An improvement in relative trends across the market-cap spectrum

Key points:

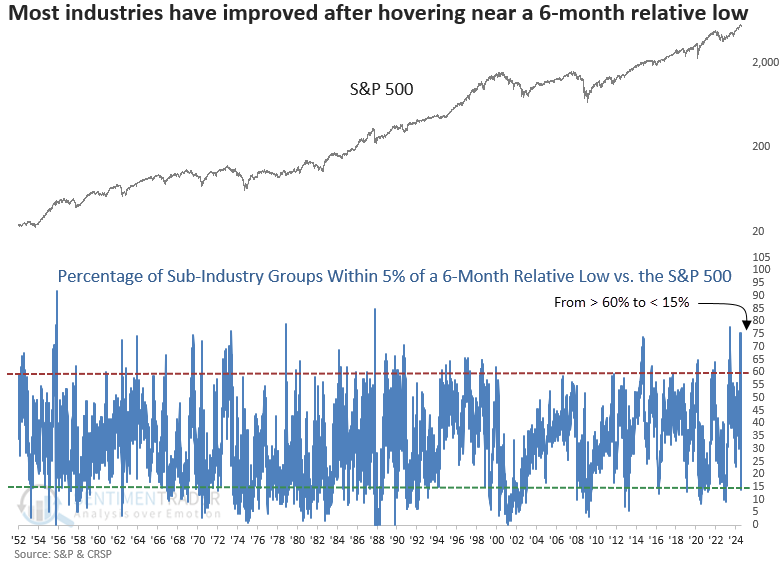

- The percentage of sub-industries within 5% of a 6-month relative low cycled from above 75% to below 15%

- Similar relative trend reversals preceded solid returns and consistency for the S&P 500 over the next year

- Despite several calls for a great rotation, a significant sector theme across all capitalizations has yet to develop

A significant reversal in relative trends

In June, I published a research note highlighting how most sub-industry groups were hovering near 6-month relative lows compared to the S&P 500. At the time, investors were crowding into predominantly mega-cap technology stocks at the expense of everything else.

After climbing to one of the highest levels in history, the percentage of S&P 1500 sub-industry groups hovering within 5% of a 6-month relative low versus the S&P 500 reversed to the downside, indicating an improvement in relative trends for stocks across all market capitalizations.

Because a reversal from above 75% to below 15% has occurred only four other times in history, I lowered the upper threshold to 60% to capture more precedents.

