Assessing the pros and cons of silver speculation

Key points:

- There are several factors pointing to a favorable outlook for the price of silver

- Silver futures are leveraged and volatile, but there is an ETF available that allows any investor access

- Options on SLV can offer an even less costly alternative, but the key is understanding the relative pros and cons

SLV as an alternative to silver futures

Earlier this week, I looked at a potentially favorable outlook for the price of silver.

The purest play on silver is to buy or sell short silver futures contracts. The good news is that because of the leverage involved with futures trading, there is potential for substantial profits if you get the price direction correct. The bad news is that leverage is a double-edged sword, and massive losses are also a distinct possibility.

Most investors never will - and probably never should - trade silver futures. Luckily, thanks to the advent of ETFs, there is an alternative. SLV is an ETF intended to track the price of silver futures, and investors can buy and sell shares of SLV just as they would any other stock.

The chart below shows SLV's daily chart since it started trading in 2006, along with a 200-day moving average.

Even though it's not inherently leveraged, SLV still has the potential to make substantial price moves. Looking at the latest action on the far right, a trader can see whatever they want.

A trader with a bullish leaning will see a market that is in the early stages of a new advance, breaking out above its 200-day moving average. A trader with a bearish leaning will see a market making a series of lower highs and overbought in the short term.

Making a bullish play in SLV

Let's consider alternatives for playing the bullish side.

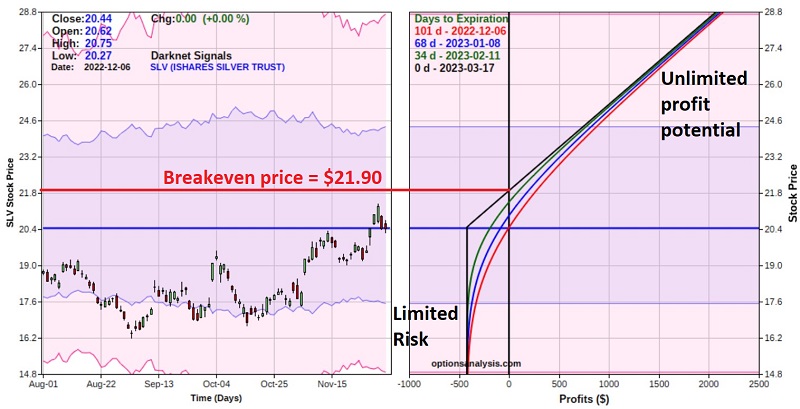

SLV closed at $20.44 a share on December 6. Let's assume a trader with a $25K account is willing to risk 2% (or $500) on silver. This trader would pay $2,044 to buy 100 shares and then need to place a stop-loss 5% lower at $19.41 a share. This is not an unreasonable approach, since $19.41 would involve a drop below the supportive 200-day moving average. However, it doesn't give SLV much wiggle room.

Let's consider an alternative trade. This one involves:

- Buying 3 SLV Mar17 2023 20.5 calls @ $1.40

The particulars for this trade and the risk curves (i.e., the expected P/L at various prices for SLV on dates leading up to option expiration) appear below courtesy of Optionsanalysis.

Things to note:

- The cost to enter this trade is $420, which also represents the maximum potential loss

- For a trader with a $25K account, this amounts to 1.7% of capital

- The breakeven price equals the option strike price plus the premium paid (20.50 + 1.40 = $21.90)

- SLV must exceed $21.90 between now and 2023-03-17 for this trade to show a profit

- Above $21.90 profit potential is unlimited

- If the trade is held until expiration and SLV is below $20.50 a share, the option will expire worthless, and the maximum loss of -$420 will occur

Is this a good trade? The honest answer is, "it depends."

Comparing a call option to a position in SLV shares

Every option trade has specific pros and cons compared to buying shares of the underlying security. So, let's illustrate this with an apples-to-apples comparison.

The Greek term delta is used in options trading to denote a stock equivalent position. A closer look at the trade particulars above reveals that at the time of purchase, the March 20.5 call has a delta of 55.29. So, buying a 3-lot gives us a position with a net delta of 165.86. Let's round up to 166. Note that delta values can and will change based on price movement in the underlying and the passage of time. But for the moment, a delta of 166 tells us that this position will behave like a position holding 166 shares of SLV.

