A lower-cost approach to fight the fear of missing out

Key points:

- The "Fear of missing out" (FOMO) is a real thing (so is the fear of being wrong)

- Sometimes, individuals feel they must choose between being "all in" or simply standing aside

- An options position can allow a trader to gain market exposure without a large dollar risk or commitment

Considering a favorable trend in gold

Trading is a game of money but also one of emotion. The "fear of missing out" and the "fear of being wrong" can cause investors to miss out and/or underperform. The fear of missing out can cause traders to take larger risks than they should (usually in an effort to make up for gains they believe they should have made earlier but missed out on). While risk is part of trading, managing risk properly - allocating and risking a reasonable amount on each trade - separates the winners from the losers.

The fear of being wrong can cause a trader to "sit on their hands" while an asset rallies sharply because they are afraid of, well, being wrong and losing money. Eventually, many traders give in to the desire to make a lot of money but rush in late to the game, risking more than they normally would to make up for the profits they did not make while they sat out the initial rally.

No surprise, this scenario is fraught with peril. This makes this an excellent time to invoke the following:

Jay's Trading Maxim #90: When in doubt, stay out (OR if you can't fight the urge to get in, consider a low-dollar-risk options trade-maybe you make a lot, but more importantly, you don't get your face kicked in if you're wrong).

Considering a favorable trend in gold

Everything that follows should not be considered investment advice or specific recommendations. The information is meant to serve as examples of the fear of missing out and the fear of being wrong and as one approach to avoiding these problems.

The chart below shows the rally in gold in the last year and the recent pullback.

Let's consider a trader with a $50K trading account, with $48K currently invested and $2K in cash. Our trader was bullish on gold when it initially broke out to new highs but never pulled the trigger because they were afraid of being wrong (and have been mentally "kicking themself" ever since). With gold experiencing a pullback, this trader is now motivated by FOMO and has decided to "take the plunge" so as not to miss what they think will be the next big up leg.

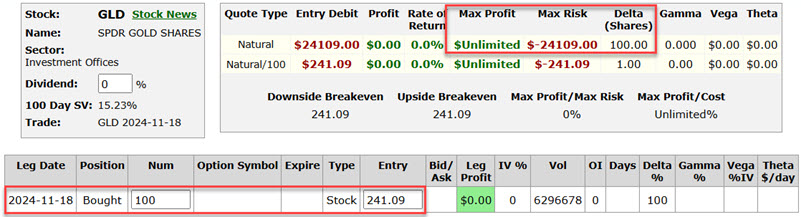

To buy 100 shares of SPDR Gold Shares (ticker GLD) at $241.09 a share will cost our trader $24,109. This represents almost 50% of their trading account. Our trader knows better than to sell nearly half of their current holdings and bet 50% of their portfolio on one security. But in a FOMO-induced moment, they decide to do just that and "take the plunge."

The screenshots below (courtesy of www.Optionsanalysis.com) show the particulars for the long 100-shares of the GLD ETF position and the "risk curves" (i.e., the expected $P/L for the position as of a given price for GLD shares).

Note that the risk "curves" are a straight line. This is because, for every $1 GLD gains or losses, the 100-share stock position will gain or lose $100. Note that "Delta" is a term used in option trading to show the "stock equivalent position." No surprise then, that a position of long 100 shares of stock has a Delta of 100.

If our trader places a stock loss at $215, they will risk $2,609, or 5.2% of their trading capital.

An option alternative

One possible alternative is the following:

- Buy 2 GLD Feb21 2025 242 calls @ $8.25

The screenshots below display the particulars for this position and the risk curves. Note that the risk curves change as time passes. This is due to "time decay" (i.e., options lose time premium as time passes, with time decay accelerating as expiration nears).

- The cost to enter this position (and the maximum dollar risk) for a 2-lot is $1,650 (versus $24,109 to buy 100 shares of GLD, or 6.8% as much)

- This represents a worst-case loss of 3.3% of a $50K trading account (this would only occur if the options were held until expiration and expired worthless)

- The breakeven price at expiration is $250.25 (strike price of 242 plus the premium of 8.25)

- If this position is held until expiration, the trade would show a profit if GLD is above $250.25

- If GLD is at $242 or lower at expiration, the trade will show a loss of -$1,650

- Between $242 and $250, the position will show a return of somewhere between -$1,650 and $0

Let's examine the "Greek" option values more closely. Note that these values are not static and can and will change over time.

