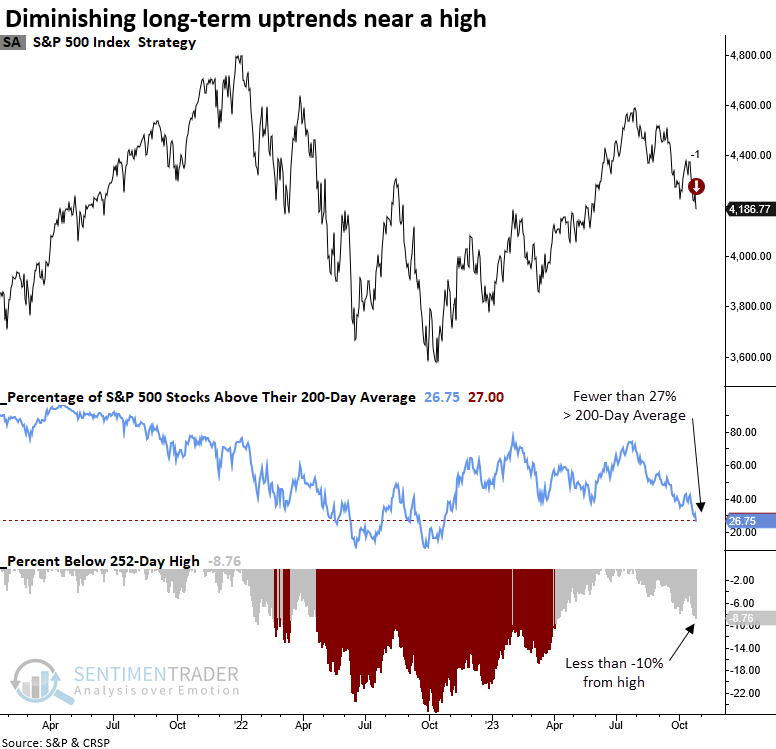

A significant divergence between the S&P 500 and stock uptrends

Key points:

- The percentage of S&P 500 stocks above their 200-day average declined below 27%

- At the same time, the S&P 500 remains less than 10% below its 252-day high

- Similar precedents led to lackluster results for the S&P 500 over the following six months

The impact of higher yields is weighing on long-term uptrends for S&P 500 stocks

On Wednesday, I published a research note highlighting the deteriorating long-term uptrend backdrop for common stocks listed on the New York Stock Exchange.

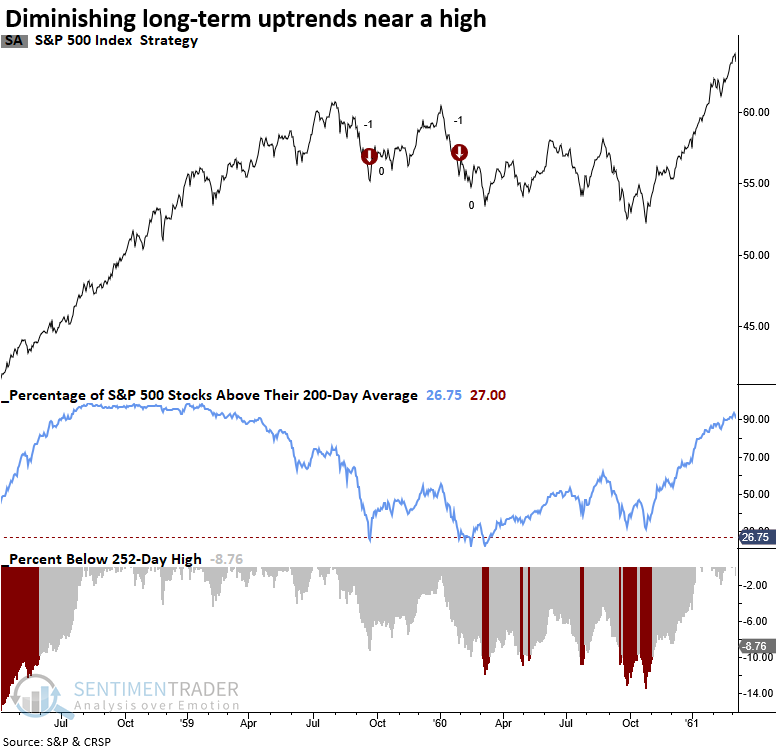

While reviewing S&P 500 market breadth data, I noticed a similar trend, with fewer than 27% of the constituent stocks trading above their 200-day average. However, what caught my attention the most was that so few stocks remained in a long-term uptrend as the S&P 500 was still trading within 10% of its last 252-day high.

