A volume ratio pattern triggered a new buy signal

Key points:

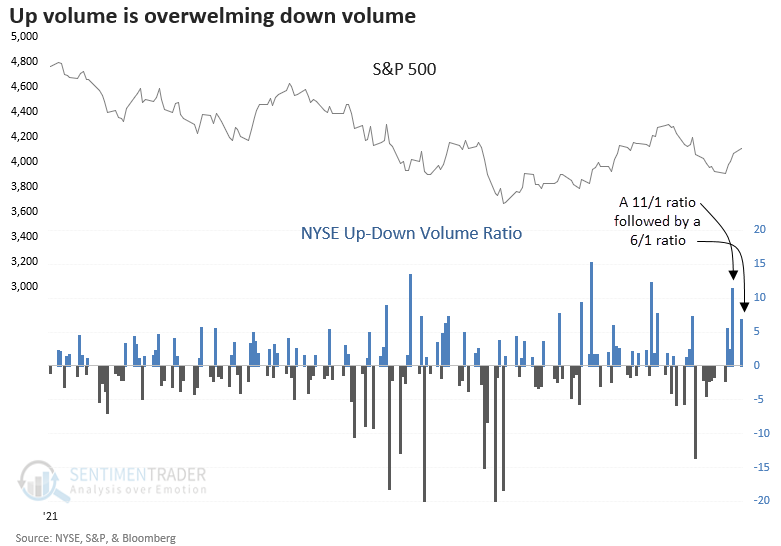

- On Monday, the ratio between NYSE up and down volume exceeded 6/1

- The bullish volume skew followed a ratio of 11/1 in the previous session

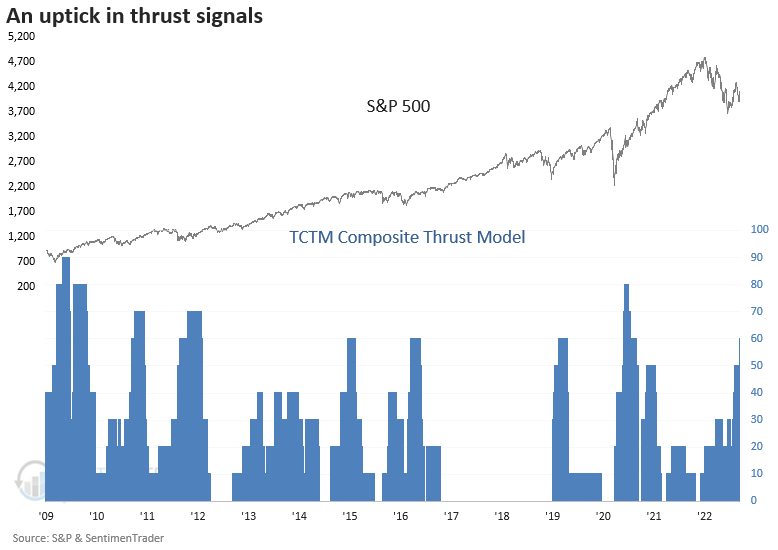

- The volume pattern triggered a signal from a TCTM Composite Thrust Model member

- After other signals, the S&P 500 rallied 92% of the time over the next six months

A short-duration volume pattern suggests demand for stocks

The bullish breadth and volume trends that started last week continued on Monday, with the NYSE up-down volume ratio exceeding 6/1. The bullish skew in volume followed an even more impressive ratio of 11/1 in the previous session.

