A look at the key relative trends in the market

Key points

- There are no permanent relationships in the financial markets

- No security, sector, index, or commodity ever has a permanent edge over another

- Alert investors often gain an advantage by monitoring key relationships

- Here, we look at the status of crucial market relationships to help highlight areas of strength and weakness

What relative strength charts can tell us

All charts below are weekly relative strength charts courtesy of Stockcharts. In other words, these charts do not show the actual price action of a single security. Instead, they compare the relative price performance of two different securities.

The black and red line displays the weekly relative performance trend, so a rising line means that the first security listed in the comparison is outperforming and vice versa. Each chart also shows a 52-week simple moving average in blue.

If the relative strength line is above the blue moving average line and/or the moving average line is rising, it's more confirmation that the first security is outperforming.

Please note that I do not use these charts' actions to generate automatic buy or sell signals. I use them strictly as a starting point in finding securities exhibiting significant strength (or weakness). The primary goal is to find opportunities to trade with the trend in the more robust security.

- A relative strength line making a new high above a rising 52-week moving average suggests further investigation for a buying opportunity in the first security listed.

- A relative strength line making a new low below a falling 52-week moving average suggests further investigation for a buying opportunity in the second security listed.

Stocks vs. Bonds

Comparing: VTI vs. AGG (Vanguard Total Stock Market ETF vs. iShares Core U.S. Aggregate Bond ETF)

Recent Action: The RS line moved back above its 52-week MA in early 2023; however, it is also unchanged from 15 months ago.

Current trend: Bond: Both stocks and bonds topped out in the fourth quarter of 2021, and both are struggling to rally off of their October 2022 lows. Stocks have once again regained the relative lead for the moment, but the jury is still out going forward.

Commodities versus U.S. Stocks

Comparing: DBC vs. VTI (Invesco DB Commodity Tracking Fund vs. Vanguard Total Stock Market ETF)

Recent Action: Commodities had a terrific run into mid-2022. But once inflation peaked, commodities backed off significantly while stocks have staged a rally since October.

Current Trend: The RS line has dropped back below the 52-week MA, thus favoring stocks over commodities. However, the 52-week MA has yet to roll over. As long as stock indexes remain above their 200-day average and inflation continues to cool off, there is not much of a catalyst to favor commodities.

Value vs. Growth

Comparing: VTV vs. VUG (Vanguard Value ETF vs. Vanguard Growth ETF)

Recent Action: Value significantly outperformed growth from November 2021 to the end of 2022. During the first quarter of 2023, growth has attempted to stage a comeback, as evidenced by a sharp drop in the RS line.

Current Trend: Despite the relative rally in growth so far in 2023, the RS line remains above a rising 52-week average. The value factor remains in favor until the RS line drops below the moving average.

Small-Cap Value vs. Large-Cap Growth

Comparing: IJS vs. IWF (iShares S&P Small-Cap 600 Value ETF vs. iShares Russell 1000 Growth ETF)

Recent Action: This chart compares the performance of two very different types of companies - small-cap value vs. large-cap growth. The RS line bottomed in late 2020 and has twice bumped its head at the 0.44 level.

Current Trend: As long as the RS line remains above a rising 52-week MA, the trend still favors small-cap value over large-cap growth. But a move above 0.44 will ultimately be needed to sustain this as a longer-term trend.

Small-Cap vs. Large-Cap

Comparing: IWM vs. SPY (iShares Russell 2000 ETF vs. SPDR S&P 500 ETF)

Recent Action: Now, let's focus solely on the size factor. This chart compares the performance of small-cap value vs. large-cap. After a significant swing back and forth, small-caps have been creeping higher relative to large caps since early 2022.

Current Trend: Large-caps significantly outperformed from 2009 into early 2020. History suggests that momentum should swing back to small-caps, and small-caps are trying to take the lead. For the moment, small-caps hold an ever so slight advantage.

Mid-Cap vs. Large-Cap

Comparing: IJH vs. SPY (iShares Core S&P Mid-Cap ETF vs. SPDR S&P 500 ETF)

Recent Action: While most focus on the battle between large-cap and small-cap, the reality is that since 1981 mid-caps have outperformed both small and large-caps (My theory is that the mid-cap space contains many formerly small-cap companies on their way to becoming large-cap companies, so that is where most of the growth occurs). So, let's take a closer look at mid-caps.

Current Trend: The RS line has been trending higher in fits and starts since early 2022 (indicating that mid-caps have held up better than large-caps in a bearish market environment). The RS line is presently in an uptrend above a rising 52-week MA. This suggests that investors looking to jump into the market may be wise to look more closely at mid-cap stocks.

Mid-Cap vs. Small-Caps Comparing: IJH vs. IWM (iShares Core S&P Mid-Cap ETF vs. iShares Russell 2000 ETF)

Comparing: IJH vs. IWM (iShares Core S&P Mid-Cap ETF vs. iShares Russell 2000 ETF)

Recent Action: While small-caps are generally the darling of the "nonlarge cap" crowd, mid-caps have held up much better. The RS line bottomed in early 2021 and has been trending steadily higher since (i.e., favoring mid-caps over small-caps).

Current Trend: The RS line has backed off since the end of 2022, meaning small-caps have slightly outperformed so far this year. However, as long as the RS line in this chart and in the previous mid-cap vs. large-cap chart remains above a rising 52-week MA, the mid-caps remain the place to be.

U.S. Stocks vs. International

Comparing: VXUS vs. VTI (Vanguard Total International ETF vs. Vanguard Total Stock Market ETF)

Recent Action: Historically, there has been a back-and-forth that takes place between U.S. stocks in international stocks. Since roughly 2007, U.S. stocks have vastly outperformed international - to the point that there was almost no reason to hold international stocks. That trend may be changing and deserves special attention as a reversal in trend could easily last for five to ten years or more.

