All but 2 sectors are enjoying breadth thrusts

Key points:

- All but two S&P 500 sectors have 89% or more of stocks in medium-term uptrends

- This is one of the widest dispersions of uptrends among sectors since 1957

- After other periods of widely dispersed uptrends, the S&P 500 equal-weight index performed exceptionally well

Almost all stocks in almost all sectors are in uptrends

The average stock has had an excellent few weeks. We've seen that from several different perspectives, like a 52-week breakout in the S&P 500 equal-weight index and nearly all stocks in the S&P 1500 being in medium-term uptrends.

Speaking to those uptrends, Dean pointed out that more than 90% of 1,500 stocks are above their 50-day moving averages. That's an impressive feat and preceded almost universal gains in the months ahead.

Another way of looking at this is the distribution of those uptrends among sectors. If a sector has a lot of stocks that are doing well, it can overwhelm the other sectors and skew the results to the positive side. But the distribution has been extremely broad, as 8 out of the 10 major historical sectors (excluding Real Estate) have 90%* or more of their stocks in medium-term uptrends.

* There is some data mining here because two sectors just barely missed the 90% round number, both exceeding 89% of stocks.

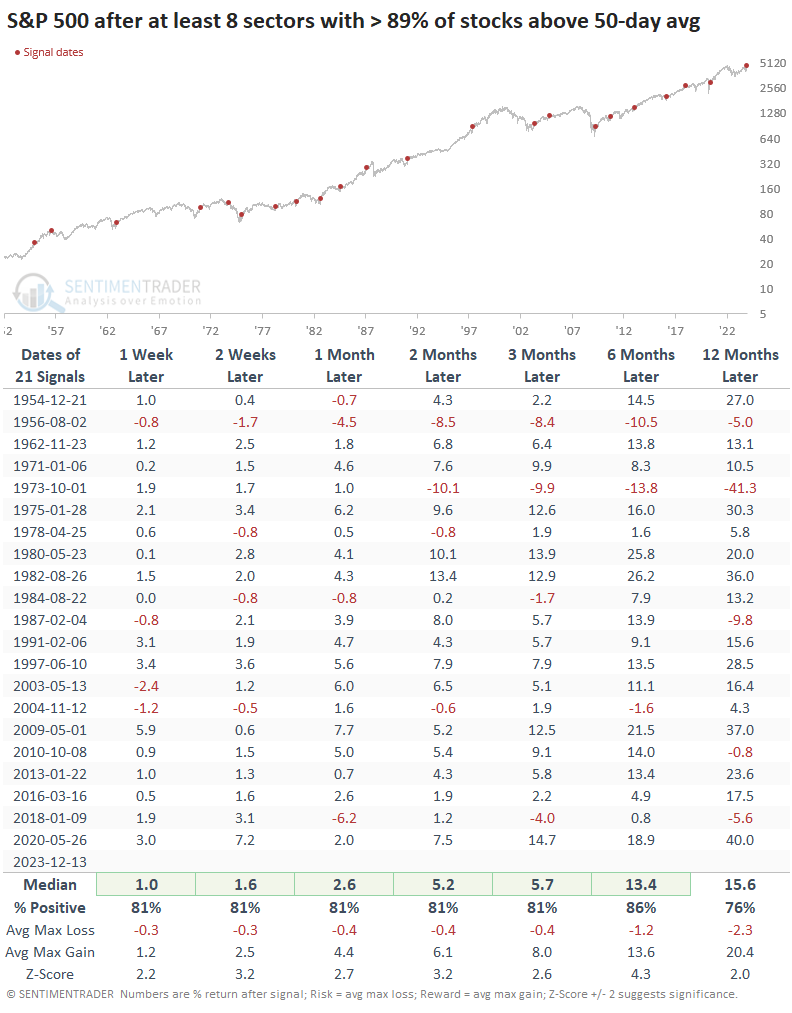

Dispersed participation has been a very good sign

The table below shows returns in the S&P 500 after at least eight sectors had at least 89% of their stocks above their 50-day moving averages. Confirming other studies we've looked at in recent weeks, those returns were quite positive across all time frames.