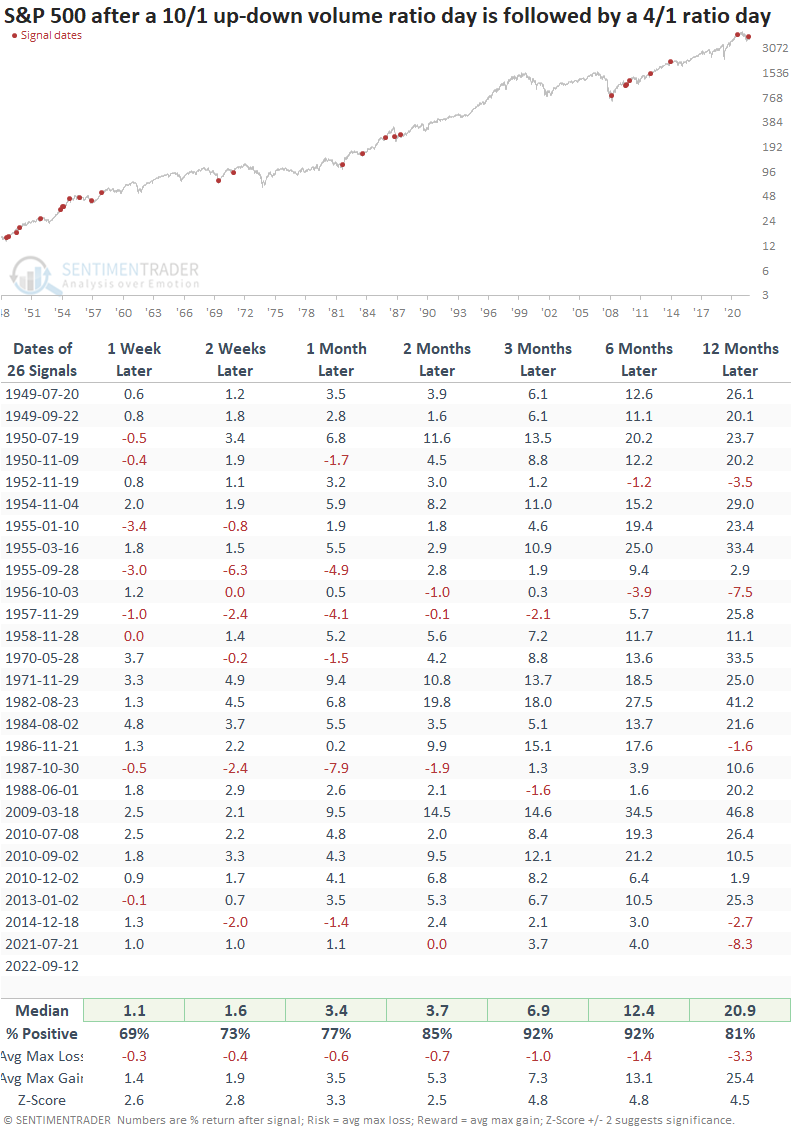

The two-day volume ratio pattern of > 10/1 and > 4/1 triggered a buy signal from a TCTM Composite Thrust Model member.

If today's selling pressure persists, then we'll have to reassess and see if it negates any of the positive implications of the positive thrusts.

Similar signals preceded gains 92% of the time

The volume ratio pattern generated 26 other signals since 1949. Returns, win rates, and z-scores were excellent across all time frames. Once the market moves past the first month, drawdowns were remarkedly benign over the next two to six months, with a worst-case return of -3.9%.

A short-term trend reversal thrust signal

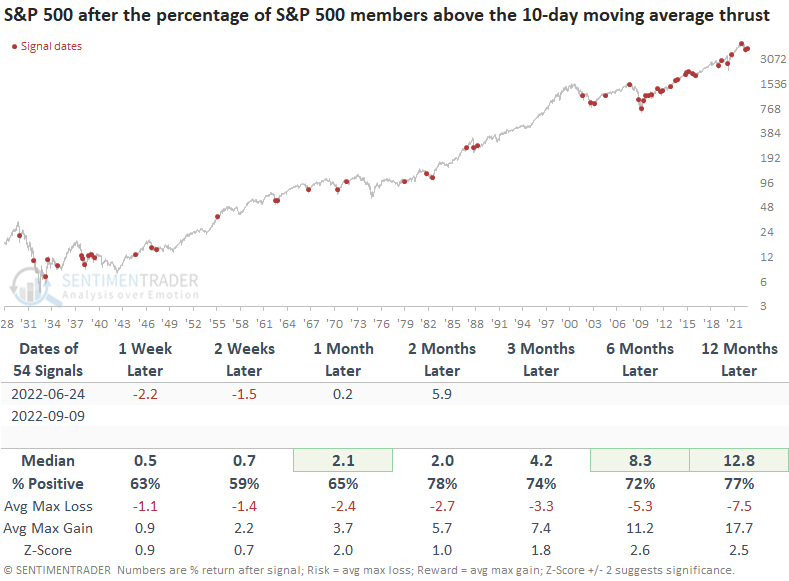

Last Friday, an additional TCTM Composite Thrust Model member triggered a buy signal when the number of S&P 500 members trading above the 10-day moving average reversed from < 7% to > 90% in three sessions. Jason highlighted a similar pattern in his note on Monday.

The previous signal from June got off to a rough start but has since recovered nicely.

Tactical Composite Trend Model (TCTM)

The Composite Thrust Model (CTM) signal count increased to 60% with the new volume ratio signal. If you recall, the CTM issued a buy signal in August when the count increased to 50%.

What the research tells us...

When the ratio between NYSE up and down volume exceeds 10/1 and 4/1 in successive sessions, the surge in up volume relative to down volume suggests demand from buyers that typically leads to further positive momentum. Similar setups to what we're seeing now have preceded excellent returns, win rates, and z-scores across all time frames. As a proponent of a weight-of-the-evidence approach, it's encouraging to see the 10-day average thrust signal trigger in conjunction with the volume ratio alert.