An increase in multiples drove almost all of last year's return

Key points:

- In 2023, most of the S&P 500's returns were driven by an increase in valuations, not earnings

- A rise in the index's P/E Ratio far outpaced the rise in earnings or declared dividends

- After such sentiment-driven years, the S&P didn't perform markedly worse than after years driven by earnings

Last year was driven by an increase in multiples, not fundamentals

Among investors' many concerns as we entered the New Year with a week of declines was that 2023 was an outlier. It was a year when investors shrugged off a multitude of concerns and drove stock prices higher without the justification of rapidly improving fundamentals.

They do have a point.

The rise in a stock (or index) can be due to three primary factors: 1) An increase in earnings per share, 2) An increase in the valuation investors place on those earnings, and 3) Dividends.

Almost all of the S&P 500's returns last year were due to #2, an increase in the valuation investors were willing to put on earnings. Very little of it was driven by an increase in actual earnings per share or dividends. Dividends are almost never the primary driver, but still.

This concerns investors because if the index's rise was due to an expansion in valuations and earnings don't follow through, we have an "all hat, no cattle" situation.

An increase in multiples as primary driver hasn't been a good sell signal

Whether any of this actually matters is up for debate. The table below shows every year since 1960 when the majority of the S&P 500's return in that year was driven by an increase in the P/E Ratio rather than Earnings Per Share (EPS).

Returns in January weren't great, as the index rallied only 40% of the time and suffered a negative median return. But over the next year, returns were about in line with any random year. There was really nothing outstanding about it either way.

If these factors matter, we should see better returns in the index following years when fundamental earnings were the primary driver of returns. These should be years when investors were afraid and didn't place much of an increase in valuations despite better fundamentals.

The table below shows these years, and returns were a bit better than after years like 2023. But it wasn't all that dramatic - the median one-year return was much better, though the mean was not due to a few significant losses. The maximum gains and losses were about the same as in the table above.

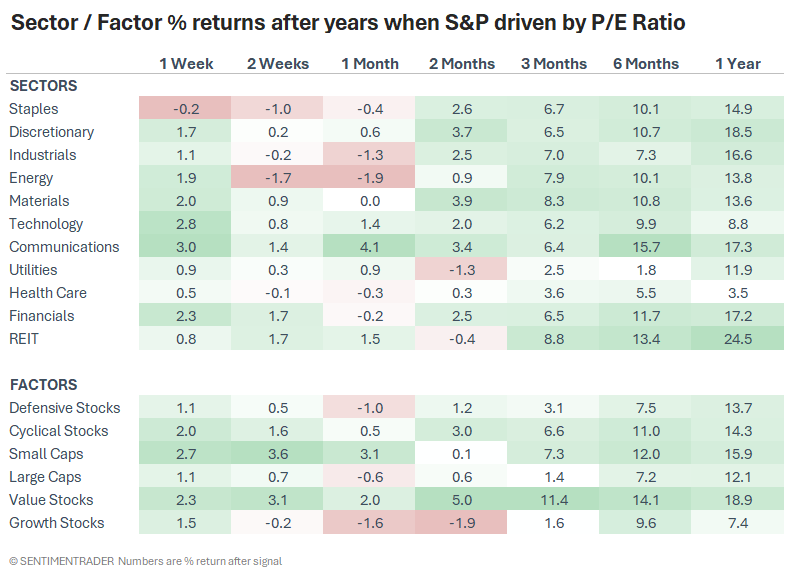

After years like 2023, when the S&P's returns were driven mostly by an increase in the P/E Ratio, Value stocks tended to shine. They showed the most consistent gains across time frames and among the highest returns.

What the research tells us...

Last year, much of the gain in the most benchmarked index in the world was due to an increase in the multiple that investors were willing to give earnings. If those earnings don't follow through and companies earn less than investors expected, then stocks could be very vulnerable to a repricing. In other words, a correction.

The trouble with this line of reasoning is that it hasn't been consistent in the past. When there have been years with most of the S&P 500's gains due to an increase in the P/E Ratio as opposed to a jump in earnings, its forward returns weren't negatively impacted in any consistent way over the following year. Investors' faith in 2023 may turn out to be misplaced, and there could be a very slight argument that an "irrational" increase in the P/E Ratio is bad for forward returns, but most of that is cherry-picking.