The first thing to note is that to buy 166 shares of SLV at $20.44 a share requires a capital commitment of $3,393 (166 x $20.44). So right off the bat, one advantage of the call option position is that it costs only 12.4% as much to enter ($420 vs. $3,393).

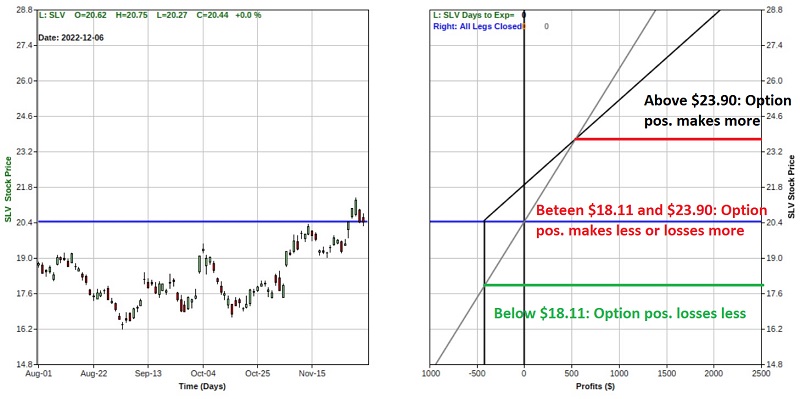

Let's overlay the risk curves for the two positions to illustrate the pros and cons. The black line in the chart below displays the expected $ + (-) for the call option position. The grey line shows the expected $ +(-) for the long 300-shares of SLV position.

The most important considerations in assessing pros and cons

First, remember that the call option has an expiration date, and the share position does not. In other words, while the 300 shares position costs considerably more to enter, they can be held indefinitely. On the other hand, SLV must move higher before mid-March for the call option position to generate a profit. If the big, anticipated move in the price of SLV does not occur until April, the holder of March calls is out of luck.

Above roughly $23.90, the call option position will generate a more significant profit than the SLV shares position. The implication: if the purpose of this trade is to maximize profitability based on a firm belief that SLV shares are about to rocket higher over the next three months, then the call option position is a better bet since it will generate a higher profit and a sharply high ROI based on its sharply lower cost.

Between $21.90 and $23.90, the option position will generate a lower $ profit than the SLV shares position

Between $20.40 and $21.90, the option position will show a loss versus a gain for the SLV position. This is the real "con" to the option position. SLV shares can remain unchanged, yet the option position experiences a 100% loss of premium! A trader must understand this possibility and be mentally prepared, so such an outcome does not adversely affect decision-making on future trades.

Between $18.11 and $20.40, the option position will show a larger $ loss than the SLV shares position. This is a function of time decay. The trade particulars screenshot above indicates that the option position has a "Theta" of -$2.25. That shows that the option position will lose roughly -$2.25 in value each day due solely to the passage of time. Here too, the call options trader must accept this potential outcome (i.e., the holder of SLV shares still holds their position with a smaller loss than the options trader, and the options trader experiences a 100% loss of the premium paid).

Below $18.11, the holder of SLV shares will continue to lose -$166 for each $1 decline in the price of SLV shares. The maximum risk for the options trader is -$420, no matter how far SLV might fall.

So, at this point, the advantages of the options trade are clear: Far lower cost of entry ($420 vs. $3,393), greater profit potential, and absolute limited risk. As I mentioned, though, every potential option position involves a trade-off. This one is no exception.

Remember, there are no free lunches.

What the research tells us…

For a non-futures trader, the most straightforward approach for a trader who believes that silver will advance in price is to buy shares of ETF ticket SLV. Forgetting stop-losses, this trader has no time constraints and can hold SLV indefinitely, hoping that silver eventually explodes higher. The holder of the options trade highlighted above faces a very different proposition. They essentially are on the clock. SLV must make a substantial percentage move higher between now and mid-March for their position to pay off. And there is no guarantee that silver will rally between now and mid-March 2023.

So, the critical question to ask and answer before entering either position is: "How confident am I that SLV will move higher over the next three months?"

Another important consideration: "If I buy the calls and suffer a 100% loss while SLV simply remains unchanged, will that psychologically impact my decision-making going forward?"

Honest answers to these critical questions are essential.