Another potential volatility play

Key points

- Spikes in the VIX Index often tend to reverse quickly

- This is especially true for ticker VXX, which already has a built-in downward bias

- A spike in bullish trader sentiment for VXX just flashed a signal

A quick refresher

As discussed in this piece, the VIX Index tracks the implied volatility for options on the S&P 500 Index. Typically, the VIX Index rises when there is fear in the market and declines when fear is low or on the decline. Ticker VXX is an exchange-traded note (ETN) that purports to track the VIX Index. However, due to how the fund is constructed, its price has a built-in long-term downward bias.

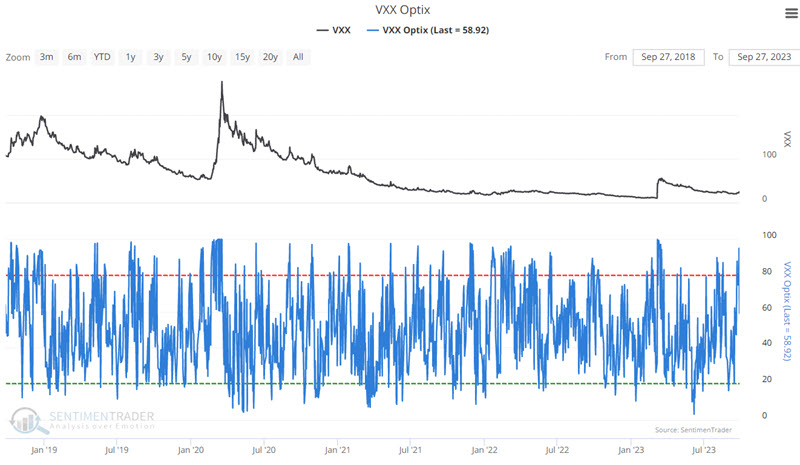

VXX Optix spikes then subsides

The chart below displays the last five years of price action for ticker VXX and our VXX Optix (trader sentiment) indicator. The long-term pattern is well-established - long periods of constant decline interspersed with occasional spikes, some large, some small.

Invariably, when the price of VXX does spike, VXX Optix also tends to shoot quickly higher, ostensibly as investors become more fearful. Now, let's look at a potential way to use these tendencies for trading.

Selling fear after a spike

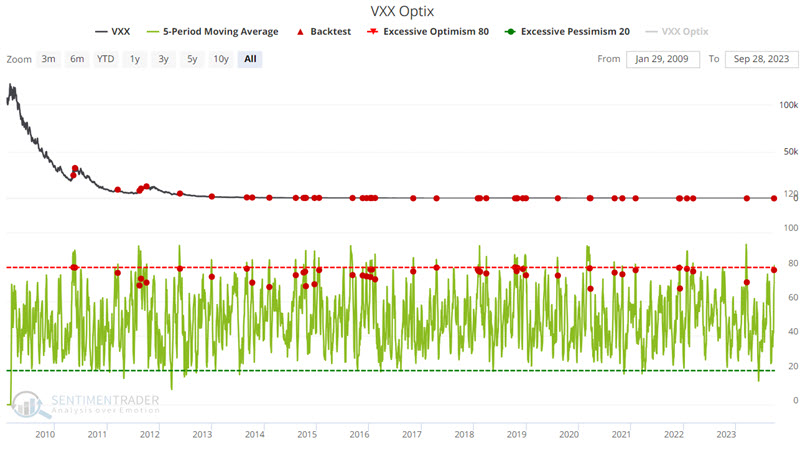

We start with a 5-day moving average for our VXX Optix indicator. The chart below highlights those dates when the 5-day moving average for our VXX Optix indicator crossed below 80%. In other words, there was first a spasm of fear (the 5-day average spiking above 80%), followed by a subsiding of that fear (the 5-day average crossing back below 80). The most recent signal occurred on 2023-09-27.

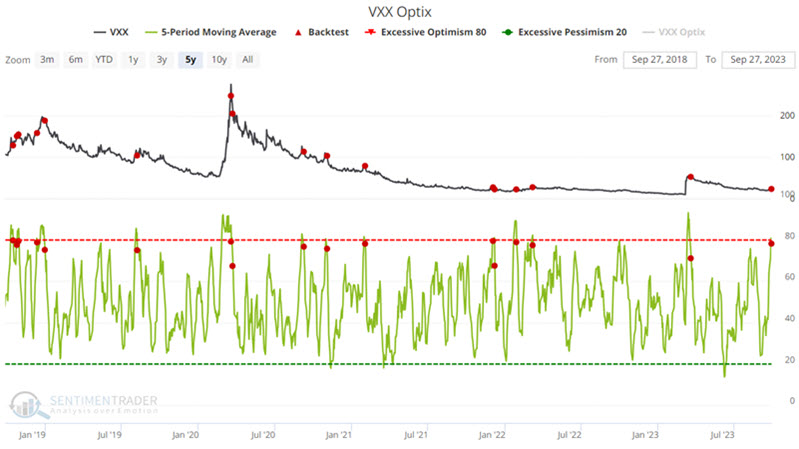

The chart below zooms in on the last five years of VXX activity to get a clearer picture.

