the-dip mentality. Stocks did tend to rise from the open to the close, but returns in the days following were relatively weak.

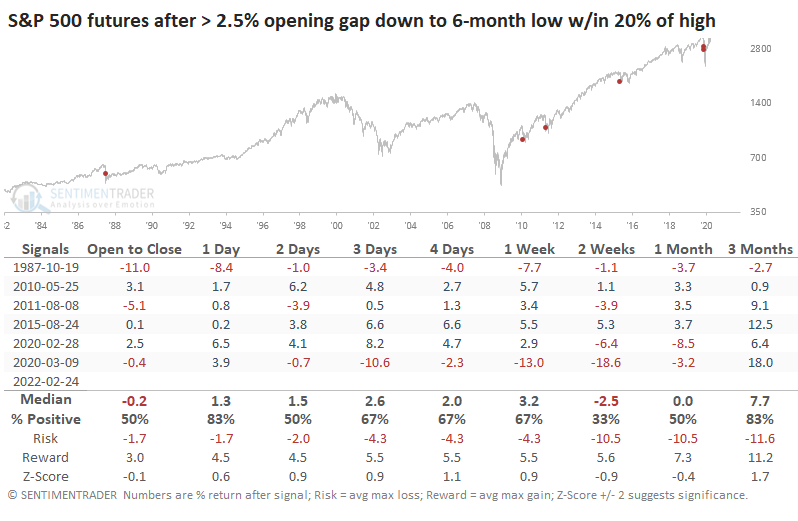

One wrinkle this time is that the S&P is still not in a bear market, while many of those occurrences were. We get the following results if we look at 2.5% gaps down to a 6 -month low when the S&P was within 20% of its most recent 52-week high.

While most of these preceded high volatility, only the shocks in October 1987 and March 2020 led to significant losses in the days ahead. The sample size is tiny (and doesn't grow even if we look at 2% gaps), but the other 4 instances all led to rebounds in the very short-term.

We're dealing with exceptional circumstances, though we could assert that's the case every time we see activity like this. Based on traders' reactions to extreme price gaps at the open, there is a weak case to be made that buyers are likely to step in, with a rally modestly likely over the next several days. Still, even if that's the case, some testing of the low would also be likely in the weeks ahead.