An extremely rare sector signal

Key points:

- Not a single S&P 500 equal-weighted sector maintains a positive relative trend score versus the S&P 500

- After similar relative trend profiles, the S&P 500 showed an upward bias, with the EW Index outperforming

- When I adjust the study conditions, an expanded sample size provides a similar message

Does a narrowing in market leadership suggest an unhealthy market

Fewer and fewer stocks and sectors are outperforming the S&P 500. However, narrowing market leadership doesn't always spell doom and gloom for the world's most benchmarked index. Sometimes, investors crowd into the relative safety of meg-cap names or rotate amongst sectors in times of uncertainty.

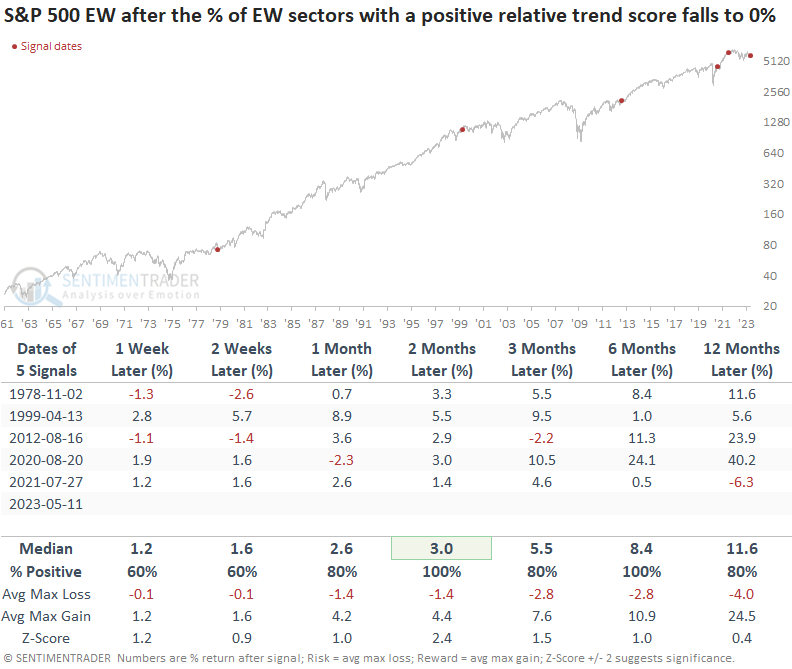

While reviewing sector trend scores last night, I noticed that not a single S&P 500 equal-weighted sector maintained a positive relative trend score versus the S&P 500 Index.

Let's assess the outlook for the S&P 500 under similar narrow leadership conditions.

The equal-weighted Consumer Discretionary sector relative trend score dropped two points on Thursday. In doing so, not a single group maintains a positive relative trend score versus the S&P 500.

Even the market capitalization weighting methodology for sectors shows a narrowing in leadership, with only two positive groups versus the S&P 500. Interestingly, the Communications Services sector maintains a perfect score of 10. In contrast, the equal-weighted version displays a score of -10.

Similar periods of narrow market leadership preceded positive gains

When the percentage of equal-weighted sectors with a positive relative trend score versus the S&P 500 falls to 0%, the S&P 500 had a positive return at some point over the next six months in every case. And the max loss over that same period was -6%.

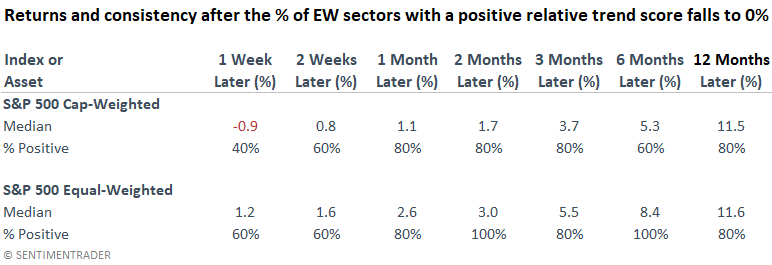

When I apply the signals to the equal-weighted S&P 500 Index, returns and win rates are excellent across all time frames. And, once again, drawdowns were minimal.

Based on the difference between the two index weighting methodologies, one could make a solid case for owning the equal-weighted S&P 500 ETF (RSP) instead of the cap-weighted ETF (SPY).