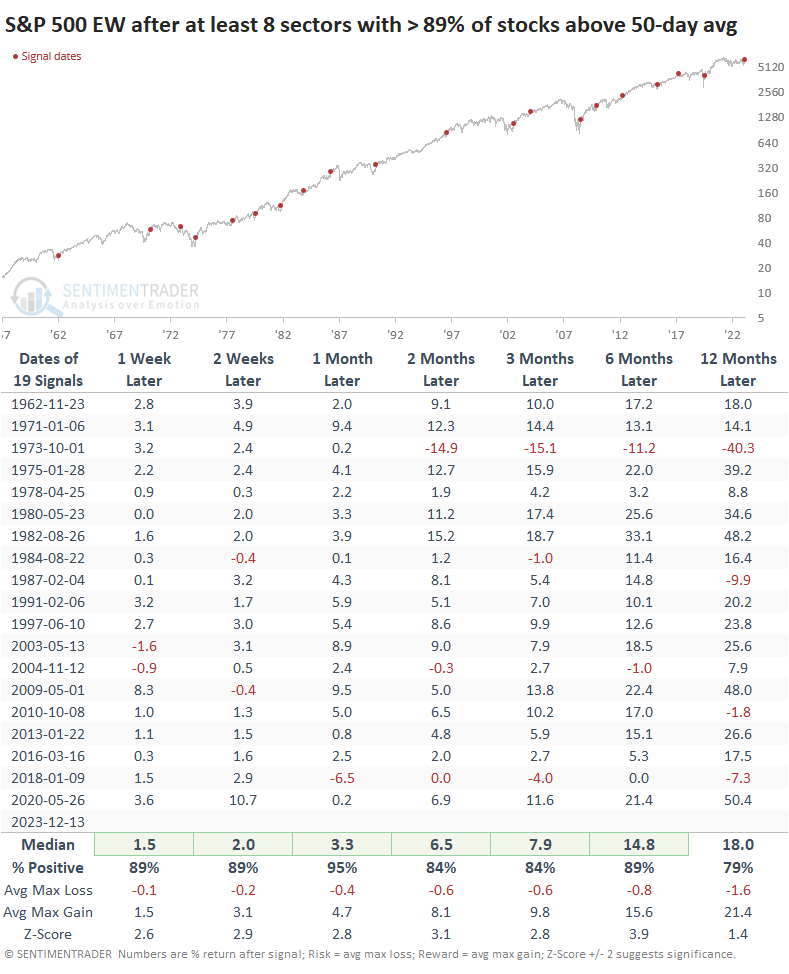

Since the uptrends are so well distributed, looking at performance for the S&P 500 equal-weight index makes sense. There are two fewer signals for this index since we don't have history before 1957. The only major failure was in 1973.

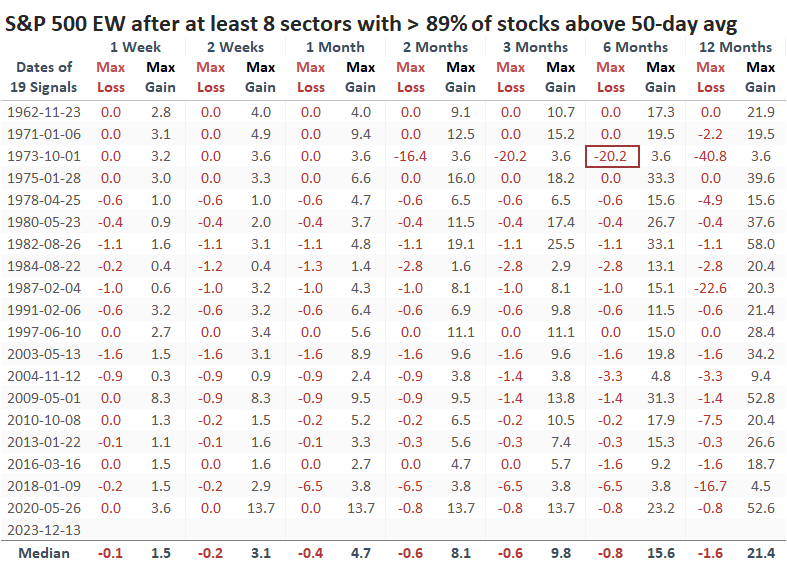

The table of maximum gains and losses across time frames shows that only the 1973 signal suffered a significant drawdown within six months. Remarkably, only two signals witnessed drawdowns worse than -3.3% at any point in the next half-year.

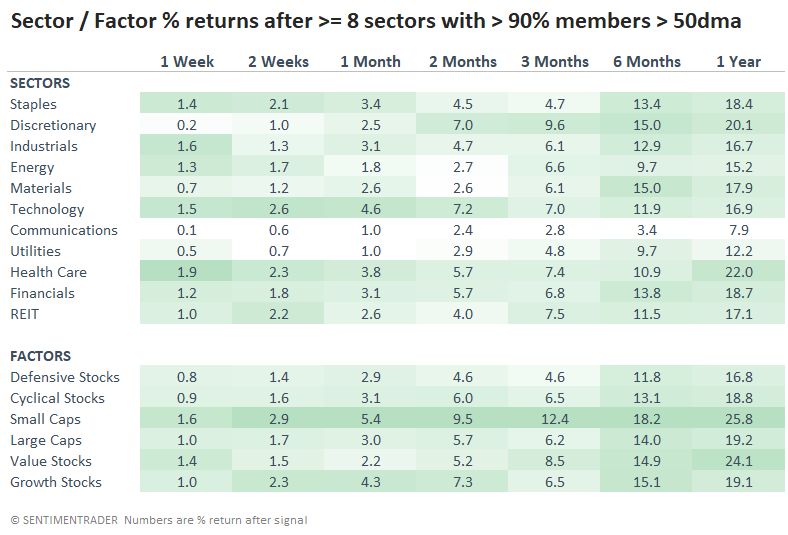

Among sectors and factors, there was a lot of green, which is to be expected given the above. Notably, Small Caps stand out for exceptionally strong returns across all time frames.

What the research tells us...

Since October 2022, we've detailed countless studies about the breadth of the advance at certain points. It has been exceptional, and that rarely, if ever, has occurred during protracted bear markets. Now that most major indexes are at or are within spitting distance of all-time highs, the rally's breadth isn't slowing down much.

While that always raises concerns about an overheated market, and there may be some shorter-term validity to that argument, over a medium- to long-term time frame, participation like this has rarely led to significant declines.