An unprecedented rise in the 10-year Treasury yield

Key points:

- The 10-year Treasury yield has risen more than 65 basis points over 30 days

- Similar surges with the Fed easing policy suggest the 10-year yield could decline in the near term

- Stocks managed to rally in the face of rising rates, achieving a 100% win rate in the following year

Should we be concerned about the rapid rise in long-term interest rates

Social media is abuzz with traders debating why the 10-year yield is surging and what the trickle-down effect could be on the economy, given that it's a critical lending benchmark.

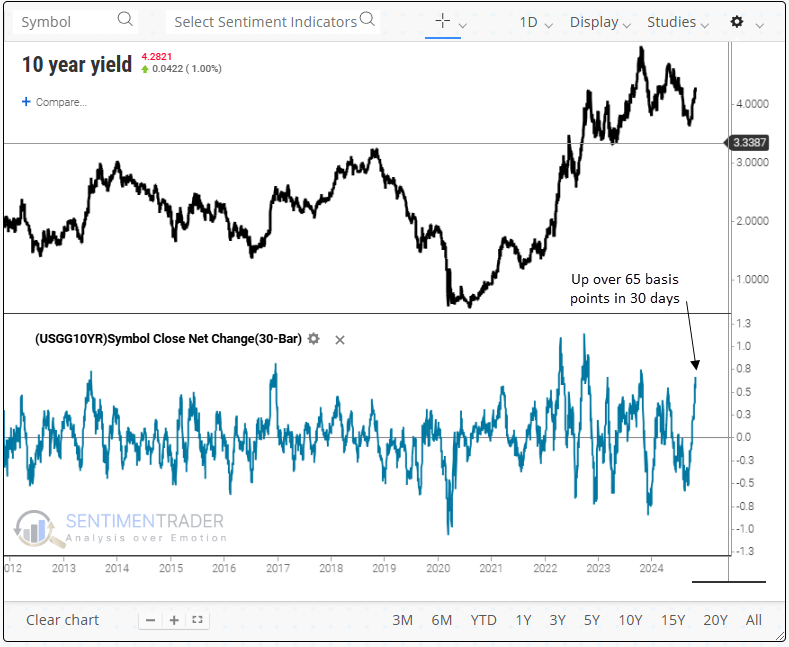

Over a rolling 30-day period, the 10-year Treasury yield has climbed over 65 basis points, a magnitude of change exceeded in only 4% of trading days since 1962.

Although a 65 bps increase over 30 days has occurred 47 other times when using a reset below zero to eliminate repeats, none took place in tandem with the Federal Reserve's initial rate cut until now.

