A major move in miners

Key points:

- Almost all gold mining stocks are above their major moving averages

- There has been a jump in miners at new highs, and not many are struggling in corrections or bear markets

- Over the past 30 years, gold miners have had great difficulty holding such impressive internal participation

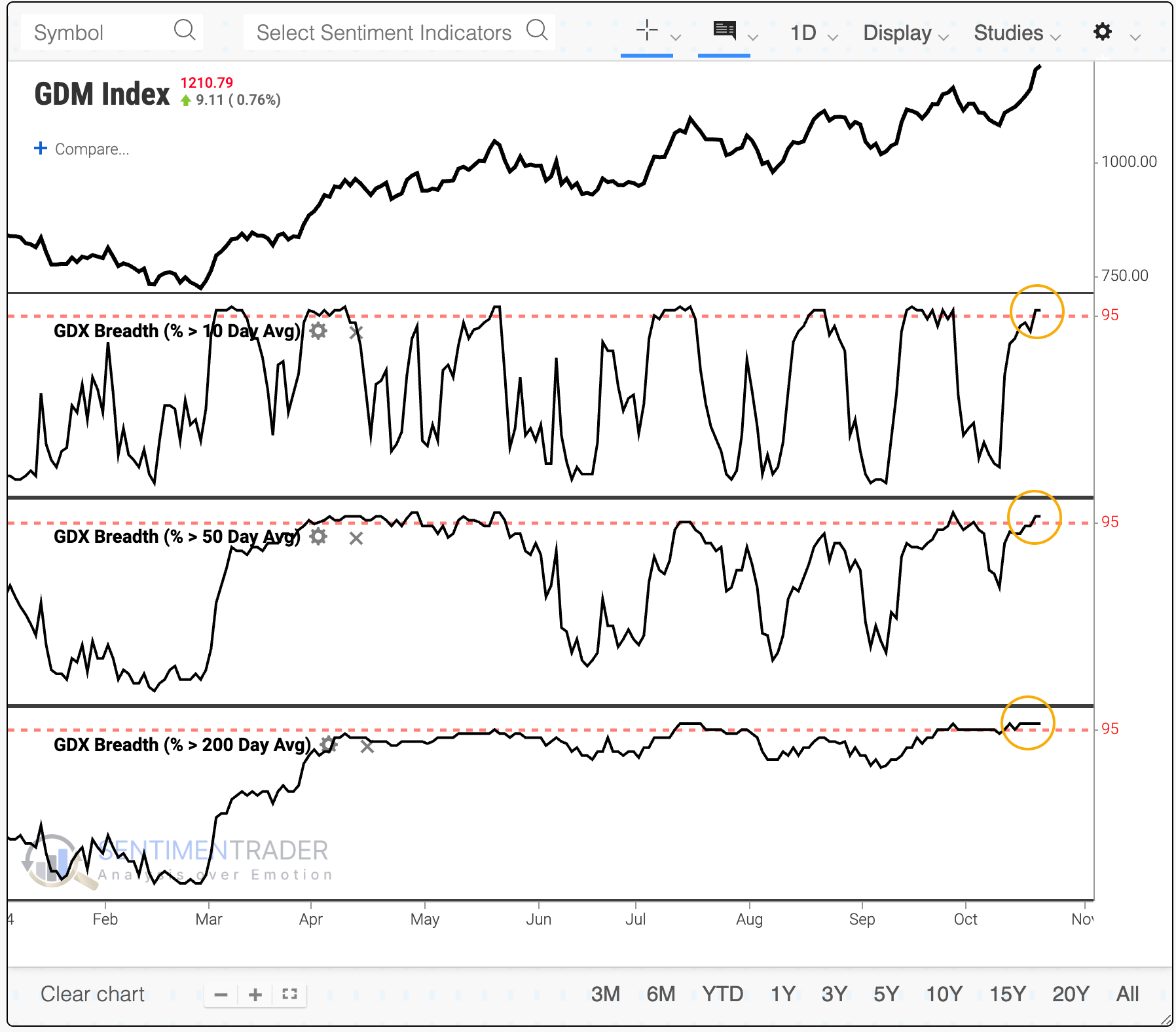

Gold miners are enjoying nearly universal uptrends

Gold has been putting in the performance of a decade. And the companies that mine the metal have, for the most part, tagged along for the ride.

The issue with those stocks, however, is that they have an inglorious history of being their own worst enemies. Investors have suffered through repeated episodes of poor capital allocation, mistimed mergers and acquisitions, and struggles with geopolitics, wildly uncertain input costs, and more mainstream business challenges.

