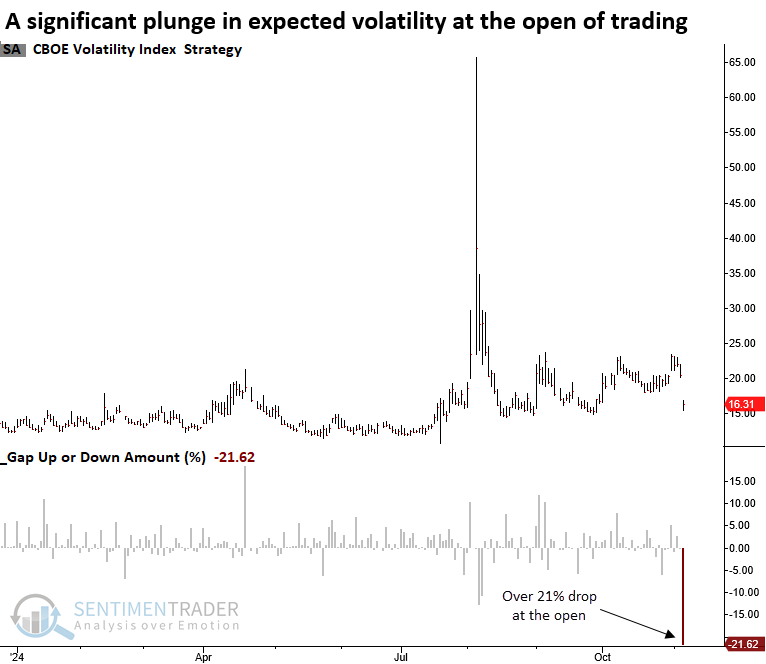

A historic plunge in the fear gauge

Key points:

- The Volatility Index (VIX) plunged by more than 21% to open today's trading session

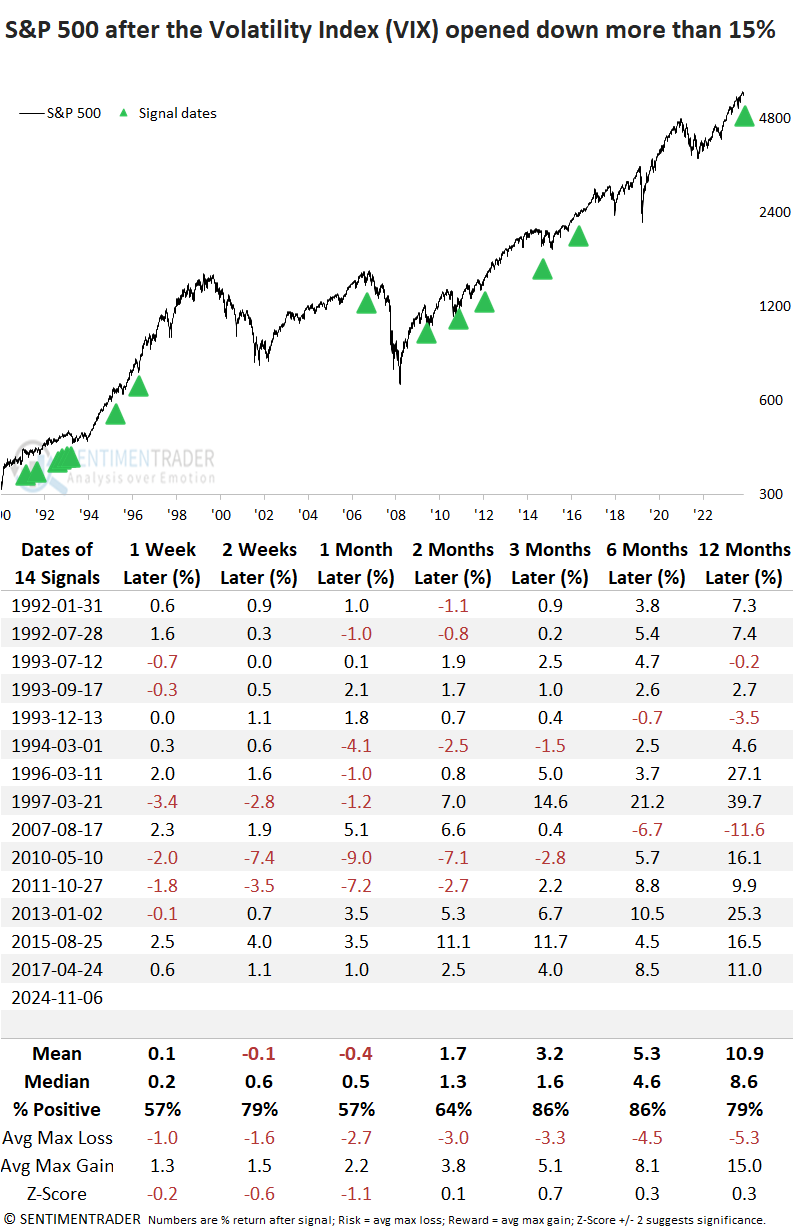

- Similar contractions in the fear gauge saw the S&P 500 rally 86% of the time over the next three months