The table below summarizes VXX performance following previous signals.

The built-in downward bias for VXX creates something of an "edge" for traders looking to play the short side.

An example options play

The expectation is not so much that VXX will automatically collapse following an Optix signal but rather that the odds favor it not going much higher (although it must also be understood that that will happen from time to time, so risk management remains the responsibility of each trader and on every trade).

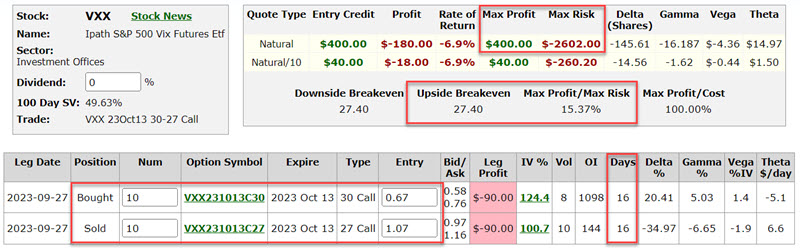

There are any number of potential option trades that could be entered. The one that follows should be considered an educational example, not a specific recommendation. Our example trade uses a strategy known as a Bear Call Credit Spread and involves:

- Buying 10 VXX Oct13 2023 30 Calls @ $0.67

- Selling 10 VXX Oct13 2023 27 Calls @ $1.07

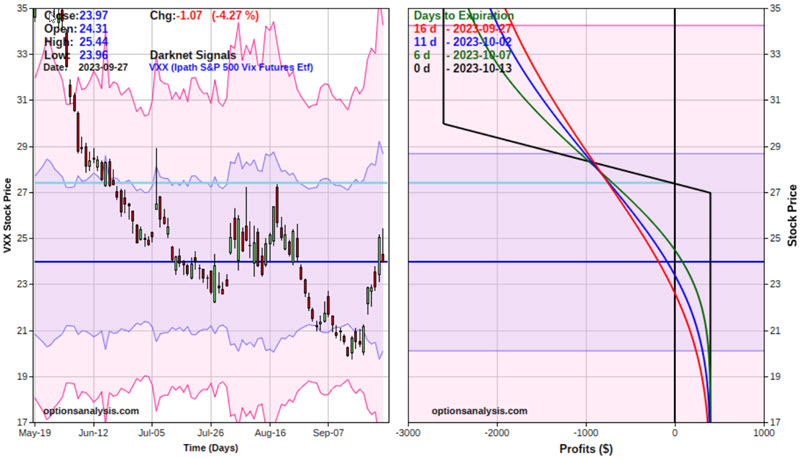

The particulars for this position (trading a 10-lot) and the risk curves (i.e., the expected $ P/L as of four different dates leading up to options expiration based on the share price for VXX) appear in the screenshots below (courtesy of Optionsanalysis.com).

Things to note:

- The maximum profit potential is $400 (this would occur if VXX is at or below $27 at expiration)

- The maximum risk is -$2,600 (this would happen if VXX was above $30 a share at expiration and no defensive action was taken)

- With VXX at $23.97 (as of the close on 9/27), the breakeven price for this position is $27.40

Thoughts on Position Management

There are no hard and fast rules for managing an option trade. Nevertheless, it is essential to long-term success to have a trade plan for each option trade entered. The primary concern for this example trade is that the maximum risk is much greater than the maximum potential profit. One possibility for this trade is to exit the position if VXX shares trade much above the breakeven price of $27.21 a share.

The other concern is when to take a profit. There are only 16 days left until expiration, so as long as VXX is trading below the breakeven price of $27.21, some traders may wish to hold on to collect the entire $400 profit if and when all the options expire worthless. Other traders may be willing to close the trade when 50% to 80% ($200 to $320) of open profit can be realized.

What the research tells us…

Spikes in the VIX Index often end abruptly (except, of course, when they don't, hence the reason risk management plans are always required). Likewise, ticker VXX is even more likely to decline than the VIX Index itself. Spasms in trader optimism have generally (but again, not always) highlighted opportunities to play the short side of volatility.