A stock equivalent example using options on SPY

Key points

- Using options can allow an investor to hold a stock equivalent position at a fraction of the cost

- The key is understanding the tradeoffs involved

The stock market has been on fire

The S&P 500 has advanced in 15 of the last 17 weeks, something it hasn't done since 1989. This rally is reflected in the chart below.

Consider an investor without much investment capital who now wants to climb aboard. But they face two problems:

- A lack of money to invest

- There is a concern that the market could suffer a sharp interim decline

So, what's an investor to do? Well, in reality, the possibilities are endless. For this piece, we will focus on one possible approach. As always, the example trades detailed below are just examples, not recommendations.

As our baseline, the figure below (all subsequent figures are courtesy of www.Optionsanalysis.com) displays the expected P/L from buying and holding 100 shares of the SPDR S&P 500 Trust (ticker SPY).

Buying 100 shares of SPY at $505.99 would cost $50,599. From there, for every dollar SPY shares rise, the position gains $100 and vice versa. But for some, a $50K+ commitment might not make sense. Let's look at one example alternative using SPY options.

A surrogate stock position using options

The "Delta" of an option approximates the stock equivalent position for that option at a given point in time (Deltas can and will change based on changes in price in the underlying stock and the passage of time). For example, the immediate risk/reward prospects for a call option with a Delta of 50 is roughly the same as holding 50 shares of the underlying stock. Buying two call options with a Delta of 50 would be approximately the equivalent of buying 100 shares of the underlying stock.

Now, let's get just slightly more creative. The example position below involves the following:

- Buying 2 SPY Apr19 2024 500 strike price calls @ $14.16

- Selling 1 SPY Apr19 2024 520 strike price call @ $4.01

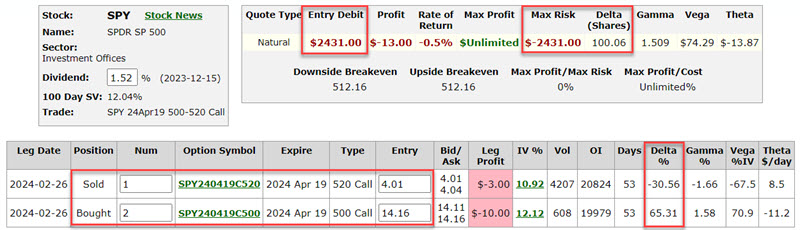

The particulars for this position appear below.

The risk curves (i.e., the expected P/L for the option position at a given price for SPY shares as of a given date leading up to option expiration) appear below.

Things to note:

- This position has a Delta of 100.06 (two long calls with a Delta of 65.31 and one short call with a Delta of -30.56)

- However, the cost to enter this position is $2,431 versus $50,599 to buy 100 shares of SPY (i.e., 4.8% of the cost)

So, is this position a "bargain?" Not necessarily. Understanding the tradeoffs involved is the key to deciding which trade makes more sense for a given individual.

Comparing long shares versus option position

The table below highlights the two trades - one is long 100 shares of SPY, and the other uses call options to create a theoretically equivalent position.

The critical difference between the two is that the option trader pays a certain amount of "time premium" to enter the trade (essentially, this is an amount that an option buyer pays to an option seller to induce the option seller to take on the risk of selling the options in the first place). All options and option positions lose their time premium by option expiration. The rate of this decline in time premium is reflected in the position's "Theta" value. As you can see in the figure above, the option position loses -$13.17 a day in "time decay." The share position has no time decay (i.e., a $1 change in the share equals a $100 change in the position's value, regardless of how long the position is held).

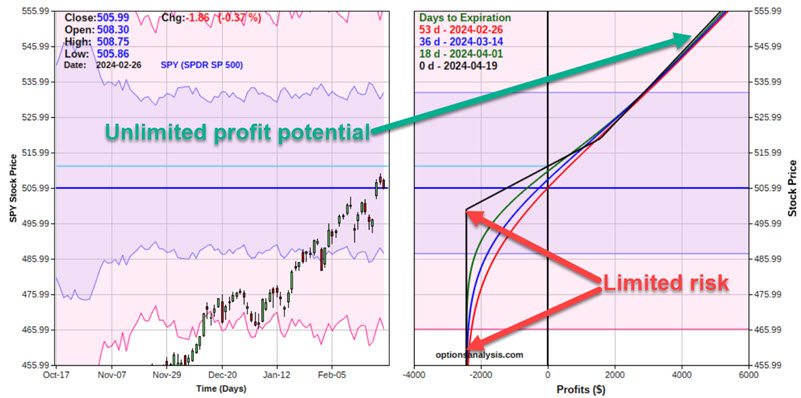

So, let's look at possible scenarios. The chart below shows that if SPY shares rise above roughly $519 a share, the option position will achieve a slightly higher point-for-point gain than the 100 shares position.

At the opposite end of the spectrum, at any price below roughly $484 a share, the option position has a maximum risk of -$2,431, while the stock position has unlimited risk.

So far, the option position looks pretty good. It retains unlimited profit potential and enjoys a maximum risk of -$2,431 (versus a significantly higher risk potential for the 100 shares position if SPY falls significantly).

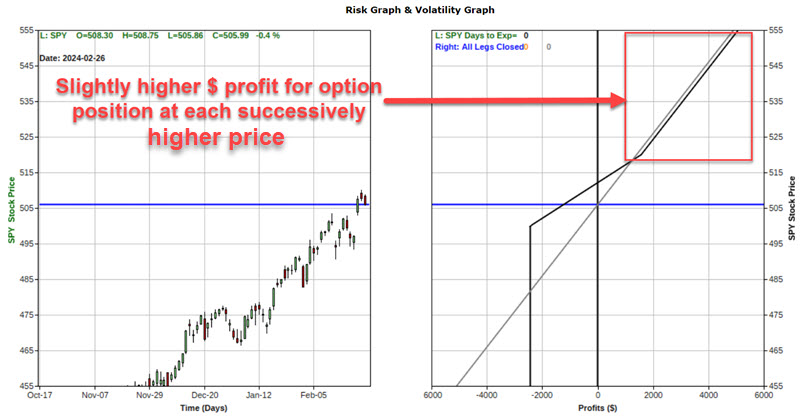

However, there are no free lunches in the financial markets. The tradeoff in this example comes if SPY is between roughly $484 and $519 at the time of option expiration. In that case - and as you can see in the chart below - the option position could suffer a loss larger than that of the investor holding 100 SPY shares. This, once again, is due to the effect of time decay.

The bottom line tradeoff is this: The option position allows one to enter a position that is long 100 Deltas at a significantly reduced entry cost (4.8% in this example) BUT also accepts the risk of a larger loss or smaller profit if the underlying security remains within a particular price range during the life of the option trade.

Another technical note: If SPY trades above $520, the short option could be "exercised" (i.e., the option trader would be required to deliver 100 SPY shares). This could be accomplished by exercising one of the two long 500 strike price calls and delivering those shares. A more practical approach would be to close out the short 520 call and sell one 500 call if SPY approaches $520.

What the research tells us…

Options give investors, well, options. The critical thing to remember is that there are no "best trades," only those that best match a given investor's objectives. There are tradeoffs between any two potential options trades - or any option trade versus long stock shares. The key to long-term success is to honestly assess those tradeoffs and make the decision that best suits your outlook, objectives, and tolerance for risk.