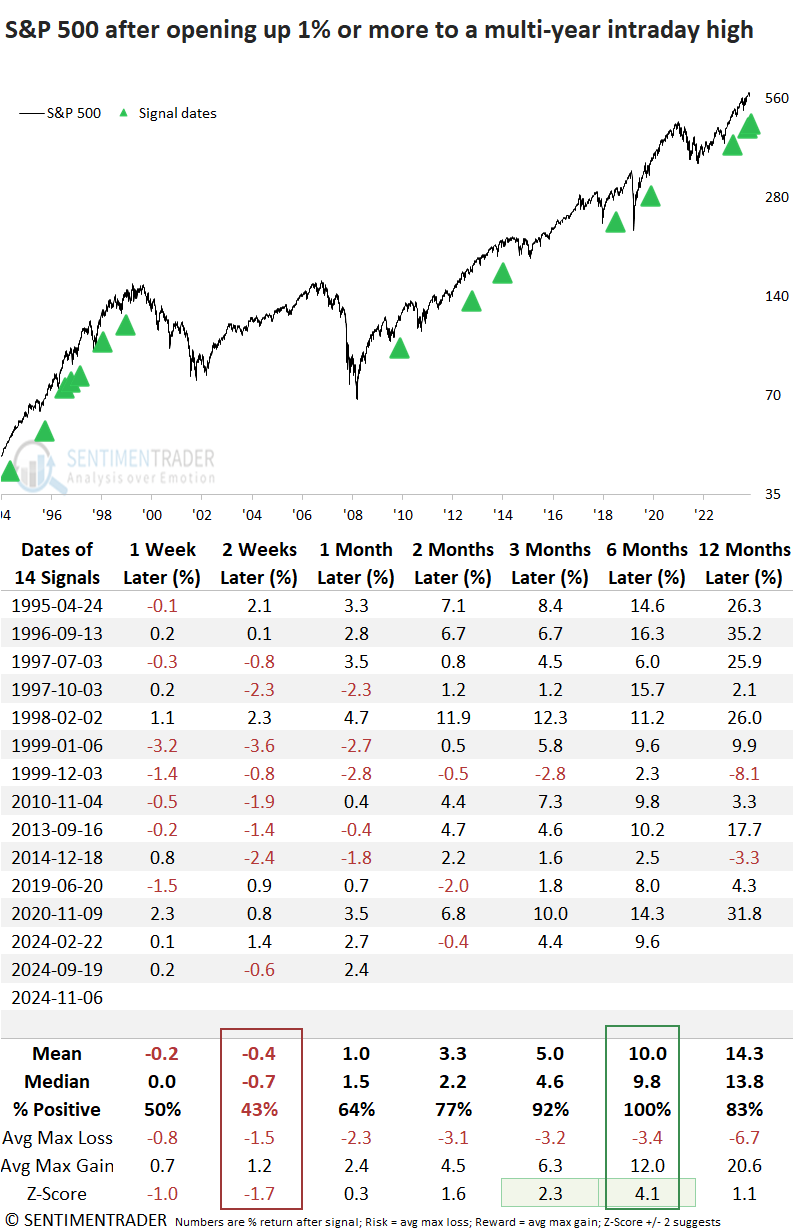

- The S&P 500 ETF (SPY) opened 2% higher to a new intraday all-time high

- Comparable gaps tended to see a short-term consolidation, followed by a rally 100% of the time

The fear gauge plummeted as election uncertainty is no longer a concern

My colleague Jay Kaeppel published a research report highlighting the seasonal trend for the Volatility Index in November, particularly during presidential election years. It suggested that volatility should decrease, a scenario that often supports stock performance.

Following the election's conclusion, the VIX adhered swiftly to its seasonal pattern, dropping over 21% as markets opened on Wednesday-a magnitude of decline seen only four other times since 1992, when intraday data became available.

To increase the sample size, I lowered the VIX drop from 21% to 15%.