Trying to jump on the momentum bandwagon in this sector has been fraught with risk. A few times in the past 30 years, they've enjoyed multi-year runs and rewarded investors who stayed through the volatility. The issue is that they've done so well lately that the few precedents are mostly peaks.

Virtually every gold miner is now trading above its 10-day moving average, showing a short-term boost in widespread buying interest. It's not just the short-term, though - almost all of them are above their 50-day and 200-day averages, too.

So many widespread uptrends across so many of these stocks have been a good sign for the sector over the following month, but that was pretty much it, at least consistently. Other time frames showed weak average returns with wide variability. Three signals preceded gains of more than +20% over the next six months, while four led to losses worse than -20%.

Few corrections, many new highs

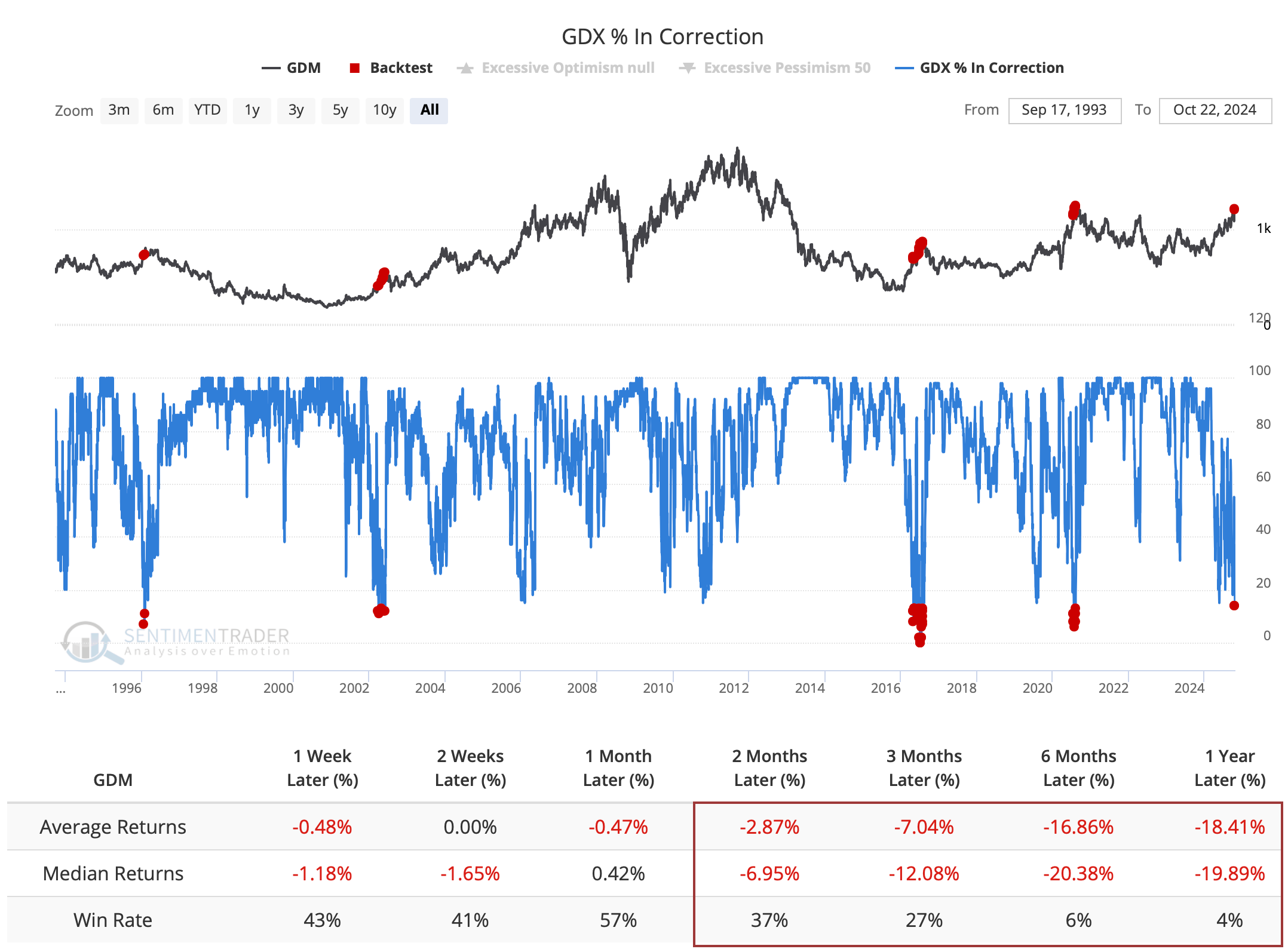

The rally over the past week, in particular, has pulled many of these stocks out of correction territory, down more than -10% from their peaks. Now, fewer than 15% of the stocks are beyond that threshold.