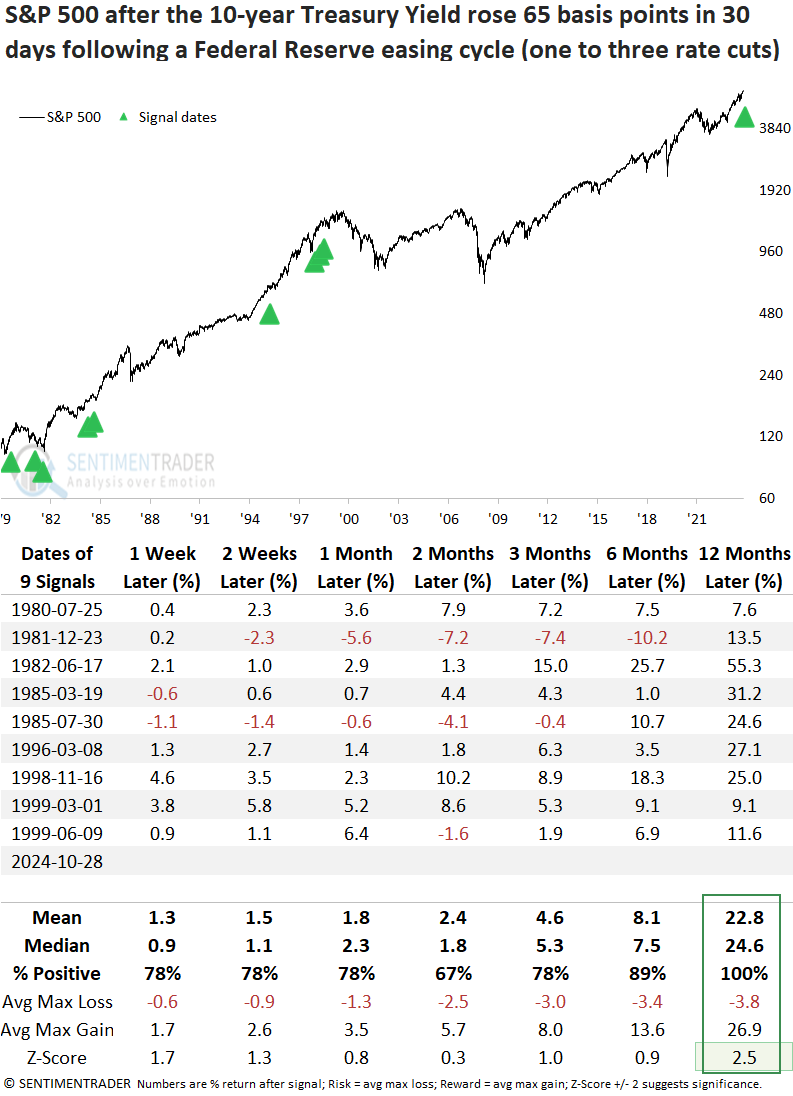

Comparable surges in the 10-year yield preceded a near-term drop in rates

Whenever the 10-year Treasury yield rose by 65 basis points over 30 days, coupled with a Fed easing cycle featuring one to three rate cuts, the benchmark yield often decreased over the following months. From three to twelve months later, yields dropped in the 1980s, whereas post-1995, they tended to increase.

Stocks didn't miss a beat despite a rapid rise in the 10-year yield

Except for an untimely signal in 1981, which occurred within the context of a bear market, a scenario unlike today, the S&P 500 rallied consistently across all time frames, culminating in a 100% win rate over the next year.

The market's ability to absorb a sudden and sharp rise in rates suggests that economic fundamentals were healthy during these periods, providing a positive backdrop for equities.

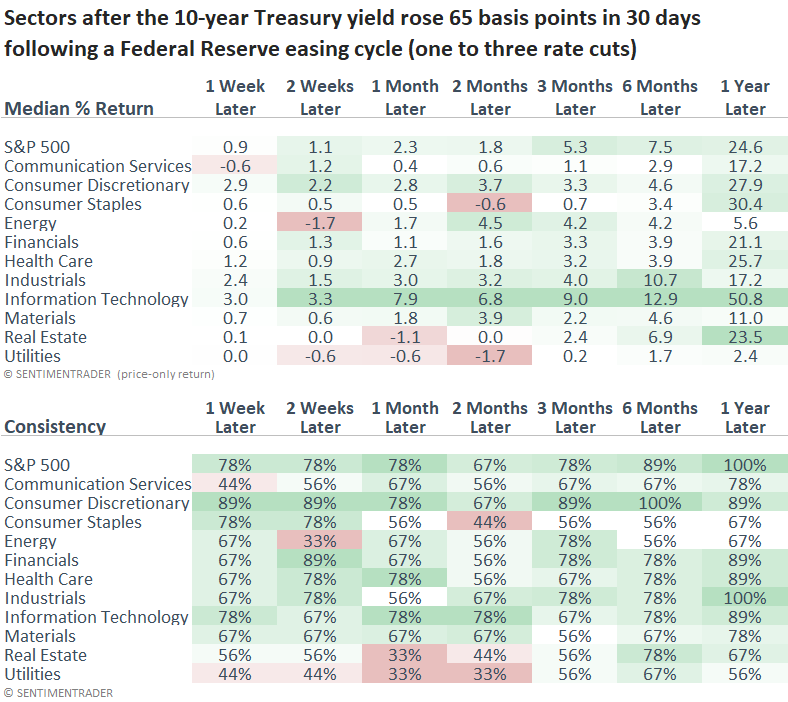

Consistent with their defensive nature, sectors such as Staples, Health Care, and Utilities lagged the S&P 500 over the initial six months. A year later, most sectors, particularly technology, achieved robust returns.

What the research tells us...

Many factors could be driving the sharp and sudden surge in the 10-year Treasury yield. Those include a resilient economy, Treasury issuance, or a technical bounce in yields following a decline. Regardless of the narrative, similar spikes in the 10-year Treasury yield near the outset of a Federal Reserve easing cycle have often reversed, leading to lower yields over the subsequent months. Notably, these reversals have correlated with S&P 500 rallies, especially over the following year. This trend likely reflects a healthy economy that fuels corporate profits, fostering a more favorable stock market environment.