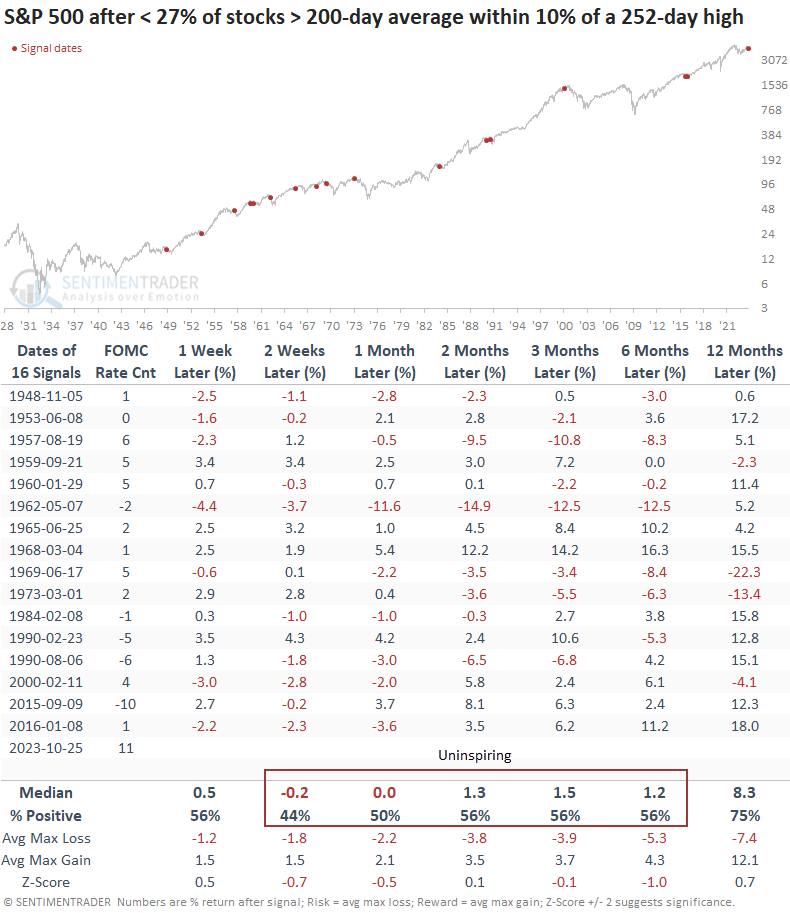

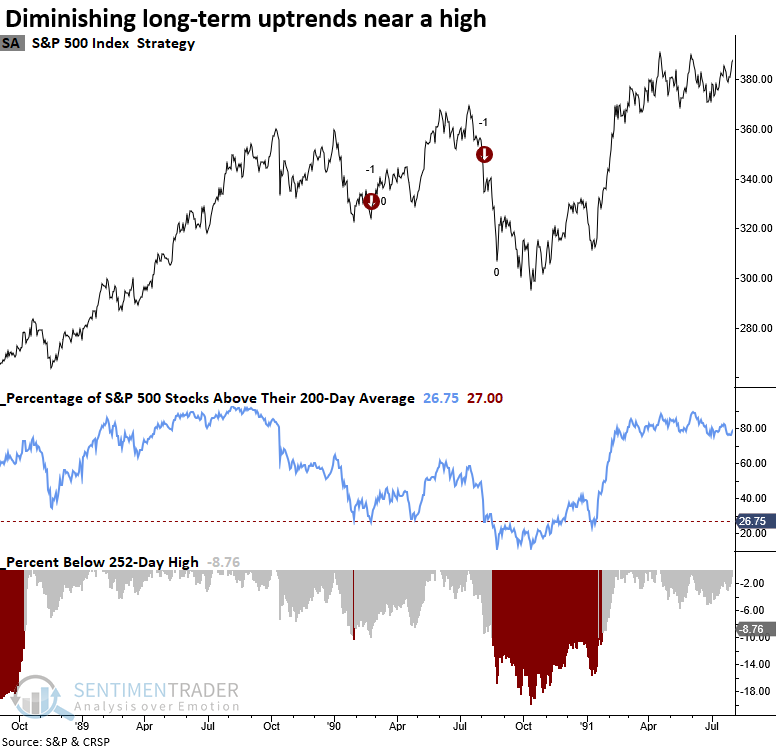

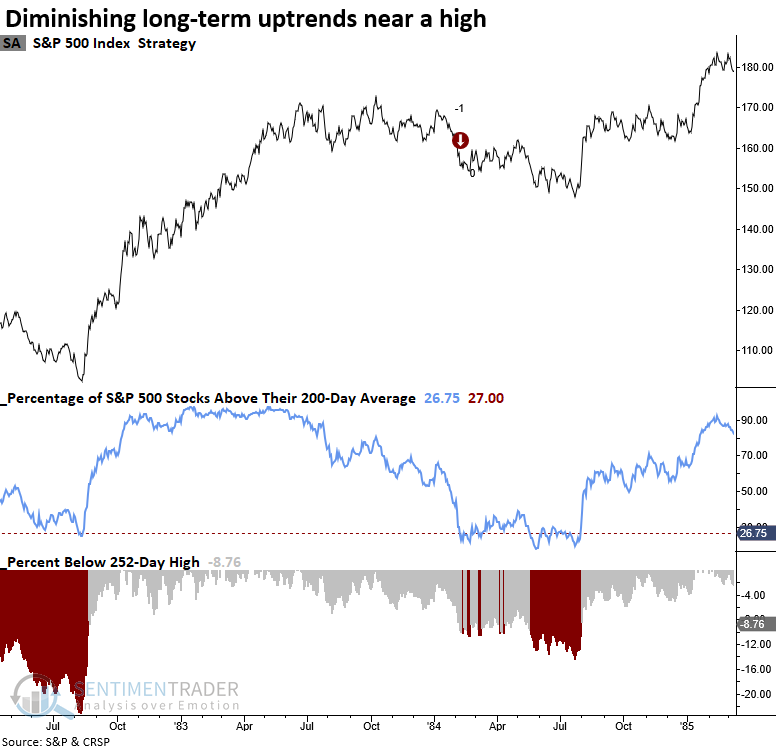

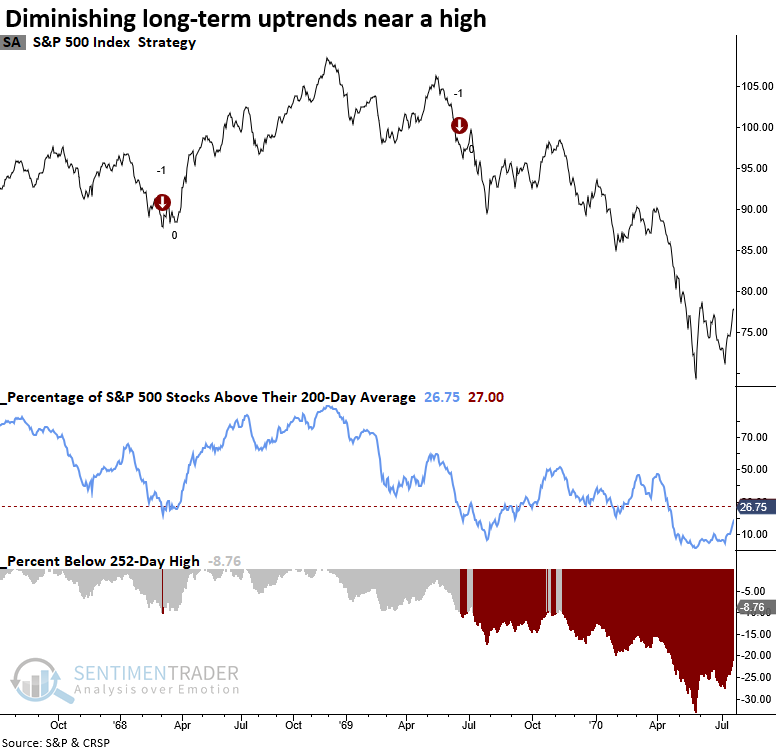

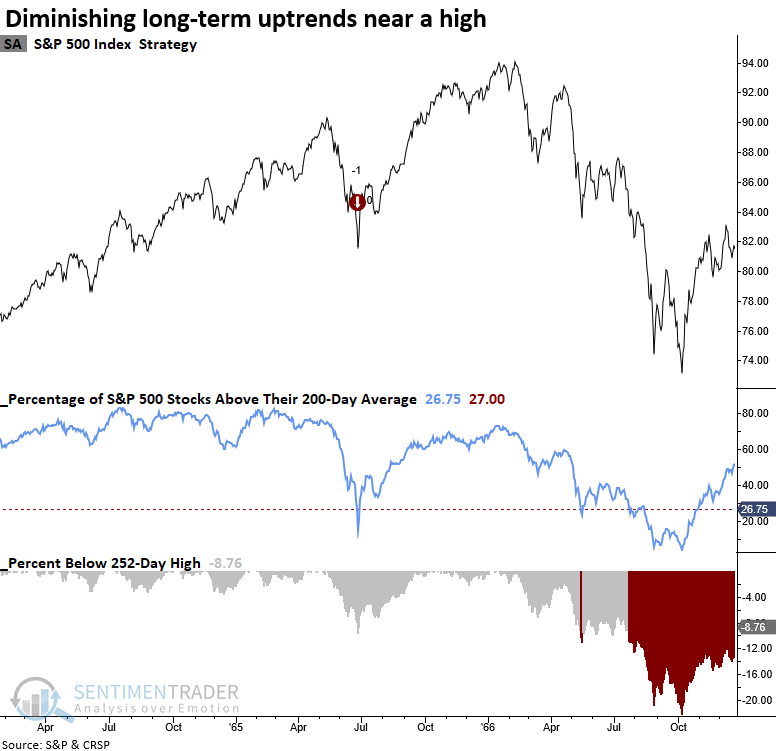

This type of divergence between the index and its member stocks has only occurred 16 other times since 1928.

Similar participation trends near a high suggest a sluggish outlook

Whenever the S&P 500 hovers within 10% of its 252-day high and less than 27% of its constituent stocks are trading above their 200-day averages, the world's most widely followed index typically encounters difficulties in the subsequent six months. Over that same time frame, the average max loss exceeded the average max gain in all but one period.

