A S-TCTM Risk Warning Model member triggers a risk-off signal

Key points

- A specific component of the S-TCTM Risk Warning Model has triggered an alert due to an unusual concentration of new lows occurring within the Financial sector.

- Historically, when Financials dominate the new low list while the S&P 500 is near its highs, the broader market tends to suffer negative returns over the following month.

- Despite this localized warning, the broader Composite Risk Warning Model has not yet triggered, as other confirming components remain quiet.

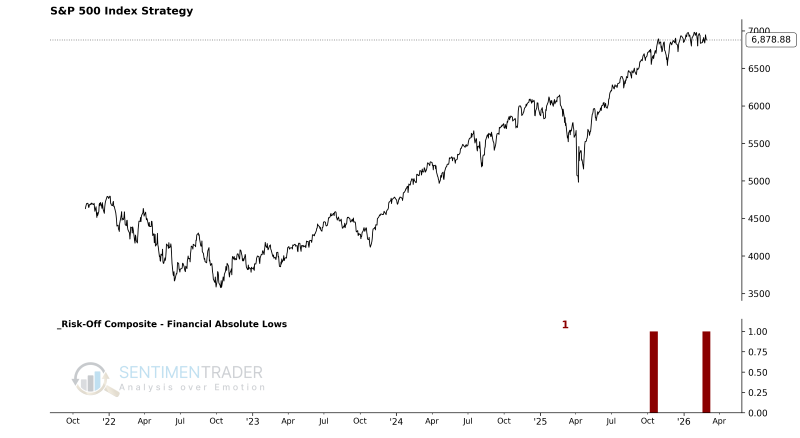

Financial sector weakness flashes a warning

Monitoring the Percentage of Financial Sector Member Lows Risk-Off Model reveals that the percentage of 63-day lows in the S&P 500 Financial sector relative to the total 63-day lows in the broader S&P 500 has exceeded 38%. Furthermore, the percentage of Financials making new 63-day lows is ≥ 12%, all while the S&P 500 Index remains within 3.0% of its 500-day high. This specific combination has triggered a risk-off signal for this individual member of the S-TCTM Risk Warning Model.

The last time this specific warning occurred was in October 2025. It was an isolated event, highlighting the principle that no single indicator or model should be used in isolation. A weight-of-the-evidence approach is always preferable.

The Financial Absolute Lows model is designed to identify when a high proportion of lows within the S&P