A historically bad 50 day stretch for Emerging Markets

Key points:

- A rising dollar and generally bad equity market have punished emerging markets badly

- A couple of breadth indicators for those stocks show extremes rarely exceeded in nearly 30 years

- The stocks had a consistent tendency to rebound in the months following similar readings

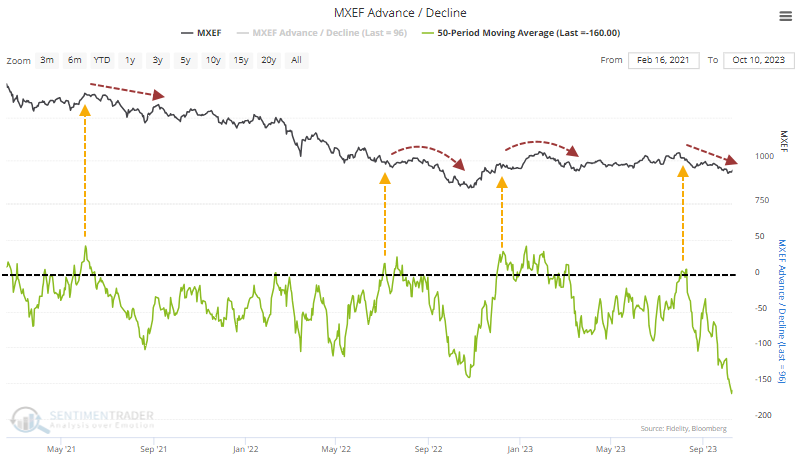

Emerging market stocks have had a bad 50-day stretch

We saw last week that some U.S. sectors have been hit hard. The average stock among the most defensive sectors has been battered, pushing long-term internal breadth metrics toward historic lows.

It hasn't just been certain U.S. pockets that have suffered. Thanks to what had been an incessant uptrend in the dollar, emerging market stocks have also been sold aggressively.

Since the MSCI Emerging Markets Index peak in February 2021, whenever breadth has turned positive over a 50-day period, rallies just about ran out of juice, if the index had managed to rally at all.

They got slapped again after the 50-day average advance-decline indicator turned positive in early August, and it has since retreated to one of the lowest levels in decades.

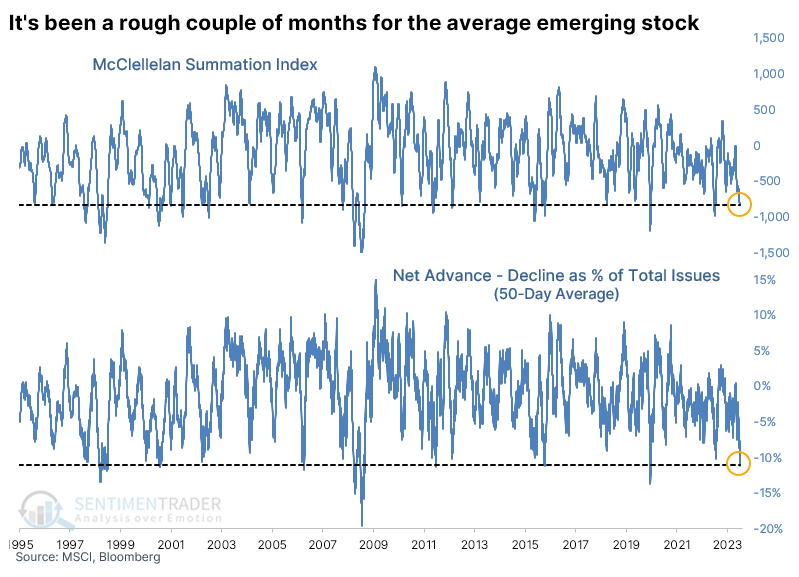

The chart below shows this 50-day average net breadth metric expressed as a percentage of the total number of stocks in the index. It has surpassed -10%, one of the most extreme figures in nearly 30 years. That woeful stretch has also pushed the McClellan Summation Index for these stocks to an extremely low level. Both indicators rank in the bottom 5% of all days since 1995.