Comparable plunges in volatility preceded a positive outlook for the S&P 500

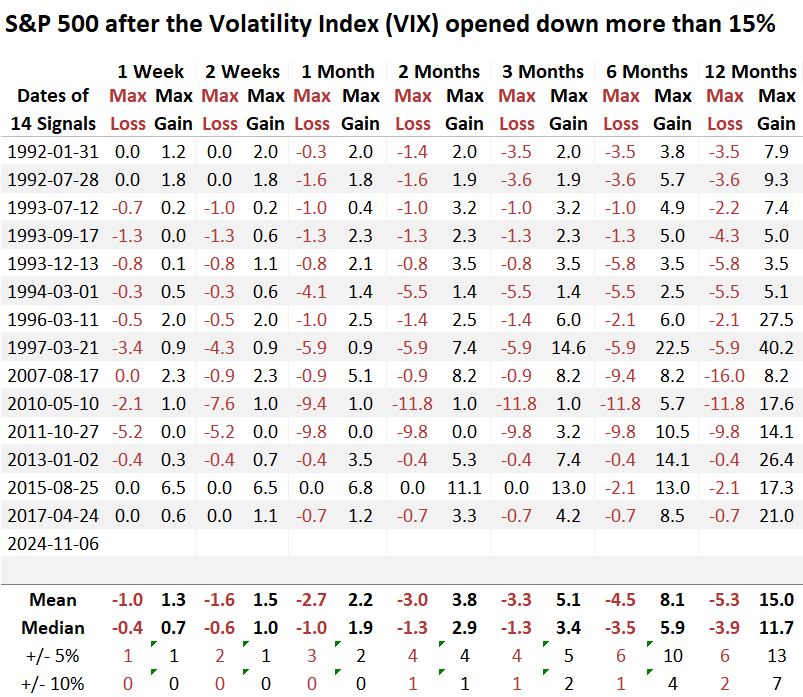

Whenever the Volatility Index (VIX) opened down 15% or more from the previous day's close, the S&P 500 showed a solid tendency to rally, advancing 86% of the time over the subsequent three and six months.

In the ensuing six months, the S&P 500 incurred three maximum losses of around 10%, each linked to events like the GFC, Flash Crash, and the European Debt Crisis-scenarios markedly different from the current backdrop.

Stocks surge higher following the conclusion of the election

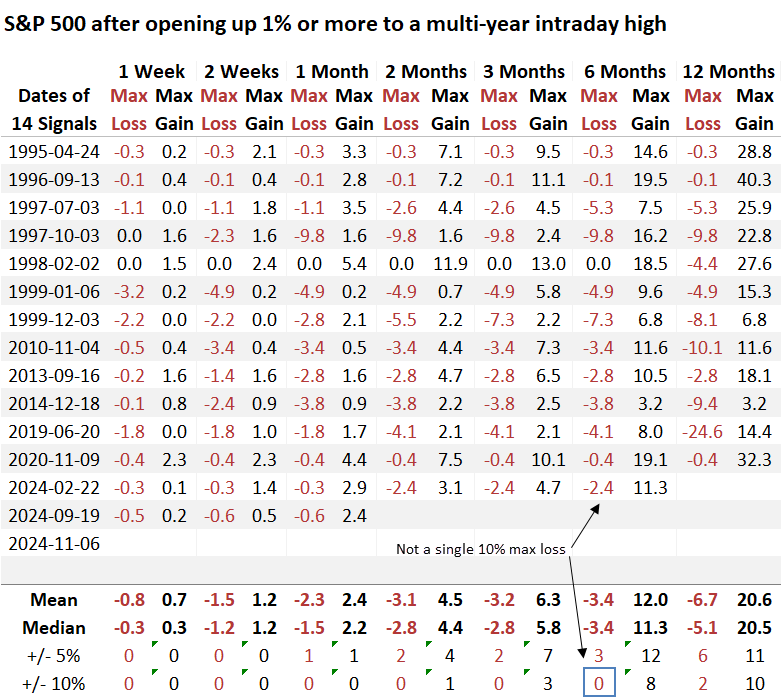

The S&P 500 ETF (SPY) increased by over 2% at the open on Wednesday to a new intraday all-time high. When I scanned the ETF for similar precedents, I found only one other instance since 1993, occurring in November 2020, four days after the previous presidential election.

Similar surges to a high preceded a rally every time

To increase the sample size, I adjusted the gap-up amount from 2% to 1%, which resulted in 14 instances. Although the S&P 500 struggled over the next two weeks, potentially indicating buyer fatigue, it achieved gains without exception over the subsequent six months.

In the following six months, just three occurrences experienced a maximum loss of over 5%, with none surpassing 10%.

What the research tells us...

Following Tuesday's election conclusion, the Volatility Index (VIX) experienced a sharp plunge, signaling a shift towards a lower volatility regime, which tends to benefit stocks. Investors, relieved from the uncertainty of the election cycle, bought stocks, driving the S&P 500 up over 2% at the open to an intraday record high. Similar precedents resulted in a 100% win rate for the S&P 500 over the next six months, which dovetails nicely with the favorable seasonal period for stocks. The year-end performance chase could get interesting.