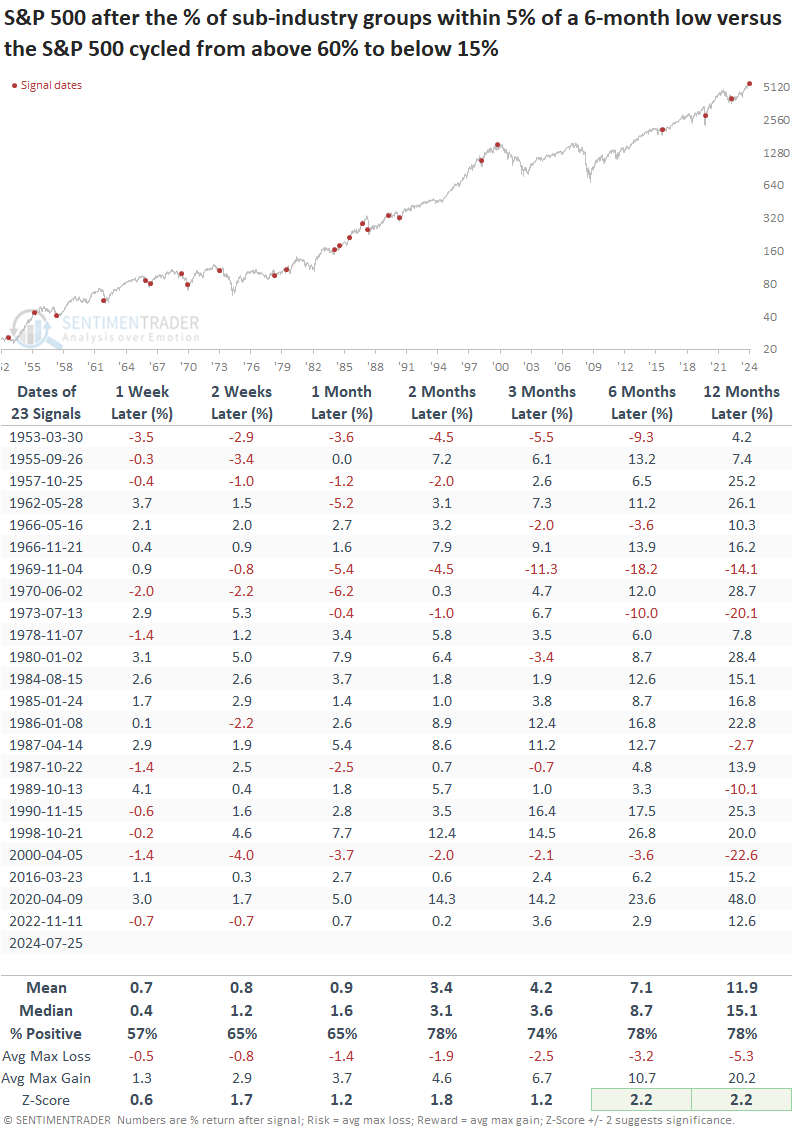

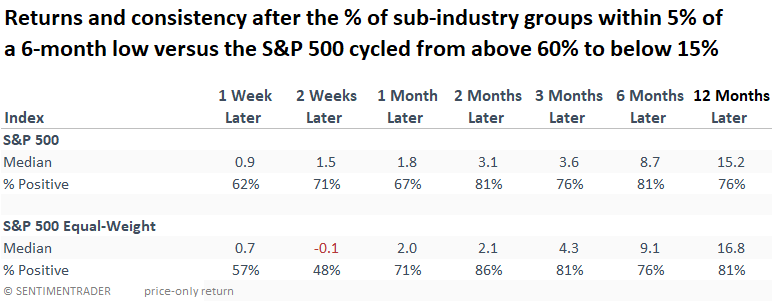

Comparable relative trend shifts preceded positive returns

Whenever the percentage of sub-industry groups within 5% of a 6-month relative versus the S&P 500 cycled from above 60% to below 15%, the world's most benchmarked index demonstrated solid returns and consistency over the following year. Furthermore, six and twelve months later, returns showed significance relative to random returns over the study period.

Suppose I isolated signals that occurred within 5% of a 5-year high in the S&P 500, context similar to now. In that case, the S&P 500 was higher in five out of six instances a year later, with the only loss being in April 2000.

Although most signals appeared after corrections or bear markets, a time when the equal-weighted S&P 500 typically outperforms the cap-weighted S&P 500, the comparison between these two index weighting methodologies does not reveal a decisive advantage for either index.

The above table contains two fewer signals due to data limitations for the equal-weighted index.

Big-picture trends

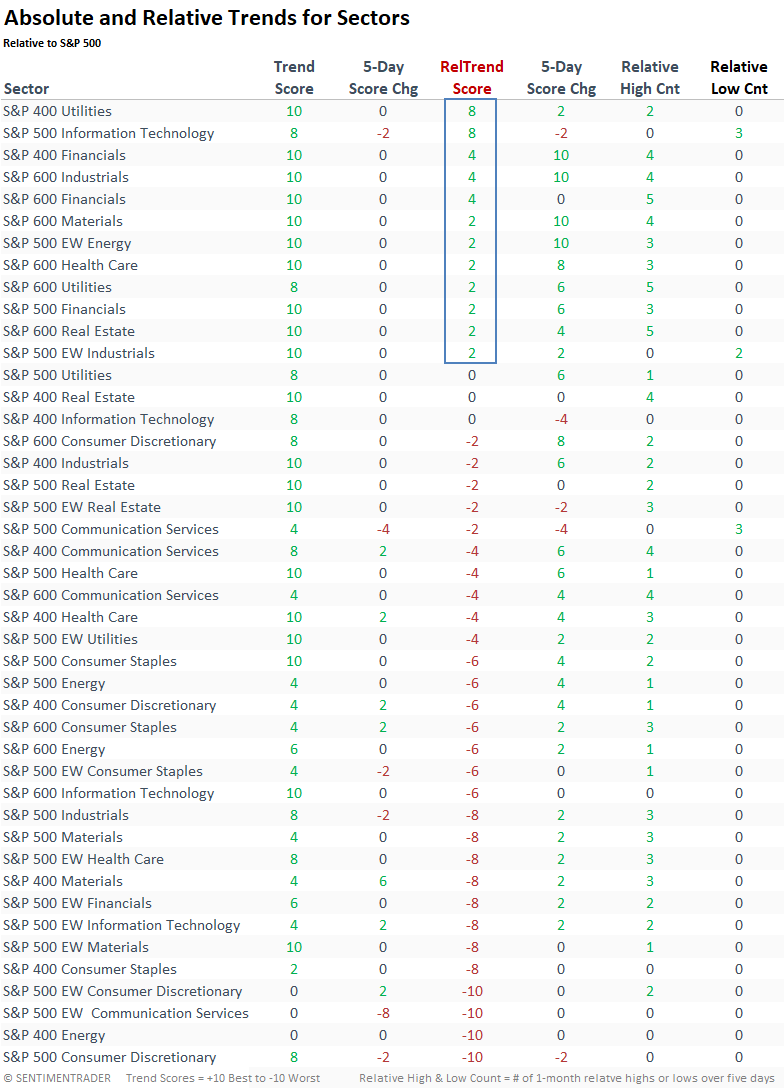

While the research team has highlighted several favorable signals, suggesting a broadening in participation and the potential for improvement in relative trends down the market-cap spectrum, a significant rotation theme has yet to emerge. Therefore, investors should rely upon individual stock selection in companies exhibiting strong absolute and relative trends rather than broadly owning a sector ETF.

What the research tells us...

Relative trends for S&P 1500 sub-industry groups reversed from a high level of groups hovering near a 6-month low to a more favorable stance, indicating improved relative performance down the market-cap spectrum. Similar shifts were more commonly associated with inflection points coming out of corrections or bear markets. Regardless of the environment, returns and consistency were solid, especially a year later.

Despite a swift transition, relative trend score rankings, which employ medium to long-term trend-following indicators, have yet to indicate a significant rotation or emerging sector theme. Consequently, without clear sector leadership, investors should focus on individual stocks with robust absolute and relative trend scores.