An update on hedging against a spike in volatility

Key points

- The VIX Index has risen in recent days, and an example option trade from last week is showing a hypothetical gain

- One advantage of trading options is the ability to adjust an existing position

- This piece looks at one potential adjustment to our VXX example trade

A quick refresher

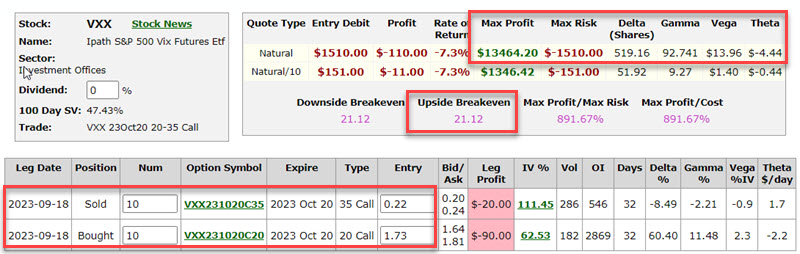

The example trade highlighted in this piece appears in the screenshots below as of the day of entry (2023-09-23). For this article, we will assume the trade was entered as a 10-lot. All charts are courtesy of www.Optionsanalysis.com.

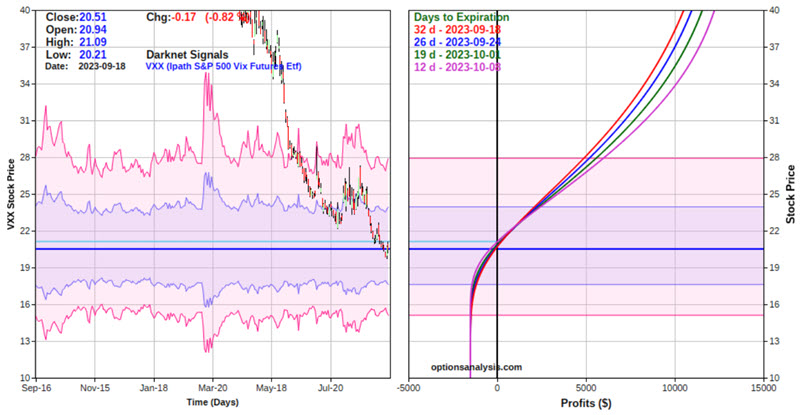

The chart above shows the expected $ P/L for the 10-lot position on four dates leading up to 2023-10-08, our anticipated exit date.

An updated look at the position

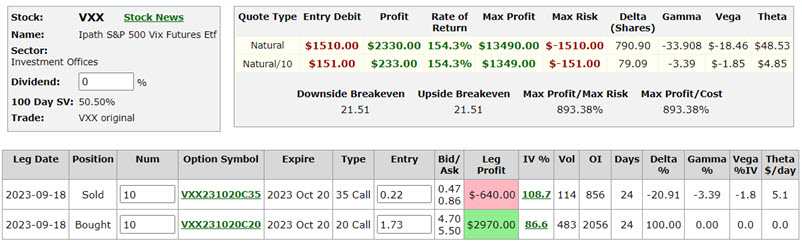

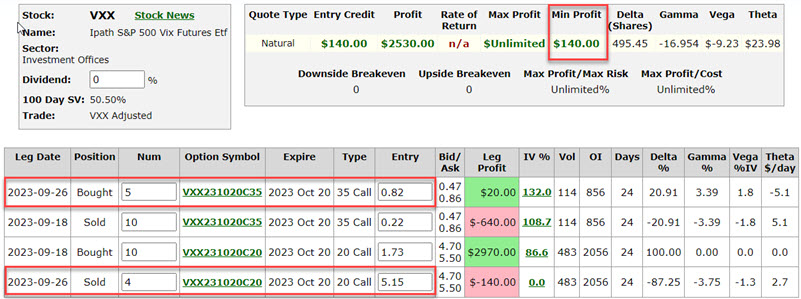

NOTE: All following information is based on daily closing data for 2023-09-26.

From 9/18 to 9/26, ticker VXX rose from $20.51 to $25.04. In the screenshots below, we see a hypothetical open profit of +$ 2,330 for our example trade based on this rise in the price of VXX shares.

This result raises a potential decision for a trader. On the one hand, this trade was highlighted as a way to hedge against a sharp drop in the stock market and a concurrent spike in options volatility. So far, so good - and if the stock market plunges, there is much more profit potential.

On the other hand, the VIX Index - and particularly ticker VXX - has a long history of sharp reversals. If the market selloff ended abruptly and stocks began to rally implied option volatility - and the price of VXX shares - would likely decline significantly. Not only could the $2,330 profit vanish quickly, but the position could still turn into a significant loss.