Current Trend: The RS line has popped above the 52-week MA (favoring international stocks to an extent not seen in years) ], and the 52-week MA is attempting to trend higher. This recent strength may be just another fake-out favoring international stocks. However, after 15 years of favoring U.S. stocks, it is inevitable that, at some point, the tide will turn. So this relationship should be watched closely.

Low Volatility vs. Momentum

Comparing: SPLV vs. MTUM (Invesco S&P 500 Low Volatility ETF vs. iShares MSCI USA Momentum Factor ETF)

Recent Action: Defensive, low-volatility stocks tend to lead during a bear market. The relationship between low-volatility stocks and momentum stocks is one way to track the "risk on, risk off" nature of the market. The market went heavily risk on from the Covid low in 2020 into early 2021. It has been chiefly risk off ever since.

Current Trend: The RS line has recently dropped slightly below the 52-week MA, and the 52-week MA has flattened out. If the overall stock market is to turn bullish, we would expect to see the RS line and the 52-week MA here begin to trend lower.

Consumer Staples vs. Consumer Discretionary

Comparing: XLP vs. XLY (Consumer Staples Select Sector SPDR Fund vs. Consumer Discretionary Sector SPDR Fund)

Recent Action: This is another "defensive versus momentum" risk on/risk off measure. In a bear market (particularly during periods of high inflation and/or higher interest rate), consumer staples tend to outperform consumer discretionary (and vice versa).

Current Trend: This risk on/risk off relationship should be watched closely. With the RS line above a rising 52-week MA, the trend is still deemed "risk off." But a break below the 52-week MA would strongly suggest that the bulls are taking charge.

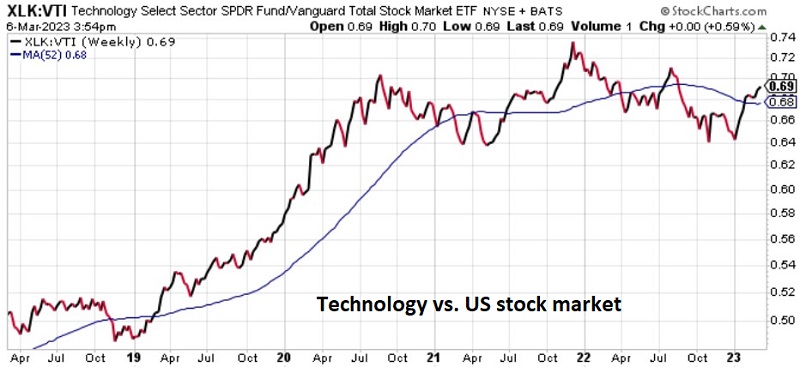

Technology vs. U.S. Stocks

Comparing: XLK vs. VTI (Technology Select Sector SPDR Fund vs. Vanguard Total Stock Market ETF)

Recent Action: With very little fanfare, the technology sector has gained strength relative to the overall market so far in 2023.

Current Trend: This is another risk on/risk off relationship (i.e., technology stocks tend to outperform during bull markets). The RS line has crept back above the 52-week MA. If this trend can continue higher, it would be a positive sign for the overall stock market. For now, note that the 52-week MA has yet to turn higher.

Energy vs. U.S. Stocks

Comparing: XLE vs. VTI (Energy Select Sector SPDR Fund vs. Vanguard Total Stock Market ETF)

Recent Action: After years of severe underperformance and a severe decline into late 2020, traditional Energy (Oil & Gas) was the undisputed leader into late 2022. In recent months the RS line has backed off of its highs.

Current Trend: There is always a lot of "chatter" that the "leading sector" is about to flame out. Nevertheless, as long as the RS line holds above a rising 52-week MA, the trend remains positive for energy.

Traditional Energy vs. Clean Energy

Comparing: XLE vs. QCLN (Energy Select Sector SPDR Fund vs. First Trust NASDAQ Clean Edge Green Energy Index Fund)

Recent Action: The clean energy sector was all the rage into early 2021. Since then, it's been oil & gas leading the way.

Current Trend: All the talk in recent years has been about how "clean energy" will replace traditional (fossil fuel-based) energy in the years ahead. And that is possible. But for investors looking to make money in stocks, it is essential to recognize the trend and to ride it for as long as possible. With the RS line in the chart above still holding above a rising 52-week MA, the trend is still favoring traditional energy at present.

Real Estate versus US Stocks

Comparing: IYR vs. VTI (iShares U.S. Real Estate ETF vs. Vanguard Total Stock Market ETF)

Recent Action: The real estate sector versus the broader stock market topped out in late 2019 and has yet to recover.

Current Trend: The RS line remains above its low in December 2020 but has shown no signs of strength. With the RS line floundering below a declining 52-week MA, the real estate sector remains weak and unattractive, except perhaps from a contrarian point of view.

Base metals vs. precious metals

Comparing: DBB vs. DBP (Invesco DB Base Metals vs. Invesco DB Precious Metals Fund)

Recent Action: Precious metals vastly outperformed from 2019 into mid-2020. For the next 18 months, base metals strongly outperformed. Since then, the trend has turned slightly back in favor of precious metals (i.e., a lower RS line and a declining 52-week MA.

Current Trend: Thanks in part to the cooling off of inflation, there is not much of anything constructive going on in the metals sector of late - industrial or precious metals. With the RS line below a declining 52-week MA, the trend presently favors precious metals. However, both gold and silver attempted to rally into early 2023 and were both soundly rebuffed.