As we see so often in this group, similar recoveries have not been encouraging. Returns were poor across every time frame and got progressively worse the further out we looked. Six months later, the NYSE Arca Gold Miner Index was positive only 6% of the time, with a median return of -20.4%.

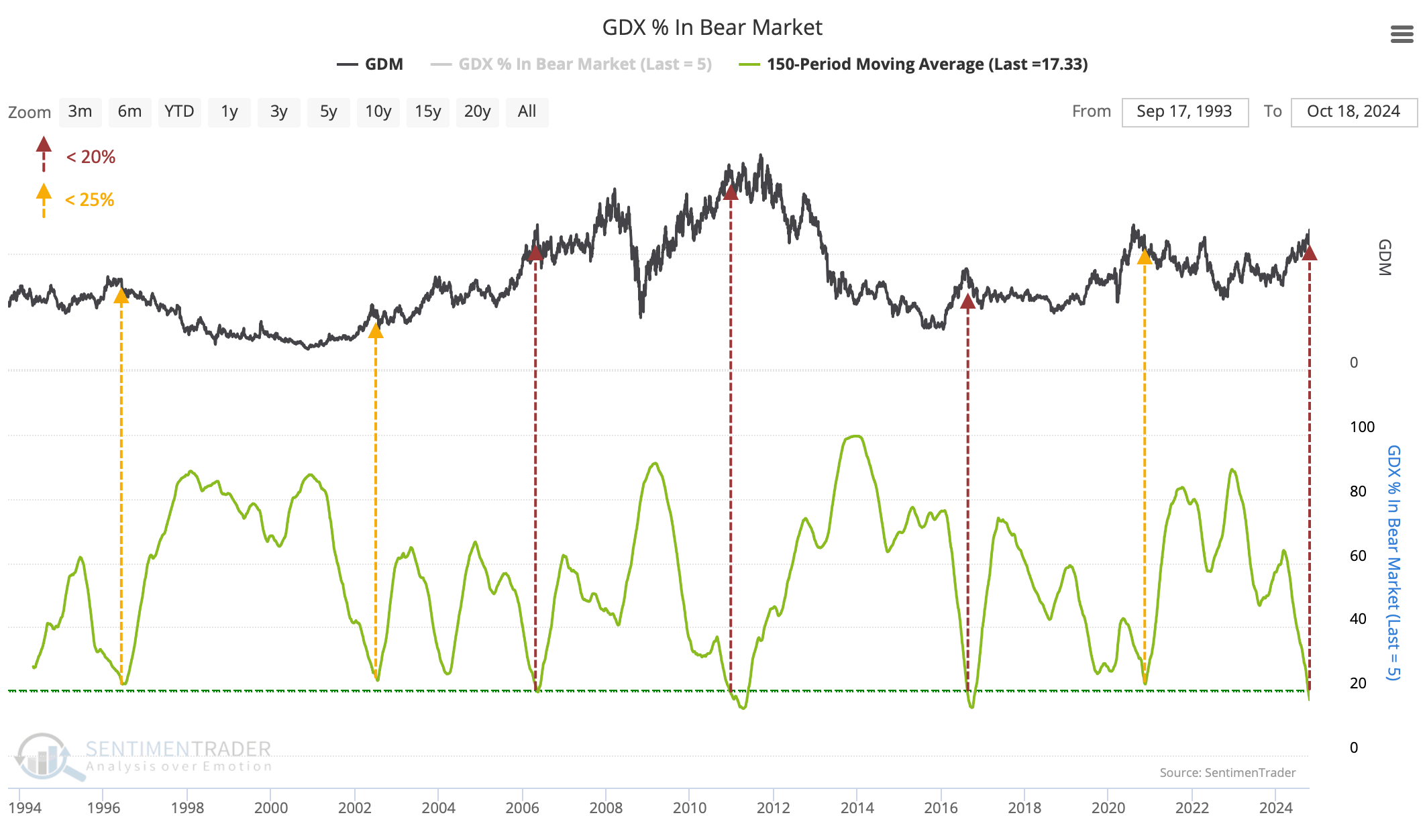

Few of the stocks are mired in bear markets, down more than -20% from their highs, and that's been the case for more than six months. An average of fewer than 20% of gold miners have been in bear markets over the past 150 sessions, among the lowest in 30 years. All three times the average got this low, miners peaked. Even when the average crossed below 25%, peaks were the norm.