The position has a:

- "Delta" of 111.06 (that means that it will behave like a long 111 shares of GLD position)

- "Gamma" of 4.362 tells us that the position will gain or lose 4.36 Deltas for each $1 price movement by GLD shares

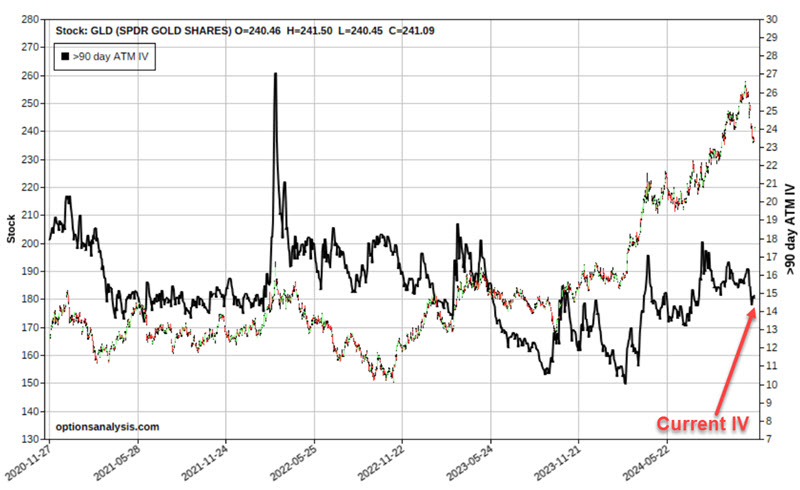

- "Vega" of $97.16 tells us the position will gain or lose $97.16 for each one-point change in implied volatility for the February 242 call option. Note the current IV is 14.94%. The status of 90+ day GLD option IV appears in the chart below versus its historical range (black line).

- "Theta" of -$10.56 tells us that this position will lose $10.56 daily due solely to time decay. This also tells us that the sooner GLD starts to rally (assuming it does at all), the better

Comparing share position to option position

Everything in trading involves tradeoffs. The good news in this example is that an option trader can assume a position with a Delta of 111 (i.e., roughly equivalent to holding 111 shares of GLD) for $1,650 instead of spending $24,109 to buy 100 shares of GLD.

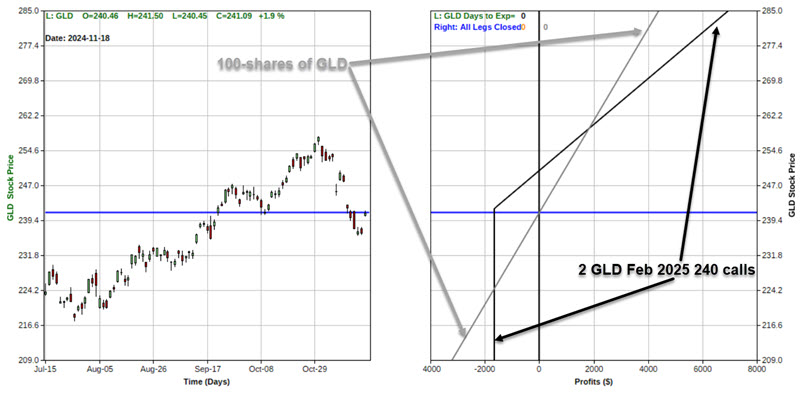

The screenshots below overlay the two positions.

- Above $260 a share, the option trade will continue to gain more than the 100-share position (because the option trade continues to gain Deltas for each $1 rise in GLD price).

A 2-standard deviation move would bring GLD shares to $280 a share. At this point, the option position would show a profit of roughly $5,950 versus $3,890 for the 100-share position. So, the option position offers significantly greater dollar profit potential BUT only if GLD actually rallies significantly.

- The bad news is that between roughly $225 and $260 a share, the option position will either experience a smaller gain or a larger dollar loss than the 100-share position. This is the effect of time decay and is a risk the trader must accept when choosing the option position.

- Below $240 a share, the option position loss is capped at a maximum of $1,650.

- Below roughly $225 a share, the 100-share position loss will continue to grow by $100 for each $1 decline in the price of GLD shares.

What the research tells us…

So, is the option position a better trade? It depends on how one defines "better." The good news is the smaller dollar commitment ($1,650 instead of $24,109), the greater profit potential (if GLD does, in fact, rally sharply), and the limited risk. The bad news is that if GLD does not rally significantly over the next three months, the option trade can suffer a larger dollar loss than the 100-share position.

Still, the overarching point is that a simple option position can help a trader gain exposure to an asset without making a major dollar commitment.