If a trader thinks the market is headed sharply lower, then retaining the position as it is makes sense. However, another trader might be enticed to adjust the position to lock in a profit while maintaining significant upside potential.

One potential position adjustment

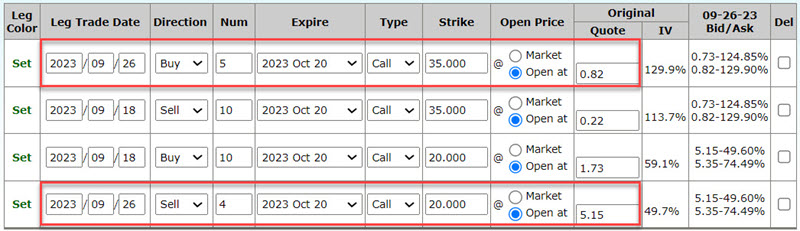

For our example, we will adjust the original 10-lot position as follows:

- Sell 4 VXX 2023 Oct20 20 calls

- Buy 5 VXX 2023 Oct20 35 calls

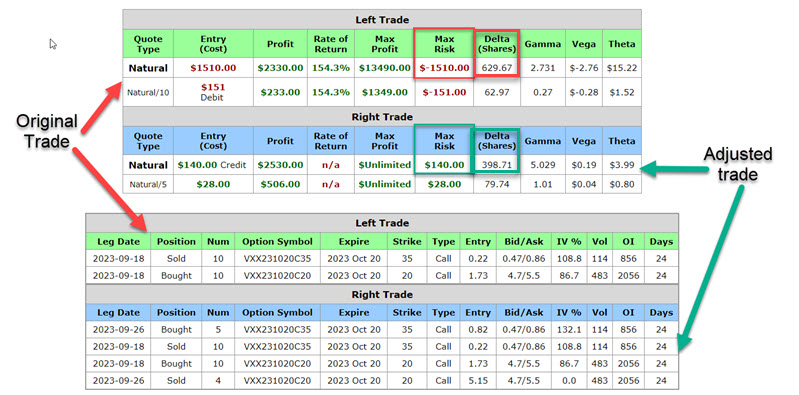

This adjustment would leave us long 6 of the 20 strike price calls and short only 5 of the 35 strike price calls.

The primary benefit of this hypothetical adjustment is that there is no longer a risk of losing money on the trade. As you can see in the screenshot below, the worst-case scenario changes from a maximum risk of -$1,510 to a minimum profit of +$140.

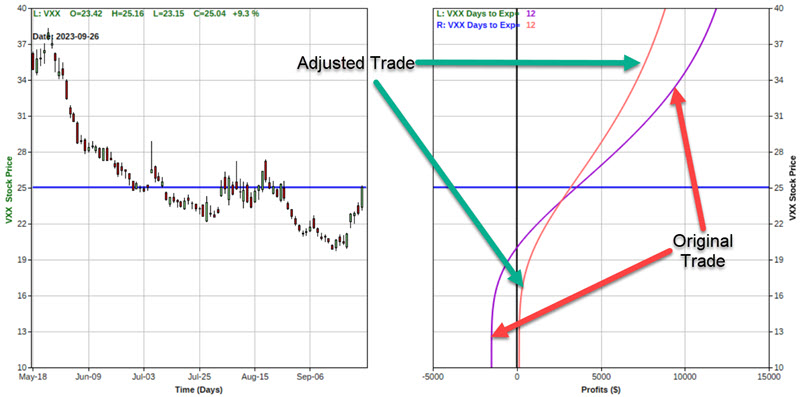

This is also reflected in the risk curves graph for the adjusted position below.

The tradeoff is reduced profit potential

The good news regarding the abovementioned adjustment is eliminating the risk of loss. The bad news is that the profit potential is somewhat diminished. The table below shows that the original position shows a Delta of 629.67. This suggests that for every $1 VXX rises in price, the original position will gain $629.67. The adjusted position shows a Delta of 398.71. This means that for every $1 VXX rises in price, the adjusted position will gain $398.71.

The chart below displays the expected profit/loss for both positions as of 2023-10-08. If VXX were trading at $40 a share as of 2023-10-08, the original trade would show a profit of approximately $11,873, while the adjusted position would show a profit of roughly $8,835.

What the research tells us…

A trader who confidently expects a continued massive spike in volatility might opt to hold the original position in hopes of garnering a more significant profit. Another trader might prefer to eliminate the risk of loss by adjusting the original position and accepting a reduced profit potential.