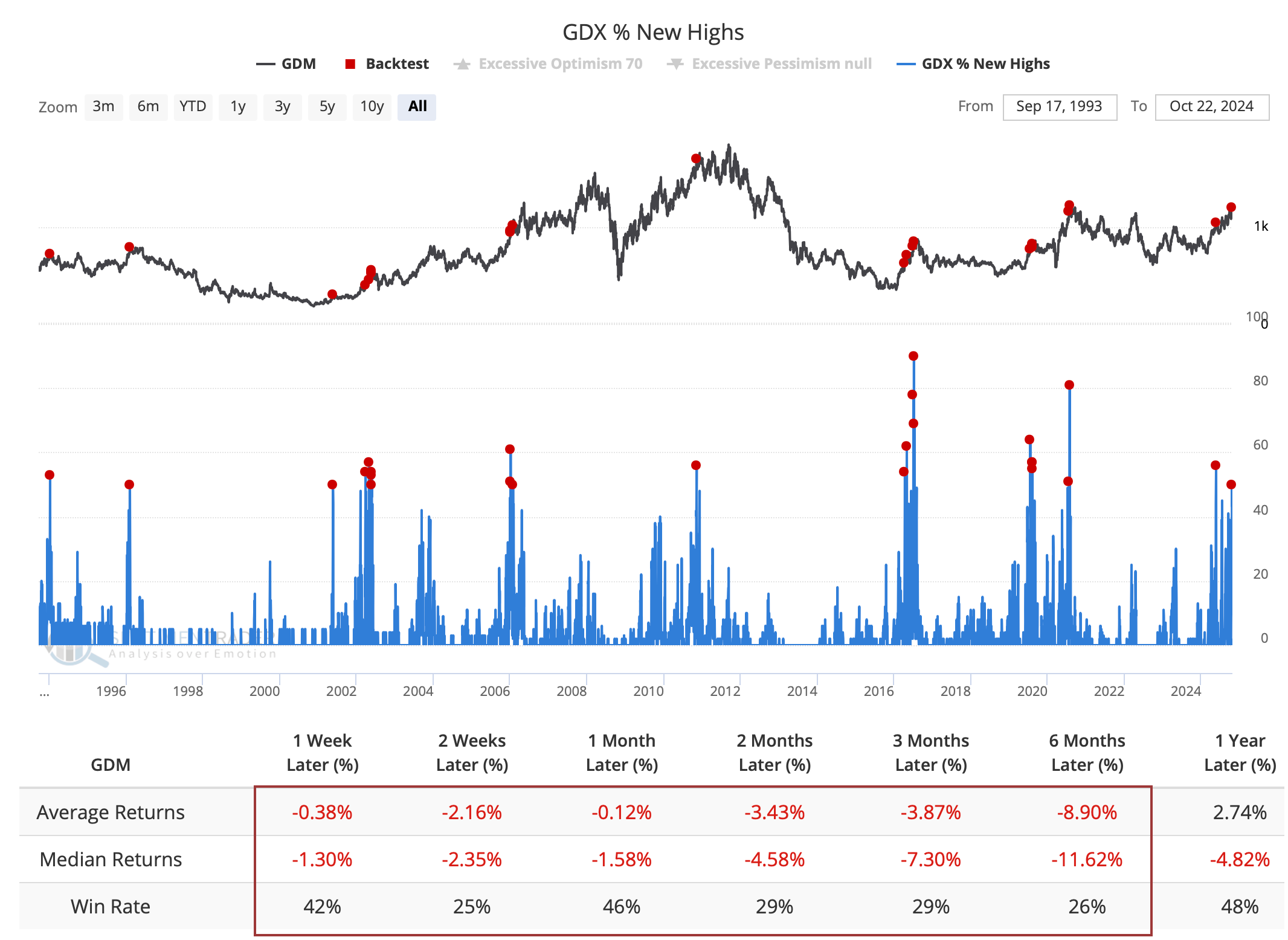

With so many of the stocks relatively close to their highs, it makes sense that we'd see a jump in the number of them actually reaching new highs, which we have. More than half of them recently hit a new high on the same day. It's no surprise, given the above, that returns were poor after similar jumps in new highs. Six months later, miners added to their gains only about a quarter of the time.