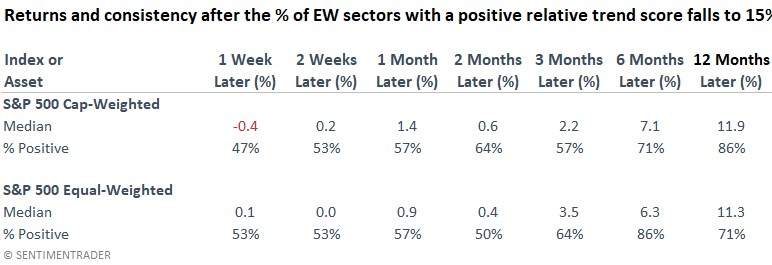

An adjustment to the threshold level

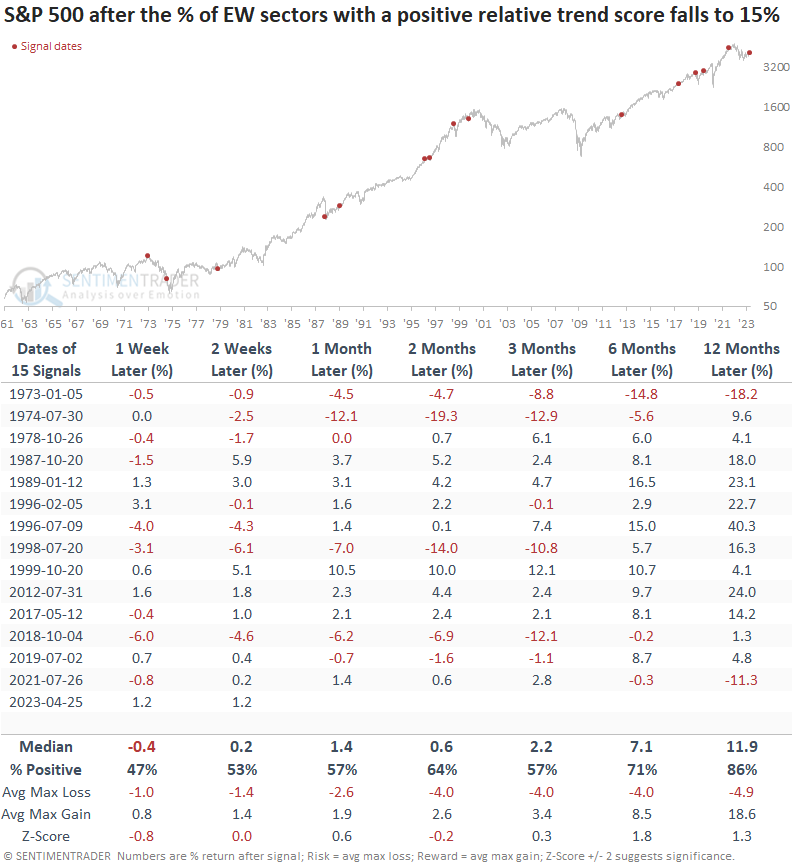

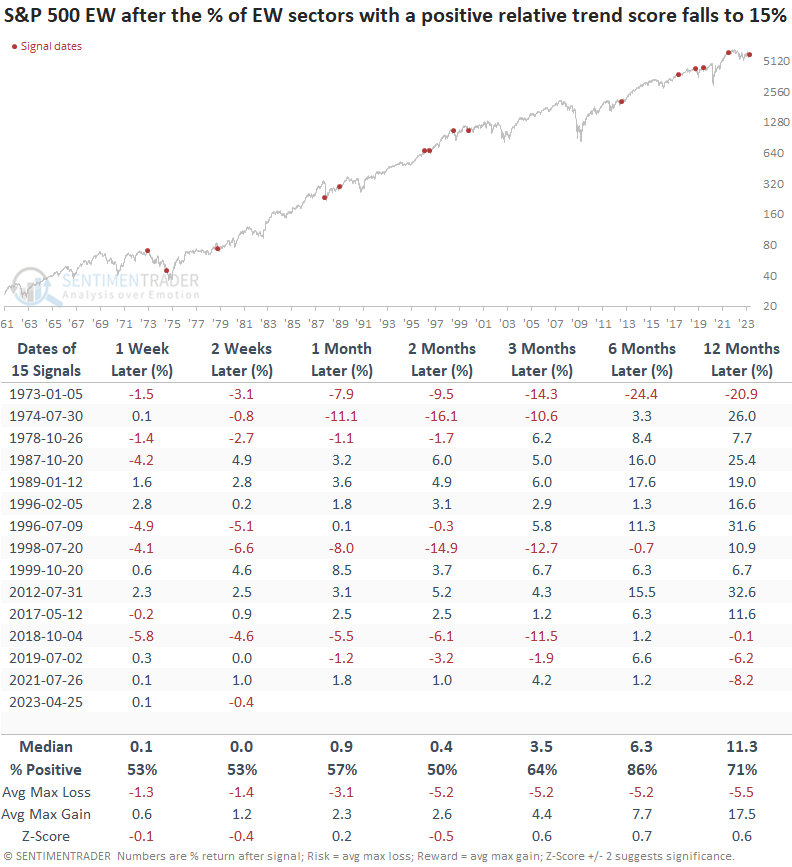

If I raise the threshold from 0% to 15% to capture a larger sample size, the study still shows a bullish upward bias. However, it picks up a few untimely precedents, like 1973, 1974, 1998, and 2018. So, in those cases, the narrowing in market leadership foreshadowed a drawdown phase.

Returns and win rates for the equal-weighted S&P 500 outlook table look similar to the cap-weighted one.

The cap-weighted version shows a slight advantage when I compare the two index methodologies, which is unsurprising as it tends to outperform in drawdown phases.

What the research tells us...

There is no denying that market leadership has narrowed to a handful of issues as uncertainty about the economy and the ongoing banking crisis remains a concern. Despite the uneasiness, other periods with a similar narrowing in market leadership have not produced a doom-and-gloom scenario for the S&P 500. More often than not, the divergence between sectors and the S&P 500 tended to resolve itself with an upward bias in price.