In 11 out of 16 cases, the Federal Reserve was increasing its target rate. Tightening cycles typically weigh on interest rate-sensitive stocks, resulting in a narrowing of market breadth. This time is no different.

The danger zone

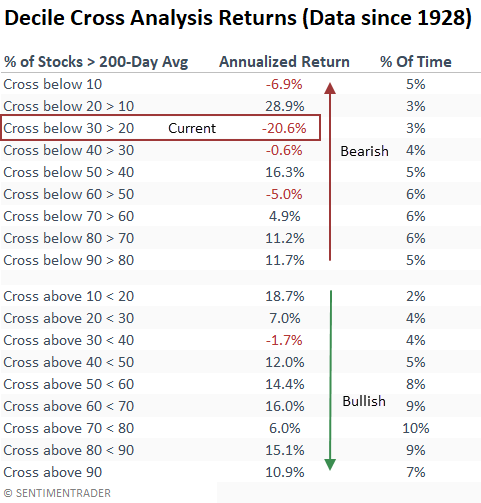

Similar to the NYSE analysis table shared on Wednesday, the annualized returns for the S&P 500 often exhibit less favorable returns when the percentage of stocks above their long-term average declines in oversold territory.

The current decile cross displays the worst annualized return outlook of any zone.

A more concerning potential outlook

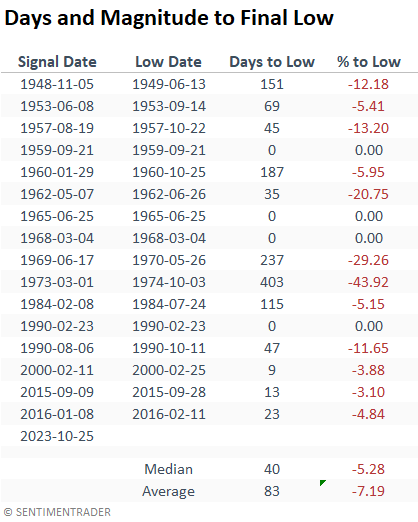

When I calculate the days and percentage change from the signal date to the low in the S&P 500, potential downside risk looks more troubling than the results in the outlook table. The instances in 1965 and 1968 are the only times the S&P 500 bottomed on the alert date and rocketed higher. While the precedents in 1959 and February 1990 were bottoms, it was within the context of an overall topping process.

Other historical chart examples

What the research tells us...

Determining the difference between a correction and the start of a bear market using market breadth indicators is a challenge. They look very similar at the outset. The more context, the better. As an increasing number of S&P 500 stocks fail to maintain a long-term uptrend, with the S&P 500 hovering within 10% of its 252-day high, all is not well with market breadth. Similar backdrops suggest the S&P 500 could struggle over the subsequent six months. For now, it's best to avoid catching the falling knife.