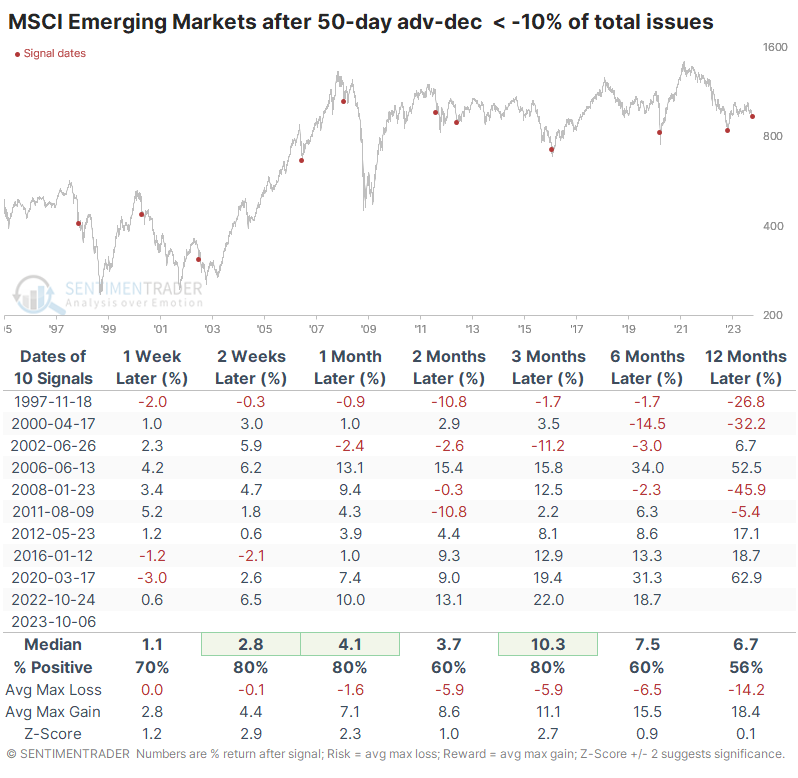

Big negative extremes in breadth mostly preceded rebounds

After the 50-day net breadth indicator surpassed -10% of issues, the Emerging Markets Index tended to rally consistently for up to three months later. There was only one loss larger than -2% over the next three months, though a few morphed into painful longer-term losses. The last four signals were superb for bulls.

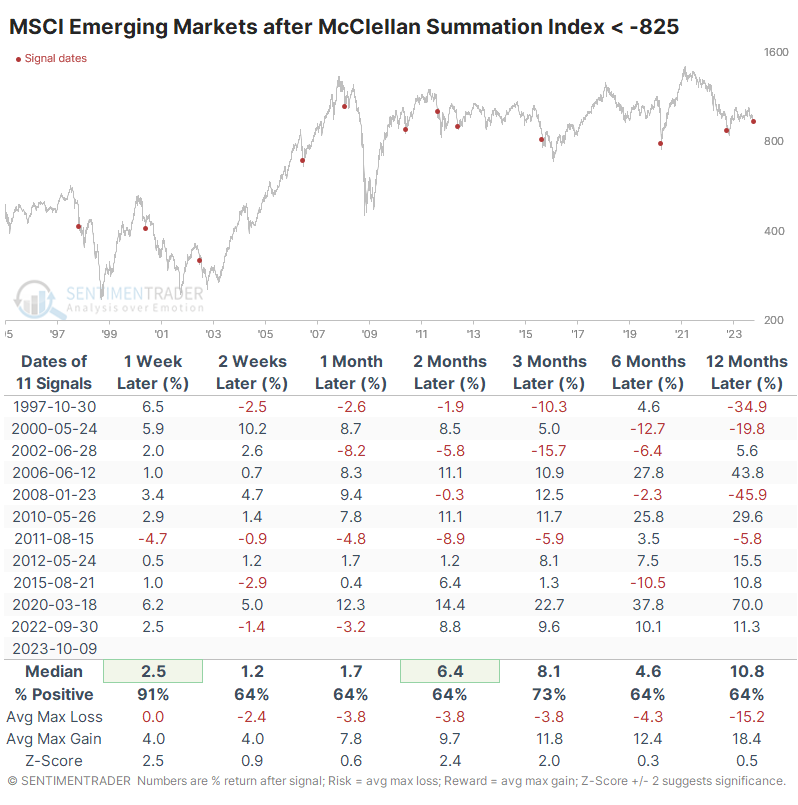

It's a similar but not quite as compelling picture when looking at the extreme in the Summation Index. Emerging markets rallied less often over the medium term, with generally lower median returns but a better risk/reward skew.

What the research tells us...

Movements in the U.S. dollar heavily influence returns in emerging markets. Over the past 50 sessions, the dollar has risen more than 4%, and emerging markets tanked more than -10%. Over the past 30 years, the 50-day rolling correlation between those returns is consistently - but not perfectly - negative. Optimism on the dollar has been high and is receding, which should be a tailwind for emerging markets if it continues.

If that's enough to push the stocks higher for more than a few sessions, it should turn the longer-term breadth stats from their severely oversold conditions. A curling up of these measures has been a fairly reliable sign that a medium-term rally was underway.