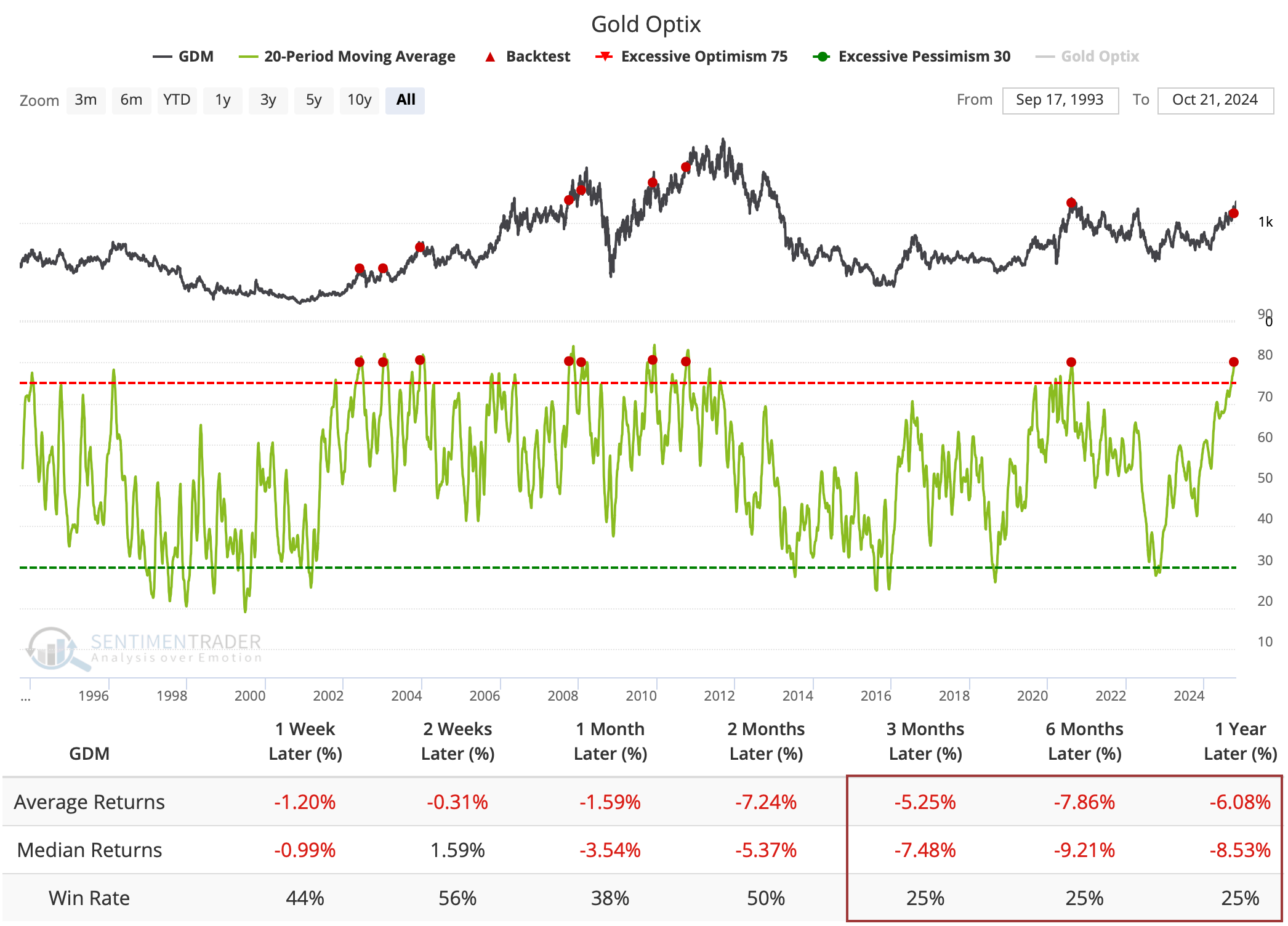

When it comes to gold itself, sentiment has become highly optimistic. A 10-day average of the Gold Optimism Index just crossed above 80%, which has preceded some tough times for miners.

What the research tells us...

As we've discussed often, gold mining stocks are kind of like Chinese equities - they suck everyone in when it looks like there has finally been a turn, then the latecomers get burned once again. It doesn't work every time, of course - every once in a decade or so, the stocks go on a massive, sustained run. But the interim rallies and rug pulls are vicious.

We don't have breadth data on gold mining stocks before the past 30 years, so the incredible run in miners in the 1970s when the stocks went up nearly 10x isn't included in any of the studies above. That could drastically change the conclusion - as Dean showed yesterday, persistent rallies in gold have been a good sign for miners during the following year, though half the signals occurred prior to the last 30 years. We tend to place more emphasis on recent history, and that recent history suggests some caution if relying on the broad participation we're seeing now to continue.